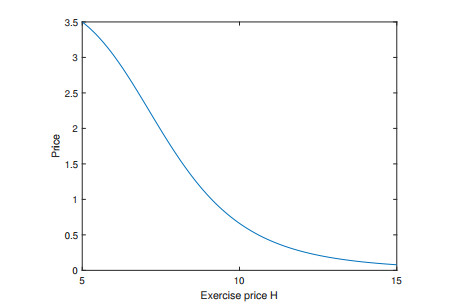

Binary options have a payoff that is either a fixed value or nothing at all. In this paper, the generalized pricing formulas of binary options, including European binary call options, European binary put options, American binary call options and American binary put options, are investigated in uncertain financial markets. By applying the Liu's stock model to describe the stock price, the explicit pricing formulas of binary options are derived successfully. Besides, the corresponding numerical examples for the above four kinds of binary options are discussed in this paper.

Citation: Ming Yang, Yin Gao. Pricing formulas of binary options in uncertain financial markets[J]. AIMS Mathematics, 2023, 8(10): 23336-23351. doi: 10.3934/math.20231186

Binary options have a payoff that is either a fixed value or nothing at all. In this paper, the generalized pricing formulas of binary options, including European binary call options, European binary put options, American binary call options and American binary put options, are investigated in uncertain financial markets. By applying the Liu's stock model to describe the stock price, the explicit pricing formulas of binary options are derived successfully. Besides, the corresponding numerical examples for the above four kinds of binary options are discussed in this paper.

| [1] |

P. W. Buchen, The pricing of dual-expiry exotics, Quant. Financ., 4 (2004), 101–108. https://doi.org/10.1088/1469-7688/4/1/009 doi: 10.1088/1469-7688/4/1/009

|

| [2] |

L. V. Ballestra, Repeated spatial extrapolation: An extraordinarily efficient approach for option pricing, J. Comput. Appl. Math., 256 (2014), 83–91. https://doi.org/10.1016/j.cam.2013.07.033 doi: 10.1016/j.cam.2013.07.033

|

| [3] | X. W. Chen, American option pricing formula for uncertain financial market, Int. J. Oper. Res., 8 (2011), 27–32. |

| [4] |

Y. Gao, X. F. Yang, Z. F. Fu, Lookback option pricing problem of uncertain exponential Ornstein–Uhlenbeck model, Soft Comput., 22 (2018), 5647–5654. https://doi.org/10.1007/s00500-017-2558-y doi: 10.1007/s00500-017-2558-y

|

| [5] |

R. Gao, W. Wu, C. Lang, L. Y. Lang, Geometric Asian barrier option pricing formulas of uncertain stock model, Chaos Solitons Fract., 140 (2020), 110178. https://doi.org/10.1016/j.chaos.2020.110178 doi: 10.1016/j.chaos.2020.110178

|

| [6] |

Y. Gao, L. F. Jia, Pricing formulas of barrier-lookback option in uncertain financial markets, Chaos Solitons Fract., 147 (2021), 110986. https://doi.org/10.1016/j.chaos.2021.110986 doi: 10.1016/j.chaos.2021.110986

|

| [7] | H. C. O, D. H. Kim, J. J. Jo, S. H. Ri, Integrals of higher binary options and defaultable bonds with discrete default information, Electron. J. Math. Anal. Appl., 2 (2014), 190–214. |

| [8] |

L. F. Jia, W. Chen, Knock-in options of an uncertain stock model with floating interest rate, Chaos Solitons Fract., 141 (2020), 110324. https://doi.org/10.1016/j.chaos.2020.110324 doi: 10.1016/j.chaos.2020.110324

|

| [9] |

T. Jin, H. Ding, H. X. Xia, J. F. Bao, Reliability index and Asian barrier option pricing formulas of the uncertain fractional first-hitting time model with Caputo type, Chaos Solitons Fract., 142 (2021), 110409. https://doi.org/10.1016/j.chaos.2020.110409 doi: 10.1016/j.chaos.2020.110409

|

| [10] | B. D. Liu, Uncertainty theory, 2 Eds., Berlin, Heidelberg: Springer, 2007. https://doi.org/10.1007/978-3-540-73165-8 |

| [11] |

B. D. Liu, Toward uncertain finance theory, J. Uncertain. Anal. Appl., 1 (2013), 1–15. https://doi.org/10.1186/2195-5468-1-1 doi: 10.1186/2195-5468-1-1

|

| [12] | M. Rubinstein, E. Reiner, Unscrambling the binary code, Risk, 4 (1991), 75–83. |

| [13] |

J. J. Sun, X. W. Chen, Asian option pricing formula for uncertain financial market, J. Uncertain. Anal. Appl., 3 (2015), 1–11. https://doi.org/10.1186/s40467-015-0035-7 doi: 10.1186/s40467-015-0035-7

|

| [14] |

M. Tian, X. F. Yang, Y. Zhang, Barrier option pricing of mean-reverting stock model in uncertain environment, Math. Comput. Simul., 166 (2019), 126–143. https://doi.org/10.1016/j.matcom.2019.04.009 doi: 10.1016/j.matcom.2019.04.009

|

| [15] |

M. Tian, X. Y. Yang, Y. Zhang, Lookback option pricing problem of mean-reverting stock model in uncertain environment, J. Ind. Manag. Optim., 17 (2021), 2703–2714. https://doi.org/10.3934/jimo.2020090 doi: 10.3934/jimo.2020090

|

| [16] |

K. Yao, X. W. Chen, A numerical method for solving uncertain differential equations, J. Intell. Fuzzy Syst., 25 (2013), 825–832. https://doi.org/10.3233/IFS-120688 doi: 10.3233/IFS-120688

|

| [17] |

X. F. Yang, Z. Q. Zhang, X. Gao, Asian-barrier option pricing formulas of uncertain financial market, Chaos Soliton Fract., 123 (2019), 79–86. https://doi.org/10.1016/j.chaos.2019.03.037 doi: 10.1016/j.chaos.2019.03.037

|

| [18] |

K. Yao, Z. F. Qin, Barrier option pricing formulas of an uncertain stock model, Fuzzy Optim. Decis. Making, 20 (2021), 81–100. https://doi.org/10.1007/s10700-020-09333-w doi: 10.1007/s10700-020-09333-w

|

| [19] | Z. Q. Zhang, W. Q. Liu, Geometric average Asian option pricing for uncertain financial market, J. Uncertain Syst., 8 (2014), 317–320. |

| [20] |

Z. Q. Zhang, W. Q. Liu, Y. H. Sheng, Valuation of power option for uncertain financial market, Appl. Math. Comput., 286 (2016), 257–264. https://doi.org/10.1016/j.amc.2016.04.032 doi: 10.1016/j.amc.2016.04.032

|

| [21] |

Z. Q. Zhang, H. Ke, W. Q. Liu, Lookback options pricing for uncertain financial market, Soft Comput., 23 (2019), 5537–5546. https://dx.doi.org/10.1007/s00500-018-3211-0 doi: 10.1007/s00500-018-3211-0

|

Figures(4)

Ming Yang, Yin Gao. Pricing formulas of binary options in uncertain financial markets[J]. AIMS Mathematics, 2023, 8(10): 23336-23351. doi: 10.3934/math.20231186

DownLoad:

DownLoad: