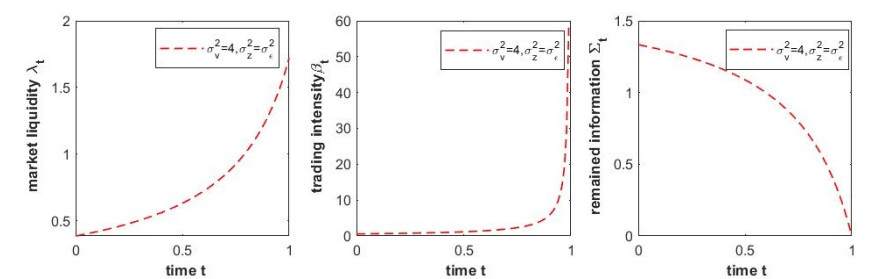

In this paper, a continuous-time insider trading model is investigated in which an insider is risk-seeking and market makers may receive partial information on the value of a risky asset. With the help of filtering theory and dynamic programming principle, the uniqueness and existence of linear equilibrium is established. It shows that (ⅰ) as time goes by, the residual information decreases, but both the trading intensity and the market liquidity increases, and (ⅱ) with the partial observation accuracy decreasing, both the market liquidity and the residual information will increase while the trading intensity decreases. On the whole, the risk-seeking insider is eager to trade all the trading period, and for market development, it is necessary to increase the insider's risk-preference behavior appropriately.

Citation: Kai Xiao. Risk-seeking insider trading with partial observation in continuous time[J]. AIMS Mathematics, 2023, 8(11): 28143-28152. doi: 10.3934/math.20231440

In this paper, a continuous-time insider trading model is investigated in which an insider is risk-seeking and market makers may receive partial information on the value of a risky asset. With the help of filtering theory and dynamic programming principle, the uniqueness and existence of linear equilibrium is established. It shows that (ⅰ) as time goes by, the residual information decreases, but both the trading intensity and the market liquidity increases, and (ⅱ) with the partial observation accuracy decreasing, both the market liquidity and the residual information will increase while the trading intensity decreases. On the whole, the risk-seeking insider is eager to trade all the trading period, and for market development, it is necessary to increase the insider's risk-preference behavior appropriately.

| [1] |

S. Baruch, Insider trading and risk aversion, J. Financ. Mark., 5 (2002), 451–464. http://dx.doi.org/10.1016/S1386-4181(01)00031-3 doi: 10.1016/S1386-4181(01)00031-3

|

| [2] |

K. Cho, Continuous auctions and insider trading: uniqueness and risk aversion, Finance Stochast., 7 (2003), 47–71. http://dx.doi.org/10.1007/s007800200078 doi: 10.1007/s007800200078

|

| [3] | F. Gong, D. Zhou, Insider trading in the market with rational expected price, arXiv: 1012.2160. |

| [4] |

A. Kyle, Continuous auctions and insider trading, Econometrica, 53 (1985), 1315–1335. http://dx.doi.org/10.2307/1913210 doi: 10.2307/1913210

|

| [5] | Z. Li, C. Liang, Z. Tang, CEO social media presence and insider trading behavior, SSRN, in press. http://dx.doi.org/10.2139/ssrn.3532495 |

| [6] |

B. Lim, A risk-averse insider and asset pricing in continuous time, Management Science and Financial Engineering, 19 (2013), 11–16. http://dx.doi.org/10.7737/MSFE.2013.19.1.011 doi: 10.7737/MSFE.2013.19.1.011

|

| [7] | R. Lipeser, A. Shiryaev, Statistic of Random process II: applications, Berlin: Springer, 2001. http://dx.doi.org/10.1007/978-3-662-10028-8 |

| [8] | G. Nunno, J. Corcuera, B. Øksendal, G. Farkas, Kyle-Back's model with Levy noise, Preprint series. |

| [9] |

K. Xiao, Y. Zhou, Insider trading with a Random deadline under partial observations: maximal principle method, Acta Math. Appl. Sin. Engl. Ser., 38 (2022), 753–762. http://dx.doi.org/10.1007/s10255-022-1112-6 doi: 10.1007/s10255-022-1112-6

|

| [10] |

K. Xiao, Y. Zhou, Linear Bayesian equilibrium in insider trading with a random time under partial observations, AIMS Mathematics, 6 (2021), 13347–13357. http://dx.doi.org/10.3934/math.2021772 doi: 10.3934/math.2021772

|

| [11] | J. Yong, X. Zhou, Stochastic controls, New York: Springer, 2012. http://dx.doi.org/10.1007/978-1-4612-1466-3 |

| [12] |

D. Zhou, F. Zhen, Risk aversion, informative noise trading, and long-lived information, Econ. Model., 97 (2021), 247–254. http://dx.doi.org/10.1016/j.econmod.2021.02.001 doi: 10.1016/j.econmod.2021.02.001

|

| [13] |

Y. Zhou, Existence of linear strategy equilibrium in insider trading with partial observations, J. Syst. Sci. Complex., 29 (2016), 1281–1292. http://dx.doi.org/10.1007/s11424-015-4186-x doi: 10.1007/s11424-015-4186-x

|

Figures(2)

Kai Xiao. Risk-seeking insider trading with partial observation in continuous time[J]. AIMS Mathematics, 2023, 8(11): 28143-28152. doi: 10.3934/math.20231440

DownLoad:

DownLoad: