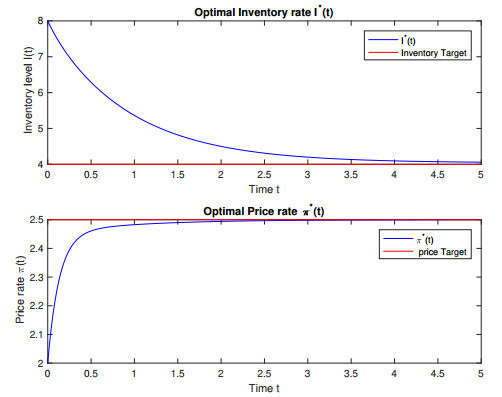

We witness an increased emphasis on the integration of different areas of manufacturing firms with the intention of avoiding suboptimal solutions. In particular, due to new technologies which make it easy to change the price of a product in real time, the integration of pricing and production planning may be garnering the most interest. We are proposing in this paper a way to model the dynamics of the price. Thus, the price and the inventory level are considered as state variables whereas the supply (production) rate is the control variable. The demand rate is dynamic and state-dependent. Using a model predictive control approach, the optimal supply rate, and thus the optimal price and inventory level, are obtained. Different examples are provided under different scenarios for the supply rate and for the demand rate.

Citation: Messaoud Bounkhel, Lotfi Tadj. Model predictive control based integration of pricing and production planning[J]. AIMS Mathematics, 2024, 9(1): 2282-2307. doi: 10.3934/math.2024113

We witness an increased emphasis on the integration of different areas of manufacturing firms with the intention of avoiding suboptimal solutions. In particular, due to new technologies which make it easy to change the price of a product in real time, the integration of pricing and production planning may be garnering the most interest. We are proposing in this paper a way to model the dynamics of the price. Thus, the price and the inventory level are considered as state variables whereas the supply (production) rate is the control variable. The demand rate is dynamic and state-dependent. Using a model predictive control approach, the optimal supply rate, and thus the optimal price and inventory level, are obtained. Different examples are provided under different scenarios for the supply rate and for the demand rate.

| [1] |

T. M. Whitin, Inventory control and price theory, Manag. Sci., 2 (1955), 61–80. https://doi.org/10.1287/mnsc.2.1.61 doi: 10.1287/mnsc.2.1.61

|

| [2] | J. Eliashberg, R. Steinberg, Marketing-production joint decision-making, In: Handbooks in operations research and management science, 5 (1993), 828–880. https://doi.org/10.1016/S0927-0507(05)80041-6 |

| [3] |

W. Elmaghraby, P. Keskinocak, Dynamic pricing in the presence of inventory considerations: research overview, current practices, and future directions, Manag. Sci., 49 (2003), 1287–1309. https://doi.org/10.1287/mnsc.49.10.1287.17315 doi: 10.1287/mnsc.49.10.1287.17315

|

| [4] | L. M. A. Chan, Z. J. M. Shen, D. Simchi-Levi, J. L. Swann, Coordination of pricing and inventory decisions: a survey and classification, In: D. Simchi-Levi, S. D. Wu, Z. J. M. Shen, Handbook of quantitative supply chain analysis, International Series in Operations Research & Management Science, Boston: Springer, 74 (2004), 335–392. https://doi.org/10.1007/978-1-4020-7953-5_9 |

| [5] | D. Simchi-Levi, X. Chen, J. Bramel, The logic of logistics: theory, algorithms, and applications for logistics and supply chain management, 2 Eds, New York: Springer, 2005 https://doi.org/10.1007/b97669 |

| [6] | C. A. Yano, S. M. Gilbert, Coordinated pricing and production/procurement decision: a review, In: A. K. Chakravarty, J. Eliashberg, Managing business interfaces, International Series in Quantitative Marketing, Boston: Springer, 16 (2005), 65–103. https://doi.org/10.1007/0-387-25002-6_3 |

| [7] | R. H. Niu, I. Castillo, T. Joro, Joint pricing and inventory/production decisions in a supply chain: a state-of-the-art survey, Proceedings of the Western Decision Sciences Institute, WDSI 2001 Fortieth Annual Meeting, Portland Oregon, 2011. |

| [8] | X. Chen, D. Simchi-Levi, Pricing and inventory management, In: R. Philips, O. Özalp, The Oxford handbook of pricing management, Oxford University Press, 2012,784–824. https://doi.org/10.1093/oxfordhb/9780199543175.013.0030 |

| [9] | R. Zhang, An introduction to joint pricing and inventory management under stochastic demand, 2013. |

| [10] |

A. V. Den Boer, Dynamic pricing and learning: Historical origins, current research, and new directions, Surv. Oper. Res. Manage. Sci., 20 (2015), 1–18. https://doi.org/10.1016/j.sorms.2015.03.001 doi: 10.1016/j.sorms.2015.03.001

|

| [11] |

G. Feichtinger, R. Hartl, Optimal pricing and production in an inventory model, Eur. J. Oper. Res., 19 (1985), 45–56. https://doi.org/10.1016/0377-2217(85)90307-8 doi: 10.1016/0377-2217(85)90307-8

|

| [12] |

P. C. Lin, L. Y. Shue, Application of optimal control theory to product pricing and warranty with free replacement under the influence of basic lifetime distributions, Comput. Ind. Eng., 48 (2005), 69–82. https://doi.org/10.1016/j.cie.2004.07.009 doi: 10.1016/j.cie.2004.07.009

|

| [13] |

P. C. Lin, Optimal pricing, production rate, and quality under learning effects, J. Bus. Res., 61 (2008), 1152–1159. https://doi.org/10.1016/j.jbusres.2007.11.008 doi: 10.1016/j.jbusres.2007.11.008

|

| [14] |

Y. Feng, J. Ou, Z. Pang, Optimal control of price and production in an assemble-to-order system, Oper. Res. Lett., 36 (2008), 506–512. https://doi.org/10.1016/j.orl.2008.01.012 doi: 10.1016/j.orl.2008.01.012

|

| [15] |

M. F. Keblis, Y. Feng, Optimal pricing and production control in an assembly system with a general stockout cost, IEEE Trans. Automat. Contr., 57 (2012), 1821–1826. https://doi.org/10.1109/TAC.2011.2178335 doi: 10.1109/TAC.2011.2178335

|

| [16] |

X. Cai, Y. Feng, Y. Li, D. Shi, Optimal pricing policy for a deteriorating product by dynamic tracking control, Int. J. Prod. Res., 51 (2013), 2491–2504. https://doi.org/10.1080/00207543.2012.743688 doi: 10.1080/00207543.2012.743688

|

| [17] |

R. Chenavaz, Better product quality may lead to lower product price, B.E. J. Theor. Econ., 17 (2016), 1–22. https://doi.org/10.1515/bejte-2015-0062 doi: 10.1515/bejte-2015-0062

|

| [18] | R. Chenavaz, Dynamic pricing rule and R & D, Econ. Bull., 31 (2011), 2229–2236. |

| [19] |

J. Vörös, Multi-period models for analyzing the dynamics of process improvement activities, Eur. J. Oper. Res., 230 (2013), 615–623. https://doi.org/10.1016/j.ejor.2013.04.036 doi: 10.1016/j.ejor.2013.04.036

|

| [20] |

E. Adida, G. Perakisy, A nonlinear continuous time optimal control model of dynamic pricing and inventory control with no backorders, Nav. Res. Log., 54 (2007), 767–795. https://doi.org/10.1002/nav.20250 doi: 10.1002/nav.20250

|

| [21] | M. Weber, Optimal inventory control in the presence of dynamic pricing and dynamic advertising, Ph.D. Dissertation, Humboldt-Universität of Berlin, Germany, 2015. https://doi.org/10.18452/17339 |

| [22] |

A. Herbon, E. Khmelnitsky, Optimal dynamic pricing and ordering of a perishable product under additive effects of price and time on demand, Eur. J. Oper. Res., 260 (2017), 546–556. https://doi.org/10.1016/j.ejor.2016.12.033 doi: 10.1016/j.ejor.2016.12.033

|

| [23] | L. Yang, Y. Cai, Optimal dynamic pricing for fresh products under the cap-and-trade scheme, 2017 International Conference on Service Systems and Service Management, Dalian, IEEE, 2017. https://doi.org/10.1109/ICSSSM.2017.7996183 |

Figures(8)

Messaoud Bounkhel, Lotfi Tadj. Model predictive control based integration of pricing and production planning[J]. AIMS Mathematics, 2024, 9(1): 2282-2307. doi: 10.3934/math.2024113

DownLoad:

DownLoad: