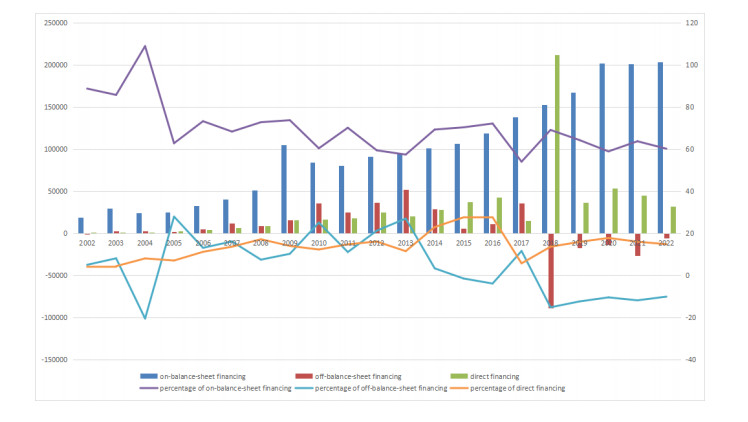

With the continuous innovation of financial instruments, the financing structure presents a diversified development trend, and the proportion of direct financing in Aggregate Financing to the Real Economy (AFRE) has been increasing. We utilized monthly data from January 2002 to March 2023 to establish a time-varying spillover index model and a large TVP-VAR model in order to investigate the dynamic impact of the social financing structure on various industry sectors. The empirical results suggested that the impact of financing structure on different industry sectors varies. Direct financing had the least impact on the industry compared to on-balance-sheet financing and off-balance-sheet financing. Lagging effects had the most significant influence on all industries. Furthermore, since 2015, the impact of different industries on the proportion of direct financing has significantly changed, indicating that the impact of direct financing on different industries became apparent during the 'stock crash'. Moreover, the impact of different financing methods on the economic development of various industry sectors was susceptible to external events, and the degree of impact varied. Our results are useful in helping policy makers better understand the changes in different industries affected by the financing structure, which can inform their policy formulation.

Citation: Xianghua Wu, Hongming Li, Yuanying Jiang. The impact of social financing structures on different industry sectors: A new perspective based on time-varying and high-dimensional methods[J]. AIMS Mathematics, 2024, 9(5): 10802-10831. doi: 10.3934/math.2024527

With the continuous innovation of financial instruments, the financing structure presents a diversified development trend, and the proportion of direct financing in Aggregate Financing to the Real Economy (AFRE) has been increasing. We utilized monthly data from January 2002 to March 2023 to establish a time-varying spillover index model and a large TVP-VAR model in order to investigate the dynamic impact of the social financing structure on various industry sectors. The empirical results suggested that the impact of financing structure on different industry sectors varies. Direct financing had the least impact on the industry compared to on-balance-sheet financing and off-balance-sheet financing. Lagging effects had the most significant influence on all industries. Furthermore, since 2015, the impact of different industries on the proportion of direct financing has significantly changed, indicating that the impact of direct financing on different industries became apparent during the 'stock crash'. Moreover, the impact of different financing methods on the economic development of various industry sectors was susceptible to external events, and the degree of impact varied. Our results are useful in helping policy makers better understand the changes in different industries affected by the financing structure, which can inform their policy formulation.

| [1] | G. Yi, Revisiting China's financial asset structure and policy implications, Econ. Res. J., 55 (2020), 4−17. |

| [2] |

B. K. Guru, I. S. Yadav, Financial development and economic growth: Panel evidence from BRICS, J. Econ. Financ. Adm. Sci., 24 (2019), 113−126. https://doi.org/10.1108/JEFAS-12-2017-0125 doi: 10.1108/JEFAS-12-2017-0125

|

| [3] |

D. Zhang, J. Li, Q. Ji, Does better access to credit help reduce energy intensity in China? Evidence from manufacturing firms, Energ. Policy, 145 (2020), 111710. https://doi.org/10.1016/j.enpol.2020.111710 doi: 10.1016/j.enpol.2020.111710

|

| [4] |

Z. He, W. Wei, China's financial system and economy: A review, Annu. Rev. Econ., 15 (2023), 451−483. https://doi.org/10.1146/annurev-economics-072622-095926 doi: 10.1146/annurev-economics-072622-095926

|

| [5] |

Y. Ning, J. Cherian, M. S. Sial, S. Álvarez-Otero, U. Comite, M. Zia-Ud-Din, Green bond as a new determinant of sustainable green financing, energy efficiency investment, and economic growth: A global perspective, Environ. Sci. Pollut. Res., 30 (2023), 61324−61339. https://doi.org/10.1007/s11356-021-18454-7 doi: 10.1007/s11356-021-18454-7

|

| [6] |

G. Zeng, H. Guo, C. Geng, Mechanism analysis of influencing factors on financing efficiency of strategic emerging industries under the "dual carbon" background: Evidence from China, Environ. Sci. Pollut. Res., 30 (2023), 10079–10098. https://doi.org/10.1007/s11356-022-22820-4 doi: 10.1007/s11356-022-22820-4

|

| [7] |

M. Brunnermeier, D. Palia, K. A. Sastry, C. A. Sims, Feedbacks: Financial markets and economic activity, Am. Econ. Rev., 111 (2021), 1845−1879. https://doi.org/10.1257/aer.20180733 doi: 10.1257/aer.20180733

|

| [8] |

B. X. Chen, Y. L. Sun, The impact of VIX on China's financial market: A new perspective based on high-dimensional and time-varying methods, N. Am. J. Econ. Financ., 63 (2022), 101831. https://doi.org/10.1016/j.najef.2022.101831 doi: 10.1016/j.najef.2022.101831

|

| [9] |

N. Antonakakis, I. Chatziantoniou, D. Gabauer, Refined measures of dynamic connectedness based on time-varying parameter vector autoregressions, J. Risk Financ. Manage., 13 (2020), 84. https://doi.org/10.3390/jrfm13040084 doi: 10.3390/jrfm13040084

|

| [10] |

M. Balcilar, D. Gabauer, Z. Umar, Crude oil futures contracts and commodity markets: New evidence from a TVP-VAR extended joint connectedness approach, Resour. Policy, 73 (2021), 102219. https://doi.org/10.1016/j.resourpol.2021.102219 doi: 10.1016/j.resourpol.2021.102219

|

| [11] | J. G. Gurley, E. S. Shaw, Financial aspects of economic development, Am. Econ. Rev., 45 (1955), 515−538. |

| [12] |

T. Beck, R. Levine, N. Loayza, Finance and the sources of growth, J. Financ. Econ., 58 (2000), 261−300. https://doi.org/10.1016/S0304-405X(00)00072-6 doi: 10.1016/S0304-405X(00)00072-6

|

| [13] |

S. Sanfilippo-Azofra, B. Torre-Olmo, M. Cantero-Saiz, C. López-Gutiérrez, Financial development and the bank lending channel in developing countries, J. Macroecon., 55 (2018), 215−234. https://doi.org/10.1016/j.jmacro.2017.10.009 doi: 10.1016/j.jmacro.2017.10.009

|

| [14] | F. S. Mishkin, The economics of money, banking and financial markets, The Pearson Series in Economics, 2012, 1−50. |

| [15] |

F. Allen, J. Q. Qian, M. Qian, A review of China's institutions, Annu. Rev. Financ. Econ., 11 (2019), 39−64. https://doi.org/10.1146/annurev-financial-110118-123027 doi: 10.1146/annurev-financial-110118-123027

|

| [16] | R. Z. Zhao, W. H. Wang, C. Y. Wang, Structural problems in and reform suggestions on the supply side of finance: A comparative analysis from the perspective of financial structure, Econ. Perspect., 710 (2020), 15−32. |

| [17] |

P. Tian, B. Lin, Impact of financing constraints on firm's environmental performance: Evidence from China with survey data, J. Clean. Prod., 217 (2019), 432−439. https://doi.org/10.1016/j.jclepro.2019.01.209 doi: 10.1016/j.jclepro.2019.01.209

|

| [18] | X. M. Feng, Z. X. Li, X. H. Guo, The impacts of financial disintermediation on commercial banks' assets and liabilities structure, Commer. Res., 469 (2016), 45−51. |

| [19] |

R. Levine, Bank-based or market-based financial systems: Which is better? J. Financ. Intermed., 11 (2002), 398−428. https://doi.org/10.1006/jfin.2002.0341 doi: 10.1006/jfin.2002.0341

|

| [20] |

T. Beck, R. Levine, Stock markets, banks, and growth: Panel evidence, J. Bank. Financ., 28 (2004), 423−442. https://doi.org/10.1016/S0378-4266(02)00408-9 doi: 10.1016/S0378-4266(02)00408-9

|

| [21] |

E. Nizam, A. Ng, G. Dewandaru, R. Nagayev, M. A. Nkoba, The impact of social and environmental sustainability on financial performance: A global analysis of the banking sector, J. Multination. Financ. M., 49 (2019), 35−53. https://doi.org/10.1016/j.mulfin.2019.01.002 doi: 10.1016/j.mulfin.2019.01.002

|

| [22] |

S. Bansal, I. Garg, G. D. Sharma, Social entrepreneurship as a path for social change and driver of sustainable development: A systematic review and research agenda, Sustainability, 11 (2019), 1091. https://doi.org/10.3390/su11041091 doi: 10.3390/su11041091

|

| [23] |

M. Qian, B. Y. Yeung, Bank financing and corporate governance, J. Corp. Financ., 32 (2015), 258−270. https://doi.org/10.1016/j.jcorpfin.2014.10.006 doi: 10.1016/j.jcorpfin.2014.10.006

|

| [24] |

P. Benczúr, S. Karagiannis, V. Kvedaras, Finance and economic growth: Financing structure and non-linear impact, J. Macroecon., 62 (2019), 103048. https://doi.org/10.1016/j.jmacro.2018.08.001 doi: 10.1016/j.jmacro.2018.08.001

|

| [25] |

L. He, R. Liu, Z. Zhong, D. Wang, Y. Xia, Can green financial development promote renewable energy investment efficiency? A consideration of bank credit, Renew. Energ., 143 (2019), 974−984. https://doi.org/10.1016/j.renene.2019.05.059 doi: 10.1016/j.renene.2019.05.059

|

| [26] | C. Deng, D. Y. Qu, K. Zhao, The effects of Chinese social financing's fluctuation on macro-economy: An empirical study based on dual perspective of scale and structure, Inquiry Econ. Issues, 11 (2018), 20−27. |

| [27] |

X. Cheng, H. Degryse, The impact of bank and non-bank financial institutions on local economic growth in China, J. Financ. Serv. Res., 37 (2010), 179−199. https://doi.org/10.1007/s10693-009-0077-4 doi: 10.1007/s10693-009-0077-4

|

| [28] |

J. Zhang, L. Wang, S. Wang, Financial development and economic growth: Recent evidence from China, J. Comp. Econ., 40 (2012), 393−412. https://doi.org/10.1016/j.jce.2012.01.001 doi: 10.1016/j.jce.2012.01.001

|

| [29] |

S. Mishra, P. K. Narayan, A nonparametric model of financial system and economic growth, Int. Rev. Econ. Financ., 39 (2015), 175−191. https://doi.org/10.1016/j.iref.2015.04.004 doi: 10.1016/j.iref.2015.04.004

|

| [30] |

P. H. Hsu, X. Tian, Y. Xu, Financial development and innovation: Cross-country evidence, J. Financ. Econ., 112 (2014), 116−135. https://doi.org/10.1016/j.jfineco.2013.12.002 doi: 10.1016/j.jfineco.2013.12.002

|

| [31] |

S. H. Law, N. Singh, Does too much finance harm economic growth? J. Bank. Financ., 41 (2014), 36−44. https://doi.org/10.1016/j.jbankfin.2013.12.020 doi: 10.1016/j.jbankfin.2013.12.020

|

| [32] | Y. Tian, Empirical study on the relation between direct financing and economical development, In: 2010 International Conference on E-Product E-Service and E-Entertainment, IEEE, Henan, China, 2010, 1−3. https://doi.org/10.1109/ICEEE.2010.5661453 |

| [33] |

X. Xiang, C. Liu, M. Yang, Who is financing corporate green innovation? Int. Rev. Econ. Financ., 78 (2022), 321−337. https://doi.org/10.1016/j.iref.2021.12.011 doi: 10.1016/j.iref.2021.12.011

|

| [34] |

A. B. Fanta, D. Makina, Equity, bonds, institutional debt and economic growth: Evidence from South Africa, S. Afr. J. Econ., 85 (2017), 86−97. https://doi.org/10.1111/saje.12122 doi: 10.1111/saje.12122

|

| [35] |

S. Zhang, Z. Wu, Y. Wang, Y. Hao, Fostering green development with green finance: An empirical study on the environmental effect of green credit policy in China, J. Environ. Manage., 296 (2021), 113159. https://doi.org/10.1016/j.jenvman.2021.113159 doi: 10.1016/j.jenvman.2021.113159

|

| [36] | A. Draksaite, V. Kazlauskiene, L. Melnyk, The perspective of the green bonds as novel debt instruments in sustainable economy, Organizational Strategy and Financial Economics: Proceedings of the 21st Eurasia Business and Economics Society Conference, Springer, Cham, 2018,221−230. https://doi.org/10.1007/978-3-319-76288-3_16 |

| [37] |

R. P. Pradhan, M. B. Arvin, S. E. Bennett, M. Nair, J. H. Hall, Bond market development, economic growth and other macroeconomic determinants: Panel VAR evidence, Asia-Pac. Financ. Mark., 23 (2016), 175−201. https://doi.org/10.1007/s10690-016-9214-x doi: 10.1007/s10690-016-9214-x

|

| [38] |

A. Singh, Financial liberalisation, stockmarkets and economic development, Econ. J., 107 (1997), 771−782. https://doi.org/10.1111/j.1468-0297.1997.tb00042.x doi: 10.1111/j.1468-0297.1997.tb00042.x

|

| [39] |

B. Holmström, J. Tirole, Market liquidity and performance monitoring, J. Polit. Econ., 101 (1993), 678−709. https://doi.org/10.1086/261893 doi: 10.1086/261893

|

| [40] |

Y. Jin, X. Gao, M. Wang, The financing efficiency of listed energy conservation and environmental protection firms: Evidence and implications for green finance in China, Energ. Policy, 153 (2021), 112254. https://doi.org/10.1016/j.enpol.2021.112254 doi: 10.1016/j.enpol.2021.112254

|

| [41] |

S. G. Anton, A. E. A. Nucu, The effect of financial development on renewable energy consumption. A panel data approach, Renew. Energ., 147 (2020), 330−338. https://doi.org/10.1016/j.renene.2019.09.005 doi: 10.1016/j.renene.2019.09.005

|

| [42] |

Y. Wang, X. Lei, R. Long, J. Zhao, Green credit, financial constraint, and capital investment: Evidence from China's energy-intensive enterprises, Environ. Manage., 66 (2020), 1059−1071. https://doi.org/10.1007/s00267-020-01346-w doi: 10.1007/s00267-020-01346-w

|

| [43] |

Y. Ouyang, P. Li, On the nexus of financial development, economic growth, and energy consumption in China: New perspective from a GMM panel VAR approach, Energ. Econ., 71 (2018), 238−252. https://doi.org/10.1016/j.eneco.2018.02.015 doi: 10.1016/j.eneco.2018.02.015

|

| [44] |

H. Nong, Y. T. Guan, Y. Y. Jiang, Identifying the volatility spillover risks between crude oil prices and China's clean energy market, Electron. Res. Arch., 30 (2022), 4593−4618. https://doi.org/10.3934/era.2022233 doi: 10.3934/era.2022233

|

| [45] |

H. Sun, F. Zou, B. Mo, Does FinTech drive asymmetric risk spillover in the traditional finance? AIMS Math., 7 (2022), 20850−20872. https://doi.org/10.3934/math.20221143 doi: 10.3934/math.20221143

|

| [46] |

M. Alharbey, T. M. Alfahaid, O. Ben-Salha, Asymmetric volatility spillover between oil prices and regional renewable energy stock markets: A time-varying parameter vector autoregressive-based connectedness approach, AIMS Math., 8 (2023), 30639−30667. https://doi.org/10.3934/math.20231566 doi: 10.3934/math.20231566

|

| [47] |

D. H. Zhou, X. X. Liu, C. Tang, G. Y. Yang, Time-varying risk spillovers in Chinese stock market–New evidence from high-frequency data, N. A. J. Econ. Financ., 64 (2023), 101870. https://doi.org/10.1016/j.najef.2022.101870 doi: 10.1016/j.najef.2022.101870

|

| [48] |

B. X. Chen, Y. L. Sun, Risk characteristics and connectedness in cryptocurrency markets: New evidence from a non-linear framework, N. A. J. Econ. Financ., 69 (2024), 102036. https://doi.org/10.1016/j.najef.2023.102036 doi: 10.1016/j.najef.2023.102036

|

| [49] |

K. S. Chen, W. C. Ong, Dynamic correlations between Bitcoin, carbon emission, oil and gold markets: New implications for portfolio management, AIMS Math., 9 (2024), 1403−1433. https://doi.org/10.3934/math.2024069 doi: 10.3934/math.2024069

|

| [50] |

E. Dogan, M. Madaleno, D. Taskin, P. Tzeremes, Investigating the spillovers and connectedness between green finance and renewable energy sources, Renew. Energ., 197 (2022), 709−722. https://doi.org/10.1016/j.renene.2022.07.131 doi: 10.1016/j.renene.2022.07.131

|

| [51] |

N. A. Kyriazis, S. Papadamou, P. Tzeremes, Are benchmark stock indices, precious metals or cryptocurrencies efficient hedges against crises? Econ. Model., 128 (2023), 106502. https://doi.org/10.1016/j.econmod.2023.106502 doi: 10.1016/j.econmod.2023.106502

|

| [52] |

E. Dogan, T. Luni, M. T. Majeed, P. Tzeremes, The nexus between global carbon and renewable energy sources: A step towards sustainability, J. Clean. Prod., 416 (2023), 137927. https://doi.org/10.1016/j.jclepro.2023.137927 doi: 10.1016/j.jclepro.2023.137927

|

| [53] |

R. Inglesi-Lotz, E. Dogan, J. Nel, P. Tzeremes, Connectedness and spillovers in the innovation network of green transportation, Energ. Policy, 180 (2023), 113686. https://doi.org/10.1016/j.enpol.2023.113686 doi: 10.1016/j.enpol.2023.113686

|

| [54] |

F. X. Diebold, K. Yılmaz, On the network topology of variance decompositions: Measuring the connectedness of financial firms, J. Econometrics, 182 (2014), 119−134. https://doi.org/10.1016/j.jeconom.2014.04.012 doi: 10.1016/j.jeconom.2014.04.012

|

| [55] |

G. Koop, D. Korobilis, A new index of financial conditions, Eur. Econ. Rev., 71 (2014), 101−116. https://doi.org/10.1016/j.euroecorev.2014.07.002 doi: 10.1016/j.euroecorev.2014.07.002

|

| [56] |

J. C. C. Chan, E. Eisenstat, R. W. Strachan, Reducing the state space dimension in a large TVP-VAR, J. Econometrics, 218 (2020), 105−118. https://doi.org/10.1016/j.jeconom.2019.11.006 doi: 10.1016/j.jeconom.2019.11.006

|

| [57] |

S. Frühwirth-Schnatter, H. Wagner, Stochastic model specification search for Gaussian and partial non-Gaussian state space models, J. Econometrics, 154 (2010), 85−100. https://doi.org/10.1016/j.jeconom.2009.07.003 doi: 10.1016/j.jeconom.2009.07.003

|

| [58] |

Z. Dong, Y. Li, X. Zhuang, J. Wang, Impacts of COVID-19 on global stock sectors: Evidence from time-varying connectedness and asymmetric nexus analysis, N. A. J. Econ. Financ., 62 (2022), 101753. https://doi.org/10.1016/j.najef.2022.101753 doi: 10.1016/j.najef.2022.101753

|

| [59] |

L. Shen, X. Lu, T. L. D. Huynh, C. Liang, Air quality index and the Chinese stock market volatility: Evidence from both market and sector indices, Int. Rev. Econ. Financ., 84 (2023), 224−239. https://doi.org/10.1016/j.iref.2022.11.027 doi: 10.1016/j.iref.2022.11.027

|

| [60] |

W. Lv, B. Li, Climate policy uncertainty and stock market volatility: Evidence from different sectors, Financ. Res. Lett., 51 (2023), 103506. https://doi.org/10.1016/j.frl.2022.103506 doi: 10.1016/j.frl.2022.103506

|

| [61] |

Z. Dai, Y. Peng, Economic policy uncertainty and stock market sector time-varying spillover effect: Evidence from China, N. A. J. Econ. Financ., 62 (2022), 101745. https://doi.org/10.1016/j.najef.2022.101745 doi: 10.1016/j.najef.2022.101745

|

| [62] |

M. K. Uddin, X. Pan, U. Saima, C. Zhang, Influence of financial development on energy intensity subject to technological innovation: Evidence from panel threshold regression, Energy, 239 (2022), 122337. https://doi.org/10.1016/j.energy.2021.122337 doi: 10.1016/j.energy.2021.122337

|

| [63] |

M. A. Khan, J. E. T. Segovia, M. I. Bhatti, A. Kabir, Corporate vulnerability in the US and China during COVID-19: A machine learning approach, J. Econ. Asymmetries, 27 (2023), e00302. https://doi.org/10.1016/j.jeca.2023.e00302 doi: 10.1016/j.jeca.2023.e00302

|

| [64] |

F. Ahmed, A. A. Syed, M. A. Kamal, M. N. López-García, J. P. Ramos-Requena, S. Gupta, Assessing the impact of COVID-19 pandemic on the stock and commodity markets performance and sustainability: A comparative analysis of South Asian countries, Sustainability, 13 (2021), 5669. https://doi.org/10.3390/su13105669 doi: 10.3390/su13105669

|

| [65] |

C. B. Wang, J. R. Rong, J. M. Zhu, Algorithm research on the influence of financing structure and cash holding on enterprise innovation based on system GMM model function theory, J. Comb. Optim., 45 (2023), 61. https://doi.org/10.1007/s10878-023-00991-1 doi: 10.1007/s10878-023-00991-1

|

| [66] |

Q. Ding, J. Huang, H. Zhang, The time-varying effects of financial and geopolitical uncertainties on commodity market dynamics: A TVP-SVAR-SV analysis, Resour. Policy, 72 (2021), 102079. https://doi.org/10.1016/j.resourpol.2021.102079 doi: 10.1016/j.resourpol.2021.102079

|

| [67] |

R. Ye, J. Gong, X. Xia, Trading risk spillover mechanism of rare earth in China: New perspective based on time-varying connectedness approach, Systems, 11 (2023), 168. https://doi.org/10.3390/systems11040168 doi: 10.3390/systems11040168

|

Figures(12) / Tables(4)

Xianghua Wu, Hongming Li, Yuanying Jiang. The impact of social financing structures on different industry sectors: A new perspective based on time-varying and high-dimensional methods[J]. AIMS Mathematics, 2024, 9(5): 10802-10831. doi: 10.3934/math.2024527

DownLoad:

DownLoad: