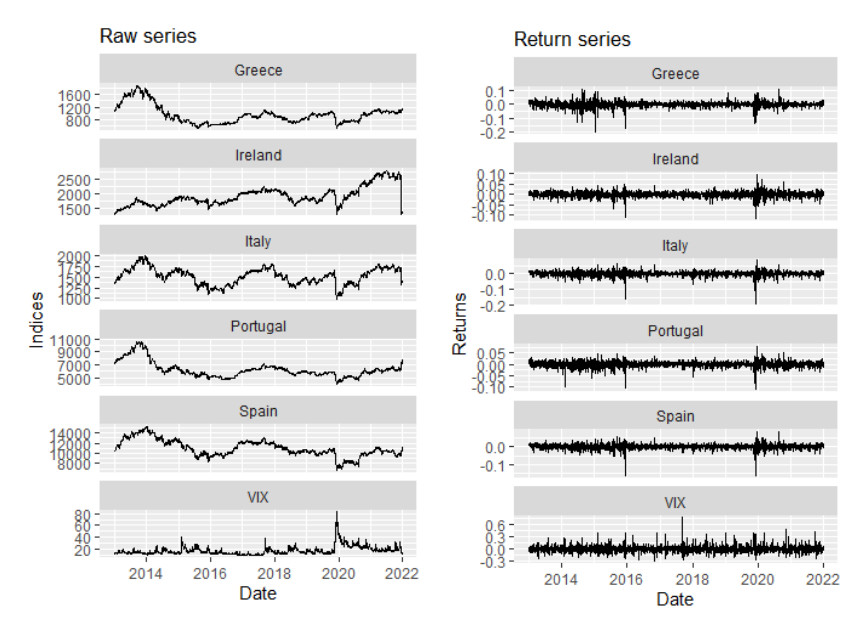

The GIIPS economies are noted to suffer the most consequences of systemic crises. Regardless of their bad performance in crisis periods, their role(s) in asset allocation and portfolio management cannot go unnoticed. For effective portfolio management across divergent timescales, cross-market interdependencies cannot be side-lined. This study examines the conditional and unconditional co-movements of stock market returns of GIIPS economies incorporating investor fear in their time-frequency connectedness. As a result, the bi-, partial, and multiple wavelet approaches are employed. Our findings explicate that the high interdependencies between the stock market returns of GIIPS across all time scales are partly driven by investor fear, implying that extreme investor sentiment could influence stock market prices in GIIPS. The lagging role of Spanish stock market returns manifests at zero lags at high (lower) and medium frequencies (scales). At lower frequencies (higher scales), particularly quarterly-to-biannual and biannual-to-annual, Spanish and Irish stock markets, respectively, lag all other markets. Although portfolio diversification and safe haven benefits are minimal with GIIPS stocks, their volatilities could be hedged against by investing in the US VIX. Intriguing inferences for international portfolio and risk management are offered by our findings.

Citation: Samuel Kwaku Agyei, Ahmed Bossman. Investor sentiment and the interdependence structure of GIIPS stock market returns: A multiscale approach[J]. Quantitative Finance and Economics, 2023, 7(1): 87-116. doi: 10.3934/QFE.2023005

The GIIPS economies are noted to suffer the most consequences of systemic crises. Regardless of their bad performance in crisis periods, their role(s) in asset allocation and portfolio management cannot go unnoticed. For effective portfolio management across divergent timescales, cross-market interdependencies cannot be side-lined. This study examines the conditional and unconditional co-movements of stock market returns of GIIPS economies incorporating investor fear in their time-frequency connectedness. As a result, the bi-, partial, and multiple wavelet approaches are employed. Our findings explicate that the high interdependencies between the stock market returns of GIIPS across all time scales are partly driven by investor fear, implying that extreme investor sentiment could influence stock market prices in GIIPS. The lagging role of Spanish stock market returns manifests at zero lags at high (lower) and medium frequencies (scales). At lower frequencies (higher scales), particularly quarterly-to-biannual and biannual-to-annual, Spanish and Irish stock markets, respectively, lag all other markets. Although portfolio diversification and safe haven benefits are minimal with GIIPS stocks, their volatilities could be hedged against by investing in the US VIX. Intriguing inferences for international portfolio and risk management are offered by our findings.

| [1] |

Adam AM (2020) Susceptibility of stock market returns to international economic policy: Evidence from effective transfer entropy of Africa with the implication for open innovation. J Open Innov Technol Mark Complex 6: 71. https://doi.org/10.3390/joitmc6030071 doi: 10.3390/joitmc6030071

|

| [2] |

Agyei SK (2022) Diversification benefits between stock returns from Ghana and Jamaica: Insights from time-frequency and VMD-based asymmetric quantile-on-quantile analysis. Math Probl Eng 2022: 1–16. https://doi.org/10.1155/2022/9375170 doi: 10.1155/2022/9375170

|

| [3] |

Agyei SK (2023) Emerging markets equities' response to geopolitical risk: Time-frequency evidence from the Russian-Ukrainian conflict era. Heliyon 9: e13319. https://doi.org/10.1016/j.heliyon.2023.e13319 doi: 10.1016/j.heliyon.2023.e13319

|

| [4] |

Agyei SK, Adam AM, Bossman A, et al. (2022a) Does volatility in cryptocurrencies drive the interconnectedness between the cryptocurrencies market? Insights from wavelets. Cogent Econ Financ 10: 2061682. https://doi.org/10.1080/23322039.2022.2061682 doi: 10.1080/23322039.2022.2061682

|

| [5] |

Agyei SK, Isshaq Z, Frimpong S, et al. (2021) COVID‐19 and food prices in sub‐Saharan Africa. Afr Dev Rev 33: S102-S113. https://doi.org/10.1111/1467-8268.12525 doi: 10.1111/1467-8268.12525

|

| [6] |

Agyei SK, Owusu Junior P, Bossman A, et al. (2022b). Spillovers and contagion between BRIC and G7 markets: New evidence from time-frequency analysis. PLoS ONE 17: e0271088. https://doi.org/10.1371/journal.pone.0271088 doi: 10.1371/journal.pone.0271088

|

| [7] |

Aharon DY, Umar Z, Vo XV (2021) Dynamic spillovers between the term structure of interest rates, bitcoin, and safe‑haven currencies. Financ Innov 7: 1–25. https://doi.org/10.1186/s40854-021-00274-w doi: 10.1186/s40854-021-00274-w

|

| [8] |

Ahmad AH, Aworinde OB (2021) Fiscal and external deficits nexus in GIIPS countries: Evidence from parametric and nonparametric causality tests. Int Adv Econ Res 27: 171–184. https://doi.org/10.1007/s11294-021-09829-0 doi: 10.1007/s11294-021-09829-0

|

| [9] |

Algieri B (2013) An empirical analysis of the nexus between external balance and government budget balance: The case of the GIIPS countries. Econ Syst 37: 233–253. https://doi.org/10.1016/j.ecosys.2012.11.002 doi: 10.1016/j.ecosys.2012.11.002

|

| [10] |

Algieri B (2014) Drivers of export demand: A focus on the GIIPS countries. World Econ 37: 1454–1482. https://doi.org/10.1111/twec.12153 doi: 10.1111/twec.12153

|

| [11] | Andreas K (2020) Twitter and traditional news media effect on Eurozone's stock market. International Hellenic University. |

| [12] |

Andrikopoulos A, Samitas A, Kougepsakis K (2014) Volatility transmission across currencies and stock markets: GIIPS in crisis. Appl Financ Econ 24: 1261–1283. https://doi.org/10.1080/09603107.2014.925054 doi: 10.1080/09603107.2014.925054

|

| [13] |

Apergis N, Chi M, Lau K, et al. (2016) Media sentiment and CDS spread spillovers: Evidence from the GIIPS countries. Int Rev Financ Anal 47: 50–59. https://doi.org/10.1016/j.irfa.2016.06.010 doi: 10.1016/j.irfa.2016.06.010

|

| [14] |

Armah M, Amewu G, Bossman A (2022) Time-frequency analysis of financial stress and global commodities prices: Insights from wavelet-based approaches. Cogent Econ Financ 10: 2114161. https://doi.org/10.1080/23322039.2022.2114161 doi: 10.1080/23322039.2022.2114161

|

| [15] |

Asafo-Adjei E, Adam AM, Darkwa P (2021) Can crude oil price returns drive stock returns of oil producing countries in Africa? Evidence from bivariate and multiple wavelet. Macroecon Financ Emerg Mark Econ, 1–19. https://doi.org/10.1080/17520843.2021.1953864 doi: 10.1080/17520843.2021.1953864

|

| [16] |

Asafo-Adjei E, Agyapong D, Agyei SK, et al. (2020) Economic policy uncertainty and stock returns of Africa: A wavelet coherence analysis. Discrete Dyn Nat Soc 2020: 1–8. https://doi.org/10.1155/2020/8846507 doi: 10.1155/2020/8846507

|

| [17] |

Asafo-Adjei E, Bossman A, Boateng E, et al. (2022) A nonlinear approach to quantifying investor fear in stock markets of BRIC. Math Probl Eng 2022: 1–20. https://doi.org/10.1155/2022/9296973 doi: 10.1155/2022/9296973

|

| [18] |

Baur DG, Lucey BM (2010) Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold. Financ Rev 45: 217–229. https://doi.org/10.1111/j.1540-6288.2010.00244.x doi: 10.1111/j.1540-6288.2010.00244.x

|

| [19] |

Beetsma R, Giuliodori M, de Jong F, et al. (2013) Spread the news: The impact of news on the European sovereign bond markets during the crisis. J Int Money Financ 34: 83–101. https://doi.org/10.1016/j.jimonfin.2012.11.005 doi: 10.1016/j.jimonfin.2012.11.005

|

| [20] |

Bossman A (2021) Information flow from COVID-19 pandemic to Islamic and conventional equities: An ICEEMDAN-induced transfer entropy analysis. Complexity 2021: 1–20. https://doi.org/10.1155/2021/4917051 doi: 10.1155/2021/4917051

|

| [21] |

Bossman A, Adam AM, Owusu Junior P, et al. (2022a) Assessing interdependence and contagion effects on the bond yield and stock returns nexus in Sub-Saharan Africa: Evidence from wavelet analysis. Sci Afr 16: e01232. https://doi.org/10.1016/j.sciaf.2022.e01232 doi: 10.1016/j.sciaf.2022.e01232

|

| [22] |

Bossman A, Agyei SK (2022a) ICEEMDAN-based transfer entropy between global commodity classes and African equities. Math Probl Eng 2022: 1–28. https://doi.org/10.1155/2022/8964989 doi: 10.1155/2022/8964989

|

| [23] |

Bossman A, Agyei SK (2022b) Interdependence structure of global commodity classes and African equity markets: A vector wavelet coherence analysis. Resour Policy 79: 103039. https://doi.org/10.1016/j.resourpol.2022.103039 doi: 10.1016/j.resourpol.2022.103039

|

| [24] |

Bossman A, Agyei SK, Owusu Junior P, et al. (2022b) Flights-to-and-from-quality with Islamic and conventional bonds in the COVID-19 pandemic era: ICEEMDAN-based transfer entropy. Complexity 2022: 1–25. https://doi.org/10.1155/2022/1027495 doi: 10.1155/2022/1027495

|

| [25] |

Bossman A, Agyei SK, Umar Z, et al. (2023) The impact of the US yield curve on sub-Saharan African equities. Financ Res Letters, 103636. https://doi.org/ 10.1016/j.frl.2023.103636 doi: 10.1016/j.frl.2023.103636

|

| [26] |

Bossman A, Owusu Junior P, Tiwari AK (2022c) Dynamic connectedness and spillovers between Islamic and conventional stock markets: time- and frequency-domain approach in COVID-19 era. Heliyon 8: e09215. https://doi.org/10.1016/J.HELIYON.2022.E09215 doi: 10.1016/J.HELIYON.2022.E09215

|

| [27] |

Bossman A, Teplova T, Umar Z (2022d) Do local and world COVID-19 media coverage drive stock markets? Time-frequency analysis of BRICS. Complexity 2022: 2249581. https://doi.org/10.1155/2022/2249581 doi: 10.1155/2022/2249581

|

| [28] |

Bossman A, Umar Z, Agyei SK, et al. (2022e) A new ICEEMDAN-based transfer entropy quantifying information flow between real estate and policy uncertainty. Res Econ, 189–205. https://doi.org/10.1016/j.rie.2022.07.002 doi: 10.1016/j.rie.2022.07.002

|

| [29] | Bouri E, Lien D, Roubaud D, et al. (2018) Fear linkages between the US and BRICS stock markets: A frequency-domain causality. Int J Econ Bus 25: 441–454. |

| [30] |

Chiang S, Liu W, Suardi S, et al. (2021) United we stand divided we fall: The time-varying factors driving European Union stock returns. J Int Financ Mark Inst Money 71: 101316. https://doi.org/10.1016/j.intfin.2021.101316 doi: 10.1016/j.intfin.2021.101316

|

| [31] |

de Vries T, de Haan J (2016) Credit ratings and bond spreads of the GIIPS. Appl Econ Lett 23: 107–111. https://doi.org/10.1080/13504851.2015.1054063 doi: 10.1080/13504851.2015.1054063

|

| [32] |

Dergiades T, Milas C, Panagiotidis T (2015) Tweets, Google trends, and sovereign spreads in the GIIPS. Oxford Econ Pap 67: 406–432. https://doi.org/10.1093/oep/gpu046 doi: 10.1093/oep/gpu046

|

| [33] | Ewaida HYM (2017) The impact of sovereign debt on growth: An empirical study on GIIPS versus JUUSD countries. Eur Res Stud J 20: 607–633. |

| [34] | Fama EF (1970) Efficient Market Hypothesis: A Review of Theory and Empirical Work. J Financ 25: 383–417. |

| [35] |

Fernández-Macho J (2012) Wavelet multiple correlation and cross-correlation: A multiscale analysis of Eurozone stock markets. Phys A 391: 1097–1104. https://doi.org/10.1016/J.PHYSA.2011.11.002 doi: 10.1016/J.PHYSA.2011.11.002

|

| [36] |

Flavin TJ, Lagoa-varela D (2019) On the stability of stock-bond comovements across market conditions in the Eurozone periphery. Global Financ J December 2018: 100491. https://doi.org/10.1016/j.gfj.2019.100491 doi: 10.1016/j.gfj.2019.100491

|

| [37] |

Forbes KJ, Rigobon R (2001) Measuring contagion: conceptual and empirical issues. Int Financ Contagion, 43–66. https://doi.org/10.1007/978-1-4757-3314-3_3 doi: 10.1007/978-1-4757-3314-3_3

|

| [38] |

Forbes KJ, Rigobon R (2002) No contagion, only interdependence: Measuring stock market comovements. J Financ 57: 2223–2261. https://doi.org/10.1111/0022-1082.00494 doi: 10.1111/0022-1082.00494

|

| [39] |

Frimpong S, Gyamfi EN, Ishaq Z, et al. (2021) Can global economic policy uncertainty drive the interdependence of agricultural commodity prices? Evidence from partial wavelet coherence analysis. Complexity. https://doi.org/10.1155/2021/8848424 doi: 10.1155/2021/8848424

|

| [40] |

He X, Gokmenoglu KK, Kirikkaleli D, et al. (2021) Co-movement of foreign exchange rate returns and stock market returns in an emerging market: Evidence from the wavelet coherence approach. Int J Financ Econ 2020: 1–12. https://doi.org/10.1002/ijfe.2522 doi: 10.1002/ijfe.2522

|

| [41] | Heryán T, Ziegelbauer J (2016) Volatility of yields of government bonds among GIIPS countries during the sovereign debt crisis in the Euro area. Q J Econ Econ Policy 11: 62–74. |

| [42] |

Islam R, Volkov V (2021) Contagion or interdependence? Comparing spillover indices. Empir Econ 63: 1403–1455. https://doi.org/10.1007/s00181-021-02169-2 doi: 10.1007/s00181-021-02169-2

|

| [43] | Kamaludin K, Sundarasen S, Ibrahim I (2021) Covid-19, Dow Jones and equity market movement in ASEAN-5 countries: evidence from wavelet analyses. Heliyon 7: e05851. |

| [44] |

Karanasos M, Yfanti S, Hunter J (2022) Emerging stock market volatility and economic fundamentals: the importance of US uncertainty spillovers, financial and health crises. Ann Oper Res 313: 1077–1116. https://doi.org/10.1007/s10479-021-04042-y doi: 10.1007/s10479-021-04042-y

|

| [45] |

Kenourgios D, Umar Z, Lemonidi P (2020) On the effect of credit rating announcements on sovereign bonds: International evidence. Int Econ 163: 58–71. https://doi.org/10.1016/j.inteco.2020.04.006 doi: 10.1016/j.inteco.2020.04.006

|

| [46] |

Lee H (2021) Time-varying comovement of stock and treasury bond markets in Europe: A quantile regression approach. Int Rev Econ Financ 75: 1–20. https://doi.org/10.1016/j.iref.2021.03.020 doi: 10.1016/j.iref.2021.03.020

|

| [47] | Lo AW (2004) The adaptive markets hypothesis. J Portf Manage 30: 15–29. |

| [48] | Magnus N, Blikstad D (2018) The GIIPS crisis in the context of the European Monetary Union: a political economy approach. Brazilian Keynesian Rev 4: 224–249. |

| [49] |

Morlet J, Arens G, Fourgeau E, et al. (1982) Wave propagation and sampling theory - Part Ⅰ: Complex signal and scattering in multilayered media. Geophysics 47: 203–221. https://doi.org/10.1190/1.1441328 doi: 10.1190/1.1441328

|

| [50] | Muller UA, Dacorogna MM, Dav RD, et al. (1997) Volatilities of different time resolutions - Analyzing the dynamics of market components. J Empir Financ 4: 213–239. |

| [51] |

Nazlioglu S, Altuntas M, Kilic E, et al. (2021) Purchasing power parity in GIIPS countries: evidence from unit root tests with breaks and non-linearity. Appl Econ Anal 30: 176–195. https://doi.org/10.1108/AEA-10-2020-0146 doi: 10.1108/AEA-10-2020-0146

|

| [52] |

Owusu Junior P, Adam AM, Asafo-Adjei E, et al. (2021) Time-frequency domain analysis of investor fear and expectations in stock markets of BRIC economies. Heliyon 7: e08211. https://doi.org/10.1016/j.heliyon.2021.e08211 doi: 10.1016/j.heliyon.2021.e08211

|

| [53] |

Owusu Junior P, Frimpong S, Adam AM, et al. (2021) COVID-19 as information transmitter to global equity markets: Evidence from CEEMDAN-based transfer entropy approach. Math Probl Eng 2021: 1–19. https://doi.org/10.1155/2021/8258778 doi: 10.1155/2021/8258778

|

| [54] | Rapach DE, Strauss JK, Zhou G (2013) International stock return predictability: what is the role of the United States? J Financ 68: 1633–1662. |

| [55] | Reichlin P (2020) The GIIPS Countries in the Great Recession: Was it a Failure of the Monetary Union? Luiss School of European Political Economy. |

| [56] |

Riaz Y, Shehzad CT, Umar Z (2020) The sovereign yield curve and credit ratings in GIIPS. Int Rev Financ 21: 895–916. https://doi.org/10.1111/irfi.12306 doi: 10.1111/irfi.12306

|

| [57] |

Rua A, Nunes LC (2009) International comovement of stock market returns: A wavelet analysis. J Empir Financ 16: 632–639. https://doi.org/10.1016/j.jempfin.2009.02.002 doi: 10.1016/j.jempfin.2009.02.002

|

| [58] | Sarwar G, Khan W (2017) The effect of US stock market uncertainty on emerging market returns. Emerg Mark Financ Trade 53: 1796–1811. |

| [59] |

Shahzad SJH, Bouri E, et al. (2022) The hedge asset for BRICS stock markets: Bitcoin, gold or VIX. World Econ 45: 292–316. https://doi.org/10.1111/TWEC.13138 doi: 10.1111/TWEC.13138

|

| [60] |

Silva N (2021) Information transmission between stock and bond markets during the Eurozone debt crisis: evidence from industry returns. Spanish J Financ Account 50: 381–394. https://doi.org/10.1080/02102412.2020.1829422 doi: 10.1080/02102412.2020.1829422

|

| [61] |

Torrence C, Compo GP (1998) A Practical Guide to Wavelet Analysis. Bull Am Meteorol Soc 79: 61–78. https://doi.org/10.1175/1520-0477 doi: 10.1175/1520-0477

|

| [62] |

Torrence C, Webster PJ (1999) Interdecadal changes in the ENSO-Monsoon system. J Clim 12: 2679–2690. https://doi.org/10.1175/1520-0442(1999)012<2679:ICITEM>2.0.CO;2 doi: 10.1175/1520-0442(1999)012<2679:ICITEM>2.0.CO;2

|

| [63] |

Umar Z, Bossman A, Choi S, et al. (2023) The relationship between global risk aversion and returns from safe-haven assets. Financ Res Lett 51: 103444. https://doi.org/10.1016/j.frl.2022.103444 doi: 10.1016/j.frl.2022.103444

|

| [64] |

Umar Z, Bossman A, Choi S, et al. (2022a) Are short stocks susceptible to geopolitical shocks? Time-Frequency evidence from the Russian-Ukrainian conflict. Financ Res Lett, 103388. https://doi.org/10.1016/j.frl.2022.103388 doi: 10.1016/j.frl.2022.103388

|

| [65] |

Umar Z, Gubareva M, Teplova T, et al. (2022b) Oil price shocks and the term structure of the US yield curve: a time-frequency analysis of spillovers and risk transmission. Ann Oper Res, 1–25. https://doi.org/10.1007/s10479-022-04786-1 doi: 10.1007/s10479-022-04786-1

|

| [66] |

Umar Z, Gubareva M, Yousaf I, et al. (2021) A tale of company fundamentals vs sentiment driven pricing: The case of GameStop. J Behav Exp Financ 30: 100501. https://doi.org/10.1016/j.jbef.2021.100501 doi: 10.1016/j.jbef.2021.100501

|

QFE-07-01-005-s001.pdf QFE-07-01-005-s001.pdf |

|

Figures(6) / Tables(3)

Samuel Kwaku Agyei, Ahmed Bossman. Investor sentiment and the interdependence structure of GIIPS stock market returns: A multiscale approach[J]. Quantitative Finance and Economics, 2023, 7(1): 87-116. doi: 10.3934/QFE.2023005

DownLoad:

DownLoad: