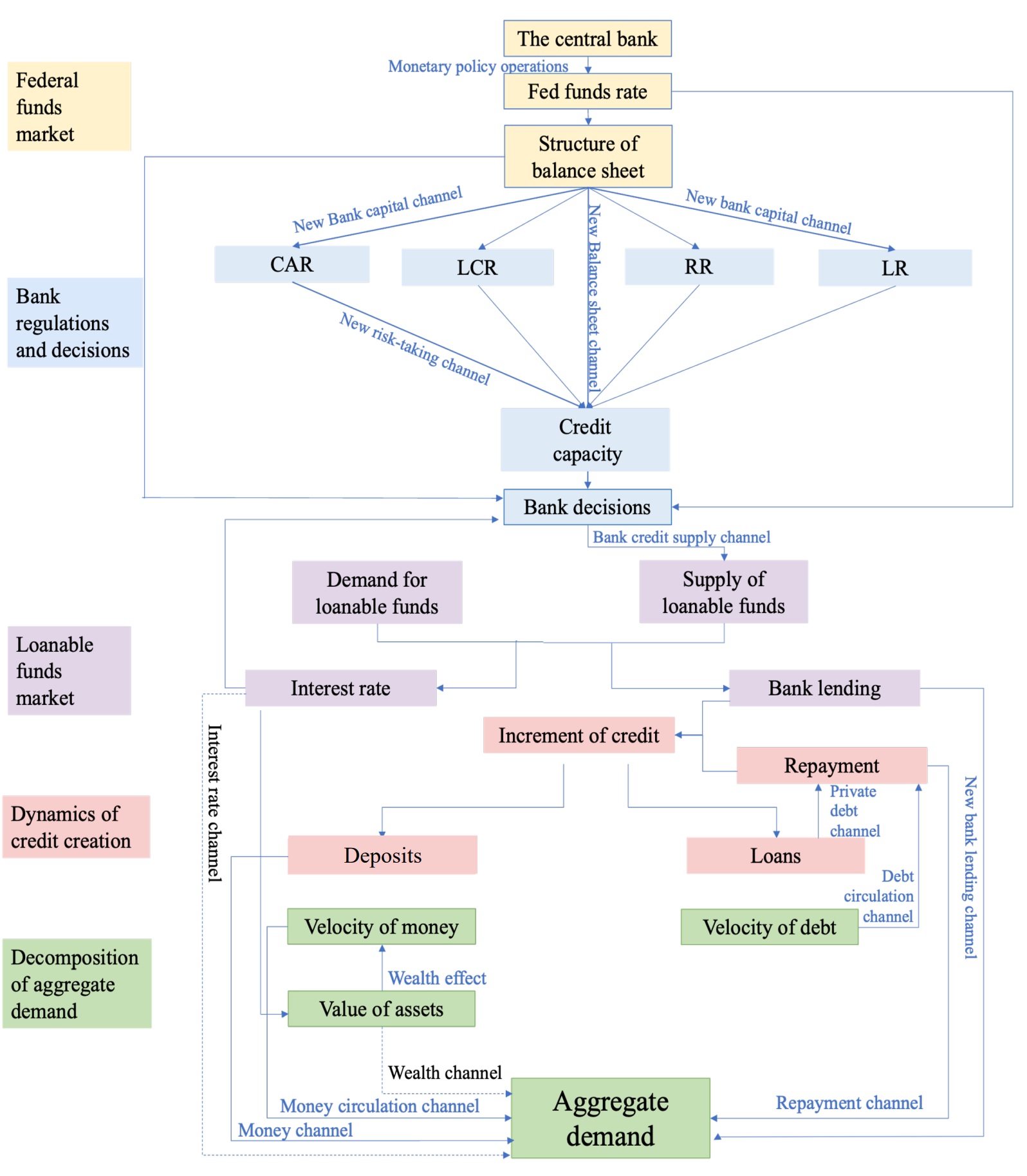

Many transmission channels of monetary policy have been proposed to enrich and deepen the understanding of its mechanisms. However, some channels have not been clarified, particularly for those unconventional quantitative policies implemented after 2008 financial crisis. In this paper, we develop a unified model of a credit economy where bank regulations and decisions and loanable funds market are placed at a central position, while stocks and flows are incorporated with each other to formulate banks' credit creation and circulation. We find that bank regulations can induce some new channels of monetary transmission by imposing credit constraints, including the new bank capital channel, the credit supply channel, the new bank balance sheet channel, and the new bank risk-taking channel. Comparing these channels with the traditional ones, we underscore the impact of bank regulations on monetary transmission. As aggregate demand can be decomposed into two monetary flows generated by money circulation and bank lending respectively, the direct channels of monetary transmission to aggregate demand can be renewed as follows: the money channel, the narrow money circulation channel, the new bank lending channel, and the repayment channel. In addition, based on the relevant data from the United States, we have conducted vector autoregressive (VAR) impulse response analysis to confirm the effectiveness of some direct channels. Our work not only aids in revisiting the monetary transmission from a credit view but also facilitates the assessment of efficiency of monetary policy.

Citation: Hua Zhong, Zijian Feng, Zifan Wang, Yougui Wang. Revisiting the monetary transmission mechanism via banking from the perspective of credit creation[J]. National Accounting Review, 2024, 6(1): 116-147. doi: 10.3934/NAR.2024006

Many transmission channels of monetary policy have been proposed to enrich and deepen the understanding of its mechanisms. However, some channels have not been clarified, particularly for those unconventional quantitative policies implemented after 2008 financial crisis. In this paper, we develop a unified model of a credit economy where bank regulations and decisions and loanable funds market are placed at a central position, while stocks and flows are incorporated with each other to formulate banks' credit creation and circulation. We find that bank regulations can induce some new channels of monetary transmission by imposing credit constraints, including the new bank capital channel, the credit supply channel, the new bank balance sheet channel, and the new bank risk-taking channel. Comparing these channels with the traditional ones, we underscore the impact of bank regulations on monetary transmission. As aggregate demand can be decomposed into two monetary flows generated by money circulation and bank lending respectively, the direct channels of monetary transmission to aggregate demand can be renewed as follows: the money channel, the narrow money circulation channel, the new bank lending channel, and the repayment channel. In addition, based on the relevant data from the United States, we have conducted vector autoregressive (VAR) impulse response analysis to confirm the effectiveness of some direct channels. Our work not only aids in revisiting the monetary transmission from a credit view but also facilitates the assessment of efficiency of monetary policy.

| [1] |

Ahrend R, Goujard A (2015) Global banking, global crises? The role of the bank balance-sheet channel. for the transmission of financial crises. Eur Econ Rev 80: 253–279. https://doi.org/10.1016/j.euroecorev.2015.10.003 doi: 10.1016/j.euroecorev.2015.10.003

|

| [2] | BCBS (2013) The liquidity coverage ratio and liquidity risk monitoring tools. Banks for International Settlements. |

| [3] |

Berger AN, Bouwman CHS (2013) How does capital affect bank performance during financial crises?. J Financ Econ 109: 146–176. https://doi.org/10.1016/j.jfineco.2013.02.008 doi: 10.1016/j.jfineco.2013.02.008

|

| [4] |

Bernanke BS (1983) Irreversilibity, uncertainty, and cyclical investment. Q J Econ 98: 85–106. https://doi.org/10.2307/1885568 doi: 10.2307/1885568

|

| [5] |

Bernanke BS, Blinder AS (1988) Credit, money and aggregate demand. Am Econ Rev 78: 435–439. https://doi.org/10.3386/w2534 doi: 10.3386/w2534

|

| [6] |

Bernanke BS, Gertler M (1995) Inside the black box the credit channel of monetary policy transmission. J Econ Perspect 9: 27–48. https://doi.org/10.3386/w5146 doi: 10.3386/w5146

|

| [7] |

Bernardo G, Campiglio E (2013) A simple model of income, aggregate demand and the process of credit creation by private banks. Empirica 41: 381–405. https://doi.org/10.1007/s10663-013-9239-6 doi: 10.1007/s10663-013-9239-6

|

| [8] | Blinder AS, Stiglitz JE (1983) Money, credit constraints, and economic activity. NBER Working Paper, No.1084. https://doi.org/10.3386/w1084 |

| [9] | Boivin J, Governor D, Lane T, et al. (2010) Should monetary policy be used to counteract financial imbalances. Bank Can Rev 23–36. |

| [10] |

Brunner K, Meltzer AH (1972) Money, debt, and economic activity. J Polit Econ 80: 951–977. https://doi.org/10.1086/259945 doi: 10.1086/259945

|

| [11] |

Calem P, Rob R (1999) The Impact of Capital-Based Regulation on Bank Risk-Taking. J Financial Intermediation 8: 317–352. https://doi.org/10.1006/jfin.1999.0276 doi: 10.1006/jfin.1999.0276

|

| [12] |

Chami R, Cosimano TF (2010) Monetary policy with a touch of Basel. J Econ Bus 62: 161–175. https://doi.org/10.1016/j.jeconbus.2009.12.001 doi: 10.1016/j.jeconbus.2009.12.001

|

| [13] |

Chen NK (2001) Bank net worth, asset prices and economic activity. J Monet Econ 48: 415–436. https://doi.org/10.1016/S0304-3932(01)00076-9 doi: 10.1016/S0304-3932(01)00076-9

|

| [14] |

Dermine J (2013) Bank Regulations after the Global Financial Crisis: Good Intentions and Unintended. Evil. Eur Financial Manag 19: 658–674. https://doi.org/10.1111/j.1468-036X.2013.12017.x doi: 10.1111/j.1468-036X.2013.12017.x

|

| [15] |

Disyatat P (2011) The bank lending channel revisited. J Money Credit Bank 43: 711–734. https://doi.org/10.1111/j.1538-4616.2011.00394.x doi: 10.1111/j.1538-4616.2011.00394.x

|

| [16] |

Eggertsson GB, Krugman P (2012) Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo. Approach. Q J Econ 127: 1469–1513. https://doi.org/10.1093/qje/qjs023 doi: 10.1093/qje/qjs023

|

| [17] |

Fisher I (1933) The Debt-Deflation Theory of Great Depressions. Econometrica 1: 337–357. https://doi.org/10.2307/1907327 doi: 10.2307/1907327

|

| [18] | Friedman A (1982) Foundations of modern analysis. New York: Dover Publications. |

| [19] |

Gambacorta L, Mistrulli PE (2004) Does bank capital affect lending behavior? J Financial Intermediation 13: 436–457. https://doi.org/10.1016/j.jfi.2004.06.001 doi: 10.1016/j.jfi.2004.06.001

|

| [20] |

Gertler M, Kiyotaki N (2010) Financial intermediation and credit policy in business cycle analysis, In: Friedman, B.M., Woodford M., Handbook of monetary economics, 3: 547–599. https://doi.org/10.1016/B978-0-444-53238-1.00011-9 doi: 10.1016/B978-0-444-53238-1.00011-9

|

| [21] |

Gertler M, Kiyotaki N (2015) Banking, Liquidity, and Bank Runs in an Infinite Horizon Economy. Am Econ Rev 105: 2011–2043. https://doi.org/10.1257/aer.20130665 doi: 10.1257/aer.20130665

|

| [22] |

Gertler M, Karadi P (2011) A model of unconventional monetary policy. J Monet Econ 58: 17–34. https://doi.org/10.1016/j.jmoneco.2010.10.004 doi: 10.1016/j.jmoneco.2010.10.004

|

| [23] |

Goodhart CAE (2010) Money, Credit and Bank Behaviour: Need for a New Approach. Natl Inst Econ Rev 214: F73–F82. https://doi.org/10.1177/0027950110389774 doi: 10.1177/0027950110389774

|

| [24] | Goyal A, Parab P (2021) Effectiveness of Expectations Channel of Monetary Policy Transmission: Evidence from India. Mumbai: Indira Gandhi Institute of Development Research, Working Paper No. 11. |

| [25] |

Gunji H, Yuan Y (2010) Bank profitability and the bank lending channel: Evidence from China. J Asian Econ 21: 129–141. https://doi.org/10.1016/j.asieco.2009.12.001 doi: 10.1016/j.asieco.2009.12.001

|

| [26] | Gurley JG, Shaw ES (1955) Financial Aspects of Economic Development. Ame Econ Rev 45: 515–538. |

| [27] | Gurley JG, Shaw ES (1960) Money in a Theory of Finance, Chicago: The Brookings Institution. |

| [28] |

Honda Y (2004) Bank capital regulations and the transmission mechanism. J Policy Model 26: 675–688. https://doi.org/10.1016/j.jpolmod.2004.01.006 doi: 10.1016/j.jpolmod.2004.01.006

|

| [29] | Jakab Z, Kumhof M (2015) Banks are not intermediaries of loanable of funds-and why this matters. Bank of England Working Paper No.529. |

| [30] | Jakab Z, Kumhof M (2019) Banks are not intermediaries of loanable funds — facts theory and evidence. Bank of England Working Paper No. 761. |

| [31] |

Jiménez G, Ongena S, Peydró JL, et al. (2012) Credit Supply and Monetary Policy: Identifying. the Bank Balance-Sheet Channel with Loan Applications. Am Econ Rev 102: 2301–2326. https://doi.org/10.1257/aer.102.5.2301 doi: 10.1257/aer.102.5.2301

|

| [32] |

Jodrà Ò, Schularick M, Taylor AM (2013) When credit bites back. J Money Credit Bank 45: 3–28. https://doi.org/10.1111/jmcb.12069 doi: 10.1111/jmcb.12069

|

| [33] |

Kapan T, Minoiu C (2018) Balance sheet strength and bank lending: Evidence from the global financial. crisis. J Bank Financ 92: 35–50. https://doi.org/10.1016/j.jbankfin.2018.04.011 doi: 10.1016/j.jbankfin.2018.04.011

|

| [34] | Kashyap AK, Stein JC (1994) Monetary Policy and Bank Lending, The University of Chicago Press. https://doi.org/10.3386/w4317 |

| [35] | Kashyap AK, Stein JC (1997) The role of banks in monetary policy: A survey with implications for the European monetary union. Economic Perspectives-Federal Reserve Bank of Chicago 21: 2–18. |

| [36] | Keen S (2016) Modeling Financial Instability, In: Malliaris, A.G., Shaw, L., Shefrin, H., The Global Financial Crisis and Its Aftermath: Hidden Factors in the Meltdown, Oxford: Oxford University Press, 67–103. https://doi.org/10.1093/acprof: oso/9780199386222.003.0004 |

| [37] | Koo RC (2011) The Holy Grail Of Macroeconomics: Lessons From Japan's Great Recession, Singapore: John Wiley & Sons (Asia) Pte. Ltd.. |

| [38] |

Kopecky KJ, VanHoose D (2004) A model of the monetary sector with and without binding capital. requirements. J Bank Financ 28: 633–646. https://doi.org/10.1016/s0378-4266(03)00038-4 doi: 10.1016/s0378-4266(03)00038-4

|

| [39] |

Krug S, Lengnick M, Wohltmann HW (2015) The impact of Basel Ⅲ on financial (in)stability: an. agent-based credit network approach. Quant Finance 15: 1917–1932. https://doi.org/10.1080/14697688.2014.999701 doi: 10.1080/14697688.2014.999701

|

| [40] |

Kumhof M, Wang X (2021) Banks, money, and the zero lower bound on deposit rates. J Econ Dyn Control 132: 104208. https://doi.org/10.1016/j.jedc.2021.104208 doi: 10.1016/j.jedc.2021.104208

|

| [41] |

Le Heron E, Mouakil T (2008) A Post-Keynesian Stock-Flow Consistent Model for Dynamic Analysis of Monetary Policy Shock on Banking Behaviour. Metroeconomica 59: 405–440. https://doi.org/10.1111/j.1467-999X.2008.00313.x doi: 10.1111/j.1467-999X.2008.00313.x

|

| [42] |

Li B, Xiong W, Chen L, et al. (2017) The impact of the liquidity coverage ratio on money creation: A stock-flow based dynamic approach. Econ Model 67: 193–202. https://doi.org/10.1016/j.econmod.2016.12.016 doi: 10.1016/j.econmod.2016.12.016

|

| [43] | Macleod HD (1866) The Theory and Practice of Banking, London: Longmans. |

| [44] | McLeay M, Radia A, Thomas R (2014a) Money Creation in the Modern Economy. Bank of England Quarterly Bulletin, Q1. |

| [45] | McLeay M, Radia A, Thomas R (2014b) Money in the modern economy: an introduction. Bank of England. Quarterly Bulletin. |

| [46] | Meh C, Moran K (2004) Bank Capital, Agency Costs, and Monetary Policy. Bank of Canada Working. Paper 2004-6. |

| [47] |

Mian A, Sufi A (2011) House Prices, Home Equity–Based Borrowing, and the US Household Leverage. Crisis. Am Econ Rev 101: 2132–2156. https://doi.org/10.1257/aer.101.5.2132 doi: 10.1257/aer.101.5.2132

|

| [48] | Mian AR, Sufi A (2012) What explains high unemployment? The aggregate demand channel. NBER Working Paper, No.17830 https://doi.org/10.3386/w17830 |

| [49] | Mian AR, Straub L, Sufi A (2020) The saving glut of the rich. NBER Working Paper, No. 26941. https://doi.org/10.3386/w26941 |

| [50] | Minsky HP (1982) The Financial-Instability Hypothesis: Capitalist Processes and the Behavior of the Economy. Hyman P. Minsky Archive. 282. |

| [51] |

Orzechowski PE (2019) The bank capital channel and bank profits. Rev Financial Econ 37: 372–388. https://doi.org/10.1002/rfe.1054 doi: 10.1002/rfe.1054

|

| [52] |

Palley TI (1997) Endogenous money and the business cycle. J Econ 65: 133–149. https://doi.org/10.1007/BF01226931 doi: 10.1007/BF01226931

|

| [53] |

Panagopoulos Y (2010) Basel Ⅱ and the money supply process: some empirical evidence from the. Greek banking system. Appl Econ Lett 17: 973–976. https://doi.org/10.1080/13504850802599482 doi: 10.1080/13504850802599482

|

| [54] | Peek J, Rosengren ES (2013) The role of banks in the transmission of monetary policy. Public Policy. Discussion Papers No. 13-5. https://doi.org/http://hdl.handle.net/10419/99119 |

| [55] |

Rajan RG (2006) Has Finance Made the World Riskier. Eur Financial Manag 12: 499–533. https://doi.org/10.1111/j.1468-036X.2006.00330.x doi: 10.1111/j.1468-036X.2006.00330.x

|

| [56] | Rasche RH, Johannes JM (2012) Controlling the Growth of Monetary Aggregates, Springer Science & Business Media. https://doi.org/10.1007/978-94-009-3275-3 |

| [57] | Rogoff K (2010) Three Challenges Facing Modern Macroeconomics. American Economic Association, Ten Years and Beyond: Economists Answer NSF's Call for Long-Term Research Agendas. https://doi.org/10.2139/ssrn.1889366 |

| [58] |

Romer CD, Romer DH, Goldfeld SM, et al. (1990) New evidence on the monetary. transmission mechanism. Brookings Pap Econ Act 1: 149–213.https://doi.org/10.2307/2534527 doi: 10.2307/2534527

|

| [59] | Schumpeter JA (1912) The Theory of Economic Development, Cambridge, MA: Harvard University Press. |

| [60] |

Stiglitz JE (2018) Where modern macroeconomics went wrong. Oxford Rev Econ Policy 34: 70–106. https://doi.org/10.1093/oxrep/grx040 doi: 10.1093/oxrep/grx040

|

| [61] | Swanson ET (2023) The federal funds market, pre-and post-2008. InResearch Handbook of Financial: 220-236. UK: Edward Elgar Publishing. |

| [62] | Tanaka M (2002) How Do Bank Capital and Capital Adequacy Regulation Affect the Monetary. Transmission Mechanism? CESIFO Working Paper No. 799. |

| [63] |

Taylor JB (1993) Discretion versus policy rules in practice. Carnegie-Rochester conference series on public policy 39: 195–214. https://doi.org/10.1016/0167-2231(93)90009-L doi: 10.1016/0167-2231(93)90009-L

|

| [64] | Tobin J, Brainard WC (1963) Financial Intermediaries and the Effectiveness of Monetary Controls. Am Econ Rev 53: 383–400. |

| [65] | Tobin J (1964) Commercial banks as creators of "money". Yale: Cowles Foundation for Research in Economics. |

| [66] |

Werner RA (2014) How do banks create money, and why can other firms not do the same? An explanation for the coexistence of lending and deposit-taking. Int Rev Financial Anal 36: 71–77. https://doi.org/10.1016/j.irfa.2014.10.013 doi: 10.1016/j.irfa.2014.10.013

|

| [67] |

Werner RA (2016) A lost century in economics: Three theories of banking and the conclusive evidence. Int Rev Financial Anal 46: 361–379. https://doi.org/10.1016/j.irfa.2015.08.014 doi: 10.1016/j.irfa.2015.08.014

|

| [68] | Wicksell K (1898) Geldzins und Güterpreise: Eine Untersuchung über die den Tauschwert des Geldes bestimmenden Ursachen (Jena: Gustav Fischer), translated as Interest and Prices: A Study of the Causes Regulating the Value of Money (London: Macmillan, 1936). |

| [69] | Wicksell K (1907) Krisernas gä ta, Statsø konomisk Tidskrift, 21 (3), 255–84, translated as The Enigma of Business Cycles, International Economic Papers, 3 (1953), 58–74. |

| [70] |

Woodford M (2010) Financial Intermediation and Macroeconomic Analysis. J Econ Perspect 24: 21–44. https://doi.org/10.1257/jep.24.4.21 doi: 10.1257/jep.24.4.21

|

| [71] |

Xing X, Wang M, Wang Y, et al. (2020) Credit creation under multiple banking regulations: The. impact of balance sheet diversity on money supply. Econ Model 91: 720–735. https://doi.org/10.1016/j.econmod.2019.09.030 doi: 10.1016/j.econmod.2019.09.030

|

| [72] |

Xing X, Xiong W, Guo J, et al. (2021) The role of debt in aggregate demand. Finance Res Lett 39: 101653. https://doi.org/10.1016/j.frl.2020.101653 doi: 10.1016/j.frl.2020.101653

|

| [73] |

Xiong W, Li B, Wang Y, et al. (2020) The versatility of money multiplier under Basel Ⅲ. regulations. Finance Res Lett 32: https://doi.org/10.1016/j.frl.2019.04.024 doi: 10.1016/j.frl.2019.04.024

|

| [74] |

Xiong W, Fu H, Wang Y (2017) Money creation and circulation in a credit economy. Physica A 465: 425–437. https://doi.org/10.1016/j.physa.2016.08.023 doi: 10.1016/j.physa.2016.08.023

|

| [75] |

Xiong W, Wang Y (2018) The impact of Basel Ⅲ on money creation: a synthetic theoretical analysis. Economics 12. https://doi.org/10.5018/economics-ejournal.ja.2018-41 doi: 10.5018/economics-ejournal.ja.2018-41

|

| [76] |

Xiong W, Wang Y (2022) A reformulation of the bank lending channel under multiple prudential. regulations. Econ Model 114: 105916. https://doi.org/10.1016/j.econmod.2022.105916 doi: 10.1016/j.econmod.2022.105916

|

Figures(4) / Tables(6)

Hua Zhong, Zijian Feng, Zifan Wang, Yougui Wang. Revisiting the monetary transmission mechanism via banking from the perspective of credit creation[J]. National Accounting Review, 2024, 6(1): 116-147. doi: 10.3934/NAR.2024006

DownLoad:

DownLoad: