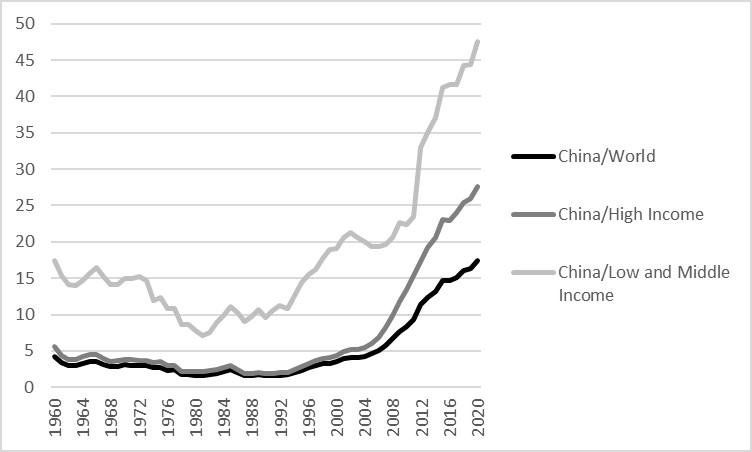

This article analyzes the influence of Chinese financial shocks on emerging and advanced economies using a GVAR (Global Vector Autoregressive) from 1985Q4 to 2016Q4. We summarize our findings in five points: i) adverse shocks in Chinese financial markets can cause a global recession; ii) these shocks trigger the "flight to quality", leading to the depreciation of domestic currencies to the U.S. dollar; iii) stock and exchange markets contribute to transmitting the shock to domestic economies; iv) commodity prices are sensitive to these shocks; v) the impact of the Chinese financial shock increased in the new millennium. Finally, the financial system of China has the potential to provoke worldwide macroeconomic fluctuations.

Citation: Luccas Assis Attílio. Impact of Chinese financial shocks: A GVAR approach[J]. National Accounting Review, 2024, 6(1): 27-49. doi: 10.3934/NAR.2024002

This article analyzes the influence of Chinese financial shocks on emerging and advanced economies using a GVAR (Global Vector Autoregressive) from 1985Q4 to 2016Q4. We summarize our findings in five points: i) adverse shocks in Chinese financial markets can cause a global recession; ii) these shocks trigger the "flight to quality", leading to the depreciation of domestic currencies to the U.S. dollar; iii) stock and exchange markets contribute to transmitting the shock to domestic economies; iv) commodity prices are sensitive to these shocks; v) the impact of the Chinese financial shock increased in the new millennium. Finally, the financial system of China has the potential to provoke worldwide macroeconomic fluctuations.

| [1] |

Adarov A (2022) Financial cycles around the world. Int J Finance Econ 27: 3163–3201. https://doi.org/10.1002/ijfe.2316 doi: 10.1002/ijfe.2316

|

| [2] |

Alzuabi R, Caglayan M, Mouratidis K (2021) The risk-taking channel in the United States: A GVAR approach. Int J Finance Econ 26: 5826–5849. https://doi.org/10.1002/ijfe.2096 doi: 10.1002/ijfe.2096

|

| [3] | Akhtaruzzaman M, Abdel-Qader W, Hammami H, et al. (2021) Is China a source of financial contagion? Finance Res Lett 38: 101393. https://doi.org/10.1016/j.frl.2019.101393 |

| [4] | Attílio LA, Faria JR, Rodrigues M (2023) Does monetary policy impact CO2 emissions? A GVAR analysis. Energy Econ 119: 106559. https://doi.org/10.1016/j.eneco.2023.106559 |

| [5] |

BenSaida A, Litimi H (2021) Financial contagion across G10 stock markets: A study during major crises. Int J Finance Econ 26: 4798–4821. https://doi.org/10.1002/ijfe.2041 doi: 10.1002/ijfe.2041

|

| [6] |

Bettendorf T (2019) Spillover effects of credit default risk in the euro area and the effects on the Euro: A GVAR approach. Int J Finance Econ 24: 296–312. https://doi.org/10.1002/ijfe.1663 doi: 10.1002/ijfe.1663

|

| [7] |

Bloom N, Draca M, Reenen VJ (2016) Trade Induced Technical Change? The Impact of Chinese Imports on Innovation, IT and Productivity. Rev Econ Stud 83: 87–117. https://doi.org/10.1093/restud/rdv039 doi: 10.1093/restud/rdv039

|

| [8] |

Çakir M, Kabundi A (2017) Transmission of China's Shocks to the BRIS Countries. S Afr J Econ 85: 430–454. https://doi.org/10.1111/saje.12164 doi: 10.1111/saje.12164

|

| [9] | Cesa-Bianchi A, Pesaran M, Rebucci A, et al. (2012) China's Emergence in the World Economy and Business Cycles in Latin America. Economía 12: 1–75. |

| [10] |

Cheung Y, Chinn M, Fujii E (2005) Dimensions of financial integration in greater China: Money markets, banks and policy effects. Int J Finance Econ 10: 117–132. https://doi.org/10.1002/ijfe.264 doi: 10.1002/ijfe.264

|

| [11] |

Chudik A, Fratzscher M (2011) Identifying the Global Transmission of the 2007–2009 Financial Crisis in a GVAR Model. Eur Econ Rev 55: 325–339. https://doi.org/10.1016/j.euroecorev.2010.12.003 doi: 10.1016/j.euroecorev.2010.12.003

|

| [12] |

Dees S, Mauro F, Pesaran M, et al. (2007) Exploring the international linkages of the Euro area: a global VAR analysis. J Appl Econ 22: 1–38. https://doi.org/10.1002/jae.932 doi: 10.1002/jae.932

|

| [13] |

Du J, Chen X, Gong J, et al. (2022) Analysis of stock markets risk spillover with copula models under the background of Chinese financial opening. Int J Finance Econ 28: 3997–401. https://doi.org/10.1002/ijfe.2632 doi: 10.1002/ijfe.2632

|

| [14] |

Eickmeier S, Ng T (2015) How do US credit supply shocks propagate internationally? A GVAR approach. Eur Econ Rev 74: 128–145. https://doi.org/10.1016/j.euroecorev.2014.11.011 doi: 10.1016/j.euroecorev.2014.11.011

|

| [15] |

Eickmeier S, Kuhnlenz M (2018) China's role in Global Inflation Dynamics. Macroeconomic Dyn 22: 225–254. https://doi.org/10.1017/S1365100516000158 doi: 10.1017/S1365100516000158

|

| [16] | Fareed F, Rezghi A, Sandoz C (2023) Inflation Dynamics in the Gulf Cooperation Council (GCC): What is the Role of External Factors? IMF Working Paper WP/23/263. |

| [17] |

Jenkins R, Peters E, Moreira M (2008) The Impact of China on Latin America and the Caribbean. World Dev 36: 235–253. https://doi.org/10.1016/j.worlddev.2007.06.012 doi: 10.1016/j.worlddev.2007.06.012

|

| [18] |

Jiang Y, Zheng L, Wang J (2021) Research on external financial risk measurement of China real estate. Int J Finance Econ 26: 5472–5484. https://doi.org/10.1002/ijfe.2075 doi: 10.1002/ijfe.2075

|

| [19] | Kim S (2001) International Transmission of U.S. Monetary Policy Shocks: Evidence from VAR's. J Monet Econ 48: 339–372. https://doi.org/10.1016/S0304-3932(01)00080-0 |

| [20] |

Liu Y, Li Z, Xu M (2020) The influential factors of financial cycle spillover: evidence from China. Emerg Mark Finance Trade 56: 1336–1350. https://doi.org/10.1080/1540496X.2019.1658076 doi: 10.1080/1540496X.2019.1658076

|

| [21] |

Ludvigson S, Ma S, Ng S (2021) Uncertainty and Business Cycles: Exogenous Impulse or Endogenous Response? Am Econ J Macroecon 13: 369–410. https://doi.org/10.1257/mac.20190171 doi: 10.1257/mac.20190171

|

| [22] |

Ma Y, Zhang J (2016) Financial cycle, business cycle and monetary policy: Evidence from four major economies. Int J Finance Econ 21: 502–527. https://doi.org/10.1002/ijfe.1566 doi: 10.1002/ijfe.1566

|

| [23] | Mauro F, Pesaran MH (2013) The GVAR handbook: Structure and applications of a macro model of the global economy for policy analysis, Oxford University Press. https://doi.org/10.1093/acprof:oso/9780199670086.001.0001 |

| [24] | Min F, Wen F, Xu J, et al. (2021) Credit supply, house prices, and financial stability. Int J Finance Econ 28: 2088–2108. https://doi.org/10.1002/ijfe.2527 |

| [25] | Mohaddes K, Raissi M (2020) Compilation, Revision and Updating of the Global VAR (GVAR) Database, 1979Q2–2016Q4, University of Cambridge: Faculty of Economics (mimeo). |

| [26] |

Ogawa E, Luo P (2022) Macroeconomic effects of global policy and financial risks. Int J Finance Econ 29: 177–205. https://doi.org/10.1002/ijfe.2681 doi: 10.1002/ijfe.2681

|

| [27] |

Pesaran MH, Schuermann T, Weiner S (2004) Modeling Regional Interdependencies Using a Global Error-Correcting Macroeconometric Model. J Bus Econ Stat 22: 129–162. https://doi.org/10.1198/073500104000000019 doi: 10.1198/073500104000000019

|

| [28] |

Shehzad K, Liu X, Tiwari A, et al. (2021) Analysing time difference and volatility linkages between China and the United States during financial crises and stable period using VARX-DCC-MEGARCH model. Int J Finance Econ 26: 814–833. https://doi.org/10.1002/ijfe.1822 doi: 10.1002/ijfe.1822

|

| [29] |

Wall DA, Eyden R (2016) The Impact of Economic Shocks in the Rest of the World on South Africa: Evidence from a Global VAR. Emerg Mark Finance Trade 52: 557–573. https://doi.org/10.1080/1540496X.2015.1103141 doi: 10.1080/1540496X.2015.1103141

|

| [30] | Wang Q, Zhang F (2021) What does the China's economic recovery after COVID-19 pandemic mean for the economic growth and energy consumption of other countries? J Clean Prod 295: 126265. https://doi.org/10.1016/j.jclepro.2021.126265 |

| [31] |

Wen F, Min F, Zhang Y, et al. (2019) Crude oil price shocks, monetary policy, and China's economy. Int J Finance Econ 24: 812–827. https://doi.org/10.1002/ijfe.1692 doi: 10.1002/ijfe.1692

|

| [32] |

Zhang Z, Zhang D, Wu F, et al. (2021) Systemic risk in the Chinese financial system: A copula-based network approach. Int J Finance Econ 26: 2044–2063. https://doi.org/10.1002/ijfe.1892 doi: 10.1002/ijfe.1892

|

NAR-06-01-002-S001.pdf NAR-06-01-002-S001.pdf |

|

Figures(14) / Tables(1)

Luccas Assis Attílio. Impact of Chinese financial shocks: A GVAR approach[J]. National Accounting Review, 2024, 6(1): 27-49. doi: 10.3934/NAR.2024002

DownLoad:

DownLoad: