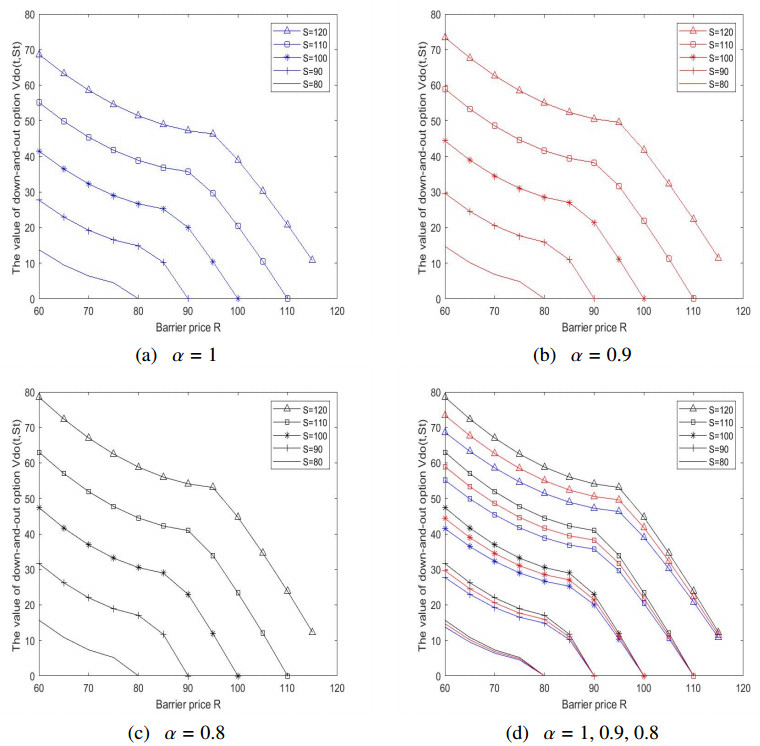

In this work, we mainly focused on the pricing formula for fractal barrier options where the underlying asset followed the sub-mixed fractional Brownian motion with jump, including the down-and-out call option, the down-and-out put option, the down-and-in call option, the down-and-in put option, and so on. To start, the fractal Black-Scholes type partial differential equation was established by using the fractal Itô's formula and a self-financing strategy. Then, by transforming the partial differential equation to the Cauchy problem, we obtained the explicit pricing formulae for fractal barrier options. Finally, the effects of barrier price, fractal dimension, Hurst index, jump intensity, and volatility on the value of fractal barrier options were exhibited through numerical experiments.

Citation: Chao Yue, Chuanhe Shen. Fractal barrier option pricing under sub-mixed fractional Brownian motion with jump processes[J]. AIMS Mathematics, 2024, 9(11): 31010-31029. doi: 10.3934/math.20241496

In this work, we mainly focused on the pricing formula for fractal barrier options where the underlying asset followed the sub-mixed fractional Brownian motion with jump, including the down-and-out call option, the down-and-out put option, the down-and-in call option, the down-and-in put option, and so on. To start, the fractal Black-Scholes type partial differential equation was established by using the fractal Itô's formula and a self-financing strategy. Then, by transforming the partial differential equation to the Cauchy problem, we obtained the explicit pricing formulae for fractal barrier options. Finally, the effects of barrier price, fractal dimension, Hurst index, jump intensity, and volatility on the value of fractal barrier options were exhibited through numerical experiments.

| [1] |

A. Dassios, J. W. Lim, Recursive formula for the double-barrier Parisian stopping time, J. Appl. Probab., 55 (2018), 282–301. http://doi.org/10.1017/jpr.2018.17 doi: 10.1017/jpr.2018.17

|

| [2] |

H. Funahashi, T. Higuchi, An analytical approximation for single barrier options under stochastic volatility models, Ann. Oper. Res., 266 (2018), 129–157. https://doi.org/10.1007/s10479-017-2559-3 doi: 10.1007/s10479-017-2559-3

|

| [3] |

T. Guillaume, Closed form valuation of barrier options with stochastic barriers, Ann. Oper. Res., 313 (2022), 1021–1050. https://doi.org/10.1007/s10479-020-03860-w doi: 10.1007/s10479-020-03860-w

|

| [4] |

Y. Gao, L. F. Jia, Pricing formulas of barrier-lookback option in uncertain financial markets, Chaos Soliton. Fract., 147 (2021), 110986–110994. https://doi.org/10.1016/j.chaos.2021.110986 doi: 10.1016/j.chaos.2021.110986

|

| [5] |

R. C. Merton, Theory of rational option pricing, Bell Econ. Manag. Sci., 4 (1973), 141–183. https://doi.org/10.2307/3003143 doi: 10.2307/3003143

|

| [6] | M. Rubinstein, Breaking down the barriers, Risk, 4 (1991), 28–35. |

| [7] |

F. Black, M. Scholes, The Pricing of Options and Corporate Liabilities, J. Polit. Econ., 81 (1973), 637–654. https://doi.org/10.1086/260062 doi: 10.1086/260062

|

| [8] |

Z. Ding, C. W. Granger, R. F. Engle, Long memory property of stock market returns and a new model, J. Empir. Financ., 1 (1993), 83–106. https://doi.org/10.1016/0927-5398(93)90006-D doi: 10.1016/0927-5398(93)90006-D

|

| [9] | A. N. Shiryaev, Essentials of stochastic finance: Facts, models, theory, World Scientific, Singapore, 1999. |

| [10] | A. N. Kolmogorov, Wienersche spiralen und einige andere interessante kurven in hilbertscen raum, cr (doklady), Acad. Sci. URSS (NS), 26 (1940), 115–118. |

| [11] | C. Necula, Option pricing in a fractional Brownian motion environment, Adv. Econ. Financ. Res.-Dofin Work. Pap. Ser., 2 (2008), 259–273. |

| [12] |

Q. Chen, Q. Zhang, C. Liu, The pricing and numerical analysis of lookback options for mixed fractional Brownian motion, Chaos Soliton. Fract., 128 (2019), 123–128. https://doi.org/10.1016/j.chaos.2019.07.038 doi: 10.1016/j.chaos.2019.07.038

|

| [13] |

L. Bian, Z. Li, Fuzzy simulation of European option pricing using sub-fractional Brownian motion, Chaos Soliton. Fract., 153 (2021), 111442–111452. https://doi.org/10.1016/j.chaos.2021.111442 doi: 10.1016/j.chaos.2021.111442

|

| [14] |

J. Wang, Y. Yan, W. Chen, W. Shao, W. Tang, Equity-linked securities option pricing by fractional Brownian motion, Chaos Soliton. Fract., 144 (2021), 110716–110723. https://doi.org/10.1016/j.chaos.2021.110716 doi: 10.1016/j.chaos.2021.110716

|

| [15] |

P. Cheridito, Arbitrage in fractional Brownian motion models, Financ. Stoch., 7 (2003), 533–553. https://doi.org/10.1007/s007800300101 doi: 10.1007/s007800300101

|

| [16] |

C. Bender, R. J. Elliott, Arbitrage in a discrete version of the Wick-fractional Black-Scholes market, Math. Oper. Res., 29 (2004), 935–945. https://doi.org/10.1287/moor.1040.0096 doi: 10.1287/moor.1040.0096

|

| [17] |

T. Bojdecki, L. G. Gorostiza, A. Talarczyk, Sub-fractional Brownian motion and its relation to occupation times, Stat. Probab. Lett., 69 (2004), 405–419. https://doi.org/10.1016/j.spl.2004.06.035 doi: 10.1016/j.spl.2004.06.035

|

| [18] |

E. N. Charles, Z. Mounir, On the sub-mixed fractional Brownian motion, Appl. Math. J. Chin. Univ., 30 (2015), 27–43. https://doi.org/10.1007/s11766-015-3198-6 doi: 10.1007/s11766-015-3198-6

|

| [19] |

C. Tudor, Some properties of the sub-fractional Brownian motion, Stochastics, 79 (2007), 431–448. https://doi.org/10.1080/17442500601100331 doi: 10.1080/17442500601100331

|

| [20] |

F. Xu, S. Zhou, Pricing of perpetual American put option with sub-mixed fractional Brownian motion, Fract. Calc. Appl. Anal., 22 (2019), 1145–1154. https://doi.org/10.1515/fca-2019-0060 doi: 10.1515/fca-2019-0060

|

| [21] |

R. C. Merton, Option pricing when underlying stock returns are discontinuous, J. Financ. Econ., 3 (1976), 125–144. https://doi.org/10.1016/0304-405X(76)90022-2 doi: 10.1016/0304-405X(76)90022-2

|

| [22] |

Q. Zhou, J. J. Yang, W. X. Wu, Pricing vulnerable options with correlated credit risk under jump-diffusion processes when corporate liabilities are random, Acta Math. Appl. Sin.-E., 35 (2019), 305–318. https://doi.org/10.1007/s10255-019-0821-y doi: 10.1007/s10255-019-0821-y

|

| [23] |

W. Sun, Y. Zhao, L. MacLean, Real options in a duopoly with jump diffusion prices, Asia-Pac. J. Oper. Res., 38 (2021), 2150009–2150037. https://doi.org/10.1142/S0217595921500093 doi: 10.1142/S0217595921500093

|

| [24] |

W. G. Zhang, Z. Li, Y. J. Liu, Y. Zhang, Pricing European option under fuzzy mixed fractional Brownian motion model with jumps, Comput. Econ., 58 (2021), 483–515. https://doi.org/10.1007/s10614-020-10043-z doi: 10.1007/s10614-020-10043-z

|

| [25] |

B. X. Ji, X. X. Tao, Y. T. Ji, Barrier option pricing in the sub-mixed fractional brownian motion with jump environment, Fractal Fract., 6 (2022), 244. https://doi.org/10.3390/fractalfract6050244 doi: 10.3390/fractalfract6050244

|

| [26] |

E. K. Akg$\ddot u$l, A. Akg$\ddot u$l, M. Yavuz, New illustrative applications of integral transforms to financial models with different fractional derivatives, Chaos Soliton. Fract., 146 (2021), 110877–110893. https://doi.org/10.1016/j.chaos.2021.110877 doi: 10.1016/j.chaos.2021.110877

|

| [27] |

S. E. Fadugba, Homotopy analysis method and its applications in the valuation of European call options with time-fractional Black-Scholes equation, Chaos Soliton. Fract., 141 (2020), 110351–110355. https://doi.org/10.1016/j.chaos.2020.110351 doi: 10.1016/j.chaos.2020.110351

|

| [28] |

X. J. Yang, J. A. T. Machado, D. Baleanu, Exact traveling-wave solution for local fractional Boussinesq equation in fractal domain, Fractals, 25 (2017), 1740006–1740012. https://doi.org/10.1142/s0218348x17400060 doi: 10.1142/s0218348x17400060

|

| [29] |

J. G. Liu, X. J. Yang, L. L. Geng, Y. R. Fan, Group analysis of the time fractional (3+1)-dimensional KdV-type equation, Fractals, 29 (2021), 2150169–2150187. https://doi.org/10.1142/S0218348X21501693 doi: 10.1142/S0218348X21501693

|

| [30] |

X. J. Yang, J. A. T. Machado, D. Baleanu, C. Cattani, On exact traveling-wave solutions for local fractional Korteweg-de Vries equation, Chaos, 26 (2016), 084312. https://doi.org/10.1063/1.4960543 doi: 10.1063/1.4960543

|

| [31] |

J. G. Liu, X. J. Yang, Y. Y. Feng, I. Muhammad, Group analysis to the time fractional nonlinear wave equation, Int. J. Math., 31 (2020), 20500299. https://doi.org/10.1142/S0129167X20500299 doi: 10.1142/S0129167X20500299

|

| [32] |

C. Yue, W. X. Ma, K. Li, A generalized method and its applications to n-dimensional fractional partial differential equations in fractal domain, Fractals, 30 (2022), 2250071–2250082. https://doi.org/10.1142/S0218348X22500712 doi: 10.1142/S0218348X22500712

|

| [33] |

S. M. Nuugulu, F. Gideon, K. C. Patidar, An efficient numerical method for pricing double-barrier options on an underlying stock governed by a fractal stochastic process, Fractal Fract., 7 (2023), 389. https://doi.org/10.3390/fractalfract7050389 doi: 10.3390/fractalfract7050389

|

| [34] |

K. F. Liu, J. C. Zhang, Y. T. Yang, Hedging lookback-barrier option by Malliavin calculus in a mixed fractional Brownian motion environment, Commun. Nonlinear Sci., 133 (2024), 107955. https://doi.org/10.1016/j.cnsns.2024.107955 doi: 10.1016/j.cnsns.2024.107955

|

| [35] |

J. H. He, Q. T. Ain, New promises and future challenges of fractal calculus: From two-scale thermodynamics to fractal variational principle, Therm. Sci., 24 (2020), 659–681. https://doi.org/10.2298/TSCI200127065H doi: 10.2298/TSCI200127065H

|

| [36] |

P. X. Wu, Q. Yang, J. H. He, Solitary waves of the variant Boussinesq-Burgers equation in a fractal-dimensional space, Fractals, 30 (2022), 2250056. https://doi.org/10.1142/S0218348X22500566 doi: 10.1142/S0218348X22500566

|

| [37] |

J. H. He, Fractal calculus and its geometrical explanation, Results Phys., 10 (2018), 272–276. https://doi.org/10.1016/j.rinp.2018.06.011 doi: 10.1016/j.rinp.2018.06.011

|

| [38] | P. Tankov, Financial modelling with jump processes, Chapman and Hall/CRC: London, UK, 2003. |

| [39] |

S. A. Metwally, A. F. Atiya, Using Brownian bridge for fast simulation of jump-diffusion processes and barrier options, J. Deriv., 10 (2002), 43–54. https://doi.org/10.3905/jod.2002.319189 doi: 10.3905/jod.2002.319189

|

Figures(2) / Tables(2)

Chao Yue, Chuanhe Shen. Fractal barrier option pricing under sub-mixed fractional Brownian motion with jump processes[J]. AIMS Mathematics, 2024, 9(11): 31010-31029. doi: 10.3934/math.20241496

DownLoad:

DownLoad: