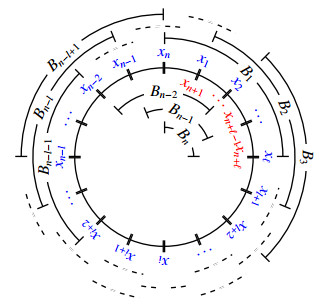

This study introduced the optimized block bootstrap (OBB), a novel method designed to enhance time series prediction by reducing the number of blocks while maintaining their representativeness. OBB minimized block overlap, resulting in greater computational efficiency while preserving the temporal structure of data. The method was evaluated through extensive simulations of autoregressive moving average (ARMA) models and South Africa economic data which included inflation rates, gross domestic product (GDP) growth, interest rates, and unemployment rates. Results demonstrated that OBB consistently outperformd circular block bootstrap (CBB), providing more accurate forecasts with lower root mean square error (RMSE), which assessed variance, and lower mean absolute error (MAE), which measured bias, across various time series models and parameter settings. Consequently, the OBB method was applied to forecasting of the South Africa economic data, extending up to 2027. The novel approach presented by OBB offered a valuable tool for improving predictive accuracy in time series forecasting, with potential applications across diverse fields such as finance and environmental modeling.

Citation: James Daniel, Kayode Ayinde, Adewale F. Lukman, Olayan Albalawi, Jeza Allohibi, Abdulmajeed Atiah Alharbi. Optimised block bootstrap: an efficient variant of circular block bootstrap method with application to South African economic time series data[J]. AIMS Mathematics, 2024, 9(11): 30781-30815. doi: 10.3934/math.20241487

This study introduced the optimized block bootstrap (OBB), a novel method designed to enhance time series prediction by reducing the number of blocks while maintaining their representativeness. OBB minimized block overlap, resulting in greater computational efficiency while preserving the temporal structure of data. The method was evaluated through extensive simulations of autoregressive moving average (ARMA) models and South Africa economic data which included inflation rates, gross domestic product (GDP) growth, interest rates, and unemployment rates. Results demonstrated that OBB consistently outperformd circular block bootstrap (CBB), providing more accurate forecasts with lower root mean square error (RMSE), which assessed variance, and lower mean absolute error (MAE), which measured bias, across various time series models and parameter settings. Consequently, the OBB method was applied to forecasting of the South Africa economic data, extending up to 2027. The novel approach presented by OBB offered a valuable tool for improving predictive accuracy in time series forecasting, with potential applications across diverse fields such as finance and environmental modeling.

| [1] |

K. Ayinde, J. Daniel, A. Adepetun, O. S. Ewemooje, Moving block bootstrap method with better elements representation for univariate time series data, Reliability: Theory & Applications, 18 (2023), 671–688. https://doi.org/10.24412/1932-2321-2023-374-671-688 doi: 10.24412/1932-2321-2023-374-671-688

|

| [2] |

P. Burridge, A. M. R. Taylor, Bootstrapping the HEGY seasonal unit root tests, J. Econometrics, 123 (2004), 67–87. https://doi.org/10.1016/j.jeconom.2003.10.029 doi: 10.1016/j.jeconom.2003.10.029

|

| [3] |

E. Carlstein, The use of subseries values for estimating the variance of a general statistic from a stationary sequence, Ann. Statist., 14 (1986), 1171–1179. https://doi.org/10.1214/aos/1176350057 doi: 10.1214/aos/1176350057

|

| [4] |

T. Chai, R. R. Draxler, Root mean square error (RMSE) or mean absolute error (MAE), Geosci. Model Dev. Discuss., 7 (2014), 1525–1534. https://doi.org/10.5194/gmdd-7-1525-2014 doi: 10.5194/gmdd-7-1525-2014

|

| [5] | J. Daniel, K. Ayinde, OBL: optimum block length, package version 0.2.1, 2022. Available from: https://CRAN.R-project.org/package=OBL. |

| [6] | B. Efron, Bootstrap methods: another look at the jackknife, In: Breakthroughs in statistics, New York, NY: Springer, 1992,569–593. https://doi.org/10.1007/978-1-4612-4380-9_41 |

| [7] |

P. Hall, Resampling a coverage pattern, Stoch. Proc. Appl., 20 (1985), 231–246. https://doi.org/10.1016/0304-4149(85)90212-1 doi: 10.1016/0304-4149(85)90212-1

|

| [8] |

M. A. Hannan, D. N. T. How, M. S. H. Lipu, M. Mansor, P. J. Ker, Z. Y. Dong, et al., Deep learning approach towards accurate state of charge estimation for lithium-ion batteries using self-supervised transformer model, Sci. Rep., 11 (2021), 19541. https://doi.org/10.1038/s41598-021-98915-8 doi: 10.1038/s41598-021-98915-8

|

| [9] | T. Hesterberg, Bootstrap, WIRS: Computational Statistics, 3 (2011), 497–526. https://doi.org/10.1002/wics.182 |

| [10] | J.-P. Kreiss, S. N. Lahiri, Bootstrap methods for time series, In: Handbook of statistics, Elsevier, 30 (2012), 3–26. https://doi.org/10.1016/B978-0-444-53858-1.00001-6 |

| [11] |

D. Kugiumtzis, Evaluation of surrogate and bootstrap tests for nonlinearity in time series, Stud. Nonlinear Dyn. Econ., 12 (2008), 4. https://doi.org/10.2202/1558-3708.1474 doi: 10.2202/1558-3708.1474

|

| [12] |

H. R. Kunsch, The jackknife and the bootstrap for general stationary observations, Ann. Statist., 17 (1989), 1217–1241. https://doi.org/10.1214/aos/1176347265 doi: 10.1214/aos/1176347265

|

| [13] |

M. W. Liemohn, A. D. Shane, A. R. Azari, A. K. Petersen, B. M. Swiger, A. Mukhopadhyay, Rmse is not enough: guidelines to robust data-model comparisons for magnetospheric physics, J. Atmos. Sol.-Terr. Phys., 218 (2021), 105624. https://doi.org/10.1016/j.jastp.2021.105624 doi: 10.1016/j.jastp.2021.105624

|

| [14] |

R. Lyu, Y. Qu, K. Divaris, D. Wu, Methodological considerations in longitudinal analyses of microbiome data: a comprehensive review, Genes, 15 (2024), 51. https://doi.org/10.3390/genes15010051 doi: 10.3390/genes15010051

|

| [15] |

T. Mathonsi, T. L. van Zyl, A statistics and deep learning hybrid method for multivariate time series forecasting and mortality modeling, Forecasting, 4 (2022), 1–25. https://doi.org/10.3390/forecast4010001 doi: 10.3390/forecast4010001

|

| [16] | Macrotrends LLC, South Africa GDP Growth Rate 1961–2022, 2023. Available from: https://www.macrotrends.net/countries/ZAF/south-africa/gdp-growth-rate. |

| [17] |

F. Petropoulos, E. Spiliotis, The wisdom of the data: getting the most out of univariate time series forecasting, Forecasting, 3 (2021), 478–497. https://doi.org/10.3390/forecast3030029 doi: 10.3390/forecast3030029

|

| [18] | D. N. Politis, J. R. Romano, A circular block-resampling procedure for stationary data, Technical reports, Stanford University Department of Statistics, & National Science Foundation, 1991. Available from: https://purl.stanford.edu/xh812zd4638. |

| [19] | D. N. Politis, J. P. Romano, The stationary bootstrap, J. Amer. Stat. Assoc., 89 (1994), 1303–1313. https://doi.org/10.1080/01621459.1994.10476870 |

| [20] |

M. R. Qader, S. Khan, M. Kamal, M. Usman, M. Haseeb, Forecasting carbon emissions due to electricity power generation in bahrain, Environ. Sci. Pollut. Res., 29 (2022), 17346–17357. https://doi.org/10.1007/s11356-021-16960-2 doi: 10.1007/s11356-021-16960-2

|

| [21] |

B. Radovanov, A. Marcikić, A comparison of four different block bootstrap methods, Croat. Oper. Res. Rev., 5 (2014), 189–202. https://doi.org/10.17535/crorr.2014.0007 doi: 10.17535/crorr.2014.0007

|

| [22] |

W. J. Raseman, B. Rajagopalan, J. R. Kasprzyk, W. Kleiber, Nearest neighbor time series bootstrap for generating influent water quality scenarios, Stoch. Environ. Res. Risk Assess., 34 (2020), 23–31. https://doi.org/10.1007/s00477-019-01762-3 doi: 10.1007/s00477-019-01762-3

|

| [23] | X. Shao, The dependent wild bootstrap, J. Amer. Stat. Assoc., 105 (2010), 218–235. https://doi.org/10.1198/jasa.2009.tm08744 |

| [24] |

K. Singh, On the asymptotic accuracy of efron's bootstrap, Ann. Statist., 9 (1981), 1187–1195. https://doi.org/10.1214/aos/1176345636 doi: 10.1214/aos/1176345636

|

| [25] | K. Singh, M. Xie, Bootstrap: a statistical method, Rutgers University, USA, 2008. Available from: https://statweb.rutgers.edu/mxie/RCPapers/bootstrap.pdf. |

| [26] | The R Core Team, The R Project for Statistical Computing, 2022. Available from: https://www.r-project.org/. |

| [27] |

H. D. Vinod, New bootstrap inference for spurious regression problems, J. Appl. Stat., 43 (2016), 317–335. https://doi.org/10.1080/02664763.2015.1049939 doi: 10.1080/02664763.2015.1049939

|

| [28] |

S. Wang, Y. Fan, S. Jin, P. Takyi-Aninakwa, C. Fernandez, Improved anti-noise adaptive long short-term memory neural network modeling for the robust remaining useful life prediction of lithium-ion batteries, Reliab. Eng. Syst. Safe., 230 (2023), 108920. https://doi.org/https://doi.org/10.1016/j.ress.2022.108920 doi: 10.1016/j.ress.2022.108920

|

| [29] |

S. Wang, F. Wu, P. Takyi-Aninakwa, C. Fernandez, D.-I. Stroe, Q. Huang, Improved singular filtering-gaussian process regression-long short-term memory model for whole-life-cycle remaining capacity estimation of lithium-ion batteries adaptive to fast aging and multi-current variations, Energy, 284 (2023), 128677. https://doi.org/10.1016/j.energy.2023.128677 doi: 10.1016/j.energy.2023.128677

|

| [30] | Y. Wang, New developments in sequential change point detection for time series and spatio-temporal analysis, PhD thesis, University of Connecticut, 2023. |

| [31] |

A. Young, Consistency without inference: instrumental variables in practical application, Eur. Econ. Rev., 147 (2022), 104112. https://doi.org/10.1016/j.euroecorev.2022.104112 doi: 10.1016/j.euroecorev.2022.104112

|

| [32] |

G. A. Young, Bootstrap: More than a stab in the dark?, Statist. Sci., 9 (1994), 382–395. https://doi.org/10.1214/ss/1177010383 doi: 10.1214/ss/1177010383

|

Figures(19) / Tables(9)

James Daniel, Kayode Ayinde, Adewale F. Lukman, Olayan Albalawi, Jeza Allohibi, Abdulmajeed Atiah Alharbi. Optimised block bootstrap: an efficient variant of circular block bootstrap method with application to South African economic time series data[J]. AIMS Mathematics, 2024, 9(11): 30781-30815. doi: 10.3934/math.20241487

DownLoad:

DownLoad: