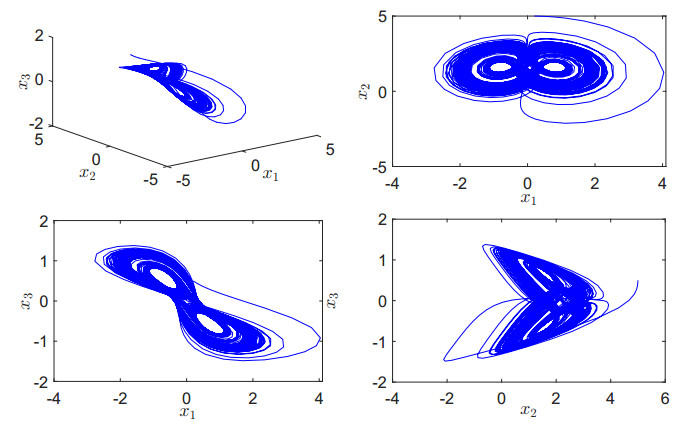

Aiming at the problem that the convergence time of the chaotic finance/economic system cannot be set independently and the continuous macro-control is required, this paper investigates the predefined-time control of the chaotic finance/economic system based on event-triggered mechanism. The predefined-time control approach ensures the chaotic finance system quickly converge to the stable state within a pre-determined time. Moreover, in order to avoid continuous macro-control, an event-trigger mechanism is added into the above predefined-time control approach, which guarantees that the control input is updated only when some predefined event occurs. Rigorous theoretical derivation is presented and concrete simulation experiments are carried out to validate the feasibility and applicability of the proposed control strategy.

Citation: Qiaoping Li, Yu Chen, Lingyuan Ma. Predefined-time control of chaotic finance/economic system based on event-triggered mechanism[J]. AIMS Mathematics, 2023, 8(4): 8000-8017. doi: 10.3934/math.2023404

Aiming at the problem that the convergence time of the chaotic finance/economic system cannot be set independently and the continuous macro-control is required, this paper investigates the predefined-time control of the chaotic finance/economic system based on event-triggered mechanism. The predefined-time control approach ensures the chaotic finance system quickly converge to the stable state within a pre-determined time. Moreover, in order to avoid continuous macro-control, an event-trigger mechanism is added into the above predefined-time control approach, which guarantees that the control input is updated only when some predefined event occurs. Rigorous theoretical derivation is presented and concrete simulation experiments are carried out to validate the feasibility and applicability of the proposed control strategy.

| [1] |

C. R. B. Moutsinga, E. Pindza, E. Maré, A robust spectral integral method for solving chaotic finance systems, Alex. Eng. J., 59 (2020), 601–611. https://doi.org/10.1016/j.aej.2020.01.016 doi: 10.1016/j.aej.2020.01.016

|

| [2] |

L. Shen, G. He, Threshold effect of financial system on high-quality economic development, J. Math., 2022 (2022), 9108130. https://doi.org/10.1155/2022/9108130 doi: 10.1155/2022/9108130

|

| [3] |

C. R. B. Moutsinga, E. Pindza, E. Mare, Comparative performance of time spectral methods for solving hyperchaotic finance and cryptocurrency systems, Chaos Solitons Fract., 145 (2021), 110770. https://doi.org/10.1016/j.chaos.2021.110770 doi: 10.1016/j.chaos.2021.110770

|

| [4] |

L. Chen, G. Chen, Controlling chaos in an economic model, Phys. A, 374 (2007), 349–358. https://doi.org/10.1016/j.physa.2006.07.022 doi: 10.1016/j.physa.2006.07.022

|

| [5] |

S. Dadras, H. R. Momeni, Control of a fractional-order economical system via sliding mode, Phys. A, 389 (2010), 2434–2442. https://doi.org/10.1016/j.physa.2010.02.025 doi: 10.1016/j.physa.2010.02.025

|

| [6] |

H. Liu, S. Li, J. Cao, G. Li, A. Alsaedi, F. E. Alsaadi, Adaptive fuzzy prescribed performance controller design for a class of uncertain fractional-order nonlinear systems with external disturbances, Neurocomputing, 219 (2017), 422–430. https://doi.org/10.1016/j.neucom.2016.09.050 doi: 10.1016/j.neucom.2016.09.050

|

| [7] |

S. Zheng, G. Dong, Q. Bi, Adaptive modified function projective synchronization of hyperchaotic systems with unknown parameters, Commun. Nonlinear Sci. Numer. Simul., 15 (2010), 3547–3556. https://doi.org/10.1016/j.cnsns.2009.12.010 doi: 10.1016/j.cnsns.2009.12.010

|

| [8] |

C. Wang, Adaptive fuzzy control for uncertain fractional-order financial chaotic systems subjected to input saturation, PLoS ONE, 11 (2016), 0164791. https://doi.org/10.1371/journal.pone.0164791 doi: 10.1371/journal.pone.0164791

|

| [9] |

H. M. Baskonus, T. Mekkaoui, Z. Hammouch, H. Bulut, Active control of a chaotic fractional order economic system, Entropy, 17 (2015), 5771–5783. https://doi.org/10.3390/e17085771 doi: 10.3390/e17085771

|

| [10] |

I. Pan, S. Das, S. Das, Multi-objective active control policy design for commensurate and incommensurate fractional order chaotic financial systems, Appl. Math. Model., 39 (2015), 500–514. https://doi.org/10.1016/j.apm.2014.06.005 doi: 10.1016/j.apm.2014.06.005

|

| [11] |

M. Zhao, J. Wang, H$_{\infty}$ control of a chaotic finance system in the presence of external disturbance and input time-delay, Appl. Math. Comput., 233 (2014), 320–327. https://doi.org/10.1016/j.amc.2013.12.085 doi: 10.1016/j.amc.2013.12.085

|

| [12] |

E. Xu, Y. Chen, J. Yang, Finite-time H$_{\infty}$ control for a chaotic finance system via delayed feedback, Syst. Sci. Control Eng., 6 (2018), 467–476. https://doi.org/10.1080/21642583.2018.1537863 doi: 10.1080/21642583.2018.1537863

|

| [13] |

I. Ahmad, A. Ouannas, M. Shafiq, V. T. Pham, D. Baleanu, Finite-time stabilization of a perturbed chaotic finance model, J. Adv. Res., 32 (2021), 1–14. https://doi.org/10.1016/j.jare.2021.06.013 doi: 10.1016/j.jare.2021.06.013

|

| [14] |

S. Harshavarthini, R. Sakthivel, Y. K. Ma, M. Muslimd, Finite-time resilient fault-tolerant investment policy scheme for chaotic nonlinear finance system, Chaos Solitons Fract., 132 (2020), 109567. https://doi.org/10.1016/j.chaos.2019.109567 doi: 10.1016/j.chaos.2019.109567

|

| [15] |

Q. Li, S. Liu, Predefined-time vector-polynomial-based synchronization among a group of chaotic systems and its application in secure information transmission, AIMS Math., 6 (2021), 11005–11028. https://doi.org/10.3934/math.2021639 doi: 10.3934/math.2021639

|

| [16] |

Q. Li, S. Liu, Switching event-triggered network-synchronization for chaotic systems with different dimensions, Neurocomputing, 311 (2018), 32–40. https://doi.org/10.1016/j.neucom.2018.05.039 doi: 10.1016/j.neucom.2018.05.039

|

| [17] |

J. Wang, B. Tian, Fixed-time distributed event-triggered formation control with state-dependent threshold, Int. J. Robust Nonlinear, 32 (2022), 1209–1228. https://doi.org/10.1002/rnc.5878 doi: 10.1002/rnc.5878

|

| [18] |

Q. Li, S. Liu, Y. Chen, Combination event-triggered adaptive networked synchronization communication for nonlinear uncertain fractional-order chaotic systems, Appl. Math. Comput., 333 (2018), 521–535. https://doi.org/10.1016/j.amc.2018.03.094 doi: 10.1016/j.amc.2018.03.094

|

| [19] |

S. Liu, L. Zhou, Network synchronization and application of chaotic lur'e systems based on event-triggered mechanism, Nonlinear Dyn., 83 (2016), 2497–2507. https://doi.org/10.1007/s11071-015-2498-y doi: 10.1007/s11071-015-2498-y

|

| [20] |

C. M. Kaneba, X. Mu, X. Li, X. Wu, Event triggered control for fault tolerant control system with actuator failure and randomly occurring parameter uncertainty, Appl. Math. Comput., 415 (2022), 126714. https://doi.org/10.1016/j.amc.2021.126714 doi: 10.1016/j.amc.2021.126714

|

| [21] |

S. Hu, J. Qiu, X. Chen, F. Zhao, X. Jiang, Dynamic event-triggered control for leader-following consensus of multiagent systems with the estimator, IET Control Theory Appl., 16 (2022), 475–484. https://doi.org/10.1049/cth2.12245 doi: 10.1049/cth2.12245

|

| [22] |

J. D. Sánchez-Torres, D. Gómez-Gutiérrez, E. López, A. G. Loukianov, A class of predefined-time stable dynamical systems, Int. J. Robust Nonlinear, 35 (2018), i1–i29. https://doi.org/10.1093/imamci/dnx004 doi: 10.1093/imamci/dnx004

|

| [23] |

C. A. Anguiano-Gijón, A. J. Muñoz-Vázquez, J. D. Sánchez-Torres, G. Romero-Galván, F. Martínez-Reyes, On predefined-time synchronisation of chaotic systems, Chaos Solitons Fract., 122 (2019), 172–178. https://doi.org/10.1016/j.chaos.2019.03.015 doi: 10.1016/j.chaos.2019.03.015

|

| [24] |

Z. Zuo, Nonsingular fixed-time consensus tracking for second-order multi-agent networks, Automatica, 54 (2015), 305–309. https://doi.org/10.1016/j.automatica.2015.01.021 doi: 10.1016/j.automatica.2015.01.021

|

| [25] | S. Fan, Y. Guo, Y. Ji, Fixed-time consensus for leader-following multi-groups of multi-agent systems with unknown non-linear inherent dynamics, 2019 Chinese Control Conference (CCC), Guangzhou, China, 2019, 5903–5908. https://doi.org/10.23919/ChiCC.2019.8865766 |

| [26] |

H. Ma, Y. Chen, Study of the bifurcation topological structure and the global complicated character of a kind of nonlinear finance system (ⅰ), Appl. Math. Mech., 22 (2001), 1240–1251. https://doi.org/10.1023/A:1016313804297 doi: 10.1023/A:1016313804297

|

| [27] | J. Jian, X. Deng, J. Wang, Globally exponentially attractive set and synchronization of a class of chaotic finance system, In: W. Yu, H. He, N. Zhang, Advances in neural networks-ISNN 2009, Springer, 5551 (2009), 253–261. https://doi.org/10.1007/978-3-642-01507-6_30 |

| [28] |

Q. Gao, J. Ma, Chaos and hopf bifurcation of a finance system, Nonlinear Dyn., 58 (2009), 209. https://doi.org/10.1007/s11071-009-9472-5 doi: 10.1007/s11071-009-9472-5

|

| [29] |

H. Jahanshahi, S. S. Sajjadi, S. Bekiros, A. A. Aly, On the development of variable-order fractional hyperchaotic economic system with a nonlinear model predictive controller, Chaos Solitons Fract., 144 (2021), 110698. https://doi.org/10.1016/j.chaos.2021.110698 doi: 10.1016/j.chaos.2021.110698

|

| [30] |

A. Yousefpour, H. Jahanshahi, J. M. Munoz-Pacheco, S. Bekiros, Z. Wei, A fractional-order hyper-chaotic economic system with transient chaos, Chaos Solitons Fract., 130 (2020), 109400. https://doi.org/10.1016/j.chaos.2019.109400 doi: 10.1016/j.chaos.2019.109400

|

Figures(9)

Qiaoping Li, Yu Chen, Lingyuan Ma. Predefined-time control of chaotic finance/economic system based on event-triggered mechanism[J]. AIMS Mathematics, 2023, 8(4): 8000-8017. doi: 10.3934/math.2023404

DownLoad:

DownLoad: