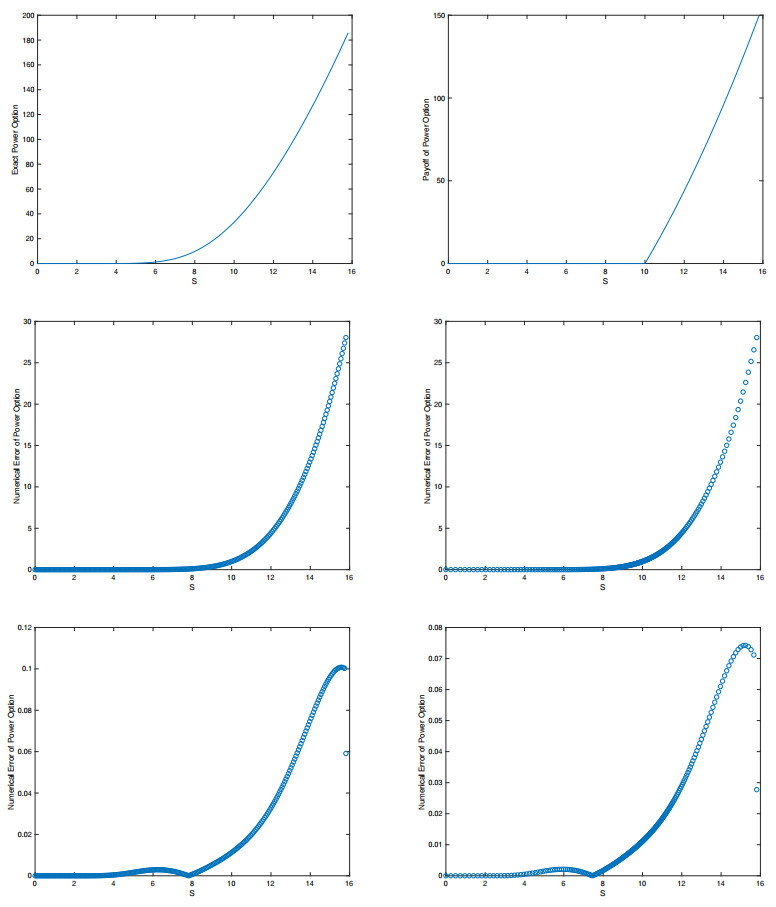

In this work, we numerically solve some different single and multi-asset European options with the finite difference method (FDM) and take the advantages of the antithetic variate method in Monte Carlo simulation (AMC) as a variance reduction technique in comparison to the standard Monte Carlo simulation (MC) in the end point of the domain, and the linear boundary condition has been implemented in other boundaries. We also apply the grid stretching transformation to make a non-equidistance discretization with more nodal points around the strike price (K) which is the non-smooth point in the payoff function to reduce the numerical errors around this point and have more accurate results. Superiority of our method (GS&AMC) will be demonstrated by comparison with the finite difference scheme with the equidistance discretization and the linear boundary conditions (Equi&L), the grid stretching discretization around K with linear boundary conditions (GS&L) and also the equidistance discretization with combination of the standard Monte Carlo simulation at the end point of the domain (Equi&MC). Furthermore, the root mean square errors (RMSE) of these four schemes in the whole region and the most interesting region which is around the strike price, have been compared.

Citation: Sima Mashayekhi, Seyed Nourollah Mousavi. A robust numerical method for single and multi-asset option pricing[J]. AIMS Mathematics, 2022, 7(3): 3771-3787. doi: 10.3934/math.2022209

In this work, we numerically solve some different single and multi-asset European options with the finite difference method (FDM) and take the advantages of the antithetic variate method in Monte Carlo simulation (AMC) as a variance reduction technique in comparison to the standard Monte Carlo simulation (MC) in the end point of the domain, and the linear boundary condition has been implemented in other boundaries. We also apply the grid stretching transformation to make a non-equidistance discretization with more nodal points around the strike price (K) which is the non-smooth point in the payoff function to reduce the numerical errors around this point and have more accurate results. Superiority of our method (GS&AMC) will be demonstrated by comparison with the finite difference scheme with the equidistance discretization and the linear boundary conditions (Equi&L), the grid stretching discretization around K with linear boundary conditions (GS&L) and also the equidistance discretization with combination of the standard Monte Carlo simulation at the end point of the domain (Equi&MC). Furthermore, the root mean square errors (RMSE) of these four schemes in the whole region and the most interesting region which is around the strike price, have been compared.

| [1] | F. Black, M. Scholes, The pricing of options and corporate liabilities, World Scientific Reference on Contingent Claims Analysis in Corporate Finance, 1 (2019), 3–21. doi: 10.1142/9789814759588_0001. |

| [2] |

W. Chen, S. Wang, A 2nd-order ADI finite difference method for a 2D fractional Black–Scholes equation governing European two asset option pricing, Math. Comput. Simul., 171 (2020), 279–293. doi: 10.1016/j.matcom.2019.10.016. doi: 10.1016/j.matcom.2019.10.016

|

| [3] |

K. Cheng, W. Feng, C. Wang, S. M. Wise, An energy stable fourth order finite difference scheme for the Cahn-Hilliard equation, J. Comput. Appl. Math., 362 (2019), 574–595. doi: 10.1016/j.cam.2018.05.039

|

| [4] | G. H. Choe, Stochastic analysis for finance with simulations, Springer, 2016. doi: 10.1007/978-3-319-25589-7. |

| [5] | D. J. Duffy, Finite difference methods in financial engineering: A partial differential equation approach, John Wiley & Sons, 2013. |

| [6] | E. G. Haug, The complete guide to option pricing formulas, New York: McGraw-Hill Companies, 2007. |

| [7] |

C. Hendricks, C. Heuer, M. Ehrhardt, M. Günther, High-order ADI finite difference schemes for parabolic equations in the combination technique with application in finance, J. Comput. Appl. Math., 316 (2017), 175–194. doi: 10.1016/j.cam.2016.08.044. doi: 10.1016/j.cam.2016.08.044

|

| [8] |

D. Jeong, M. Yoo, C. Yoo, J. Kim, A hybrid Monte Carlo and finite difference method for option pricing, Comput. Econ., 53 (2019), 111–124. doi: 10.1007/s10614-017-9730-4. doi: 10.1007/s10614-017-9730-4

|

| [9] |

L. Khodayari, M. Ranjbar, A computationally efficient numerical approach for multi-asset option pricing, Int. J. Comput. Math., 96 (2019), 1158–1168. doi: 10.1080/00207160.2018.1458096. doi: 10.1080/00207160.2018.1458096

|

| [10] |

M. N. Koleva, W. Mudzimbabwe, L. G. Vulkov, Fourth-order compact finite schemes for a parabolic-ordinary system of European option pricing liquidity shock model, Numer. Algor., 74 (2017), 59–75. doi: 10.1007/s11075-016-0138-3. doi: 10.1007/s11075-016-0138-3

|

| [11] |

X. Li, Z. Qiao, H. Zhang, Convergence of a fast explicit operator splitting method for the epitaxial growth model with slope selection, SIAM J. Numer. Anal., 55 (2017), 265–285. doi: 10.1137/15M1041122. doi: 10.1137/15M1041122

|

| [12] |

C. Liu, C. Wang, Y. Wang, A structure-preserving, operator splitting scheme for reaction-diffusion equations with detailed balance, J. Comput. Phys., 436 (2021), 110253. doi: 10.1016/j.jcp.2021.110253. doi: 10.1016/j.jcp.2021.110253

|

| [13] | S. Mashayekhi, J. Hugger, K$\alpha$-Shifting, Rannacher time stepping and mesh grading in Crank-Nicolson FDM for Black-Scholes option pricing, Commun. Math. Finance, 5 (2016), 1–31. |

| [14] |

B. J. McCartin, S. M. Labadie, Accurate and efficient pricing of vanilla stock options via the Crandall-Douglas scheme, Appl. Math. Comput., 143 (2003), 39–60. doi: 10.1016/S0096-3003(02)00343-0. doi: 10.1016/S0096-3003(02)00343-0

|

| [15] |

L. Qiao, W. Qiu, D. Xu, A second-order ADI difference scheme based on non-uniform meshes for the three-dimensional nonlocal evolution problem, Comput. Math. Appl., 102 (2021), 137–145. doi: 10.1016/j.camwa.2021.10.014. doi: 10.1016/j.camwa.2021.10.014

|

| [16] | D. Tavella, C. Randall, Pricing financial instruments: The finite difference method, Wiley, New York, 2000. |

| [17] | R. M. Stulz, Options on the minimum or the maximum of two risky assets, J. Financ. Econ., 10 (1982), 161–185. doi: 10.1016/0304-405X(82)90011-3. |

| [18] | P. G. Zhang, Correlation digital options, J. Financ. Eng., 4 (1995), 75–96. |

Figures(6) / Tables(6)

Sima Mashayekhi, Seyed Nourollah Mousavi. A robust numerical method for single and multi-asset option pricing[J]. AIMS Mathematics, 2022, 7(3): 3771-3787. doi: 10.3934/math.2022209

DownLoad:

DownLoad: