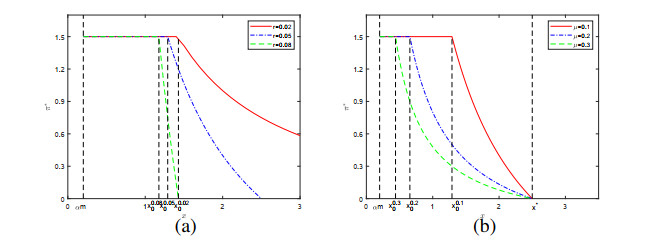

We study the optimal investment problem in a constrained financial market,where the proportion of borrowed amount to the current wealth level is no more than a given constant. The objective is to maximize the goal-reaching probability before drawdown,namely,the probability that the value of the wealth process reaches the safe level before hitting a lower dynamic barrier. The financial market consists of a risk-free asset and multiple risky assets. By the construction of auxiliary market and convex analysis,we relax the borrowing constraint and investigate the new optimization problem in an auxiliary market,where there is no such borrowing constraint. Then,we find the relationship between the optimal results in auxiliary market and those in constrained market. The explicit expressions for the optimal investment strategy and the maximum goal-reaching probability before drawdown are derived in closed-form. Finally,we provide some numerical examples to show the effect of model parameters on the behaviors of investor.

Citation: Yu Yuan, Qicai Li. Maximizing the goal-reaching probability before drawdown with borrowing constraint[J]. AIMS Mathematics, 2021, 6(8): 8868-8882. doi: 10.3934/math.2021514

We study the optimal investment problem in a constrained financial market,where the proportion of borrowed amount to the current wealth level is no more than a given constant. The objective is to maximize the goal-reaching probability before drawdown,namely,the probability that the value of the wealth process reaches the safe level before hitting a lower dynamic barrier. The financial market consists of a risk-free asset and multiple risky assets. By the construction of auxiliary market and convex analysis,we relax the borrowing constraint and investigate the new optimization problem in an auxiliary market,where there is no such borrowing constraint. Then,we find the relationship between the optimal results in auxiliary market and those in constrained market. The explicit expressions for the optimal investment strategy and the maximum goal-reaching probability before drawdown are derived in closed-form. Finally,we provide some numerical examples to show the effect of model parameters on the behaviors of investor.

| [1] |

B. Angoshtari, E. Bayraktar, V. R. Young, Optimal investment to minimize the probability of drawdown, Stochastics, 88 (2016), 946–958. doi: 10.1080/17442508.2016.1155590

|

| [2] |

B. Angoshtari, E. Bayraktar, V. R. Young, Minimizing the probability of lifetime drawdown under constant consumption, Insur. Math. Econ., 69 (2016), 210–223. doi: 10.1016/j.insmatheco.2016.05.007

|

| [3] |

E. Bayraktar, V. R. Young, Minimizing the probability of lifetime ruin under borrowing constraints, Insur. Math. Econ., 41 (2007), 196–221. doi: 10.1016/j.insmatheco.2006.10.015

|

| [4] |

N. B$\ddot{a}$uerle, Benchmark and mean-variance problems for insurers, Math. Method. Ope. Res., 62 (2005), 159–165. doi: 10.1007/s00186-005-0446-1

|

| [5] | S. Browne, Optimal investment policies for a firm with a random risk process: Exponential utility and minimizing the probaiblity of ruin, Math. Oper. Res., 22 (1995), 468–493. |

| [6] | S. Browne, Survival and growth with a liability: Optimal portfolios in continuous time, Math. Oper. Res., 20 (1997), 937–958. |

| [7] |

X. Chen, D. Landriault, B. Li, D. Li, On minimizing drawdown risks of lifetime investments, Insur. Math. Econ., 65 (2015), 46–54. doi: 10.1016/j.insmatheco.2015.08.007

|

| [8] |

C. Hipp, M. Taksar, Optimal non-proportional reinsurance, Insur. Math. Econ., 47 (2010), 246–254. doi: 10.1016/j.insmatheco.2010.04.001

|

| [9] |

X. Han, Z. Liang, K. C. Yuen, Optimal proportional reinsurance to minimize the probability of drawdown under thinning-dependence structure, Scand. Actuar. J., 2018 (2018), 863–889. doi: 10.1080/03461238.2018.1469098

|

| [10] |

X. Han, Z. Liang, C. Zhang, Optimal proportional reinsurance with common shock dependence to minimise the probability of drawdown, Annals of Actuarial Science, 13 (2019), 268–294. doi: 10.1017/S1748499518000210

|

| [11] |

X. Han, Z. Liang, Optimla reinsurance and investment in danager and safe-region, Optima. Contr. Appl. Met., 41 (2020), 765–792. doi: 10.1002/oca.2568

|

| [12] | I. Karatzas, S. Shreve, Method of mathematical finance, New York: Springer, 1998. |

| [13] |

S. Luo, Ruin Minimization for Insurers with Borrowing Constrainsts, N. Am. Actuar. J., 12 (2008), 143–174. doi: 10.1080/10920277.2008.10597508

|

| [14] |

R. C. Merton, Lifetime portfolio selection under uncertainty: The continuoustime case, Rev. Econ. Stat., 51 (1969), 247–257. doi: 10.2307/1926560

|

| [15] |

S. D. Promislow, V. R. Young, Minimizing the probability of ruin when claims follow Brownian motion with drift, N. Am. Actuar. J., 9 (2005), 110–128. doi: 10.1080/10920277.2005.10596214

|

| [16] | R. T. Rockafellar, Convex analysis, Princeton University Press, 1970. |

| [17] |

H. Sun, Z. Sun, Y. Huang, Equilibrium investment and risk control for an insurer with non-Markovian regime-switching and no-shorting constraints, AIMS Mathematics, 5 (2020), 6996–7013. doi: 10.3934/math.2020449

|

| [18] |

H. Yener, Minimizing the lifetime ruin under borrowing and short-selling constraints, Scand. Actuar. J., 2014 (2014), 535–560. doi: 10.1080/03461238.2012.745448

|

| [19] |

H. Yener, Maximizing survival, growth and goal reaching under borrowing constraints, Quant. Financ., 15 (2015), 2053–2065. doi: 10.1080/14697688.2014.972435

|

| [20] | Y. Yuan, Z. Liang, X. Han, Optimal investment and reinsurance to minimize the probability of drawdown with borrowing costs, J. Ind. Manag. Optim., 2021, Doi: 10.3934/jimo.2021003. |

| [21] | Y. Yuan, H. Mi, H. Chen, Mean-variance problem for an insurer with dependent risks and stochastic interest rate in a jump-diffusion market, Optimization, 2021, Doi: 10.1080/02331934.2021.1887179. |

| [22] |

X. Zhang, H. Meng, Y. Zeng, Optimal investment and reinsurance strategies for insurers with generalized mean-variance premium principle and no-short selling, Insur. Math. Econ., 67 (2016), 125–132. doi: 10.1016/j.insmatheco.2016.01.001

|

Figures(3)

Yu Yuan, Qicai Li. Maximizing the goal-reaching probability before drawdown with borrowing constraint[J]. AIMS Mathematics, 2021, 6(8): 8868-8882. doi: 10.3934/math.2021514

DownLoad:

DownLoad: