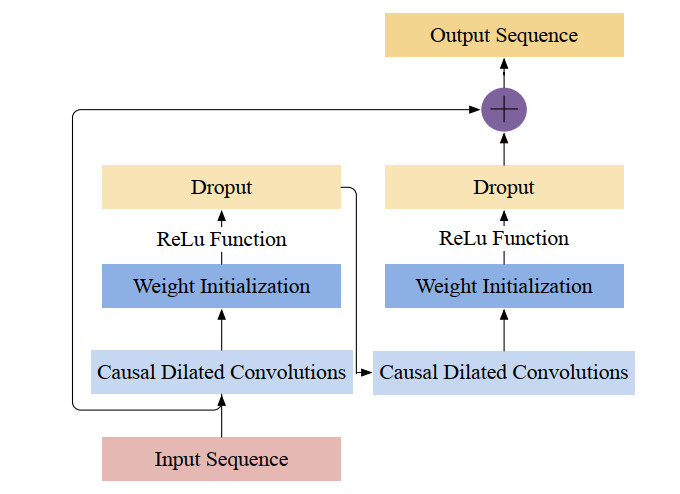

Based on the data from January 2007 to December 2021, this paper selects 14 representatives from four levels of the extreme risk of financial institutions, the contagion effect between financial systems, volatility and instability of financial markets, liquidity, and credit risk systemic risk. By constructing a Savitzky-Golay-TCN deep convolutional neural network, the systemic risk indicators of China's financial market are predicted, and their accuracy and reliability are analyzed. The research found that: 1) Savitzky-Golay-TCN deep convolutional neural network has a strong generalization ability, and the prediction effect on all indices is stable. 2) Compared with the three control models (time-series convolutional network (TCN), convolutional neural network (CNN), and long short-term memory (LSTM)), the Savitzky-Golay-TCN deep convolutional neural network has excellent prediction accuracy, and its average prediction accuracy for all indices has increased. 3) Savitzky-Golay-TCN deep convolutional neural network can better monitor financial market changes and effectively predict systemic risk.

Citation: Xite Yang, Ankang Zou, Jidi Cao, Yongzeng Lai, Jilin Zhang. Systemic risk prediction based on Savitzky-Golay smoothing and temporal convolutional networks[J]. Electronic Research Archive, 2023, 31(5): 2667-2688. doi: 10.3934/era.2023135

Based on the data from January 2007 to December 2021, this paper selects 14 representatives from four levels of the extreme risk of financial institutions, the contagion effect between financial systems, volatility and instability of financial markets, liquidity, and credit risk systemic risk. By constructing a Savitzky-Golay-TCN deep convolutional neural network, the systemic risk indicators of China's financial market are predicted, and their accuracy and reliability are analyzed. The research found that: 1) Savitzky-Golay-TCN deep convolutional neural network has a strong generalization ability, and the prediction effect on all indices is stable. 2) Compared with the three control models (time-series convolutional network (TCN), convolutional neural network (CNN), and long short-term memory (LSTM)), the Savitzky-Golay-TCN deep convolutional neural network has excellent prediction accuracy, and its average prediction accuracy for all indices has increased. 3) Savitzky-Golay-TCN deep convolutional neural network can better monitor financial market changes and effectively predict systemic risk.

| [1] |

J. Cao, X. Chen, R. Qiu, S. Hou, Electric vehicle industry sustainable development with a stakeholder engagement system, Technol. Soc., 67 (2021), 101771. https://doi.org/10.1016/j.techsoc.2021.101771 doi: 10.1016/j.techsoc.2021.101771

|

| [2] |

H. Liu, Y. Wang, R. Xue, M. Linnenluecke, C. W. Cai, Green commitment and stock price crash risk, Financ. Res. Lett., 47 (2022), 102646. https://doi.org/10.1016/j.frl.2021.102646 doi: 10.1016/j.frl.2021.102646

|

| [3] |

X. Yang, J. Cao, Z. Liu, Y. Lai, Environmental policy uncertainty and green innovation: A TVP-VAR-SV model approach, Quant. Financ. Econ., 6 (2022), 604–621. https://doi.org/10.3934/QFE.2022026 doi: 10.3934/QFE.2022026

|

| [4] |

Z. Ouyang, S. Chen, Y. Lai, X. Yang, The correlations among COVID-19, the effect of public opinion, and the systemic risks of China's financial industries, Physica A, 600 (2022), 127518. https://doi.org/10.1016/j.physa.2022.127518 doi: 10.1016/j.physa.2022.127518

|

| [5] |

M. Billio, M. Getmansky, A. W. Lo, L. Pelizzon, Econometric measures of connectedness and systemic risk in the finance and insurance sectors, J. Financ. Econ., 104 (2012), 535–559. https://doi.org/10.1016/j.jfineco.2011.12.010 doi: 10.1016/j.jfineco.2011.12.010

|

| [6] |

L. Eisenberg, T. H. Noe, Systemic risk in financial systems, Manage. Sci., 47 (2001), 236–249. http:/doi.org/10.1287/mnsc.47.2.236.9835 doi: 10.1287/mnsc.47.2.236.9835

|

| [7] |

A. G. Haldane, R. M. May, Systemic risk in banking ecosystems, Nature, 469 (2011), 351–355. https://doi.org/10.1038/nature09659 doi: 10.1038/nature09659

|

| [8] | V. V. Acharya, L. H. Pedersen, T. Philippon, M. Richardson, Measuring systemic risk, in AFA 2011 Denver Meetings Paper, 30 (2017), 2–47. http://doi.org/10.2139/ssrn.1573171 |

| [9] | O. Hart, L. Zingales, A new capital regulation for large financial institutions, Am. Law Econ. Rev., 13 (2011), 453–490. |

| [10] |

M. Foglia, A. Addi, G. J. Wang, E. Angelini, Bearish Vs Bullish risk network: A Eurozone financial system analysis, J. Int. Financ. Mark. Inst. Money, 77 (2022), 101522. https://doi.org/10.1016/j.intfin.2022.101522 doi: 10.1016/j.intfin.2022.101522

|

| [11] |

D. Bisias, M. D. Flood, A. W. Lo, S. Valavanis, A survey of systemic risk analytics, Annu. Rev. Financ. Econ., 4 (2012), 255–296. https://doi.org/10.1146/annurev-financial-110311-101754 doi: 10.1146/annurev-financial-110311-101754

|

| [12] |

G. J. Wang, S. Yi, C. Xie, H. E. Stanley, Multilayer information spillover networks: Measuring interconnectedness of financial institutions, Quant. Financ., 21 (2021), 1163–1185. https://doi.org/10.1080/14697688.2020.1831047 doi: 10.1080/14697688.2020.1831047

|

| [13] |

I. Kurt, M. Ture, A. T. Kurum, Comparing performances of logistic regression, classification and regression tree, and neural networks for predicting coronary artery disease, Expert Syst. Appl., 34 (2008), 366–374. https://doi.org/10.1016/j.eswa.2006.09.004 doi: 10.1016/j.eswa.2006.09.004

|

| [14] |

T. Mo, C. Xie, K. Li, Y. Ouyang, Z. Zeng, Transmission effect of extreme risks in China's financial sectors at major emergencies: Empirical study based on the GPD-CAViaR and TVP-SV-VAR approach, Electron. Res. Arch., 30 (2022), 4657–4673. https://doi.org/10.3934/era.2022236 doi: 10.3934/era.2022236

|

| [15] |

R. E. Streit, D. Borenstein, An agent-based simulation model for analyzing the governance of the Brazilian Financial System, Expert Syst. Appl., 36 (2009), 11489–11501. https://doi.org/10.1016/j.eswa.2009.03.043 doi: 10.1016/j.eswa.2009.03.043

|

| [16] |

H. Wang, W. Yi, Y. Liu, An innovative approach of determining the sample data size for machine learning models: a case study on health and safety management for infrastructure workers, Electron. Res. Arch., 30 (2022), 3452–3462. https://doi.org/10.3934/era.2022176 doi: 10.3934/era.2022176

|

| [17] |

J. A. Frankel, A. K. Rose, Currency crashes in emerging markets: An empirical treatment, J. Int. Econ., 41 (1996), 351–366. https://doi.org/10.1016/S0022-1996(96)01441-9 doi: 10.1016/S0022-1996(96)01441-9

|

| [18] |

J. Sachs, A. Tornell, A. Velasco, The Mexican peso crisis: Sudden death or death foretold?, J. Int. Econ., 41 (1996), 265–283. https://doi.org/10.1016/S0022-1996(96)01437-7 doi: 10.1016/S0022-1996(96)01437-7

|

| [19] |

G. Kaminsky, S. Lizondo, C. M. Reinhart, Leading indicators of currency crises, IMF Staff Pap., 45 (1998), 1–48, . https://doi.org/10.2307/3867328 doi: 10.2307/3867328

|

| [20] |

A. Alter, Y. S. Schüler, Credit spread interdependencies of European states and banks during the financial crisis, J. Bank Financ., 36 (2012), 3444–3468. https://doi.org/10.1016/j.jbankfin.2012.08.002 doi: 10.1016/j.jbankfin.2012.08.002

|

| [21] |

J. Yun, H. Moon, Measuring systemic risk in the Korean banking sector via dynamic conditional correlation models, Pac.-Basin Financ. J., 27 (2014), 94–114. https://doi.org/10.1016/j.pacfin.2014.02.005 doi: 10.1016/j.pacfin.2014.02.005

|

| [22] |

R. Deyoung, A. Gron, G. Torna, A. Winton, Risk overhang and loan portfolio decisions: Small business loan supply before and during the financial crisis, J. Financ., 70 (2015), 2451–2488. https://doi.org/10.1111/jofi.12356 doi: 10.1111/jofi.12356

|

| [23] |

F. J. L. Iturriaga, I. P. Sanz, Bankruptcy visualization and prediction using neural networks: A study of US commercial banks, Expert Syst. Appl., 42 (2015), 2857–2869. https://doi.org/10.1016/j.eswa.2014.11.025 doi: 10.1016/j.eswa.2014.11.025

|

| [24] |

J. Cao, Z. Li, J. Li, Financial time series forecasting model based on CEEMDAN and LSTM, Physica A, 519 (2019), 127–139. https://doi.org/10.1016/j.physa.2018.11.061 doi: 10.1016/j.physa.2018.11.061

|

| [25] |

G. Ding, L. Qin, Study on the prediction of stock price based on the associated network model of LSTM, Int. J. Mach. Learn. Cyber., 11 (2020), 1307–1317. https://doi.org/10.1007/s13042-019-01041-1 doi: 10.1007/s13042-019-01041-1

|

| [26] |

E. Hadavandi, H. Shavandi, A. Ghanbari, Integration of fuzzy genetic systems and artificial neural networks for stock price forecasting, Knowledge-Based Syst., 23 (2010), 800–808. https://doi.org/10.1016/j.knosys.2010.05.004 doi: 10.1016/j.knosys.2010.05.004

|

| [27] |

B. M. Henrique, V. A. Sobreiro, H. Kimura, Literature review: Machine learning techniques applied to financial market prediction, Expert Syst. Appl., 124 (2019), 226–251. https://doi.org/10.1016/j.eswa.2019.01.012 doi: 10.1016/j.eswa.2019.01.012

|

| [28] |

U. Ugurlu, I. Oksuz, O. Tas, Electricity price forecasting using recurrent neural networks, Energies, 11 (2018), 1255. https://doi.org/10.3390/en11051255 doi: 10.3390/en11051255

|

| [29] |

D. Xiao, C. Qin, J. Ge, P. Xia, Y. Huang, C. Liu, Self-attention-based adaptive remaining useful life prediction for IGBT with Monte Carlo dropout, Knowledge-Based Syst., 239 (2022), 107902. https://doi.org/10.1016/j.knosys.2021.107902 doi: 10.1016/j.knosys.2021.107902

|

| [30] |

W. Dai, Y. An, W. Long, Price change prediction of ultra high-frequency financial data based on temporal convolutional network, Procedia Comput. Sci., 199 (2022), 1177–1183. https://doi.org/10.1016/j.procs.2022.01.149 doi: 10.1016/j.procs.2022.01.149

|

| [31] | S. Deng, N. Zhang, W. Zhang, J. Chen, J. Z. Pan, H. Chen, Knowledge-driven stock trend prediction and explanation via a temporal convolutional network, in Companion Proceedings of The 2019 World Wide Web Conference, (2019), 678–685. https://doi.org/10.1145/3308560.3317701 |

| [32] |

R. W. Schafer, What is a Savitzky-Golay filter?, IEEE Signal Process. Mag., 28 (2011), 111–117. https://doi.org/10.1109/MSP.2011.941097 doi: 10.1109/MSP.2011.941097

|

| [33] |

S. Giglio, B. Kelly, S. Pruitt, Systemic risk and the macroeconomy: An empirical evaluation, J. Financ. Econ., 119 (2016), 457–471. https://doi.org/10.1016/j.jfineco.2016.01.010 doi: 10.1016/j.jfineco.2016.01.010

|

| [34] | T. Adrian, M. K. Brunnermeier, CoVaR, Am. Econ. Rev., 106 (2016), 1705–1741. http://doi.org/10.3386/w17454 |

| [35] |

L. Allen, T. G. Bali, Y. Tang, Does systemic risk in the financial sector predict future economic downturns?, Rev. Financ. Stud., 25 (2012), 3000–3036. https://doi.org/10.1093/rfs/hhs094 doi: 10.1093/rfs/hhs094

|

| [36] |

M. Kritzman, Y. Li, S. Page, R. Rigobon, Principal components as a measure of systemic risk, MIT Sloan Res. Pap., 37 (2010), 112–126. http://doi.org/10.2139/ssrn.1582687 doi: 10.2139/ssrn.1582687

|

| [37] |

J. M. Pollet, M. Wilson, Average correlation and stock market returns, J. Financ. Econ., 96 (2010), 364–380. https://doi.org/10.1016/j.jfineco.2010.02.011 doi: 10.1016/j.jfineco.2010.02.011

|

| [38] |

D. K. Patro, M. Qi, X. Sun, A simple indicator of systemic risk, J. Financ. Stab., 9 (2013), 105–116. https://doi.org/10.1016/j.jfs.2012.03.002 doi: 10.1016/j.jfs.2012.03.002

|

| [39] | L. Di Persio, O. Honchar, Artificial neural network architectures for stock price prediction: Comparisons and applications, Int. J. Circuits Syst. Signal Process., 10 (2016), 403–413. |

Figures(7) / Tables(6)

Xite Yang, Ankang Zou, Jidi Cao, Yongzeng Lai, Jilin Zhang. Systemic risk prediction based on Savitzky-Golay smoothing and temporal convolutional networks[J]. Electronic Research Archive, 2023, 31(5): 2667-2688. doi: 10.3934/era.2023135

DownLoad:

DownLoad: