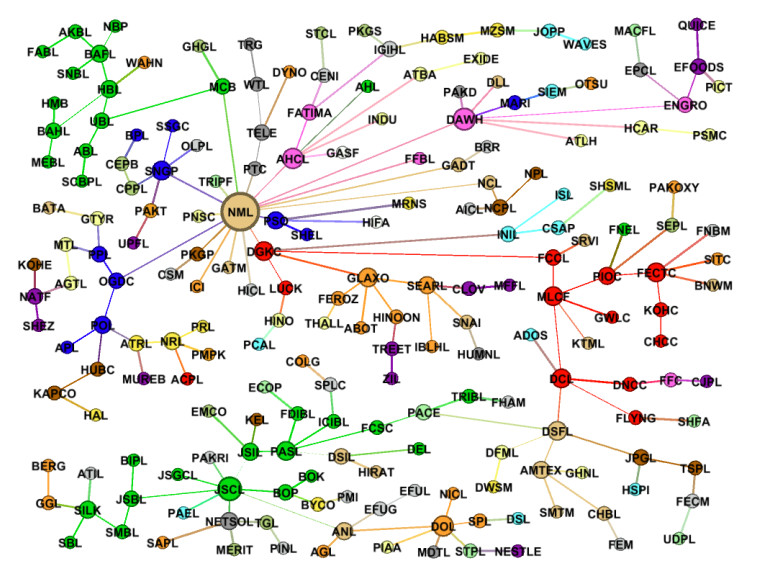

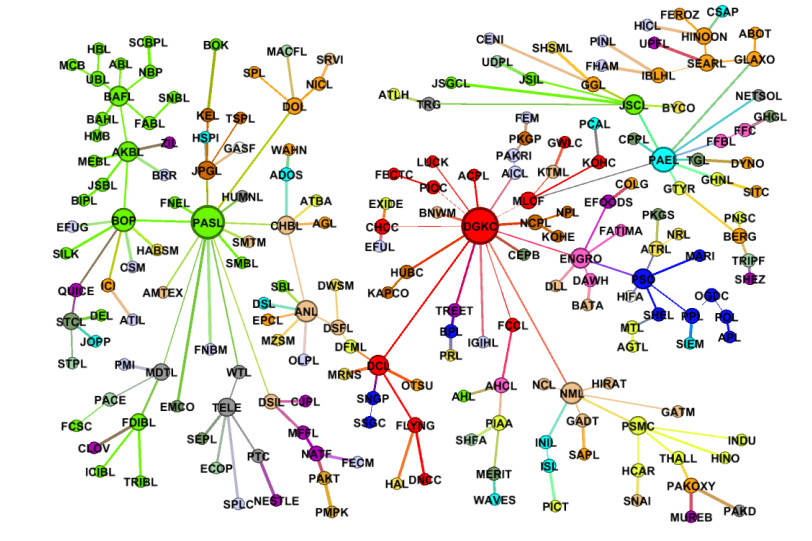

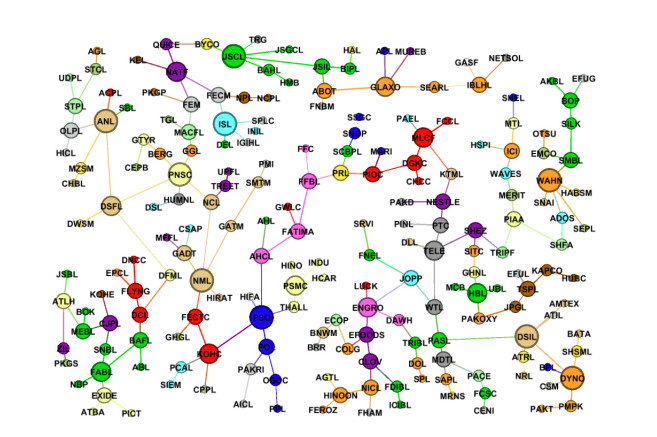

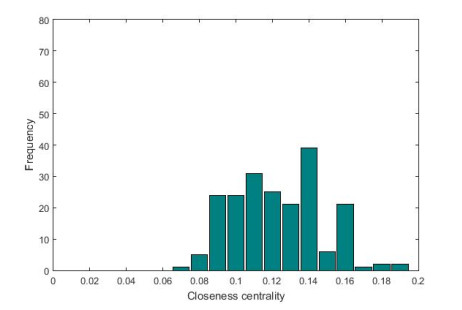

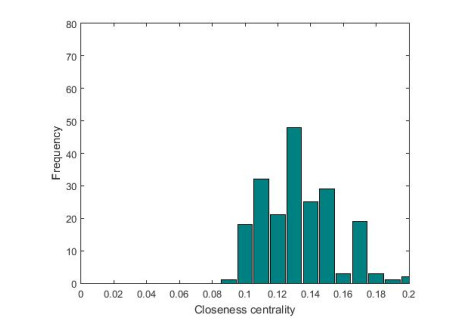

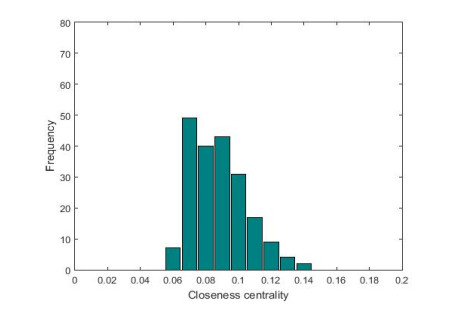

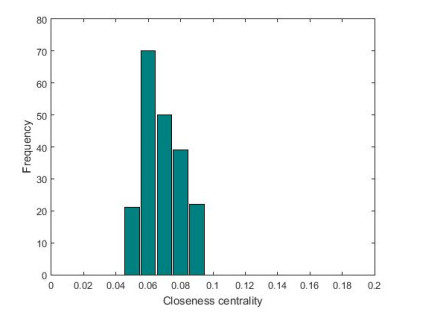

We study topology of correlation structures and construct Pearson correlation-based networks (MST-Pearson) and partial correlation-based networks (MST-Partial) during two time periods of extreme terrorist activities (High civilian and security forces fatalities) and relaxed period (low civilian and security forces fatalities). Our results find that probability density function of Pearson correlation coefficients for relaxed period and partial correlation coefficients for both periods slightly deviates from the gaussian function. MST-Pearson during the period of extreme terrorist activities is a crisis like less stable market structure in comparison with the meta-stable market state structure of relaxed period. Our studies also find presence of two most prominent clusters belonging to cement, and chemical and pharmaceutical sectors among four MSTs. In addition, we find important role of few sectors during the period of extreme terrorist activities in comparison with a more diversified sectoral role in the relaxed period. Furthermore, time varying topological properties indicate an expansion in both MST-Pearson and MST-Partial length in the relaxed period due to counter terrorism strategies. Thus, the study reveals interesting findings and implications for the policymakers and investors of Pakistan stock market during the event of terrorism.

Citation: Bilal Ahmed Memon, Hongxing Yao. Correlation structure networks of stock market during terrorism: evidence from Pakistan[J]. Data Science in Finance and Economics, 2021, 1(2): 117-140. doi: 10.3934/DSFE.2021007

We study topology of correlation structures and construct Pearson correlation-based networks (MST-Pearson) and partial correlation-based networks (MST-Partial) during two time periods of extreme terrorist activities (High civilian and security forces fatalities) and relaxed period (low civilian and security forces fatalities). Our results find that probability density function of Pearson correlation coefficients for relaxed period and partial correlation coefficients for both periods slightly deviates from the gaussian function. MST-Pearson during the period of extreme terrorist activities is a crisis like less stable market structure in comparison with the meta-stable market state structure of relaxed period. Our studies also find presence of two most prominent clusters belonging to cement, and chemical and pharmaceutical sectors among four MSTs. In addition, we find important role of few sectors during the period of extreme terrorist activities in comparison with a more diversified sectoral role in the relaxed period. Furthermore, time varying topological properties indicate an expansion in both MST-Pearson and MST-Partial length in the relaxed period due to counter terrorism strategies. Thus, the study reveals interesting findings and implications for the policymakers and investors of Pakistan stock market during the event of terrorism.

| [1] |

Abadie A, Gardeazabal J (2008). Terrorism and the world economy. Eur Econ Rev 52: 1-27. doi: 10.1016/j.euroecorev.2007.08.005

|

| [2] |

Arin KP, Ciferri D, Spagnolo N (2008) The price of terror: The effects of terrorism on stock market returns and volatility. Econ Lett 101: 164-167. doi: 10.1016/j.econlet.2008.07.007

|

| [3] |

Bandyopadhyay S, Sandler T, Younas J (2014) Foreign Direct Investment, Aid, and Terrorism. Oxford Econ Pap 66: 25-50. doi: 10.1093/oep/gpt026

|

| [4] | Barnett GA, Jiang K, Hammond JR (2015) Using coherencies to examine network evolution and co-evolution. Soc Network Anal Mining 5: 53. |

| [5] |

Barnett GA, Ruiz JB, Hammond JR, et al. (2013) An examination of the relationship between international telecommunication networks, terrorism and global news coverage. Soc Network Anal Mining 3: 721-747. doi: 10.1007/s13278-013-0117-9

|

| [6] |

Blomberg SB, Hess GD, Orphanides A (2004) The macroeconomic consequences of terrorism. J Monetary Econ 51: 1007-1032. doi: 10.1016/j.jmoneco.2004.04.001

|

| [7] |

Brandes U (2001) A faster algorithm for betweenness centrality. J Math Soc 25: 163-177. doi: 10.1080/0022250X.2001.9990249

|

| [8] |

Brida JG, Matesanz D, Seijas MN (2016) Network analysis of returns and volume trading in stock markets: The Euro Stoxx case. Phys A 444: 751-764. doi: 10.1016/j.physa.2015.10.078

|

| [9] |

Brounen D, Derwall J (2010) The Impact of Terrorist Attacks on International Stock Markets. Eur Financ Manage 16: 585-598. doi: 10.1111/j.1468-036X.2009.00502.x

|

| [10] |

Coelho R, Hutzler S, Repetowicz P, et al. (2007) Sector analysis for a FTSE portfolio of stocks. Phys A 373: 615-626. doi: 10.1016/j.physa.2006.02.050

|

| [11] |

Coletti P, Murgia M (2016) The network of the Italian stock market during the 2008-2011 financial crises. Algorithmic Financ 5: 111-137. doi: 10.3233/AF-160177

|

| [12] |

Dias J (2012) Sovereign debt crisis in the European Union: A minimum spanning tree approach. Phys A 391: 2046-2055. doi: 10.1016/j.physa.2011.11.004

|

| [13] |

Eckstein Z, Tsiddon D (2004) Macroeconomic consequences of terror: theory and the case of Israel. J Monetary Econ 51: 971-1002. doi: 10.1016/j.jmoneco.2004.05.001

|

| [14] |

Efobi U, Asongu S (2016) Terrorism and capital flight from Africa. Int Econ 148: 81-94. doi: 10.1016/j.inteco.2016.06.004

|

| [15] |

Essaddam N, Karagianis JM (2014) Terrorism, country attributes, and the volatility of stock returns. Res Int Bus Financ 31: 87-100. doi: 10.1016/j.ribaf.2013.11.001

|

| [16] |

Gilmore CG, Lucey BM, Boscia MW (2010) Comovements in government bond markets: A minimum spanning tree analysis. Phys A 389: 4875-4886. doi: 10.1016/j.physa.2010.06.057

|

| [17] |

Haddad M, Hakim S (2008) The impact of war and terrorism on sovereign risk in the Middle East. J Deriv Hedge Funds 14: 237-250. doi: 10.1057/jdhf.2008.17

|

| [18] | Haider M, Anwar A (2014) Impact of terrorism on FDI flows to Pakistan. MPRA Paper, University Library of Munich, Germany. |

| [19] |

Jang W, Lee J, Chang W (2011) Currency crises and the evolution of foreign exchange market: Evidence from minimum spanning tree. Phys A 390: 707-718. doi: 10.1016/j.physa.2010.10.028

|

| [20] |

Jo SK, Kim MJ, Lim K, et al. (2018) Correlation analysis of the Korean stock market: Revisited to consider the influence of foreign exchange rate. Phys A 491: 852-868. doi: 10.1016/j.physa.2017.09.071

|

| [21] |

Kantar E, Keskin M, Deviren B (2012) Analysis of the effects of the global financial crisis on the Turkish economy, using hierarchical methods. Phys A 391: 2342-2352. doi: 10.1016/j.physa.2011.12.014

|

| [22] |

Khan A, Estrada MAR, Yusof Z (2016) Terrorism and India: an economic perspective. Qual Quant 50: 1833-1844. doi: 10.1007/s11135-015-0239-4

|

| [23] |

Khashanah K, Li Y (2016) Dynamic Structure of the Global Financial System of Systems. Mod Econ 7: 1303-1330. doi: 10.4236/me.2016.711124

|

| [24] |

khoojine AS, Han D (2019) Network analysis of the Chinese stock market during the turbulence of 2015-2016 using log-returns, volumes and mutual information. Phys A 523: 1091-1109. doi: 10.1016/j.physa.2019.04.128

|

| [25] |

Kim HJ, Lee Y, Kahng B, et al. (2002) Weighted Scale-Free Network in Financial Correlations. J Phys Soc Japan 71: 2133-2136. doi: 10.1143/JPSJ.71.2133

|

| [26] |

Kollias C, Papadamou S, Stagiannis A (2011) Terrorism and capital markets: The effects of the Madrid and London bomb attacks. Int Rev Econ Financ 20: 532-541. doi: 10.1016/j.iref.2010.09.004

|

| [27] |

Kruskal JB (1956) On the Shortest Spanning Subtree of a Graph and the Traveling Salesman Problem. Pro Am Math Soc 7: 48-50. doi: 10.1090/S0002-9939-1956-0078686-7

|

| [28] |

Lee JW, Nobi A (2018) State and Network Structures of Stock Markets Around the Global Financial Crisis. Comput Econ 51: 195-210. doi: 10.1007/s10614-017-9672-x

|

| [29] | Li B, Pi D (2018) Analysis of global stock index data during crisis period via complex network approach. PLOS ONE 13: e0200600. |

| [30] |

Llussá F, Tavares J (2011) THE ECONOMICS OF TERRORISM: A (SIMPLE) TAXONOMY OF THE LITERATURE. Defence Peace Econ 22: 105-123. doi: 10.1080/10242694.2011.542331

|

| [31] |

Majapa M, Gossel SJ (2016) Topology of the South African stock market network across the 2008 financial crisis. Phys A 445: 35-47. doi: 10.1016/j.physa.2015.10.108

|

| [32] | Mantegna RN (1999) Hierarchical structure in financial markets. Eur Phys J B 11: 193-197. |

| [33] | Mantegna RN, Stanley HE (2000) An Introduction to Econophysics: Correlations and Complexity in Finance, Cambridge, UK. |

| [34] |

Matesanz D, Ortega GJ (2015) Sovereign public debt crisis in Europe. A network analysis. Phys A 436: 756-766. doi: 10.1016/j.physa.2015.05.052

|

| [35] |

Memon BA, Tahir R (2021) Examining network structures and dynamics of world energy companies in stock markets: A complex network approach. Int J Energy Econ Policy 11: 329-344. doi: 10.32479/ijeep.11287

|

| [36] | Memon BA, Yao H (2019) Structural Change and Dynamics of Pakistan Stock Market during Crisis: A Complex Network Perspective. Entropy 21: 248. |

| [37] |

Memon BA, Yao H, Aslam F, et al. (2019) Network analysis of Pakistan stock market during the turbulence of economic crisis. Bus Manage Educ 17: 269-285. doi: 10.3846/bme.2019.11394

|

| [38] | Memon BA, Yao H, Tahir R (2020) General election effect on the network topology of Pakistan's stock market: network-based study of a political event. Financ Innovation 6: 2. |

| [39] |

Mnasri A, Nechi S (2016) Impact of terrorist attacks on stock market volatility in emerging markets. Emerg Mark Rev 28: 184-202. doi: 10.1016/j.ememar.2016.08.002

|

| [40] |

Nguyen Q, Nguyen NKK, Nguyen LHN (2019) Dynamic topology and allometric scaling behavior on the Vietnamese stock market. Phys A 514: 235-243. doi: 10.1016/j.physa.2018.09.061

|

| [41] |

Nobi A, Maeng SE, Ha GG, et al. (2014) Effects of global financial crisis on network structure in a local stock market. Phys A 407: 135-143. doi: 10.1016/j.physa.2014.03.083

|

| [42] |

Nobi A, Maeng SE, Ha GG, et al. (2015) Structural changes in the minimal spanning tree and the hierarchical network in the Korean stock market around the global financial crisis. J Korean Phys Soc 66: 1153-1159. doi: 10.3938/jkps.66.1153

|

| [43] | Onnela JP, Chakraborti A, Kaski K, et al. (2003) Dynamics of market correlations: Taxonomy and portfolio analysis. Phys Rev E 68: 056110. |

| [44] | Onnela JP, Chakraborti A, Kaski K, et al. (2003) Asset Trees and Asset Graphs in Financial Markets. Phys Scr T106: 48. |

| [45] |

Papana A, Kyrtsou C, Kugiumtzis D, et al. (2017) Financial networks based on Granger causality: A case study. Phys A 482: 65-73. doi: 10.1016/j.physa.2017.04.046

|

| [46] |

Procasky WJ, Ujah NU (2016) Terrorism and its impact on the cost of debt. J Int Money Financ 60: 253-266. doi: 10.1016/j.jimonfin.2015.04.007

|

| [47] | Qiao H, Xia Y, Li Y (2016) Can Network Linkage Effects Determine Return? Evidence from Chinese Stock Market. PLOS ONE 11: e0156784. |

| [48] |

Radhakrishnan S, Duvvuru A, Sultornsanee S, et al. (2016) Phase synchronization based minimum spanning trees for analysis of financial time series with nonlinear correlations. Phys A 444: 259-270. doi: 10.1016/j.physa.2015.09.070

|

| [49] |

Rehman FU, Nasir M, Shahbaz M (2017) What have we learned? Assessing the effectiveness of counterterrorism strategies in Pakistan. Econ Model 64: 487-495. doi: 10.1016/j.econmod.2017.02.028

|

| [50] |

Rehman FU, Vanin P (2017) Terrorism risk and democratic preferences in Pakistan. J Dev Econ 124: 95-106. doi: 10.1016/j.jdeveco.2016.09.003

|

| [51] |

Sabidussi G (1966) The centrality index of a graph. Psychometrika 31: 581-603. doi: 10.1007/BF02289527

|

| [52] | Sandoval L (2012) A Map of the Brazilian Stock Market. Adv Complex Syst 15: 1250042. |

| [53] |

Setiawan K (2014) Global stock market landscape: an application of minimum spanning tree technique. Int J Oper Res 20: 41-67. doi: 10.1504/IJOR.2014.060514

|

| [54] |

Shahbaz M (2013) Linkages between inflation, economic growth and terrorism in Pakistan. Econ Model 32: 496-506. doi: 10.1016/j.econmod.2013.02.014

|

| [55] |

Sharif S, Ismail S, Zurni O, et al. (2016) Validation of Global Financial Crisis on Bursa Malaysia Stocks Market Companies via Covariance Structure. Am J Appl Sci 13: 1091-1095. doi: 10.3844/ajassp.2016.1091.1095

|

| [56] | Song DM, Tumminello M, Zhou WX, et al. (2011) Evolution of worldwide stock markets, correlation structure, and correlation-based graphs. Phys Rev E 84: 026108. |

| [57] |

Song JW, Ko B, Chang W (2018) Analyzing systemic risk using non-linear marginal expected shortfall and its minimum spanning tree. Phys A 491: 289-304. doi: 10.1016/j.physa.2017.08.076

|

| [58] |

Tabak BM, Serra TR, Cajueiro DO (2010) Topological properties of stock market networks: The case of Brazil. Phys A 389: 3240-3249. doi: 10.1016/j.physa.2010.04.002

|

| [59] |

Tumminello M, Aste T, Di Matteo T, et al. (2005) A tool for filtering information in complex systems. Proc Natl Acad Sci 102: 10421-10426. doi: 10.1073/pnas.0500298102

|

| [60] |

Ulusoy T, Keskin M, Shirvani A, et al. (2012) Complexity of major UK companies between 2006 and 2010: Hierarchical structure method approach. Phys A 391: 5121-5131. doi: 10.1016/j.physa.2012.01.026

|

| [61] | Wang GJ, Xie C, Chen YJ, et al. (2013) Statistical Properties of the Foreign Exchange Network at Different Time Scales: Evidence from Detrended Cross-Correlation Coefficient and Minimum Spanning Tree. Entropy 15: 1643. |

| [62] |

Wang GJ, Xie C, Stanley HE (2018) Correlation Structure and Evolution of World Stock Markets: Evidence from Pearson and Partial Correlation-Based Networks. Comput Econ 51: 607-635. doi: 10.1007/s10614-016-9627-7

|

| [63] |

Wiliński M, Sienkiewicz A, Gubiec T, et al. (2013) Structural and topological phase transitions on the German Stock Exchange. Phys A 392: 5963-5973. doi: 10.1016/j.physa.2013.07.064

|

| [64] |

Xia L, You D, Jiang X, et al. (2018) Comparison between global financial crisis and local stock disaster on top of Chinese stock network. Phys A 490: 222-230. doi: 10.1016/j.physa.2017.08.005

|

| [65] | Yan H, Han L (2019) Empirical distributions of stock returns: Mixed normal or kernel density? Phys A 514: 473-486. |

| [66] |

Yang R, Li X, Zhang T (2014) Analysis of linkage effects among industry sectors in China's stock market before and after the financial crisis. Phys A 411: 12-20. doi: 10.1016/j.physa.2014.05.072

|

| [67] |

Yao H, Memon BA (2019) Network topology of FTSE 100 Index companies: From the perspective of Brexit. Phys A 523: 1248-1262. doi: 10.1016/j.physa.2019.04.106

|

| [68] |

Yin K, Liu Z, Liu P (2017) Trend analysis of global stock market linkage based on a dynamic conditional correlation network. J Bus Econ Manage 18: 779-800. doi: 10.3846/16111699.2017.1341849

|

DSFE-01-02-007-s001.pdf DSFE-01-02-007-s001.pdf |

|

Figures(14) / Tables(7)

Bilal Ahmed Memon, Hongxing Yao. Correlation structure networks of stock market during terrorism: evidence from Pakistan[J]. Data Science in Finance and Economics, 2021, 1(2): 117-140. doi: 10.3934/DSFE.2021007

DownLoad:

DownLoad: