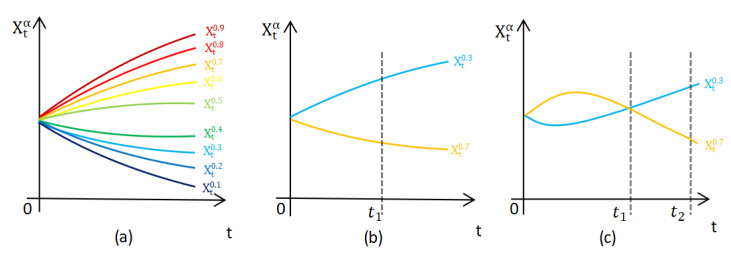

In this paper, we study the higher-order uncertain differential equations (UDEs) as defined by Kaixi Zhang [

Citation: Zeman Wang, Zhong Liu, Zikun Han, Xiuying Guo, Qiubao Wang. The inverse uncertainty distribution of the solutions to a class of higher-order uncertain differential equations[J]. AIMS Mathematics, 2024, 9(11): 33023-33061. doi: 10.3934/math.20241579

In this paper, we study the higher-order uncertain differential equations (UDEs) as defined by Kaixi Zhang [

| [1] | B. Liu, Uncertainty theory, 2 Eds., Berlin: Springer Berlin Heidelberg, 2007. |

| [2] |

K. Yao, X. Chen, A numerical method for solving uncertain differential equations, J. Intell. Fuzzy Syst., 25 (2013), 825–832. http://doi.org/10.3233/IFS-120688 doi: 10.3233/IFS-120688

|

| [3] |

B. Liu, Toward uncertain finance theory, J. Uncertain. Anal. Appl., 1 (2013), 1. https://doi.org/10.1186/2195-5468-1-1 doi: 10.1186/2195-5468-1-1

|

| [4] |

L. Sheng, Y. Zhu, Optimistic value model of uncertain optimal control, Int. J. Uncert. Fuzz. Knowledge-Based Syst., 21 (2013), 75–87. https://doi.org/10.1142/S0218488513400060 doi: 10.1142/S0218488513400060

|

| [5] |

Z. Zhang, X. Yang, Uncertain population model, Soft Comput., 24 (2020), 2417–2423. https://doi.org/10.1007/s00500-018-03678-6 doi: 10.1007/s00500-018-03678-6

|

| [6] |

Z. Liu, X. Yang, A linear uncertain pharmacokinetic model driven by Liu process, Appl. Math. Model., 89 (2021), 1881–1899. https://doi.org/10.1016/j.apm.2020.08.061 doi: 10.1016/j.apm.2020.08.061

|

| [7] |

Z. Liu, R. Kang, Pharmacokinetics with intravenous infusion of two-compartment model based on Liu process, Commun. Statistics-Theory Meth., 53 (2024), 4975–4990. https://doi.org/10.1080/03610926.2023.2198626 doi: 10.1080/03610926.2023.2198626

|

| [8] |

Z. Li, Y. Sheng, Z. Teng, H. Miao, An uncertain differential equation for SIS epidemic model, J. Intell. Fuzzy Syst., 33 (2017), 2317–2327. https://doi.org/10.3233/JIFS-17354 doi: 10.3233/JIFS-17354

|

| [9] |

C. Tian, T. Jin, X. Yang, Q. Liu, Reliability analysis of the uncertain heat conduction model, Comput. Math. Appl., 119 (2022), 131–140. https://doi.org/10.1016/j.camwa.2022.05.033 doi: 10.1016/j.camwa.2022.05.033

|

| [10] |

X. Yang, K. Yao, Uncertain partial differential equation with application to heat conduction, Fuzzy Optim. Decis. Making, 16 (2017), 379–403. https://doi.org/10.1007/s10700-016-9253-9 doi: 10.1007/s10700-016-9253-9

|

| [11] |

K. Zhang, B. Liu, Higher-order derivative of uncertain process and higher-order uncertain differential equation, Fuzzy Optim. Decis. Making, 23 (2024), 295–318. https://doi.org/10.1007/s10700-024-09422-0 doi: 10.1007/s10700-024-09422-0

|

| [12] | B. Liu, Uncertainty theory, 5 Eds., Berlin: Springer, 2024. |

| [13] | B. Liu, Uncertainty theory, 3 Eds., Berlin: Springer, 2010. |

| [14] | B. Liu, Some research problems in uncertainty theory, J. Uncertain Syst., 3 (2009), 3–10. |

| [15] |

X. Chen, D. A. Ralescu, Liu process and uncertain calculus, J. Uncertain. Anal. Appl., 1 (2013), 3. https://doi.org/10.1186/2195-5468-1-3 doi: 10.1186/2195-5468-1-3

|

| [16] |

T. Ye, A rigorous proof of fundamental theorem of uncertain calculus, J. Uncertain Syst., 14 (2021), 2150009. https://doi.org/10.1142/S1752890921500094 doi: 10.1142/S1752890921500094

|

| [17] | B. Liu, Uncertainty theory, 4 Eds., Berlin: Springer Berlin Heidelberg, 2015. |

| [18] |

L. Jia, W. Dai, Uncertain spring vibration equation, J. Indust. Manage. Optim., 18 (2022), 2401. https://doi.org/10.3934/jimo.2021073 doi: 10.3934/jimo.2021073

|

| [19] |

A. Shekhovtsov, Higher order maximum persistency and comparison theorems, Comput. Vision Image Underst., 143 (2016), 54–79. https://doi.org/10.1016/j.cviu.2015.05.002 doi: 10.1016/j.cviu.2015.05.002

|

| [20] | W. Walter, Ordinary differential equations, Berlin: Springer Science & Business Media, 2013. |

Figures(8) / Tables(1)

Zeman Wang, Zhong Liu, Zikun Han, Xiuying Guo, Qiubao Wang. The inverse uncertainty distribution of the solutions to a class of higher-order uncertain differential equations[J]. AIMS Mathematics, 2024, 9(11): 33023-33061. doi: 10.3934/math.20241579

DownLoad:

DownLoad: