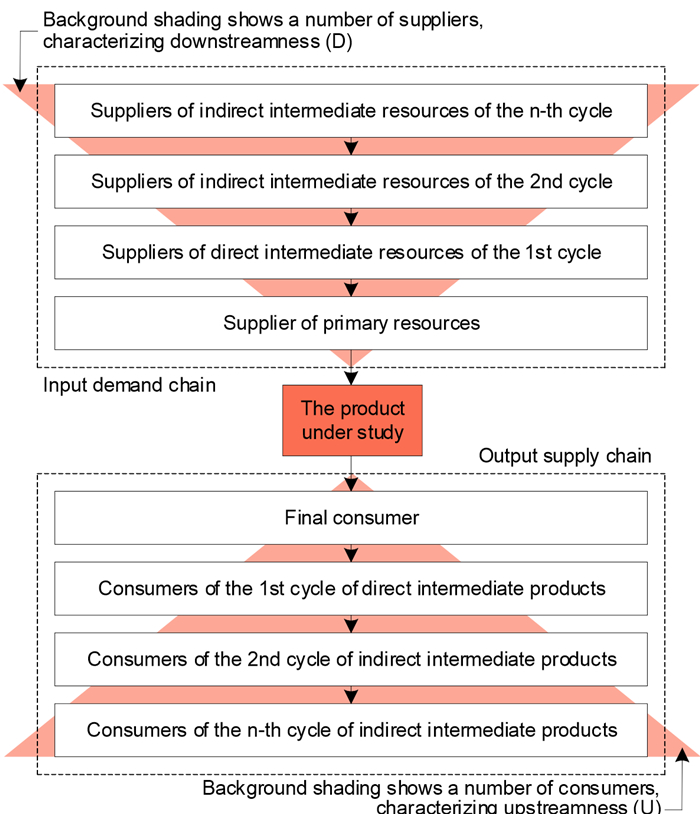

We analyze the dynamics of the production cooperation development in Russia in 2011–2020 on the basis of Input-Output tables. For this purpose, we use indicators that characterize the degree of fragmentation of production and help assess enterprises' interaction in input demand and output supply chains.

Citation: Evgenii Lukin, Tamara Uskova. Development of production cooperation in Russia: Quantitative measurement[J]. National Accounting Review, 2023, 5(4): 322-337. doi: 10.3934/NAR.2023019

We analyze the dynamics of the production cooperation development in Russia in 2011–2020 on the basis of Input-Output tables. For this purpose, we use indicators that characterize the degree of fragmentation of production and help assess enterprises' interaction in input demand and output supply chains.

| [1] |

Antràs P, Chor D, Fally T, et al. (2012) Measuring the upstreamness of production and trade flows. Am Econ Rev 102: 412–416. https://doi.org/10.3386/w17819. doi: 10.3386/w17819

|

| [2] | Belousova AV (2012) Interregional interaction: impact on the regional economy (Khabarovsk krai). Spatial Economics 4: 127–137. |

| [3] |

Ben Yahia W, Cheikhrouhou N, Ayadi O, et al. (2017) A multi-objective optimisation model for cooperative supply chain planning. Int J Serv Oper Manag 26: 211–237. https://doi.org/10.1504/IJSOM.2017.081491 doi: 10.1504/IJSOM.2017.081491

|

| [4] |

Chen B (2017) Upstreamness, exports, and wage inequality: evidence from Chinese manufacturing data. J Asian Econ 48: 66–74. https://doi.org/10.1016/j.asieco.2016.11.003 doi: 10.1016/j.asieco.2016.11.003

|

| [5] | De P (2014) Strengthening Regional Trade and Production Networks Through Transport Connectivity in South and South-West Asia. South and South-West Asia Development Papers 1401: 1–35. |

| [6] | Fally T (2012) Production Staging: Measurement and Facts. University of Colorado-Boulder. |

| [7] | Gavrilyuk AV (2016) Scientific, Technological and Industrial Cooperation: Development Trends. E-Journal. Public Administration 56: 114–133. |

| [8] |

Han W, Wang J (2015) The impact of cooperation mechanism on the chaotic behaviours in nonlinear supply chains. Eur J Ind Eng 9: 595–612. https://doi.org/10.1504/EJIE.2015.071773 doi: 10.1504/EJIE.2015.071773

|

| [9] | Joudeh S (2018) Global Value Chain Participation and Prospects for Local Upgrading in the Egyptian-Chinese Economic and Trade Cooperation Zone. The Economic Research Forum 1278: 25. |

| [10] |

Kim T, Cheong JW, Lee JH, et al. (2013) Strategies to Strengthen Industrial Cooperation with Major Emerging Countries in Southeast Asia. KIEP Research Paper, Policy Analysis 13–22. https://doi.org/10.2139/ssrn.2436804 doi: 10.2139/ssrn.2436804

|

| [11] | Kurganov YA (2016) Industrial cooperation development in Russia's automotive industry under sanctions. Russ Foreign Econ J 1: 119–127. |

| [12] | Kuznetsov D, Sedalishchev V (2018) Research on the average position of Russian economic sectors in value chains. Econ Policy 13: 48–63. |

| [13] |

Lukin EV (2019) Sectoral and territorial specifics of value-added chains in Russia: the input-output approach. Econ Soc Chang Facts Trends Forecast 12: 129–149. https://doi.org/10.15838/esc.2019.6.66.7 doi: 10.15838/esc.2019.6.66.7

|

| [14] | Makarov AV, Trapeznikov VA (2011) Theoretical bases of development of production and technological cooperation. Manager 5–6: 45–51. |

| [15] |

Matsui M (2006) Management game theory: manufacturing vs service enterprise type. Int J Product Qual Manag 1: 103–115. https://doi.org/10.1504/IJPQM.2006.008376 doi: 10.1504/IJPQM.2006.008376

|

| [16] |

Meshkova T, Moiseichev E (2016) Foresight Applications to the Analysis of Global Value Chains. Foresight STI Gov 10: 69–82. https://doi.org/10.17323/1995-459x.2016.1.69.82 doi: 10.17323/1995-459x.2016.1.69.82

|

| [17] |

Miller RE, Temurshoev U (2017) Output upstreamness and input downstreamness of industries/countries in world production. Int Reg Sci Rev 40: 443–475. https://doi.org/10.1177/0160017615608095 doi: 10.1177/0160017615608095

|

| [18] | Okten A, Sengezer B, Camlibel N, et al. (1998) Spatial implications of the organization of production in the automotive industry in Turkey. 38th Congress of the European Regional Science Association, Vienna. Available from: http://www-sre.wu.ac.at/ersa/ersaconfs/ersa98/papers/430.pdf. |

| [19] | Ustyuzhanina EV, Evsyukov SG, Petrov AG (2010) State and prospects of development of the corporate sector of the Russian economy. Moscow: CEMI RAS, 141. |

| [20] |

Voronkova OY, Sorokina VV, Baburin SV (2019) The organizational-economic mechanism for the development of integration processes in the production and processing of products. Int J Econ Bus Admin 7: 207–214. https://doi.org/10.35808/ijeba/236 doi: 10.35808/ijeba/236

|

| [21] |

Yazan DM, Fraccascia L, Mes M, et al. (2018) Cooperation in manure-based biogas production networks: An agent-based modeling approach. Appl Energy 212: 820–833. https://doi.org/10.1016/j.apenergy.2017.12.074 doi: 10.1016/j.apenergy.2017.12.074

|

| [22] | Zaclicever D (2017) Trade integration and production sharing: A characterization of Latin American and Caribbean countries' participation in regional and global value chains. Comer Int 137: 84. |

Figures(8)

Evgenii Lukin, Tamara Uskova. Development of production cooperation in Russia: Quantitative measurement[J]. National Accounting Review, 2023, 5(4): 322-337. doi: 10.3934/NAR.2023019

DownLoad:

DownLoad: