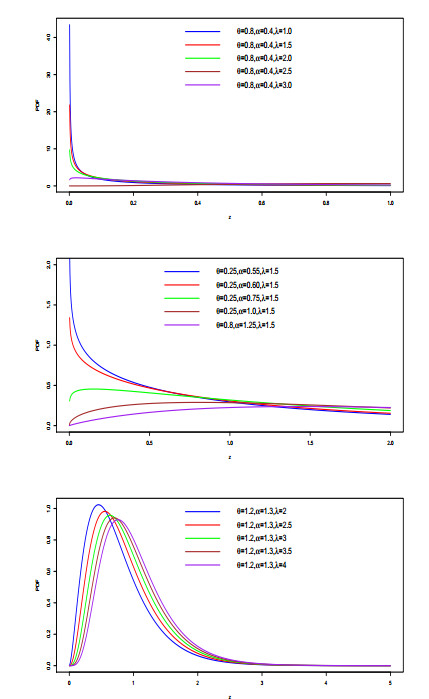

We proposed in this article a new three-parameter distribution, which is referred as the Topp-Leone exponentiated exponential model is proposed. It is used in modeling claim and risk data applied in actuarial and insurance studies. The probability density function of the suggested distribution can be unimodel and positively skewed. Different distributional and mathematical properties of the TL-EE model were provided. Furthermore, we established a maximum likelihood estimation method for estimating the unknown parameters involved in the model, and some actuarial measures were calculated. Also, the potential of these actuarial statistics were provided via numerical simulation experiments. Finally, two real datasets of insurance losses were analyzed to prove the performance and superiority of the suggested model among all its competitors distributions.

Citation: Hassan Alsuhabi. The new Topp-Leone exponentied exponential model for modeling financial data[J]. Mathematical Modelling and Control, 2024, 4(1): 44-63. doi: 10.3934/mmc.2024005

We proposed in this article a new three-parameter distribution, which is referred as the Topp-Leone exponentiated exponential model is proposed. It is used in modeling claim and risk data applied in actuarial and insurance studies. The probability density function of the suggested distribution can be unimodel and positively skewed. Different distributional and mathematical properties of the TL-EE model were provided. Furthermore, we established a maximum likelihood estimation method for estimating the unknown parameters involved in the model, and some actuarial measures were calculated. Also, the potential of these actuarial statistics were provided via numerical simulation experiments. Finally, two real datasets of insurance losses were analyzed to prove the performance and superiority of the suggested model among all its competitors distributions.

| [1] |

M. A. Meraou, M. Z. Raqab, Statistical properties and different estimation procedures of poisson-Lindley distribution, J. Stat. Theory Appl., 20 (2021), 33–45. https://doi.org/10.2991/jsta.d.210105.001 doi: 10.2991/jsta.d.210105.001

|

| [2] |

F. Hashemi, M. Naderi, A. Jamalizadeh, Normal mean-variance Lindley Birnbaum-Saunders distribution, Stat. Interface, 12 (2019), 585–597. https://doi.org/10.4310/SII.2019.V12.N4.A8 doi: 10.4310/SII.2019.V12.N4.A8

|

| [3] |

R. J. Abdelghani, M. A. Meraou, M. Z. Raqab, Bivariate compound distribution based on Poisson maxima of gamma variates and related applications, Int. J. Appl. Math., 34 (2021), 957. https://doi.org/10.12732/ijam.v34i5.6 doi: 10.12732/ijam.v34i5.6

|

| [4] |

M. Naderi, F. Hashemi, A. Bekker, A. Jamalizadeh, Modeling right-skewed fnancial data streams: a likelihood inference based on the generalized Birnbaum-Saunders mixture model, Appl. Math. Comput., 376 (2021), 125109. https://doi.org/10.1016/j.amc.2020.125109 doi: 10.1016/j.amc.2020.125109

|

| [5] |

S. Nadarajah, The skew logistic distribution, AStA Adv. Stat. Anal., 93 (2009), 187–203. https://doi.org/10.1007/s10182-009-0105-6 doi: 10.1007/s10182-009-0105-6

|

| [6] | S. Chakraborty, P. J. Hazarika, M. M. Ali, A new skew logistic distribution and its properties, Pak. J. Stat., 28 (2012), 513–524. |

| [7] |

Z. Ahmad, E. Mahmoudi, M. Alizadeh, Modelling insurance losses using a new beta power transformed family of distributions, Commun. Stat., 51 (2022), 4470–4491. https://doi.org/10.1080/03610918.2020.1743859 doi: 10.1080/03610918.2020.1743859

|

| [8] |

A. W. Marshall, I. A. Olkin, New method for adding a parameter to a family of distributions with application to the exponential and Weibull families, Biometrika, 84 (1997), 641–652. https://doi.org/10.1093/biomet/84.3.641 doi: 10.1093/biomet/84.3.641

|

| [9] |

A. Mahdavi, D. Kundu, A new method for generating distributions with an application to exponential distribution, Commun. Stat., 46 (2017), 6543–6557. https://doi.org/10.1080/03610926.2015.1130839 doi: 10.1080/03610926.2015.1130839

|

| [10] |

Z. Ahmad, M. Ilyas, G. G. Hamedani, The extended alpha power transformed family of distributions: properties and applications, J. Data Sci., 17 (2019), 726–741. https://doi.org/10.6339/JDS.201910_17(4).0006 doi: 10.6339/JDS.201910_17(4).0006

|

| [11] |

M. Alizadeh, M. H. Tahir, M. C. Gauss, M. Mansoor, M. Zubair, G. G. Hamedani, The Kumaraswamy Marshal-Olkin family of distributions, J. Egypt. Math. Soc., 23 (2015), 546–557. https://doi.org/10.1016/j.joems.2014.12.002 doi: 10.1016/j.joems.2014.12.002

|

| [12] |

A. Fayomi, E. M. Almetwally, M. E. Qura, Exploring new horizons: advancing data analysis in kidney patient infection rates and UEFA champions league scores using bivariate Kavya-Manoharan transformation family of distributions, Mathematics, 11 (2023), 2986. https://doi.org/10.3390/math11132986 doi: 10.3390/math11132986

|

| [13] |

A. Ahmad, N. Alsadat, M. N. Atchade, S. Q. ul Ain, A. M. Gemeay, M. A, Meraou, et al., New hyperbolic sine-generator with an example of Rayleigh distribution: simulation and data analysis in industry, Alex. Eng. J., 73 (2023), 415–426. https://doi.org/10.1016/j.aej.2023.04.048 doi: 10.1016/j.aej.2023.04.048

|

| [14] |

I. Elbatal, S. M. Alghamdi, F. Jamal, S. Khan, E. M. Almetwally, M. Elgarhy, Kavya-Manoharan Weibull-g family of distributions: statistical inference under progressive type-Ⅱ censoring scheme, Adv. Appl. Stat., 87 (2023), 191–223. https://doi.org/10.17654/0972361723034 doi: 10.17654/0972361723034

|

| [15] |

A. A. M. Teamah, A. A. Elbanna, A. M. Gemeay, Heavy-tailed log-logistic distribution: properties, risk measures and applications, Stat. Optim. Inf. Comput., 9 (2021), 910–941. https://doi.org/10.19139/soic-2310-5070-1220 doi: 10.19139/soic-2310-5070-1220

|

| [16] |

J. Zhao, Z. Ahmad, E. Mahmoudi, E. H. Hafez, M. M. M. El-Din, A new class of heavy-tailed distributions: modeling and simulating actuarial measures, Complexity, 2021 (2021), 5580228. https://doi.org/10.1155/2021/5580228 doi: 10.1155/2021/5580228

|

| [17] | P. M. Chiroque-Solano, F. A. da S. Moura, A heavy-tailed and overdispersed collective risk model, arXiv, 2021. https://doi.org/10.48550/arXiv.2101.09022 |

| [18] |

A. M. Basheer, Alpha power inverse weibull distribution with reliability application, J. Taibah Univ. Sci., 13 (2019), 423–432. https://doi.org/10.1080/16583655.2019.1588488 doi: 10.1080/16583655.2019.1588488

|

| [19] |

E. Yildirim, E. S. Ilıkkan, A. M. Gemeay, N. Makumi, M. E. Bakr, O. S. Balogun, Power unit Burr-XII distribution: statistical inference with applications, AIP Adv., 13 (2023), 105107. https://doi.org/10.1063/5.0171077 doi: 10.1063/5.0171077

|

| [20] |

M. Shakil, M. Munir, N. Kausar, M. Ahsanullah, A. Khadim, M. Sirajo, et al., Some inferences on three parameters Birnbaum-Saunders distribution: statistical properties, characterizations and applications, Comput. J. Math. Stat. Sci., 2 (2023), 197–222. https://doi.org/10.21608/cjmss.2023.224583.1011 doi: 10.21608/cjmss.2023.224583.1011

|

| [21] |

L. P. Sapkota, V. Kumar, A. M. Gemeay, M. E. Bakr, O. S. Balogun, A. H. Muse, New Lomax-G family of distributions: statistical properties and applications, AIP Adv., 13 (2023), 095128. https://doi.org/10.1063/5.0171949 doi: 10.1063/5.0171949

|

| [22] |

A. Z. Afify, A. M. Gemeay, N. A. Ibrahim, The heavy-tailed exponential distribution: risk measures, estimation, and application to actuarial data, Mathematics, 8 (2020), 1276. https://doi.org/10.3390/math8081276 doi: 10.3390/math8081276

|

| [23] |

A. A. M. Teamah, M. A. Elbanna, A. M. Gemeay, Heavy-tailed log-logistic distribution: properties, risk measures and applications, Stat. Optim. Inf. Comput., 9 (2021), 910–941. https://doi.org/10.19139/soic-2310-5070-1220 doi: 10.19139/soic-2310-5070-1220

|

| [24] |

A. M. Gemeay, K. Karakaya, M. E. Bakr, O. S. Balogun, M. N. Atchadé, E. Hussam, Power Lambert uniform distribution: statistical properties, actuarial measures, regression analysis, and applications, AIP Adv., 13 (2023), 095318. https://doi.org/10.1063/5.0170964 doi: 10.1063/5.0170964

|

| [25] |

M. Kamal, M. N. Atchadé, Y. M. Sokadjo, Nayabuddin, E. Hussam, A. M. Gemeay, et al., Statistical study for Covid-19 spread during the armed crisis faced by Ukrainians, Alex. Eng. J., 78 (2023), 419–425. https://doi.org/10.1016/j.aej.2023.07.040 doi: 10.1016/j.aej.2023.07.040

|

| [26] |

S. D. Tomarchio, A. Punzo, Dichotomous unimodal compound models: application to the distribution of insurance losses, J. Appl. Stat., 47 (2020), 2328–2353. https://doi.org/10.1080/02664763.2020.1789076 doi: 10.1080/02664763.2020.1789076

|

| [27] |

A. Al-Shomrani, O. Arif, A. Shawky, S. Hanif, M. Q. Shahbaz, Topp-Leone family of distributions: some properties and application, Pak. J. Stat. Oper. Res., 12 (2016), 443–451. https://doi.org/10.18187/pjsor.v12i3.1458 doi: 10.18187/pjsor.v12i3.1458

|

| [28] |

D. O. Tuoyo, F. C. Opone, N. Ekhosuehi, Topp-Leone Weibull distribution: its properties and applications, Earthline J. Math. Sci., 7 (2021), 381–401. https://doi.org/10.34198/ejms.7221.381401 doi: 10.34198/ejms.7221.381401

|

| [29] |

G. M. Ibrahim, A. S. Hassan, E. M. Almetwally, H. M. Almongy, Parameter estimation of alpha power inverted Topp-Leone distribution with applications, Intell. Autom. Soft Comput., 29 (2021), 353–371. https://doi.org/10.32604/iasc.2021.017586 doi: 10.32604/iasc.2021.017586

|

| [30] | L. P. Sapkota, Topp-Leone Fréchet distribution with theory and application, Janapriya J. Interdiscip. Stud., (2021), 65–80. |

| [31] |

A. S. Alyami, E. Ibrahim, N. Alotaibi, E. M. Almetwally, M. H. Okasha, M. Elgarhy, Topp-Leone modified Weibull model: theory and applications to medical and engineering data, Appl. Sci., 12 (2022), 10431. https://doi.org/10.3390/app122010431 doi: 10.3390/app122010431

|

| [32] |

A. A. Ogunde, O. E. Adenijia, Type Ⅱ Topp-Leone Bur Ⅻ distribution: properties and applications to failure time data, Sci. Afr., 16 (2022), e01200. https://doi.org/10.1016/j.sciaf.2022.e01200 doi: 10.1016/j.sciaf.2022.e01200

|

| [33] |

A. E. Teamah, A. A. Elbanna, A. M. Gemeay, Right truncated fréchet-weibull distribution: statistical properties and application, Delta J. Sci., 41 (2019), 20–29. https://doi.org/10.21608/djs.2020.139880 doi: 10.21608/djs.2020.139880

|

| [34] |

M. M. Ristić, N. Balakrishnan, The gamma-exponentiated exponential distribution, J. Stat. Comput. Simul., 82 (2012), 1191–1206. https://doi.org/10.1080/00949655.2011.574633 doi: 10.1080/00949655.2011.574633

|

| [35] |

M. Nagy, E. M. Almetwally, A. M. Gemeay, H. S. Mohammed, T. M. Jawa, N. Sayed-Ahmed, et al., The new novel discrete distribution with application on COVID-19 mortality numbers in Kingdom of Saudi Arabia and Latvia, Complexity, 2021 (2021), 7192833. https://doi.org/10.1155/2021/7192833 doi: 10.1155/2021/7192833

|

| [36] |

T. A. de Andrade, M. Bourguignon, G. M. Cordeiro, The exponentiated generalized extended exponential distribution, J. Data Sci., 14 (2016), 393–413. https://doi.org/10.6339/JDS.201607_14(3).0001 doi: 10.6339/JDS.201607_14(3).0001

|

| [37] |

M. A. Almuqrin, A. M. Gemeay, M. A. El-Raouf, M. Kilai, R. Aldallal, E. Hussam, A flexible extension of reduced kies distribution: properties, inference, and applications in biology, Complexity, 2022 (2022), 6078567. https://doi.org/10.1155/2022/6078567 doi: 10.1155/2022/6078567

|

| [38] | M. M. Salama, E. S. A. El-Sherpieny, A. E. A. Abd-Elaziz, The length-biased weighted exponentiated inverted exponential distribution: properties and estimation, Comput. J. Math. Stat. Sci., 2 (2023), 181–196. |

| [39] |

M. M. Raqab, M. Ahsanullah, Estimation of the location and scale parameters of generalized exponential distribution based on order statistics, J. Stat. Comput. Simul., 69 (2021), 109–123. https://doi.org/10.1080/00949650108812085 doi: 10.1080/00949650108812085

|

| [40] |

G. Mustafa, M. Ijaz, F. Jamal, Order statistics of inverse pareto distribution, Comput. J. Math. Stat. Sci., 1 (2022), 51–62. https://doi.org/10.21608/cjmss.2022.272724 doi: 10.21608/cjmss.2022.272724

|

| [41] |

S. Nadarajah, The exponentiated exponential distribution: a survey, AStA Adv. Stat. Anal., 95 (2011), 219–251. https://doi.org/10.1007/s10182-011-0154-5 doi: 10.1007/s10182-011-0154-5

|

| [42] |

S. E. Abu-Youssef, B. I. Mohammed, M. G. Sief, An extended exponentiated exponential distribution and its properties, Int. J. Comput. Appl., 121 (2015), 1–6. https://doi.org/10.5120/21533-4518 doi: 10.5120/21533-4518

|

| [43] |

E. S. A. El-Sherpieny, E. M. Almetwally, A. H. Muse, E. Hussam, Data analysis for COVID-19 deaths using a novel statistical model: simulation and fuzzy application, Plos One, 18 (2023), e0283618. https://doi.org/10.1371/journal.pone.0283618 doi: 10.1371/journal.pone.0283618

|

| [44] |

E. Hussam, M. A. Sabry, M. M. A. El-Raouf, E. M. Almetwally, Fuzzy vs. traditional reliability model for inverse Weibull distribution, Axioms, 12 (2023), 582. https://doi.org/10.3390/axioms12060582 doi: 10.3390/axioms12060582

|

| [45] |

C. Chesneau, V. Kumar, M. Khetan, M. Arshad, On a modified weighted exponential distribution with applications, Math Comput. Appl., 27 (2022), 17. https://doi.org/10.3390/mca27010017 doi: 10.3390/mca27010017

|

| [46] |

R. D. Gupta, D. Kundu, Generalized exponential distribution: existing results and some recent developments, J. Stat. Plan. Infer., 137 (2007), 3537–3547. https://doi.org/10.1016/j.jspi.2007.03.030 doi: 10.1016/j.jspi.2007.03.030

|

| [47] |

M. A. Meraou, N. M. Al-Kandari, M. Z. Raqab, D. Kundu, Analysis of skewed data by using compound poisson exponential distribution with applications to insurance claims, J. Stat. Comput. Simul., 92 (2022), 928–956. https://doi.org/10.1080/00949655.2021.1981324 doi: 10.1080/00949655.2021.1981324

|

| [48] |

M. A. Meraou, N. M. Al-Kandari, M. Z. Raqab, Univariate and bivariate compound models based on random sum of variates with application to the insurance losses data, J. Stat. Theory Pract., 16 (2022), 56. https://doi.org/10.1007/s42519-022-00282-8 doi: 10.1007/s42519-022-00282-8

|

| [49] |

N. M. Alfaer, A. M. Gemeay, H. M. Aljohani, A. Z. Afify, The extended log-logistic distribution: inference and actuarial applications, Mathematics, 9 (2021), 1386. https://doi.org/10.3390/math9121386 doi: 10.3390/math9121386

|

| [50] | C. Dutang, A. Charpentier, CASdatasets: insurance datasets, 2019. Available from: http://dutangc.free.fr/pub/RRepos/web/CASdatasets-index.html. |

| [51] |

V. Brazauskas, A. Kleefeld, Modeling severity and measuring tail risk of Norwegian fire claims, N. Amer. Actuar. J., 20 (2016), 1–16. https://doi.org/10.1080/10920277.2015.1062784 doi: 10.1080/10920277.2015.1062784

|

| [52] |

A. Bander, S. Hanaa, The Poisson-Lomax distribution, Rev. Colomb. Estad., 37 (2014), 223–243. https://doi.org/10.15446/rce.v37n1.44369 doi: 10.15446/rce.v37n1.44369

|

| [53] |

V. G. Cancho, F. Louzada-Neto, G. D. Barriga, Poisson-exponential lifetime distribution, Comput. Stat. Data Anal., 55 (2011), 677–686. https://doi.org/10.1016/j.csda.2010.05.033 doi: 10.1016/j.csda.2010.05.033

|

| [54] |

M. E. Ghitany, D. K. Al-Mutairi, N. Balakrishnan, L. J. Al-Enezi, Power lindley distribution and associated inference, Comput. Stat. Data Anal., 64 (2013), 20–33. https://doi.org/10.1016/j.csda.2013.02.026 doi: 10.1016/j.csda.2013.02.026

|

| [55] |

K. Adamidis, T. Dimitrakopoulou, S. Loukas, On an extension of the exponential-geometric distribution, Stat. Probab. Lett., 73 (2005), 259–269. https://doi.org/10.1016/j.spl.2005.03.013 doi: 10.1016/j.spl.2005.03.013

|

| [56] | S. Sen, S. K. Ghosh, H. Al-Mofleh, The mirra distribution for modeling time-to-event data sets, Springer, 2021, 59–73. https://doi.org/10.1007/978-981-16-13685 |

| [57] |

N. Alsadat, A. S. Hassan, A. M. Gemeay, C. Chesneau, M. Elgarhy, Different estimation methods for the generalized unit half-logistic geometric distribution: using ranked set sampling, AIP Adv., 13 (2023), 085230. https://doi.org/10.1063/5.0169140 doi: 10.1063/5.0169140

|

Figures(13) / Tables(16)

Hassan Alsuhabi. The new Topp-Leone exponentied exponential model for modeling financial data[J]. Mathematical Modelling and Control, 2024, 4(1): 44-63. doi: 10.3934/mmc.2024005

DownLoad:

DownLoad: