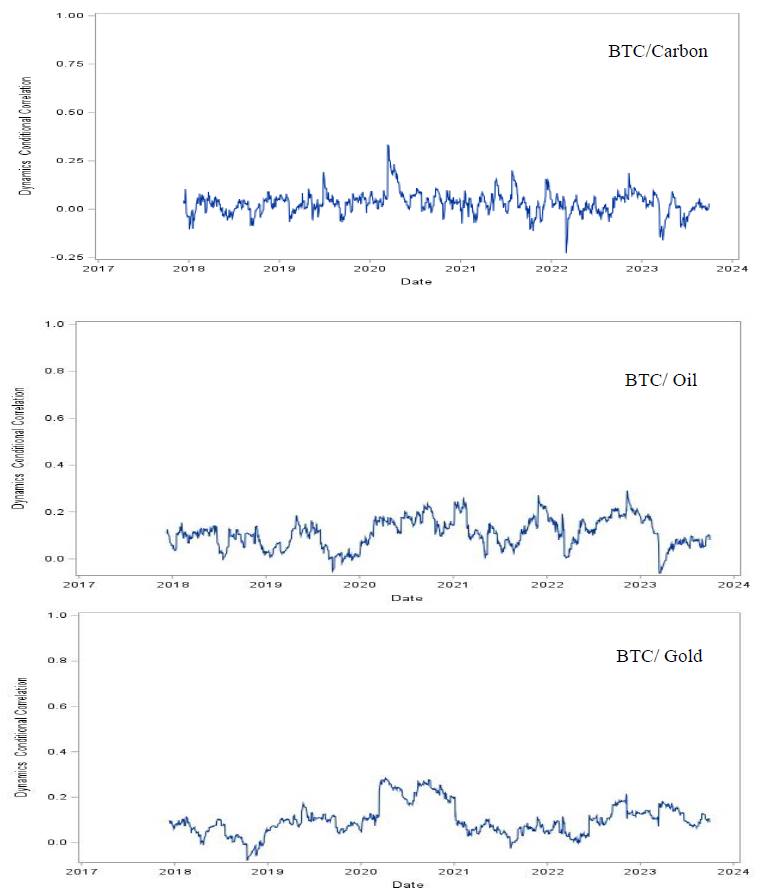

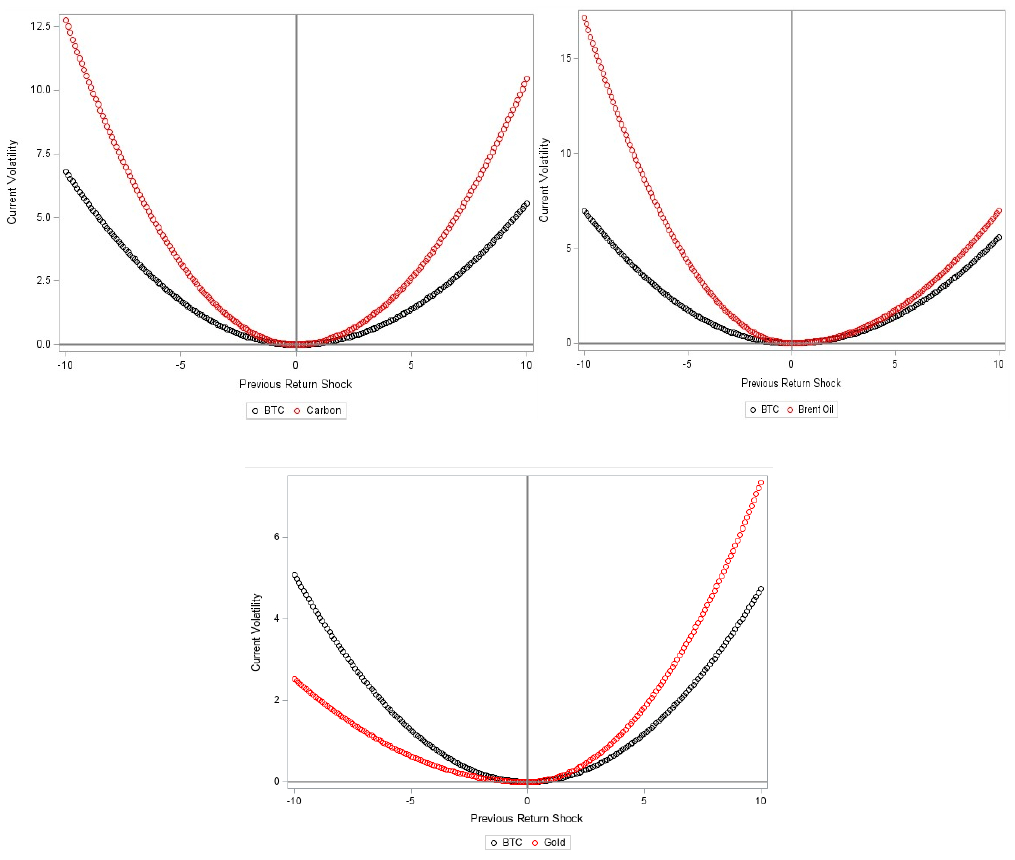

In this paper, we aim to uncover the dynamic spillover effects of Bitcoin environmental attention (EBEA) on major asset classes: Carbon emission, crude oil and gold futures, and analyze whether the integration of Bitcoin into portfolio allocation performance. In this study, we document the properties of futures assets and empirically investigate their dynamic correlation between Bitcoin, carbon emission, oil and gold futures. Overall, it is evident that the volatility of Bitcoin, as well as other prominent returns, exhibit an asymmetric response to good and bad news. Additionally, we evaluate the hedge potential benefits of these emerging futures assets for market participants. The evidence supports the idea that the leading cryptocurrency-Bitcoin can be a suitable hedge instrument after the COVID-19 pandemic outbreak. More importantly, our analysis of the portfolio's performance shows that carbon emission futures are diversification benefit products in most of the considered cases. Notably, incorporating carbon futures into portfolios may attract new investors to carbon markets for double goals of risk diversification. These findings also provide insightful evidence to investors, crypto traders, and portfolio managers in terms of hedging strategy, diversification and risk aversion [

Citation: Kuo-Shing Chen, Wei-Chen Ong. Dynamic correlations between Bitcoin, carbon emission, oil and gold markets: New implications for portfolio management[J]. AIMS Mathematics, 2024, 9(1): 1403-1433. doi: 10.3934/math.2024069

In this paper, we aim to uncover the dynamic spillover effects of Bitcoin environmental attention (EBEA) on major asset classes: Carbon emission, crude oil and gold futures, and analyze whether the integration of Bitcoin into portfolio allocation performance. In this study, we document the properties of futures assets and empirically investigate their dynamic correlation between Bitcoin, carbon emission, oil and gold futures. Overall, it is evident that the volatility of Bitcoin, as well as other prominent returns, exhibit an asymmetric response to good and bad news. Additionally, we evaluate the hedge potential benefits of these emerging futures assets for market participants. The evidence supports the idea that the leading cryptocurrency-Bitcoin can be a suitable hedge instrument after the COVID-19 pandemic outbreak. More importantly, our analysis of the portfolio's performance shows that carbon emission futures are diversification benefit products in most of the considered cases. Notably, incorporating carbon futures into portfolios may attract new investors to carbon markets for double goals of risk diversification. These findings also provide insightful evidence to investors, crypto traders, and portfolio managers in terms of hedging strategy, diversification and risk aversion [

| [1] |

M. K. Hassan, M. B. Hasan, Z. A. Halim, N. Maroney, M. M. Rashid, Exploring the dynamic spillover of cryptocurrency environmental attention across the commodities, green bonds, and environment-related stocks, N. Am. J. Econ. Financ., 61 (2022), 101700. https://doi.org/10.1016/j.najef.2022.101700 doi: 10.1016/j.najef.2022.101700

|

| [2] |

M. P. Yadav, S. Kumar, D. Mukherjee, P. Rao, Do green bonds offer a diversification opportunity during COVID-19?—an empirical evidence from energy, crypto, and carbon markets, Environ. Sci. Pollut. Res., 30 (2023), 7625−7639. https://doi.org/10.1007/s11356-022-22492-0 doi: 10.1007/s11356-022-22492-0

|

| [3] |

C. Stoll, L. Klaaßen, U. Gallersdörfer, The carbon footprint of bitcoin, Joule, 3 (2019), 1647−1661. https://doi.org/10.1016/j.joule.2019.05.012 doi: 10.1016/j.joule.2019.05.012

|

| [4] |

E. Symitsi, K. J. Chalvatzis, Return, volatility and shock spillovers of Bitcoin with energy and technology companies, Econ. Lett., 170 (2018), 27−130. https://doi.org/10.1016/j.econlet.2018.06.012 doi: 10.1016/j.econlet.2018.06.012

|

| [5] |

D. I. Okorie, B. Lin, Crude oil price and cryptocurrencies: Evidence of volatility connectedness and hedging strategy, Energy Econ., 87 (2020), 104703. https://doi.org/10.1016/j.eneco.2020.104703 doi: 10.1016/j.eneco.2020.104703

|

| [6] |

I. Yousaf, R. Patel, L. Yarovaya, The reaction of G20+ stock markets to the Russia-Ukraine conflict "black-swan" event: Evidence from event study approach, J. Behav. Exp. Financ., 35 (2022), 100723. https://doi.org/10.1016/j.jbef.2022.100723 doi: 10.1016/j.jbef.2022.100723

|

| [7] |

M. A. Naeem, S. Karim, Tail dependence between bitcoin and green financial assets, Econ. Lett., 208 (2021), 110068. https://doi.org/10.1016/j.econlet.2021.110068 doi: 10.1016/j.econlet.2021.110068

|

| [8] |

W. Mensi, M. A. Naeem, X. V. Vo, S. H. Kang, Dynamic and frequency spillovers between green bonds, oil and G7 stock markets: Implications for risk management, Econ. Anal. Policy, 73 (2022), 331−344. https://doi.org/10.1016/j.eap.2021.11.015 doi: 10.1016/j.eap.2021.11.015

|

| [9] |

K. C. Lu, K. S. Chen, Uncovering information linkages between Bitcoin, sustainable finance and the impact of COVID-19: Fractal and Entropy analysis, Fractal Fract., 7 (2023), 424. https://doi.org/10.3390/fractalfract7060424 doi: 10.3390/fractalfract7060424

|

| [10] | M. Nerlinger, S. Utz, The impact of the Russia—Ukraine conflict on the green energy transition–A capital market perspective, Swiss Financ. Inst. Res., 22 (2022), 49. Available from: https://ssrn.com/abstract = 4132666. |

| [11] |

R. Ibar-Alonso, R. Quiroga-García, M. Arenas-Parra, Opinion mining of green energy sentiment: A Russia-Ukraine conflict analysis, Mathematics, 10 (2022), 2532. https://doi.org/10.3390/math10142532 doi: 10.3390/math10142532

|

| [12] |

A. Dutta, D. Das, R. K. Jana, X. V. Vo, COVID-19 and oil market crash: Revisiting the safe haven property of gold and Bitcoin, Resour. Policy, 69 (2020), 101816. https://doi.org/10.1016/j.resourpol.2020.101816 doi: 10.1016/j.resourpol.2020.101816

|

| [13] |

I. Yousaf, R. Nekhili, M. Umar, Extreme connectedness between renewable energy tokens and fossil fuel markets, Energy Econ., 114 (2022), 106305. https://doi.org/10.1016/j.eneco.2022.106305 doi: 10.1016/j.eneco.2022.106305

|

| [14] |

R. Zha, L. Yu, Y. Su, H. Yin, Dependences and risk spillover effects between Bitcoin, crude oil and other traditional financial markets during the COVID-19 outbreak, Environ. Sci. Pollut. Res., 30 (2023), 40737−40751. https://doi.org/10.1007/s11356-022-25107-w doi: 10.1007/s11356-022-25107-w

|

| [15] |

M. Akhtaruzzaman, A. Sensoy, S. Corbet, The influence of Bitcoin on portfolio diversification and design, Financ. Res. Lett., 37 (2020), 101344. https://doi.org/10.1016/j.frl.2019.101344 doi: 10.1016/j.frl.2019.101344

|

| [16] |

M. Akhtaruzzaman, A. K. Banerjee, V. Le, F. Moussa, Hedging precious metals with impact investing, Int. Rev. Econ. Finance, 89 (2024), 651−664. https://doi.org/10.1016/j.iref.2023.07.047 doi: 10.1016/j.iref.2023.07.047

|

| [17] |

M. Akhtaruzzaman, A. K. Banerjee, S. Boubaker, F. Moussa, Does green improve portfolio optimisation? Energy Econ., 124 (2023), 106831. https://doi.org/10.1016/j.eneco.2023.106831 doi: 10.1016/j.eneco.2023.106831

|

| [18] | L. Charfeddine, N. Benlagha, A time-varying copula approach for modelling dependency: New evidence from commodity and stock markets, J. Multinatl. Financ. Manag., 37 (2016), 168−189. |

| [19] |

P. Wang, W. Zhang, X. Li, D. Shen, Is cryptocurrency a hedge or a safe haven for international indices? A comprehensive and dynamic perspective, Financ. Res. Lett., 31 (2019), 1–18. https://doi.org/10.1016/j.frl.2019.04.031 doi: 10.1016/j.frl.2019.04.031

|

| [20] |

S. J. H. Shahzad, E. Bouri, D. Roubaud, L. Kristoufek, B. Lucey, Is Bitcoin a better safe-haven investment than gold and commodities? Int. Rev. Financ. Anal., 63 (2019), 322–330. https://doi.org/10.1016/j.irfa.2019.01.002 doi: 10.1016/j.irfa.2019.01.002

|

| [21] |

T. Zeng, M. Yang, Y. Shen, Fancy Bitcoin and conventional financial assets: Measuring market integration based on connectedness networks, Econ. Modell., 90 (2020), 209–220. https://doi.org/10.1016/j.econmod.2020.05.003 doi: 10.1016/j.econmod.2020.05.003

|

| [22] |

A. H. Dyhrberg, Bitcoin, gold and the dollar—A GARCH volatility analysis, Financ. Res. Lett., 16 (2016), 85–92. https://doi.org/10.1016/j.frl.2015.10.008 doi: 10.1016/j.frl.2015.10.008

|

| [23] |

J. C. Reboredo, A. Ugolini, The impact of energy prices on clean energy stock prices: A multivariate quantile dependence approach, Energy Econ., 76 (2018), 136–152. https://doi.org/10.1016/j.eneco.2018.10.012 doi: 10.1016/j.eneco.2018.10.012

|

| [24] |

J. A. Batten, G. E. Maddox, M. R. Young, Does weather, or energy prices, affect carbon prices? Energy Econ., 96 (2021), 105016. https://doi.org/10.1016/j.eneco.2020.105016 doi: 10.1016/j.eneco.2020.105016

|

| [25] |

F. Wen, L. Zhao, S. He, G. Yang, Asymmetric relationship between carbon emission trading market and stock market: Evidences from China, Energy Econ., 91 (2020), 104850. https://doi.org/10.1016/j.eneco.2020.104850 doi: 10.1016/j.eneco.2020.104850

|

| [26] |

S. I. Krokida, N. Lambertides, C. S. Savva, D. A. Tsouknidis, The effects of oil price shocks on the prices of EU emission trading system and European stock returns, Eur. J. Financ., 26 (2020), 1–13. https://doi.org/10.1080/1351847X.2019.1637358 doi: 10.1080/1351847X.2019.1637358

|

| [27] |

K. Duan, X. Ren, Y. Shi, T. Mishra, C. Yan, The marginal impacts of energy prices on carbon price variations: evidence from a quantile-on-quantile approach, Energ. Econ., 95 (2021), 105–131. https://doi.org/10.1016/j.eneco.2021.105131 doi: 10.1016/j.eneco.2021.105131

|

| [28] |

M. Balcılar, R. Demirer, S. Hammoudeh, D. K. Nguyen, Risk spillovers across the energy and carbon markets and hedging strategies for carbon risk, Energ. Econ., 54 (2016), 159–172. https://doi.org/10.1016/j.eneco.2015.11.003 doi: 10.1016/j.eneco.2015.11.003

|

| [29] |

G. S. Uddin, J. A. Hernandez, S. J. H. Shahzad, A. Hedström, Multivariate dependence and spillover effects across energy commodities and diversification potentials of carbon assets, Energ. Econ., 71 (2018), 35–46. https://doi.org/10.1016/j.eneco.2018.01.035 doi: 10.1016/j.eneco.2018.01.035

|

| [30] |

T. Klein, H. P. Thu, T. Walther, Bitcoin is not the new gold—A comparison of volatility, correlation, and portfolio performance, Int. Rev. Financ. Anal., 59 (2018), 105–116. https://doi.org/10.1016/j.irfa.2018.07.010 doi: 10.1016/j.irfa.2018.07.010

|

| [31] |

L. Charfeddine, N. Benlagha, Y. Maouchi, Investigating the dynamic relationship between cryptocurrencies and conventional assets: Implications for financial investors, Econ. Model., 85 (2020), 198–217. https://doi.org/10.1016/j.econmod.2019.05.016 doi: 10.1016/j.econmod.2019.05.016

|

| [32] |

E. Bouri, S. J. H. Shahzad, D. Roubaud, L. Kristoufek, B. Lucey, Bitcoin, gold, and commodities as safe havens for stocks: New insight through wavelet analysis, Q. Rev. Econ. Financ., 77 (2020), 156–164. https://doi.org/10.1016/j.qref.2020.03.004 doi: 10.1016/j.qref.2020.03.004

|

| [33] |

T. Conlon, S. Corbet, R. J. McGee, Are cryptocurrencies a safe haven for equity markets? An international perspective from the COVID-19 pandemic, Res. Int. Bus. Financ., 54 (2020), 101248. https://doi.org/10.1016/j.ribaf.2020.101248 doi: 10.1016/j.ribaf.2020.101248

|

| [34] |

J. Cui, A. Maghyereh, Higher-order moment risk connectedness and optimal investment strategies between international oil and commodity futures markets: Insights from the COVID-19 pandemic and Russia-Ukraine conflict, Int. Rev. Financ. Anal., 86 (2023), 102520. https://doi.org/10.1016/j.irfa.2023.102520 doi: 10.1016/j.irfa.2023.102520

|

| [35] |

M. Huang, W. Shao, J. Wang, Correlations between the crude oil market and capital markets under the Russia-Ukraine conflict: A perspective of crude oil importing and exporting countries, Resour. Policy, 80 (2023), 103233. https://doi.org/10.1016/j.resourpol.2022.103233 doi: 10.1016/j.resourpol.2022.103233

|

| [36] |

K. Guesmi, S. Saadi, I. Abid, Z. Ftiti, Portfolio diversification with virtual currency: Evidence from bitcoin, Int. Rev. Financ. Anal., 63 (2019), 431–437. https://doi.org/10.1016/j.irfa.2018.03.004 doi: 10.1016/j.irfa.2018.03.004

|

| [37] | L. Bauwens, G. Storti, F. Violante, Dynamic conditional correlation models for realized covariance matrices, CORE, 60 (2012), 104–108. Available from: https://dial.uclouvain.be. |

| [38] | M. Sahamkhadam, A. Stephan, R. Östermark, Portfolio optimization based on GARCH-EVT-Copula forecasting models, Int. J. Forecast., 34 (2018), 497–506. |

| [39] | A. Díaz, C. Esparcia, R. López, The diversifying role of socially responsible investments during the COVID-19 crisis: A risk management and portfolio performance analysis, Econ. Anal. Policy, 75 (2022), 39–60. |

| [40] | W. Zhang, X. He, S. Hamori, Volatility spillover and investment strategies among sustainability-related financial indexes: Evidence from the DCC-GARCH-based dynamic connectedness and DCC-GARCH t-copula approach, Int. Rev. Financ. Anal., 83 (2022), 102223. |

| [41] | P. Zhang, Z. X. Lv, Z. Pei, Y. Zhao, Systemic risk spillover of financial institutions in China: A copula-DCC-GARCH approach, J. Eng. Res., 2023, 100078. |

| [42] |

M. Arouri, J. Jouini, D. K. Nguyen, Volatility spillovers between oil prices and stock sector returns: Implications for portfolio management, J. Int. Money Financ., 30 (2011), 1387–1405. https://doi.org/10.1016/j.jimonfin.2011.07.008 doi: 10.1016/j.jimonfin.2011.07.008

|

| [43] |

A. Creti, M. Joëts, V. Mignon, On the links between stock and commodity markets' volatility, Energ. Econ., 37 (2013), 16–28. https://doi.org/10.1016/j.eneco.2013.01.005 doi: 10.1016/j.eneco.2013.01.005

|

| [44] |

H. Sun, F. Zou, B. Mo, Does FinTech drive asymmetric risk spillover in the traditional finance? AIMS Math., 7 (2022), 20850–20872. https://doi.org/10.3934/math.20221143 doi: 10.3934/math.20221143

|

| [45] |

L. Cappiello, R. Engle, K. Sheppard, Asymmetric dynamics in the correlations of global equity and bond returns, J. Financ. Econ., 4 (2006), 537–572. https://doi.org/10.1093/jjfinec/nbl005 doi: 10.1093/jjfinec/nbl005

|

| [46] |

L. R. Glosten, R. Jagannathan, D. E. Runkle, On the relation between the expected value and the volatility of the nominal excess return on stocks, J. Financ., 48 (1993), 1779–1801. https://doi.org/10.1111/j.1540-6261.1993.tb05128.x doi: 10.1111/j.1540-6261.1993.tb05128.x

|

| [47] |

R. Engle, Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models, J. Bus. Econ. Stat., 20 (2002), 339–350. https://doi.org/10.1198/073500102288618487 doi: 10.1198/073500102288618487

|

| [48] | M. Sklar, Fonctions de répartition à n dimensions et leurs marges, Univ. Paris, 8 (1959). |

| [49] |

K. F. Kroner, J. Sultan, Time-varying distributions and dynamic hedging with foreign currency futures, J. Financ. Quant. Ann., 28 (1993), 535–551. https://doi.org/10.2307/2331164 doi: 10.2307/2331164

|

| [50] | C. Brooks, O. T. Henry, G. Persand, The effect of asymmetries on optimal hedge ratios, J. Bus., 75 (2002), 333–352. Available from: https://www.jstor.org/stable/10.1086/338484. |

| [51] | H. Markowitz, Portfolio selection, J. Financ., 7 (1952), 77–91. Available from: https://www.jstor.org/stable/2975974. |

| [52] |

H. Markowitz, Mean-variance approximations to expected utility, Eur. J. Oper. Res., 234 (2014), 346–355. https://doi.org/10.1016/j.ejor.2012.08.023 doi: 10.1016/j.ejor.2012.08.023

|

| [53] | N. Jegadeesh, S. Titman, Returns to buying winners and selling losers: Implications for stock market efficiency, J. Finance, 48 (1993), 65–91. |

| [54] |

B. R. I. K. Hatem, J. El Ouakdi, Z. Ftiti, Roles of stable versus nonstable cryptocurrencies in Bitcoin market dynamics, Res. Int. Bus. Financ., 62 (2022), 101720. https://doi.org/10.1016/j.ribaf.2022.101720 doi: 10.1016/j.ribaf.2022.101720

|

| [55] |

N. P. Canh, U. Wongchoti, S. D. Thanh, N. T. Thong, Systematic risk in cryptocurrency market: Evidence from DCC-MGARCH model, Financ. Res. Lett., 29 (2019), 90e100. https://doi.org/10.1016/j.frl.2019.03.011 doi: 10.1016/j.frl.2019.03.011

|

| [56] |

R. F. Engle, K. F. Kroner, Multivariate simultaneous generalized ARCH, Economet. Theor., 11 (1995), 122–150. https://doi.org/10.1017/S0266466600009063 doi: 10.1017/S0266466600009063

|

| [57] |

K. Ng, V. Kroner, Modelling asymmetric movements of asset prices, Rev. Financ. Study, 11 (1998), 844–871. https://doi.org/10.1093/rfs/11.4.817 doi: 10.1093/rfs/11.4.817

|

| [58] |

P. Katsiampa, S. Corbet, B. Lucey, Volatility spillover effects in leading cryptocurrencies: A BEKK-MGARCH analysis, Financ. Res. Lett., 29 (2019), 68–74. https://doi.org/10.1016/j.frl.2019.03.009 doi: 10.1016/j.frl.2019.03.009

|

| [59] |

A. Haffar, É. Le Fur, Time-varying dependence of Bitcoin, Q. Rev. Econ. Financ., 86 (2022), 211–220. https://doi.org/10.1016/j.qref.2022.07.008 doi: 10.1016/j.qref.2022.07.008

|

| [60] | T. Emura, C. W. Lin, W. Wang, A goodness-of-fit test for Archimedean copula models in the presence of right censoring, Comput. Stat. Data Anal., 54 (2010), 3033–3043. |

| [61] | V. Alexeev, K. Ignatieva, T. Liyanage, Dependence modelling in insurance via copulas with skewed generalised hyperbolic marginals, Stud. Nonlinear Dyn. Econ., 25 (2019), 20180094. |

| [62] |

M. Arif, M. Hasan, S. M. Alawi, M. A. Naeem, COVID-19 and time-frequency connectedness between green and conventional financial markets, Glob. Financ. J., 49 (2021), 100650. http://dx.doi.org/10.1016/J.GFJ.2021.100650 doi: 10.1016/J.GFJ.2021.100650

|

| [63] |

G. D. Sharma, T. Sarker, A. Rao, G. Talan, M. Jain, Revisiting conventional and green finance spillover in post-COVID world: Evidence from robust econometric models, Glob. Financ. J., 51 (2022), 100691. http://dx.doi.org/10.1016/J.GFJ.2021.100691 doi: 10.1016/J.GFJ.2021.100691

|

| [64] | X. Sibande, R. Demirer, M. Balcilar, R. Gupta, On the pricing effects of bitcoin mining in the fossil fuel market: The case of coal, Resour. Policy, 85 (2023), 103539. |

Figures(8) / Tables(6)

Kuo-Shing Chen, Wei-Chen Ong. Dynamic correlations between Bitcoin, carbon emission, oil and gold markets: New implications for portfolio management[J]. AIMS Mathematics, 2024, 9(1): 1403-1433. doi: 10.3934/math.2024069

DownLoad:

DownLoad: