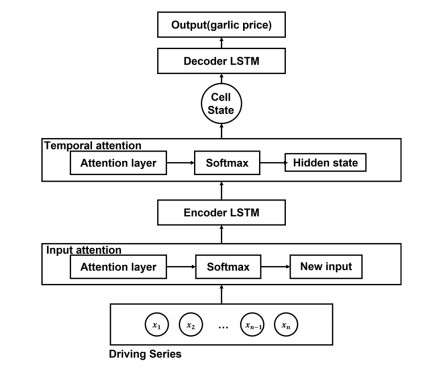

Garlic is a major condiment vegetable grown in South Korea. The price of garlic has a great impact on Korean society and the economy, which requires price stabilization through preemptive supply and demand management. Therefore, the government attempts to keep the price adjusted according to the predicted production cost. However, classic statistical models or well-known deep learning models have lower forecast accuracy when the number of input factors increases. The aforementioned issue could make analysis approaches and their implementation difficult, and the government would confront failure in proper supply and demand management. To solve this problem, we propose a new hybrid deep-learning approach that employs well-known attention models. Recent attention models have achieved outstanding performance in time-series dataset forecasting. However, when input datasets contain dozens or hundreds of variables, the forecasting performance cannot be guaranteed because the prediction accuracy decreases. In this study, a novel approach utilizing attention weights for forecasting prices is introduced. Experience shows that forecasting accuracy can be improved using the proposed model, which deals with different variables related to garlic prices, such as atmospheric conditions, logistics processes, and environmental circumstances. The proposed approach and its model contribute to forecasting outputs for different research domains by using a variety of attention weight models.

Citation: Eunjae Choi, Yoosang Park, Jongsun Choi, Jaeyoung Choi, Libor Mesicek. Forecasting of garlic price based on DA-RNN using attention weight of temporal fusion transformers[J]. Mathematical Biosciences and Engineering, 2023, 20(5): 9041-9061. doi: 10.3934/mbe.2023397

Garlic is a major condiment vegetable grown in South Korea. The price of garlic has a great impact on Korean society and the economy, which requires price stabilization through preemptive supply and demand management. Therefore, the government attempts to keep the price adjusted according to the predicted production cost. However, classic statistical models or well-known deep learning models have lower forecast accuracy when the number of input factors increases. The aforementioned issue could make analysis approaches and their implementation difficult, and the government would confront failure in proper supply and demand management. To solve this problem, we propose a new hybrid deep-learning approach that employs well-known attention models. Recent attention models have achieved outstanding performance in time-series dataset forecasting. However, when input datasets contain dozens or hundreds of variables, the forecasting performance cannot be guaranteed because the prediction accuracy decreases. In this study, a novel approach utilizing attention weights for forecasting prices is introduced. Experience shows that forecasting accuracy can be improved using the proposed model, which deals with different variables related to garlic prices, such as atmospheric conditions, logistics processes, and environmental circumstances. The proposed approach and its model contribute to forecasting outputs for different research domains by using a variety of attention weight models.

| [1] |

J. H. Ha, S. T. Seo, S. W. Kim, Improving forecasting performance for onion and garlic prices, J. Korean Soc. Rural Plann., 25 (2019), 109–117. https://doi.org/10.7851/ksrp.2019.25.4.109 doi: 10.7851/ksrp.2019.25.4.109

|

| [2] | A. Ranjana, S. C. Mehta, Weather based forecasting of crop yields, pests and diseases-IASRI models, J. Ind. Soc. Agril Stat., 61 (2007), 255–263. |

| [3] |

F. Tao, M. Yokozawa, Z. Zhang, Modelling the impacts of weather and climate variability on crop productivity over a large area: a new process-based model development, optimization, and uncertainties analysis, Agric. For. Meteorol., 149 (2009), 831–850. https://doi.org/10.1016/j.agrformet.2008.11.004 doi: 10.1016/j.agrformet.2008.11.004

|

| [4] |

S. Choi, J. Kim, H. Seo, Estimation of garlic's bulb weight at harvest using a multi-level model based on growth and meteorological data, Hortic. Sci. Technol., 39 (2021), 521–529. https://doi.org/10.7235/HORT.20210047 doi: 10.7235/HORT.20210047

|

| [5] |

S. Choi, J. Baek, Garlic yields estimation using climate data, J. Korean Data Inf. Sci. Soc., 27 (2016), 969–977. https://doi.org/10.7465/jkdi.2016.27.4.969 doi: 10.7465/jkdi.2016.27.4.969

|

| [6] |

J. Choi, P. Helmberger, How sensitive are crop yields to price changes and farm programs?, J. Agric. Appl. Econ., 25 (1993), 237–244. https://doi.org/10.1017/S1074070800018794 doi: 10.1017/S1074070800018794

|

| [7] | KREI (Korea Rural Economic Institute), A Study on the Development of Agri-food Trade Model Reflecting Climate Change, 2021. Available from: https://repository.krei.re.kr/bitstream/2018.oak/26046/1/R901.pdf |

| [8] | Hortidaily, 2021. Available from: https://www.hortidaily.com/article/9340224/heavy-rain-causes-severe-damage-to-open-field-fruit-and-vegetable-crops-in-western-europe. |

| [9] | REUTERS, 2021. Available from: https://www.reuters.com/world/us/wither-away-die-us-pacific-northwest-heat-wave-bakes-wheat-fruit-crops-2021-07-12/. |

| [10] | H. Lim, Dual Attention-based LSTM Model for Produce Price Prediction, Master thesis, Sejong university graduate school, Seoul, Korea, 2020. |

| [11] |

H. Yin, D. Jin, Y. H. Gu, C. J. Park, S. K. Han, S. J. Yoo, STL-ATTLSTM: vegetable price forecasting using STL and attention mechanism-based LSTM, Agriculture, 10 (2020), 612. https://doi.org/10.3390/agriculture10120612 doi: 10.3390/agriculture10120612

|

| [12] |

S. Y. Shih, F. K. Sun, H. Y. Lee, Temporal pattern attention for multivariate time series forecasting, Mach. Learn., 108 (2019), 1421–1441. https://doi.org/10.1007/s10994-019-05815-0 doi: 10.1007/s10994-019-05815-0

|

| [13] | S. Huang, D. Wang, X. Wu, A. Tang, DSANet: Dual self-attention network for multivariate time series forecasting, in Proceedings of the 28th ACM International Conference on Information and Knowledge Management, (2019), 2129–2132. https://doi.org/10.1145/3357384.3358132 |

| [14] | T. Hollis, A. Viscardi, S. E. Yi, A comparison of LSTMs and attention mechanisms for forecasting financial time series, preprint, arXiv: 1812.07699. |

| [15] | D. Jin, H. Yin, Y. Gu, S. J. Yoo, Forecasting of vegetable prices using STL-LSTM method, in 2019 6th International Conference on Systems and Informatics (ICSAI), (2019), 866–871. https://doi.org/10.1109/ICSAI48974.2019.9010181 |

| [16] | S. S. Dahikar, S. V. Rode, Agricultural crop yield prediction using artificial neural network approach, Int. J. Innovative Res. Electr., Electron., Instrum. Control Eng., 2 (2014), 683–686. |

| [17] | M. Subhasree, C. A. Priya, Forecasting vegetable price using time series data, Int. J. Adv. Res., 3 (2016), 535–641. |

| [18] | R. K. Kumar, Short term forecasting of Agro-products pricing using Multivariate time series analysis, Doctoral dissertation, Dublin, National College of Ireland, 2020. |

| [19] | S. D. Alwis, Y. Zhang, M. Na, G. Li, Duo attention with deep learning on tomato yield prediction and factor interpretation, in Pacific Rim International Conference on Artificial Intelligence, Springer, Cham, 2019. https://doi.org/10.1007/978-3-030-29894-4_56 |

| [20] |

Y. H. Gu, D. Jin, H. Yin, R. Zheng, X. Piao, S. J. Yoo, Forecasting agricultural commodity prices using dual input attention LSTM, Agriculture, 12 (2022), 256. https://doi.org/10.3390/agriculture12020256 doi: 10.3390/agriculture12020256

|

| [21] | T. Gao, X. Han, Z. Liu, M. Sun, Hybrid attention-based prototypical networks for noisy few-shot relation classification, in Proceedings of the AAAI Conference on Artificial Intelligence, 33 (2019), 6407–6414. https://doi.org/10.1609/aaai.v33i01.33016407 |

| [22] | T. Shen, T. Zhou, G. Long, J. Jiang, S. Wang, C. Zhang, Reinforced self-attention network: a hybrid of hard and soft attention for sequence modeling, preprint, arXiv: 1801.10296. https://doi.org/10.48550/arXiv.1801.10296 |

| [23] | A. Islam, C. Long, R. Radke, A hybrid attention mechanism for weakly-supervised temporal action localization, in Proceedings of the AAAI Conference on Artificial Intelligence, 35 (2021), 1637–1645. |

| [24] | D. Bahdanau, K. Cho, Y. Bengio, Neural machine translation by jointly learning to align and translate, preprint, arXiv: 1409.0473. |

| [25] | K. Cho, B. Van Merriënboer, C. Gulcehre, D. Bahdanau, F. Bougares, H. Schwenk, et al., Learning phrase representations using RNN encoder-decoder for statistical machine translation, preprint, arXiv: 1406.1078. https://doi.org/10.48550/arXiv.1406.1078 |

| [26] | I. Sutskever, O. Vinyals, Q. V. Le, Sequence to sequence learning with neural networks, Adv. Neural Inf. Process. Syst., 27 (2014), 3104–3112. |

| [27] | Y. Qin, D. Song, H. Chen, W. Cheng, G. Jiang, G. Cottrell, A dual-stage attention-based recurrent neural network for time series prediction, preprint, arXiv: 1704.02971. |

| [28] |

B. Lim, S. Ö. Arık, N. Loeff, T. Pfister, Temporal fusion transformers for interpretable multi-horizon time series forecasting, Int. J. Forecasting, 37 (2021), 1748–1764. https://doi.org/10.1016/j.ijforecast.2021.03.012 doi: 10.1016/j.ijforecast.2021.03.012

|

| [29] | Seoul Agro-Fisheries & Food Corporation, Wholesale market information (Garak market), 2021. Available from: https://www.garak.co.kr/cntnts/selectContents.do?cntnts_id = CC010200. |

| [30] | NongNet, Analysis of the amount brought into the wholesale market (garlic), 2021. Available from: https://www.nongnet.or.kr/anss/tkinVolmInfo.do. |

| [31] | Trends and Prospects in Supply and Demand of Seasoning Vegetables in Chapter 14, Agricultural Outlook 2021: Changes in agriculture and rural areas after COVID-19, (2021), 425–441. |

| [32] | R. B. Cleveland, W. S. Cleveland, J. E. McRae, I. J. Terpenning, STL: A seasonal-trend decomposition procedure based on loess, J. Off. Stat., 6 (1990), 3–33. |

| [33] | E. B. Dagum, S. Bianconcini, 2016, Seasonal Adjustment Methods and Real Time Trend-Cycle Estimation, Berlin/Heidelberg, Germany: Springer International Publishing, (2016), 29–57. https://doi.org/10.1007/978-3-319-31822-6_2 |

| [34] |

V. Gómez, A. Maravall, Seasonal adjustment and signal extraction in economic time series, Course Time Ser. Anal., 2001 (2001), 202–247. https://doi.org/10.1002/9781118032978.ch8 doi: 10.1002/9781118032978.ch8

|

Figures(6) / Tables(5)

Eunjae Choi, Yoosang Park, Jongsun Choi, Jaeyoung Choi, Libor Mesicek. Forecasting of garlic price based on DA-RNN using attention weight of temporal fusion transformers[J]. Mathematical Biosciences and Engineering, 2023, 20(5): 9041-9061. doi: 10.3934/mbe.2023397

DownLoad:

DownLoad: