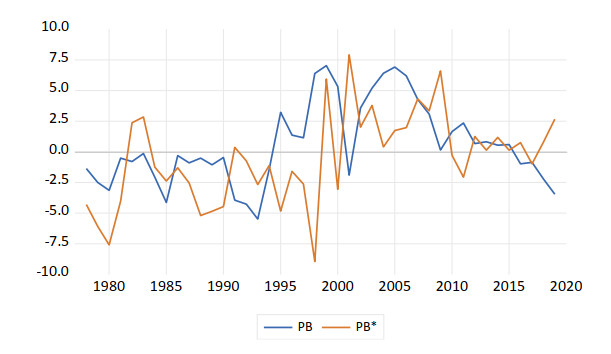

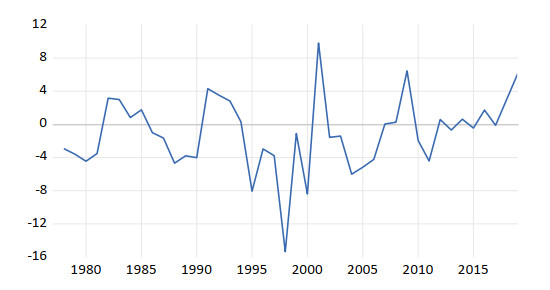

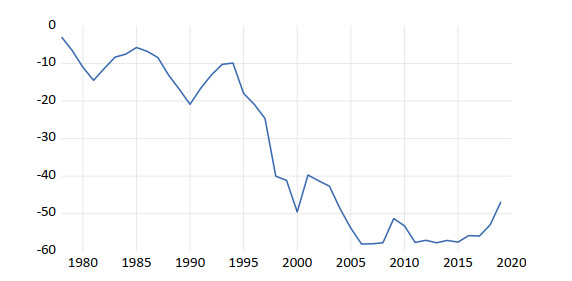

This study gauges the degree of fiscal vulnerability in Turkey by calculating the debt stabilising primary balance level and evaluates how this variable measures up against the actual primary balance levels for the 1978–2019 period. Based on this comparison, we build up a fiscal fragility index using the methodology described in

Citation: Cansın Kemal CAN. How vulnerable is the fiscal posture in Turkey?[J]. Green Finance, 2021, 3(3): 319-336. doi: 10.3934/GF.2021016

This study gauges the degree of fiscal vulnerability in Turkey by calculating the debt stabilising primary balance level and evaluates how this variable measures up against the actual primary balance levels for the 1978–2019 period. Based on this comparison, we build up a fiscal fragility index using the methodology described in

| [1] |

Afonso A, Jalles TJ (2016) The elusive character of fiscal sustainability. Appl Econ 48: 2651-2664. doi: 10.1080/00036846.2015.1128074

|

| [2] | Alesina A, Campante FR, Tabellini G (2008) Why is fiscal policy often procyclical? J Eur Econ Assoc 6: 1006-1036. |

| [3] |

Argitis G, Nikolaidi M (2014) The financial fragility and the crisis of the greek government sector. Int Rev Appl Econ 28: 274-292. doi: 10.1080/02692171.2013.858667

|

| [4] | Baldacci E, McHugh J, Petrova I K (2011B) Measuring fiscal vulnerability and fiscal stress: a proposed set of indicators. IMF Working Pap, 1-20. |

| [5] | Baldacci E, Petrova IK, Belhocine N, et al. (2011A) Assessing fiscal stress. IMF Working Pap, 1-41. |

| [6] |

Burger P, Stuart I, Jooste C, et al. (2012) Fiscal sustainability and the fiscal reaction function for south africa: assesment of the past and future policy. S Afr J Econ 80: 1-19. doi: 10.1111/j.1813-6982.2012.01321.x

|

| [7] | Celasun M, Rodrik D (1989) Turkish experience with debt: macroeconomic policy and performance. Nat Bur Econ Res, 193-211. |

| [8] | Herrera-Ramos MC, Prats MA (2020) Fiscal sustainability in the european countries: a panel ARDL approach and a dynamic panel threshold model. Sustainability 12: 8505. |

| [9] | Horne J (1991) Indicators of Fiscal Sustainability. IMF Working Pap 1991: 1-34. |

| [10] |

Karlsson HK (2020) Investigation of the time-dependent dynamics between government revenue and expenditure in China: a wavelet approach. J Asia Pac Econ 25: 250-269. doi: 10.1080/13547860.2019.1646573

|

| [11] | Nikolaidi M (2014) Essays on Financial Fragility, Instability and Macroeconomy. (Doctoral dissertation). Athens: National and Kapodistrian University of Athens. |

| [12] | Rodriguez AC (2014) Is There a Relationship between Fiscal Sustainability and Currency Crises? International Evidence-Based on Causality Tests. Int J Econ Sci Appl Res 7: 69-87. |

| [13] |

Shevchuk V, Kopych R (2018) Assessing the Fiscal Sustainability in Ukraine: TVP and VAR/VEC approaches. Entrepreneurial Bus Econ Rev 6: 73-87. doi: 10.15678/EBER.2018.060305

|

| [14] | Stoian A. (2011) A Simple Public Debt Dynamic Model for Assessing Fiscal Vulnerability: Empirical Evidence for EU Countries. Res Appl Econ 3: E3. |

| [15] | Stoian A (2012) How vulnerable is fiscal policy in Central and Eastern European countries? Romanian J Fiscal Policy 3: 68-81. |

| [16] | Stoian A, Obreja Brașoveanu L, Brașoveanu IV, et al. (2018). A Framework to Assess Fiscal Vulnerability: Empirical Evidence for European Union Countries. Sustainability 10: 2482. |

| [17] | Stoian A, Obreja Brașoveanu L, Dumitrescu B, et al. (2015). A new framework for detecting the short-term fiscal vulnerability for the European Union countries. MPRA Paper. |

| [18] | Tanzi V, Schuknecht L (1997) Reconsidering the Fiscal Role of Government: The International Perspective. Am Econ Rev 87: 164-168. |

| [19] |

Toda H Y, Yamamoto T (1995) Statistical inference in vector autoregressions with possibly integrated processes. J Economet 66: 225-250. doi: 10.1016/0304-4076(94)01616-8

|

| [20] |

Terra FHB, Ferrari-Filho F (2020) Public Sector Financial Fragility Index: an analysis of the Brazilian federal government from 2000 to 2016. J Post Keynesian Econ 44: 365-389. doi: 10.1080/01603477.2020.1713006

|

| [21] | Voyvoda E, Yeldan E (2015) Aspects of Fiscal Policy in Turkey. Ankara: Financialisation, Economy, Society and Sustainable Development Working Paper Series No.109. |

| [22] | Zarei Z (2018) Cross Effect between Fiscal Sustainability and Financial Stability in Iran. Monetary and Banking Research Institute Central Bank of the Islamic Republic of Iran MBRI PP-97005. |

Figures(8) / Tables(3)

Cansın Kemal CAN. How vulnerable is the fiscal posture in Turkey?[J]. Green Finance, 2021, 3(3): 319-336. doi: 10.3934/GF.2021016

DownLoad:

DownLoad: