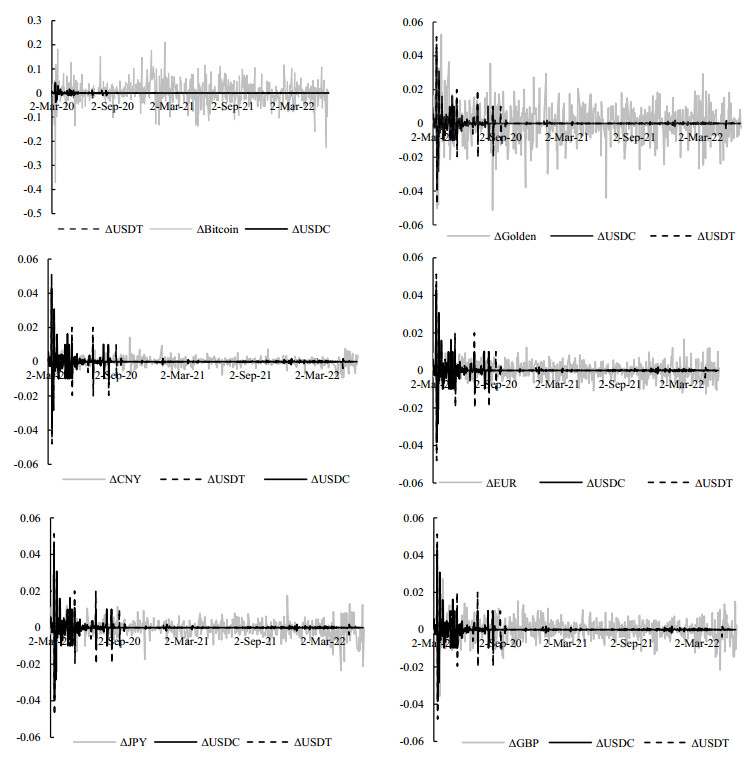

With the continuous expansion of their market size and scope of use, the monetary attribute of stablecoins has become a focal point. The identification of the monetary attribute of stablecoins is a prerequisite for their supervision. Based on the essence and macroeconomic effects of money, this paper analyzes the monetary attribute of stablecoins from theoretical and empirical perspectives. We find that in the traditional financial market, stablecoins are not widely accepted, and their increased supply competes with traditional financial assets. As new types of digital assets, they do not possess a monetary attribute. However, in the digital asset market, stablecoins are widely used. The increase in issuance pushes up asset prices and brings liquidity effects to the market. Therefore, stablecoins possess a monetary attribute in the digital asset market and play the role of "digital fiat currency". This private sector liquidity is not controlled by the government and tends to accumulate risk. Therefore, the government should clarify the legal attribute of stablecoins according to their monetary attribute, strengthen the supervision of stablecoin issuers and prevent the private sector from monopolizing the digital asset market transaction medium.

Citation: Meng Fan, Jinping Dai. Monetary attribute of stablecoins: A theoretical and empirical test[J]. National Accounting Review, 2023, 5(3): 261-281. doi: 10.3934/NAR.2023016

With the continuous expansion of their market size and scope of use, the monetary attribute of stablecoins has become a focal point. The identification of the monetary attribute of stablecoins is a prerequisite for their supervision. Based on the essence and macroeconomic effects of money, this paper analyzes the monetary attribute of stablecoins from theoretical and empirical perspectives. We find that in the traditional financial market, stablecoins are not widely accepted, and their increased supply competes with traditional financial assets. As new types of digital assets, they do not possess a monetary attribute. However, in the digital asset market, stablecoins are widely used. The increase in issuance pushes up asset prices and brings liquidity effects to the market. Therefore, stablecoins possess a monetary attribute in the digital asset market and play the role of "digital fiat currency". This private sector liquidity is not controlled by the government and tends to accumulate risk. Therefore, the government should clarify the legal attribute of stablecoins according to their monetary attribute, strengthen the supervision of stablecoin issuers and prevent the private sector from monopolizing the digital asset market transaction medium.

| [1] | Amar AB (2019) The Effectiveness of Monetary Policy Transmission in a Dual Banking System: further Insights from TVP-VAR Model. Econ Bull 39: 2317–2332. |

| [2] | Arner DW, Auer R, Frost J (2020) Stablecoins: Risks, Potential and Regulation. BIS Working Paper. |

| [3] | Auer R, Böhme R (2020) CBDC Architectures, the Financial System, and the Central Bank of the Future. Available from: https://cepr.org/voxeu/columns/cbdc-architectures-financial-system-and-central-bank-future. |

| [4] | Bianchi D, Rossini L, Iacopini M (2020) Stablecoins and Cryptocurrency Returns: Evidence from Large Bayesian Vars. https://doi.org/10.2139/ssrn.3605451 |

| [5] |

Bojaj MM, Muhadinovic M, Bracanovic A, et al. (2022) Forecasting Macroeconomic Effects of Stablecoin Adoption: A Bayesian Approach. Econ Model 109: 105792. https://doi.org/10.1016/j.econmod.2022.105792 doi: 10.1016/j.econmod.2022.105792

|

| [6] |

Bouri E, Das M, Gupta R, et al. (2018) Spillovers between Bitcoin and Other Assets During Bear and Bull Markets. Appl Econ 50: 5935–5949. https://doi.org/10.1080/00036846.2018.1488075 doi: 10.1080/00036846.2018.1488075

|

| [7] |

Conrad C, Custovic A, Ghysels E (2018) Long- and Short-Term Cryptocurrency Volatility Components: a GARCH-MIDAS Analysis. J Risk Financ Manag 11. https://doi.org/10.3390/jrfm11020023 doi: 10.3390/jrfm11020023

|

| [8] |

Corbet S, Meegan A, Larkin C, et al. (2018) Exploring the Dynamic Relationships Between Cryptocurrencies and Other Financial Assets. Econ Lett 165: 28–34. https://doi.org/10.1016/j.econlet.2018.01.004 doi: 10.1016/j.econlet.2018.01.004

|

| [9] |

Eichengreen B (2019) From Commodity to Fiat and Now to Crypto: What Does History Tell Us? National Bureau of Economic Research. https://doi.org/10.3386/w25426 doi: 10.3386/w25426

|

| [10] | Financial Stability Board (2019) Regulatory Issues of Stablecoins. Available from: https://www.fsb.org/wp-content/uploads/P181019.pdf. |

| [11] | Gorton GB, Ross CP, Ross SY (2022) Making Money. National Bureau of Economic Research. https://doi.org/10.3386/w29710 |

| [12] |

Griffin JM, Shams A (2019) Is Bitcoin Really Untethered? The Journal of Finance 75: 1913–1964. https://doi.org/10.1111/jofi.12903 doi: 10.1111/jofi.12903

|

| [13] | Hileman G (2019) State of Stablecoins. |

| [14] |

Kristoufek L (2021) Tethered, or Untethered? On the Interplay Between Stablecoins and Major Cryptoassets. Finance Res Lett 43: 101991. https://doi.org/10.1016/j.frl.2021.101991 doi: 10.1016/j.frl.2021.101991

|

| [15] | Liao GY, Caramichael J (2022) Stablecoins: Growth Potential and Impact on Banking. Available from: https://www.federalreserve.gov/econres/ifdp/files/ifdp1334.pdf. |

| [16] | Lyons RK, Viswanath-Natraj G (2020) What Keeps Stablecoins Stable? National Bureau of Economic Research. Available from: https://www.nber.org/system/files/working_papers/w27136/w27136.pdf. |

| [17] | Mita M, Ito K, Ohsawa S, et al. (2019) What is Stablecoin? A Survey on Price Stabilization Mechanisms for Decentralized Payment Systems. 2019 8th International Congress on Advanced Applied Informatics, 2019. |

| [18] | Nakajima J (2011) Time-Varying Parameter VAR Model with Stochastic Volatility: An Overview of Methodology and Empirical Applications. Available from: https://www.imes.boj.or.jp/research/papers/english/me29-6.pdf. |

| [19] |

Primiceri GE (2005) Time Varying Structural Vector Autoregressions and Monetary Policy. Rev Econ Stud 72: 821–852. https://doi.org/10.1111/j.1467-937X.2005.00353.x doi: 10.1111/j.1467-937X.2005.00353.x

|

| [20] |

Rogalski RJ, Vinso JD (1977) Stock Returns, Money Supply and the Direction of Causality. J Finance 32: 1017–1030. https://doi.org/10.1111/j.1540-6261.1977.tb03306.x doi: 10.1111/j.1540-6261.1977.tb03306.x

|

| [21] | Sokolov M (2020) Are Libra, Tether, MakerDAO and Paxos Issuing E-Money? Analysis of 9 Stablecoin Types Under the EU and UK E-Money Frameworks. Working Paper, 2020. |

| [22] | Tether (2014) Tether: Fiat Currencies on the Bitcoin Blockchain. Available from: https://assets.ctfassets.net/vyse88cgwfbl/5UWgHMvz071t2Cq5yTw5vi/c9798ea8db99311bf90ebe0810938b01/TetherWhitePaper.pdf. |

| [23] | Wallace N (2010) The Mechanism-Design Approach to Monetary Theory, In: Handbook of Monetary Economics 3: 3–23. https://doi.org/10.1016/B978-0-444-53238-1.00001-6 |

| [24] | Xu C, Yang H (2022) Real Effects of Stabilizing Private Money Creation. National Bureau of Economic Research. |

| [25] | Yermack D (2015) Is Bitcoin a Real Currency? An economic appraisal, In: Chuen, D.L.K., Handbook of digital currency, Academic Press, San Diego, 31–43. https://doi.org/10.1016/B978-0-12-802117-0.00002-3 |

Figures(5) / Tables(1)

Meng Fan, Jinping Dai. Monetary attribute of stablecoins: A theoretical and empirical test[J]. National Accounting Review, 2023, 5(3): 261-281. doi: 10.3934/NAR.2023016

DownLoad:

DownLoad: