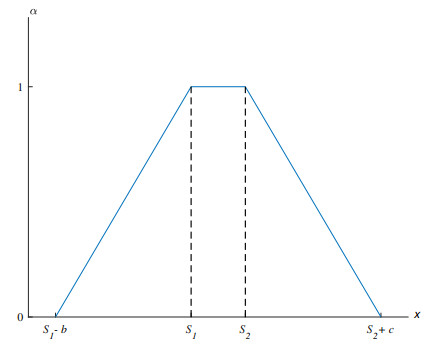

In this paper, we develop a Malliavin calculus approach for hedging a fixed strike lookback option in fuzzy space. Due to the uncertainty in financial markets, it is not accurate to describe the problems of option pricing and hedging in terms of randomness alone. We consider a fuzzy pricing model by introducing a fuzzy stochastic differential equation with Skorohod sense. In this way, our model simultaneously involves randomness and fuzziness. A well-known hedging strategy for vanilla options is so-called $ \Delta $-hedging, which is usually derived from the Itô formula and some properties of partial differentiable equations. However, when dealing with some complex path-dependent options (such as lookback options), the major challenge is that the payoff function of these options may not be smooth, resulting in the estimates are computationally expensive. With the help of the Malliavin derivative and the Clark-Ocone formula, the difficulty will be readily solved, and it is also possible to apply this hedging strategy to fuzzy space. To obtain the explicit expression of the fuzzy hedging portfolio for lookback options, we adopt the Esscher transform and reflection principle techniques, which are beneficial to the calculation of the conditional expectation of fuzzy random variables and the payoff function with extremum, respectively. Some numerical examples are performed to analyze the sensitivity of the fuzzy hedging portfolio concerning model parameters and give the permissible range of the expected hedging portfolio of lookback options with uncertainty by a financial investor's subjective judgment.

Citation: Kefan Liu, Jingyao Chen, Jichao Zhang, Yueting Yang. Application of fuzzy Malliavin calculus in hedging fixed strike lookback option[J]. AIMS Mathematics, 2023, 8(4): 9187-9211. doi: 10.3934/math.2023461

In this paper, we develop a Malliavin calculus approach for hedging a fixed strike lookback option in fuzzy space. Due to the uncertainty in financial markets, it is not accurate to describe the problems of option pricing and hedging in terms of randomness alone. We consider a fuzzy pricing model by introducing a fuzzy stochastic differential equation with Skorohod sense. In this way, our model simultaneously involves randomness and fuzziness. A well-known hedging strategy for vanilla options is so-called $ \Delta $-hedging, which is usually derived from the Itô formula and some properties of partial differentiable equations. However, when dealing with some complex path-dependent options (such as lookback options), the major challenge is that the payoff function of these options may not be smooth, resulting in the estimates are computationally expensive. With the help of the Malliavin derivative and the Clark-Ocone formula, the difficulty will be readily solved, and it is also possible to apply this hedging strategy to fuzzy space. To obtain the explicit expression of the fuzzy hedging portfolio for lookback options, we adopt the Esscher transform and reflection principle techniques, which are beneficial to the calculation of the conditional expectation of fuzzy random variables and the payoff function with extremum, respectively. Some numerical examples are performed to analyze the sensitivity of the fuzzy hedging portfolio concerning model parameters and give the permissible range of the expected hedging portfolio of lookback options with uncertainty by a financial investor's subjective judgment.

| [1] | L. Zadeh, Fuzzy sets, Inform. Control, 8 (1965), 338–353. https://doi.org/10.1016/S0019-9958(65)90241-X |

| [2] | P. Nowak, M. Romaniuk, Computing option price for levy process with fuzzy parameters, Eur. J. Oper. Res., 201 (2010), 206–210. https://doi.org/10.1016/j.ejor.2009.02.009 |

| [3] | H. C. Wu, Using fuzzy sets theory and black-scholes formula to generate pricing boundaries of european options, Appl. Math. Comput., 185 (2007), 136–146. https://doi.org/10.1016/j.amc.2006.07.015 |

| [4] | Y. Yoshida, The valuation of european options in uncertain environment, Eur. J. Oper. Res., 145 (2003), 221–229. https://doi.org/10.1016/S0377-2217(02)00209-6 |

| [5] | X. Wang, J. He, A geometric levy model for n-fold compound option pricing in a fuzzy framework, J. Comput. Appl. Math., 306 (2016), 248–264. https://doi.org/10.1016/j.cam.2016.04.021 |

| [6] | H. C. Wu, Pricing european options based on the fuzzy pattern of black-scholes formula, Comput. Oper. Res., 31 (2004), 1069–1081. https://doi.org/10.1016/S0305-0548(03)00065-0 |

| [7] | V. Lakshmikantham, R. Mohapatra, Theory of fuzzy differential equations and inclusions, Nonlinear Anal.-Theor., 1 (2003). https://doi.org/10.1201/9780203011386 |

| [8] |

Y. Feng, Fuzzy stochastic differential systems, Fuzzy Set. Syst., 115 (2000), 351–363. https://doi.org/10.1016/S0165-0114(98)00389-3 doi: 10.1016/S0165-0114(98)00389-3

|

| [9] | O. Kaleva, Fuzzy differential equations, Fuzzy Set. Syst., 24 (1987), 301–317. https://doi.org/10.1016/0165-0114(87)90029-7 |

| [10] |

H. Kwakernaak, Fuzzy random variables—I. definitions and theorems, Inform. Sciences, 15 (1978), 1–29. https://doi.org/10.1016/0020-0255(78)90019-1 doi: 10.1016/0020-0255(78)90019-1

|

| [11] | M. L. Puri, D. A. Ralescu Fuzzy random variables, Read. Fuzzy Set. Intell. Syst., 1993,265–271. https://doi.org/10.1016/B978-1-4832-1450-4.50029-8. |

| [12] |

M. Michta, K. Ł. Świkatek, Two-parameter fuzzy-valued stochastic integrals and equations, Stoch. Anal. Appl., 33 (2015), 1115–1148. https://doi.org/10.1080/07362994.2015.1089516 doi: 10.1080/07362994.2015.1089516

|

| [13] |

M. T. Malinowski, M. Michta, J. Sobolewska, Set-valued and fuzzy stochastic differential equations driven by semimartingales, Nonlinear Anal.-Theor., 79 (2013), 204–220. https://doi.org/10.1016/j.na.2012.11.015 doi: 10.1016/j.na.2012.11.015

|

| [14] | M. T. Malinowski, M. Michta, Stochastic fuzzy differential equations with an application, Kybernetika, 47 (2011), 123–143. |

| [15] |

W. Fei, Existence and uniqueness of solution for fuzzy random differential equations with non-lipschitz coefficients, Inform. Sciences, 177 (2007), 4329–4337. https://doi.org/10.1016/j.ins.2007.03.004 doi: 10.1016/j.ins.2007.03.004

|

| [16] |

M. T. Malinowski, Itô type stochastic fuzzy differential equations with delay, Syst. Control Lett., 61 (2012), 692–701. https://doi.org/10.1016/j.sysconle.2012.02.012 doi: 10.1016/j.sysconle.2012.02.012

|

| [17] |

M. T. Malinowski, Strong solutions to stochastic fuzzy differential equations of Itô type, Math. Comput. Model., 55 (2012), 918–928. https://doi.org/10.1016/j.mcm.2011.09.018 doi: 10.1016/j.mcm.2011.09.018

|

| [18] |

M. T. Malinowski, Some properties of strong solutions to stochastic fuzzy differential equations, Inform. Sciences, 252 (2013), 62–80. https://doi.org/10.1016/j.ins.2013.02.053 doi: 10.1016/j.ins.2013.02.053

|

| [19] |

W. Fei, H. Liu, W. Zhang, On solutions to fuzzy stochastic differential equations with local martingales, Syst. Control Lett., 65 (2014), 96–105. https://doi.org/10.1016/j.sysconle.2013.12.009 doi: 10.1016/j.sysconle.2013.12.009

|

| [20] |

H. Jafari, Sensitivity of option prices via fuzzy malliavin calculus, Fuzzy Set. Syst., 434 (2022), 98–116. https://doi.org/10.1016/j.fss.2021.11.005 doi: 10.1016/j.fss.2021.11.005

|

| [21] |

H. Li, A. Ware, L. Di, G. Yuan, A. Swishchuk, S. Yuan, The application of nonlinear fuzzy parameters pde method in pricing and hedging european options, Fuzzy Set. Syst., 331 (2018), 14–25. https://doi.org/10.1016/j.fss.2016.12.005 doi: 10.1016/j.fss.2016.12.005

|

| [22] |

X. Yu, W. Huang, Y. Tan, L. Liu, The optimal fuzzy portfolio strategy with option hedging, Theor. Math. Appl., 2 (2012), 1–12. https://doi.org/10.1166/asl.2012.2662 doi: 10.1166/asl.2012.2662

|

| [23] | Y. Yoshida, M. Yasuda, J. I. Nakagami, M. Kurano, A new evaluation of mean value for fuzzy numbers and its application to american put option under uncertainty, Fuzzy Set. Syst., 157 (2006), 2614–2626. https://doi.org/10.1016/j.fss.2003.11.022 |

| [24] |

F. Escher, On the probability function in the collective theory of risk, Skand. Aktuar. J., 15 (1932), 175–195. https://doi.org/10.1080/03461238.1932.10405883 doi: 10.1080/03461238.1932.10405883

|

| [25] | H. U. Gerber, E. S. W. Shiu, Option pricing by esscher transforms, HEC Ecole des hautes études commerciales, Paris, 1994. https://doi.org/10.1016/0167-6687(95)97170-Y |

| [26] |

L. Stefanini, L. Sorini, M. L. Guerra, W. Pedrycz, A. Skowron, V. Kreinovich, Fuzzy numbers and fuzzy arithmetic, Handb. Granul. Comput., 12 (2008), 249–284. https://doi.org/10.1002/9780470724163.ch12 doi: 10.1002/9780470724163.ch12

|

| [27] |

B. K. Kim, J. H. Kim, Stochastic integrals of set-valued processes and fuzzy processes, J. Math. Anal. Appl., 236 (1999), 480–502. https://doi.org/10.1006/jmaa.1999.6461 doi: 10.1006/jmaa.1999.6461

|

| [28] |

G. Wang, Y. Zhang, The theory of fuzzy stochastic processes, Fuzzy Set. Syst., 51 (1992), 161–178. https://doi.org/10.1016/0165-0114(92)90189-B doi: 10.1016/0165-0114(92)90189-B

|

| [29] |

Y. K. Kim, Measurability for fuzzy valued functions, Fuzzy Set. Syst., 129 (1993), 105–109. https://doi.org/10.1016/S0165-0114(01)00121-X doi: 10.1016/S0165-0114(01)00121-X

|

| [30] |

J. Li, J. Wang, Fuzzy set-valued stochastic lebesgue integral, Fuzzy Set. Syst., 200 (2012), 48–64. https://doi.org/10.1016/j.fss.2012.01.021 doi: 10.1016/j.fss.2012.01.021

|

| [31] |

H. Jafari, H. Farahani, M. Paripour, Fuzzy malliavin derivative and linear skorohod fuzzy stochastic differential equation, J. Intell. Fuzzy Syst., 35 (2018), 2447–2458. https://doi.org/10.3233/JIFS-18043 doi: 10.3233/JIFS-18043

|

| [32] | M. Kisielewicz, Differential inclusions and optimal control, Springer, Netherlands, 1991. |

| [33] |

M. T. Malinowski, M. Michta, Fuzzy stochastic integral equations, Dyn. Syst. Appl., 19 (2010), 473. https://doi.org/10.1016/j.amc.2013.05.040 doi: 10.1016/j.amc.2013.05.040

|

| [34] | B. Bede, L. Stefanini, Generalized differentiability of fuzzy-valued functions, Fuzzy Set. Syst., 230 (2013), 119–141. https://doi.org/10.1016/j.fss.2012.10.003 |

| [35] | L. T. Gomes, L. C. Barros, A note on the generalized difference and the generalized differentiability, Fuzzy Set. Syst., 280 (2015), 142–145. https://doi.org/10.1016/j.fss.2015.02.015 |

| [36] | I. Nourdin, G. Peccati, Normal approximations with Malliavin calculus: From Stein's method to universality, Cambridge University Press, USA, 2012. http://dx.doi.org/10.1017/CBO9781139084659.003 |

| [37] | G. D. Nunno, B. Øksendal, F. Proske, Malliavin calculus for Lévy processes with applications to finance, Springer, Berlin, 2009. https://doi.org/10.1007/978-3-540-78572-9 |

| [38] |

D. Nualart, É. Pardoux, Stochastic calculus with anticipating integrands, Prob. Theory Rel., 78 (1988), 535–581. https://doi.org/10.1007/BF00353876 doi: 10.1007/BF00353876

|

| [39] |

H. P. Bermin, Hedging lookback and partial lookback options using malliavin calculus, Appl. Math. Financ., 7 (2000), 75–100. https://doi.org/10.1080/13504860010014052 doi: 10.1080/13504860010014052

|

| [40] |

H. Lee, E. Kim, B. Ko, Valuing lookback options with barrier, N. Am. J. Econ. Financ., 60 (2022), 101660. https://doi.org/10.1016/j.najef.2022.101660 doi: 10.1016/j.najef.2022.101660

|

| [41] |

W. Zhang, Z. Li, Y. Liu, Y. Zhang, Pricing European option under fuzzy mixed fractional brownian motion model with jumps, Comput. Econ., 58 (2021), 483–515. https://doi.org/10.1007/s10614-020-10043-z doi: 10.1007/s10614-020-10043-z

|

Figures(3) / Tables(1)

Kefan Liu, Jingyao Chen, Jichao Zhang, Yueting Yang. Application of fuzzy Malliavin calculus in hedging fixed strike lookback option[J]. AIMS Mathematics, 2023, 8(4): 9187-9211. doi: 10.3934/math.2023461

DownLoad:

DownLoad: