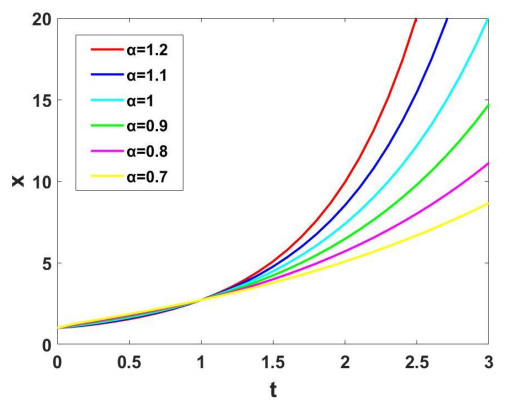

This paper argues that any economic phenomena should be observed by two different scales, and any economic laws are scale-dependent. A one-scale law arising in either macroeconomics or microeconomics might be mathematically correct and economically relevant, however, sparking debates might arise for a different scale. This paper re-analyzes the basic assumptions of the Evans model for dynamic economics, and it concludes that they are quite reasonable on a large time-scale, but the assumptions become totally invalid on a smaller scale, and a fractal modification has to be adopted. A two-scale price dynamics is suggested and a fractal variational theory is established to maximize the profit at a given period. Furthermore Evans 1924 variational principle for the maximal profit is easy to be solved for a quadratic cost function using the Lagrange multiplier method. Here a quadratic-cubic cost function and a nonlinear demand function are used, and the stationary condition of the variational formulation is derived step by step, and a more complex dynamic system is obtained. The present derivation process can be extended to a more complex cost function and a more complex demand function, and the paper sheds a promising light on mathematics treatment of complex economic problems.

Citation: Ji-Huan He, Chun-Hui He, Hamid M. Sedighi. Evans model for dynamic economics revised[J]. AIMS Mathematics, 2021, 6(9): 9194-9206. doi: 10.3934/math.2021534

This paper argues that any economic phenomena should be observed by two different scales, and any economic laws are scale-dependent. A one-scale law arising in either macroeconomics or microeconomics might be mathematically correct and economically relevant, however, sparking debates might arise for a different scale. This paper re-analyzes the basic assumptions of the Evans model for dynamic economics, and it concludes that they are quite reasonable on a large time-scale, but the assumptions become totally invalid on a smaller scale, and a fractal modification has to be adopted. A two-scale price dynamics is suggested and a fractal variational theory is established to maximize the profit at a given period. Furthermore Evans 1924 variational principle for the maximal profit is easy to be solved for a quadratic cost function using the Lagrange multiplier method. Here a quadratic-cubic cost function and a nonlinear demand function are used, and the stationary condition of the variational formulation is derived step by step, and a more complex dynamic system is obtained. The present derivation process can be extended to a more complex cost function and a more complex demand function, and the paper sheds a promising light on mathematics treatment of complex economic problems.

| [1] | G. C. Evans, The dynamics of monopoly, Am. Math. Mon., 31 (1924), 77-83. |

| [2] |

V. E. Tarasov, Fractional econophysics: Market price dynamics with memory effects, Phys. A: Stat. Mech. Appl., 557 (2020), 124865. doi: 10.1016/j.physa.2020.124865

|

| [3] |

M. Pomini, Economic dynamics and the calculus of variations in the interwar period, J. Hist. Econ. Thought, 40 (2018), 57-79. doi: 10.1017/S1053837217000116

|

| [4] |

Z. Nahorski, H. F. Ravn, A review of mathematical models in economic environmental problems, Ann. Oper. Res., 97 (2000), 165-201. doi: 10.1023/A:1018913316076

|

| [5] | K. D. Avinash, J. E. Stiglitz, Monopolistic competition and optimum product diversity, Am. Econ. Rev., 67 (1977), 297-308. |

| [6] | J. H. He, A simple approach to Volterra-Fredholm integral equations, J. Appl. Comput. Mech., 6 (2020), 1184-1186. |

| [7] |

P. A. Samuelson, Law of conservation of the capital-output ratio, Proc. Natl. Acad. Sci., 67 (1970), 1477-1479. doi: 10.1073/pnas.67.3.1477

|

| [8] | P. A. Samuelson, Two conservation laws in theoretical economics, In: R. Sato, R. V. Ramachandran, Conservation Laws and Symmetry: Applications to Economics and Finance, Springer, 1990. |

| [9] | P. A. Samuelson, Law of conservation of the capital-output ratio in closed von Neumann systems, In: R. Sato, R. V. Ramachandran, Conservation Laws and Symmetry: Applications to Economics and Finance, Springer, 1990. |

| [10] |

P. A. Samuelson, Conserved energy without work or heat, Proc. Natl. Acad. Sci., 89 (1992), 1090-1094. doi: 10.1073/pnas.89.3.1090

|

| [11] | D. Romer, Advanced Macroeconomics, 4 Eds., McGraw-Hill Equcation, 2019. |

| [12] | A. C. Chiang, Element of Dynamic Optimization, Singapore: Science Typographers Inc, 1992. |

| [13] |

J. H. He, Fractal calculus and its geometrical explanation, Results Phys., 10 (2018), 272-276. doi: 10.1016/j.rinp.2018.06.011

|

| [14] |

Y. Khan, Fractal Lakshmanan-Porsezian-Daniel model with different forms of nonlinearity and its novel soliton solutions, Fractals, 29 (2021), 2150032. doi: 10.1142/S0218348X21500328

|

| [15] |

Y. Khan, Fractal modification of complex Ginzburg-Landau model arising in the oscillating phenomena, Results Phys., 18 (2020), 103324. doi: 10.1016/j.rinp.2020.103324

|

| [16] |

Y. Khan, A novel soliton solutions for the fractal Radhakrishnan-Kundu-Lakshmanan model arising in birefringent fibers, Opt. Quant. Electron., 53 (2021), 127. doi: 10.1007/s11082-021-02775-5

|

| [17] |

J. H. He, Thermal science for the real world: Reality and Challenge, Therm. Sci., 24 (2020), 2289-2294. doi: 10.2298/TSCI191001177H

|

| [18] | N. Anjum, C. H. He, J. H. He, Two-scale fractal theory for the population dynamics, Fractals, 2021. Available from: https://doi.org/10.1142/S0218348X21501826. |

| [19] |

B. Mandelbrot, How long is the coast of Britain? Statistical self-similarity and fractional dimension, Science, 156 (1967), 636-638. doi: 10.1126/science.156.3775.636

|

| [20] |

J. H. He, Q. T. Ain, New promises and future challenges of fractal calculus: From two-scale thermodynamics to fractal variational principle, Therm. Sci., 24 (2020), 659-681. doi: 10.2298/TSCI200127065H

|

| [21] |

J. H. He, A tutorial review on fractal spacetime and fractional calculus, Int. J. Theor. Phys., 53 (2014), 3698-3718. doi: 10.1007/s10773-014-2123-8

|

| [22] |

X. J. Li, Z. Liu, J. H. He, A fractal two-phase flow model for the fiber motion in a polymer filling process, Fractals, 28 (2020), 2050093. doi: 10.1142/S0218348X20500930

|

| [23] | D. Tian, C. H. He, J. H. He, Fractal pull-in stability theory for microelectromechanical systems, Front. Phys., 9 (2021), 145. |

| [24] | C. H. He, C. Liu, J. H. He, K. A. Gepreel, Low frequency property of a fractal vibration model for a concrete beam, Fractals, 2021. Available from: https://doi.org/10.1142/S0218348X21501176. |

| [25] | C. H. He, C. Liu, J. H. He, A. H. Shirazi, H. Mohammad-Sedighi, Passive atmospheric water harvesting utilizing an ancient Chinese ink slab and its possible applications in modern architecture, Facta Univ. Ser.-Mech. Eng., 2021. Available from: http://casopisi.junis.ni.ac.rs/index.php/FUMechEng/article/view/7202. |

| [26] | C. H. He, C. Liu, J. H. He, H. Mohammad-Sedighi, A. Shokri, K. A. Gepreel, A fractal model for the internal temperature response of a porous concrete, Appl. Comput. Math., 20 (2021). |

| [27] |

J. H. He, S. J. Kou, C. H. He, Z. W. Zhang, K. A. Gepreel, Fractal oscillation and its frequency-amplitude property, Fractals, 29 (2021), 2150105. doi: 10.1142/S0218348X2150105X

|

| [28] | J. H. He, W. F. Hou, N. Qie, K. A. Gepreel, A. H. Shirazi, H. Mohammad-Sedighi, Hamiltonian-based frequency-amplitude formulation for nonlinear oscillators, Facta Univ. Ser.-Mech. Eng., 2021. Available from: http://casopisi.junis.ni.ac.rs/index.php/FUMechEng/article/view/7223. |

| [29] |

C. H. He, Y. Shen, F. Y. Ji, J. H. He, Taylor series solution for fractal Bratu-type equation arising in electrospinning process, Fractals, 28 (2020), 2050011. doi: 10.1142/S0218348X20500115

|

| [30] |

J. H. He, N. Qie, C. H. He, T. Saeed, On a strong minimum condition of a fractal variational principle, Appl. Math. Lett., 119 (2021), 107199. doi: 10.1016/j.aml.2021.107199

|

| [31] |

J. H. He, N. Qie, C. H. He, Solitary waves travelling along an unsmooth boundary, Results Phys., 24 (2021), 104104. doi: 10.1016/j.rinp.2021.104104

|

| [32] |

Y. T. Zuo, Effect of SiC particles on viscosity of 3-D print paste: A fractal rheological model and experimental verification, Therm. Sci., 25 (2021), 2405-2409. doi: 10.2298/TSCI200710131Z

|

| [33] | J. H. He, W. F. Hou, C. H. He, T. Saeed, T. Hayat, Variational approach to fractal solitary waves, Fractals, 29 (2021). |

| [34] |

Y. Wu, J. H. He, A remark on Samuelson's variational principle in economics, Appl. Math. Lett., 84 (2018), 143-147. doi: 10.1016/j.aml.2018.05.008

|

| [35] | J. H. He, Lagrange crisis and generalized variational principle for 3D unsteady flow, Int. J. Numer. Methods Heat Fluid Flow, 30 (2020), 1189-1196. |

| [36] | J. H. He, N. Anjum, P. S. Skrzypacz, A variational principle for a nonlinear oscillator arising in the microelectromechanical system, J. Appl. Comput. Mech., 7 (2021), 78-83. |

| [37] | J. H. He, P. S. Skrzypacz, Y. N. Zhang, J. Pang, Approximate periodic solutions to microelectromechanical system oscillator subject to magnetostatic excitation, Math. Meth. Appl. Sci., 2020. Available from: https://doi.org/10.1002/mma.7018. |

| [38] | J. H. He, Y. O. El-Dib, The enhanced homotopy perturbation method for axial vibration of strings, Facta Univ. Ser.-Mech. Eng., 2021. Available from: http://casopisi.junis.ni.ac.rs/index.php/FUMechEng/article/view/7385. |

| [39] | J. H. He, Y. O. El-Dib, Homotopy perturbation method with three expansions, J. Math. Chem., 59 (2021), 1139-1150. |

| [40] | J. H. He, G. M. Moatimid, D. R. Mostapha, Nonlinear instability of two streaming-superposed magnetic Reiner-Rivlin Fluids by He-Laplace method, J. Electroanal. Chem., 2021. Available from: https://doi.org/10.1016/j.jelechem.2021.115388. |

| [41] | M. Ali, N. Anjum, Q. T. Ain, J. H. He, Homotopy perturbation method for the attachment oscillator arising in nanotechnology, Fibers Polym, 2021. Available from: https://doi.org/10.1007/s12221-021-0844-x. |

| [42] | N. Anjum, J. H. He, Q. T. Ain, D. Tian, Li-He's modified homotopy perturbation method for doubly-clamped electrically actuated microbeams-based microelectromechanical system, Facta Univ. Ser.-Mech. Eng., 2021. Available from: http://casopisi.junis.ni.ac.rs/index.php/FUMechEng/article/view/7346. |

| [43] | J. H. He, Y. O. El-Dib, The reducing rank method to solve third-order Duffing equation with the homotopy perturbation, Numer. Methods Partial Differ. Equations, 37 (2021), 1800-1808. |

| [44] | J. H. He, Y. O. El-Dib, Homotopy perturbation method for Fangzhu oscillator, J. Math. Chem. 58 (2020), 2245-2253. |

| [45] | J. H. He, Y. O. El-Dib, Periodic property of the time-fractional Kundu-Mukherjee-Naskar equation, Results Phys., 19 (2020), 103345. |

| [46] | M. Hvistendahl, Analysis of China's onechild policy sparks uproar colleagues call demographer's findings flawed and irresponsible, Science, 358 (2017), 283-284. |

| [47] | L. Cameron, N. Erkal, L. Gangadharan, X. Meng, Little emperors: Behavioral impacts of China's one-child policy, Science, 339 (2013), 953-957. |

| [48] | M. Hvistendahl, Has China outgrown the one-child policy? Science, 329 (2010), 1458-1461. |

| [49] | C. Djerassi, Political, not scientific, birth control solutions, Science, 297 (2002), 1120-1120. |

| [50] |

J. H. He, Seeing with a single scale is always unbelieving: From magic to two-scale fractal, Therm. Sci., 25 (2021), 1217-1219. doi: 10.2298/TSCI2102217H

|

| [51] | Y. Khan, Fractal higher-order dispersions model and its fractal variational principle arising in the field of physcial process, Fluctuation Noise Lett., 2021. Available from: https://doi.org/10.1142/S0219477521500346. |

| [52] | Y. Khan, Novel solitary wave solution of the nonlinear fractal Schrödinger equation and its fractal variational principle, Multidiscip. Model. Mater. Struct., 17 (2020), 630-635. |

| [53] |

Y. Khan, A variational approach for novel solitary solutions of FitzHugh-Nagumo equation arising in the nonlinear reaction-diffusion equation, Int. J. Numer. Methods Heat Fluid Flow, 31 (2021), 1104-1109. doi: 10.1108/HFF-05-2020-0299

|

Figures(1)

Ji-Huan He, Chun-Hui He, Hamid M. Sedighi. Evans model for dynamic economics revised[J]. AIMS Mathematics, 2021, 6(9): 9194-9206. doi: 10.3934/math.2021534

DownLoad:

DownLoad: