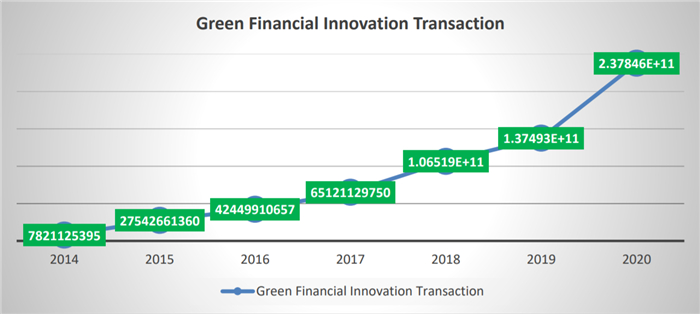

Green innovation is the creation of new and competitive products, services, processes, procedures and systems designed to use natural resources at a minimum level and to provide better quality of life on behalf of all that respects sustainability of the nature and of the future generations. The study objective was to examine the relationship between green innovation and financial performance. The study used an explanatory research design and a quantitative research approach to achieve the study's objective. Secondary time series data collected quarterly during the study period (2014–2020) was utilized to run the regression model. Autoregressive moving average (ARIMA) was used to forecast the growing level of green financial innovation transactions, and autoregressive distributed lag model (ARDL) was used to examine the effect of green financial innovation transactions on financial performance. According to forecasted results, on average green financial innovation transaction is expected to grow by 11 percent each quarter, and its impact on financial performance is found positive and significant in the short run. However, the long-run estimation of ARDL shows the positive and insignificant effect of green financial innovation on financial performance. Based on the study's findings, we recommend that the banking sector focuses on adopting green financial innovations to improve financial performance by taking into account both the short-run and long-run benefits of the products. At the same time, we suggest that the sector focus on those green financial innovations which have the lowest adoption and development costs compared to others since the long-run effect affects the overall financial performance of the sector. The main contribution of this study is to provide future indication on the relationship between the two variables in order to provide proper decision making in a bid to make green innovation investment.

Citation: Goshu Desalegn, Anita Tangl. Forecasting green financial innovation and its implications for financial performance in Ethiopian Financial Institutions: Evidence from ARIMA and ARDL model[J]. National Accounting Review, 2022, 4(2): 95-111. doi: 10.3934/NAR.2022006

Green innovation is the creation of new and competitive products, services, processes, procedures and systems designed to use natural resources at a minimum level and to provide better quality of life on behalf of all that respects sustainability of the nature and of the future generations. The study objective was to examine the relationship between green innovation and financial performance. The study used an explanatory research design and a quantitative research approach to achieve the study's objective. Secondary time series data collected quarterly during the study period (2014–2020) was utilized to run the regression model. Autoregressive moving average (ARIMA) was used to forecast the growing level of green financial innovation transactions, and autoregressive distributed lag model (ARDL) was used to examine the effect of green financial innovation transactions on financial performance. According to forecasted results, on average green financial innovation transaction is expected to grow by 11 percent each quarter, and its impact on financial performance is found positive and significant in the short run. However, the long-run estimation of ARDL shows the positive and insignificant effect of green financial innovation on financial performance. Based on the study's findings, we recommend that the banking sector focuses on adopting green financial innovations to improve financial performance by taking into account both the short-run and long-run benefits of the products. At the same time, we suggest that the sector focus on those green financial innovations which have the lowest adoption and development costs compared to others since the long-run effect affects the overall financial performance of the sector. The main contribution of this study is to provide future indication on the relationship between the two variables in order to provide proper decision making in a bid to make green innovation investment.

| [1] |

Aastvedt T, Behmiri N, Lu L (2021) Does green innovation damage financial performance of oil and gas companies? Resour Policy 73. https://doi.org/10.1016/j.resourpol.2021.102235 doi: 10.1016/j.resourpol.2021.102235

|

| [2] |

Abbasi A, Khalili K, Behmanesh J, Shirzad A (2021) Estimation of ARIMA model parameters for drought prediction using the genetic algorithm. Arab J Geosci 14. https://doi.org/10.1007/s12517-021-07140-0 doi: 10.1007/s12517-021-07140-0

|

| [3] |

Acar G, Yilmaz I (2020) The impact of discretionary accruals on corporate investment decisions: Evidence from GCC countries. Acad J Stud 9: 193-205. https://doi.org/10.36941/AJIS-2020-0124 doi: 10.36941/AJIS-2020-0124

|

| [4] |

Achi A, Adeola O, Achi FC (2022) CSR and green process innovation as antecedents of micro, small, and medium enterprise performance: Moderating role of perceived environmental volatility. J Bus Res 139: 771-781. https://doi.org/10.1016/j.jbusres.2021.10.016 doi: 10.1016/j.jbusres.2021.10.016

|

| [5] |

Achmad Kuncoro E, Sari SA (2015) Factors that affect competitive advantage in freight forwarding industry on Jakarta-Indonesia. Adv Sci Lett 21: 1008-1011. https://doi.org/10.1166/asl.2015.5968 doi: 10.1166/asl.2015.5968

|

| [6] |

Acquah ISK, Essel D, Baah C, et al., (2021) Investigating the efficacy of isomorphic pressures on the adoption of green manufacturing practices and its influence on organizational legitimacy and financial performance. J Manuf Technol Mana 32: 1399-1420. https://doi.org/10.1108/JMTM-10-2020-0404 doi: 10.1108/JMTM-10-2020-0404

|

| [7] |

Adhikari P, Momaya KS (2021) Innovation Capabilities, Environmentally Sustainable Practices and Export Competitiveness: An Exploratory Study of Firms From India. Int J Innov Technol Manage 18. https://doi.org/10.1142/S0219877021500358 doi: 10.1142/S0219877021500358

|

| [8] |

Agarwal S, Zhang J (2020) FinTech, Lending and Payment Innovation: A Review. Asia-Pacific J Financ Stud 49: 353-367. https://doi.org/10.1111/ajfs.12294 doi: 10.1111/ajfs.12294

|

| [9] |

Aguilera-Caracuel J, Ortiz-de-Mandojana N (2013) Green Innovation and Financial Performance: An Institutional Approach. Organ Environ 26: 365-385. https://doi.org/10.1177/1086026613507931 doi: 10.1177/1086026613507931

|

| [10] |

Ahmad M, Wu Y (2022) Combined role of green productivity growth, economic globalization, and eco-innovation in achieving ecological sustainability for OECD economies. J Environ Manage 302. https://doi.org/10.1016/j.jenvman.2021.113980 doi: 10.1016/j.jenvman.2021.113980

|

| [11] |

Ahmar AS, del Val EB, Safty MAE, et al., (2022) SutteARIMA: A novel method for forecasting the infant mortality rate in Indonesia. Comput Mater Con 70: 6007-6022. https://doi.org/10.32604/cmc.2022.021382 doi: 10.32604/cmc.2022.021382

|

| [12] |

Aji BS, Indwiarti, Rohmawati AA (2021) Forecasting Number of COVID-19 Cases in Indonesia with ARIMA and ARIMAX Models. 2021 9th International Conference on Information and Communication Technology (ICoICT) 71-75. https://doi.org/10.1109/ICoICT52021.2021.9527453 doi: 10.1109/ICoICT52021.2021.9527453

|

| [13] |

Akdere C, Benli P (2018) The Nature of Financial Innovation: A Post-Schumpeterian Analysis. J Econ Issues 52: 717-748. https://doi.org/10.1080/00213624.2018.1498717 doi: 10.1080/00213624.2018.1498717

|

| [14] |

Aladağ E (2021a) Forecasting of particulate matter with a hybrid ARIMA model based on wavelet transformation and seasonal adjustment. Urban Clim 39. https://doi.org/10.1016/j.uclim.2021.100930 doi: 10.1016/j.uclim.2021.100930

|

| [15] |

Aladağ E (2021b) Forecasting of particulate matter with a hybrid ARIMA model based on wavelet transformation and seasonal adjustment. Urban Clim 39. https://doi.org/10.1016/j.uclim.2021.100930 doi: 10.1016/j.uclim.2021.100930

|

| [16] |

Allen F (2012) Trends Financial Innovation and their Welfare Impact: An Overview. Eur Financ Manag 18: 493-514. https://doi.org/10.1111/j.1468-036X.2012.00658.x doi: 10.1111/j.1468-036X.2012.00658.x

|

| [17] | Allen F, Qian JQJ, Qian M, et al., (2009) A Review of China's Financial System and Initiatives for the Future, In: Barth, J.R., Tatom, J.A., Yago, G., China's Emerging Financial Markets, Springer, Boston, MA, 8: 3-72. https://doi.org/10.1007/978-0-387-93769-4_1 |

| [18] |

Amore MD, Bennedsen M (2016) Corporate governance and green innovation. J Environ Econ Manag 75: 54-72. https://doi.org/10.1016/j.jeem.2015.11.003 doi: 10.1016/j.jeem.2015.11.003

|

| [19] |

Aron A, Molina O (2020) Green innovation in natural resource industries: The case of local suppliers in the Peruvian mining industry. Extract Ind Soc 7: 353-365. https://doi.org/10.1016/j.exis.2019.09.002 doi: 10.1016/j.exis.2019.09.002

|

| [20] |

Asadi S, OmSalameh Pourhashemi S, Nilashi M, et al., (2020) Investigating influence of green innovation on sustainability performance: A case on Malaysian hotel industry. J Clean Prod 258. https://doi.org/10.1016/j.jclepro.2020.120860 doi: 10.1016/j.jclepro.2020.120860

|

| [21] |

Asni N, Agustia D (2021) The mediating role of financial performance in the relationship between green innovation and firm value: Evidence from ASEAN countries. Eur J Innov Manag. https://doi.org/10.1108/EJIM-11-2020-0459 doi: 10.1108/EJIM-11-2020-0459

|

| [22] |

Baah C, Opoku-Agyeman D, Acquah ISK, et al., (2021) Examining the correlations between stakeholder pressures, green production practices, firm reputation, environmental and financial performance: Evidence from manufacturing SMEs. Sustain Prod Consump 27: 100-114. https://doi.org/10.1016/j.spc.2020.10.015 doi: 10.1016/j.spc.2020.10.015

|

| [23] |

Bakari IH, Idi A, Ibrahim Y (2018) Innovation Determinants of Financial Inclusion in Top Ten African Countries: a System GMM Approach. Market Manag Innov 4: 98-106. https://doi.org/10.21272/mmi.2018.4-09 doi: 10.21272/mmi.2018.4-09

|

| [24] |

Barra C, Ruggiero N (2021) Firm innovation and local bank efficiency in Italy: Does the type of bank matter? Ann Public Coop Econ, 1-46. https://doi.org/10.1111/apce.12345 doi: 10.1111/apce.12345

|

| [25] |

Bartolacci F, Caputo A, Soverchia M (2020) Sustainability and financial performance of small and medium sized enterprises: A bibliometric and systematic literature review. Bus Strateg Environ 29: 1297-1309. https://doi.org/10.1002/bse.2434 doi: 10.1002/bse.2434

|

| [26] |

Benfratello L, Schiantarelli F, Sembenelli A (2008) Banks and innovation: Microeconometric evidence on Italian firms. J Financ Econ 90: 197-217. ELSEVIER SCIENCE SA. https://doi.org/10.1016/j.jfineco.2008.01.001 doi: 10.1016/j.jfineco.2008.01.001

|

| [27] |

Bontis N, Ciambotti M, Palazzi F, et al. (2018) Intellectual capital and financial performance in social cooperative enterprises. J Intellect Cap 19: 294-320. https://doi.org/10.1108/JIC-03-2017-0049 doi: 10.1108/JIC-03-2017-0049

|

| [28] |

Bousqaoui H, Slimani I, Achchab S (2021) Comparative analysis of short-term demand predicting models using ARIMA and deep learning. Int J Elec Comput Eng 11: 3319-3328. Scopus. https://doi.org/10.11591/ijece.v11i4.pp3319-3328 doi: 10.11591/ijece.v11i4.pp3319-3328

|

| [29] |

Calomiris CW (2009) Financial innovation, regulation, and reform. Cato J 29: 65-91. https://doi.org/10.7916/D87M0JFV doi: 10.7916/D87M0JFV

|

| [30] |

Cao S, Nie L, Sun H, et al., (2021) Digital finance, green technological innovation and energy-environmental performance: Evidence from China's regional economies. J Clean Prod 327. https://doi.org/10.1016/j.jclepro.2021.129458 doi: 10.1016/j.jclepro.2021.129458

|

| [31] |

Corrocher N, Ozman M (2020) Green technological diversification of European ICT firms: A patent-based analysis. Econ Innov New Tech 29: 559-581. https://doi.org/10.1080/10438599.2019.1645989 doi: 10.1080/10438599.2019.1645989

|

| [32] |

de Oliveira JA, Cruz Basso LF, Kimura H, et al., (2018) Innovation and financial performance of companies doing business in Brazil. Int J Innov Stud 2: 153-164. https://doi.org/10.1016/j.ijis.2019.03.001 doi: 10.1016/j.ijis.2019.03.001

|

| [33] | Hằng LTT, Dũng NX (2022) ARIMA Model-Vietnam's GDP Forecasting, In: Ngoc Thach, N., Ha, D.T., Trung, N.D., Kreinovich, V., Prediction and Causality in Econometrics and Related Topics, Springer, Cham, 983: 145-151. https://doi.org/10.1007/978-3-030-77094-5_14 |

| [34] |

Hurley DT, Papanikolaou N (2021) Autoregressive Distributed Lag (ARDL) analysis of U.S.-China commodity trade dynamics. Q Rev Econ Financ 81: 454-467. https://doi.org/10.1016/j.qref.2020.10.019 doi: 10.1016/j.qref.2020.10.019

|

| [35] |

Lee KH, Min B (2015) Green R & D for eco-innovation and its impact on carbon emissions and firm performance. J Clean Prod 108: 534-542. https://doi.org/10.1016/j.jclepro.2015.05.114 doi: 10.1016/j.jclepro.2015.05.114

|

| [36] |

Li Y, Ye F, Sheu C, et al., (2018) Linking green market orientation and performance: Antecedents and processes. J Clean Prod 192: 924-931. https://doi.org/10.1016/j.jclepro.2018.05.052 doi: 10.1016/j.jclepro.2018.05.052

|

| [37] |

Lin WL, Cheah JH, Azali M, et al., (2019) Does firm size matter? Evidence on the impact of the green innovation strategy on corporate financial performance in the automotive sector. J Clean Prod 229: 974-988. https://doi.org/10.1016/j.jclepro.2019.04.214 doi: 10.1016/j.jclepro.2019.04.214

|

| [38] | Maan S, Devi G, Rizvi SAM (2022) To Predicit the Layout of COVID-19 by Using ARIMA Model. In: Somani, A.K., Mundra, A., Doss, R., Bhattacharya, S., Smart Innovation, Systems and Technologies, Singapore: Springer, 235: 633-641. https://doi.org/10.1007/978-981-16-2877-1_58 |

| [39] |

Merton RC (1992) Financial Innovation and Economic Performance. J Appl Corp Financ 4: 12-22. https://doi.org/10.1111/j.1745-6622.1992.tb00214.x doi: 10.1111/j.1745-6622.1992.tb00214.x

|

| [40] | National Bank of Ethiopia (2020) Annual report 2020-2021. Available from: https://nbe.gov.et/annual-report/. |

| [41] |

Rezende LA, Bansi AC, Alves MFR, et al., (2019) Take your time: Examining when green innovation affects financial performance in multinationals. J Clean Prod 233: 993-1003. https://doi.org/10.1016/j.jclepro.2019.06.135 doi: 10.1016/j.jclepro.2019.06.135

|

| [42] | Temam R (2018) The effect of financial innovation on financial performance of commercial banks in Ethiopia. Available from: http://etd.aau.edu.et/handle/123456789/13307 |

| [43] | Tiwari SK, Kumaraswamidhas LA, Garg N (2022) Comparison of SVM and ARIMA Model in Time-Series Forecasting of Ambient Noise Levels, In: Bansal, R.C., Agarwal, A., Jadoun, V.K., Lecture Notes in Electrical Engineering, Singapore: Springer, 766: 777-786. https://doi.org/10.1007/978-981-16-1476-7_69 |

| [44] | Wagner ED (2005) Enabling mobile learning. EDUCAUSE review 40: 41-42. |

| [45] | Walley N, Whitehead B (1994) It's not easy being green. Reader Bus Environ 36. |

| [46] |

Wanditra LC, Alamsyah IM, Rachmaputri G, et al., (2021) Forecasting total suspended solid using wavelet ARIMA model. AIP Conference Proceedings 2423. https://doi.org/10.1063/5.0075561 doi: 10.1063/5.0075561

|

| [47] |

Wang M, Li Y, Li J, et al., (2021) Green process innovation, green product innovation and its economic performance improvement paths: A survey and structural model. J Environ Manage 297. https://doi.org/10.1016/j.jenvman.2021.113282 doi: 10.1016/j.jenvman.2021.113282

|

| [48] |

Xie X, Huo J, Zou H (2019) Green process innovation, green product innovation, and corporate financial performance: A content analysis method. J Bus Res 101: 697-706. https://doi.org/10.1016/j.jbusres.2019.01.010 doi: 10.1016/j.jbusres.2019.01.010

|

| [49] |

Yang J, Luo P (2020) Review on international comparison of carbon financial market. Green Financ 2: 55-74. https://doi.org/10.3934/GF.2020004 doi: 10.3934/GF.2020004

|

| [50] |

Yusr MM, Salimon MG, Mokhtar SSM, et al., (2020) Green innovation performance! How to be achieved? A study applied on Malaysian manufacturing sector. Sustain Futures 2. https://doi.org/10.1016/j.sftr.2020.100040 doi: 10.1016/j.sftr.2020.100040

|

| [51] |

Zhang D, Rong Z, Ji Q (2019) Green innovation and firm performance: Evidence from listed companies in China. Resour Conserv Recy 144: 48-55. https://doi.org/10.1016/j.resconrec.2019.01.023 doi: 10.1016/j.resconrec.2019.01.023

|

Nar-04-02-006-s001.pdf Nar-04-02-006-s001.pdf |

|

Figures(7) / Tables(2)

Goshu Desalegn, Anita Tangl. Forecasting green financial innovation and its implications for financial performance in Ethiopian Financial Institutions: Evidence from ARIMA and ARDL model[J]. National Accounting Review, 2022, 4(2): 95-111. doi: 10.3934/NAR.2022006

DownLoad:

DownLoad: