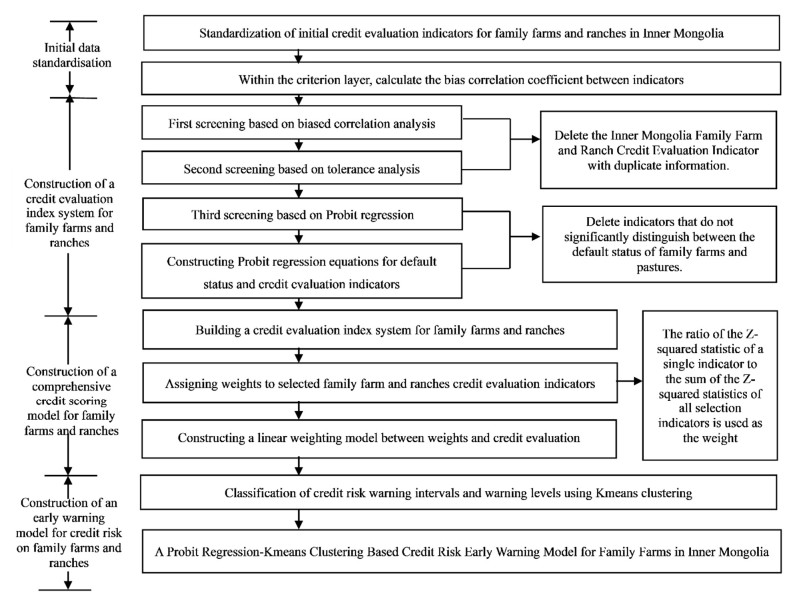

Early warning models credit risk play a crucial role in helping the financial institutions to reasonably predict the credit status of family farms and ranches. An attempt is made in this paper to construct a new credit risk early warning model based on Probit regression and Kmeans clustering algorithm, and testing the model by using data from 246 family farms in 12 leagues and cities in Inner Mongolia. First, the credit risk evaluation indicators of family farms and ranches were screened out through a three-combination model with partial correlation analysis, tolerance analysis and Probit regression. Second, the ratios of the Z-squared statistic of a single indicator to the sum of the Z-squared statistics of all the selected indicators were used to measure the weights of the credit evaluation indicators. Finally, four warning levels containing heavy alert level Ⅰ, medium alert level Ⅱ, light alert level Ⅲ and no alert level Ⅳ were classified by Kmeans clustering with large intra-cluster similarity and small inter-cluster similarity. The empirical evidence shows that the early warning model of credit risk for family farms and ranches is effective.

Citation: Zhanjiang Li, Yixiao Yuan, Tianning Sun, Pengfei Li. Early warning model of credit risk for family farms and ranches in Inner Mongolia based on Probit regression-Kmeans clustering[J]. Mathematical Biosciences and Engineering, 2023, 20(5): 8546-8560. doi: 10.3934/mbe.2023375

Early warning models credit risk play a crucial role in helping the financial institutions to reasonably predict the credit status of family farms and ranches. An attempt is made in this paper to construct a new credit risk early warning model based on Probit regression and Kmeans clustering algorithm, and testing the model by using data from 246 family farms in 12 leagues and cities in Inner Mongolia. First, the credit risk evaluation indicators of family farms and ranches were screened out through a three-combination model with partial correlation analysis, tolerance analysis and Probit regression. Second, the ratios of the Z-squared statistic of a single indicator to the sum of the Z-squared statistics of all the selected indicators were used to measure the weights of the credit evaluation indicators. Finally, four warning levels containing heavy alert level Ⅰ, medium alert level Ⅱ, light alert level Ⅲ and no alert level Ⅳ were classified by Kmeans clustering with large intra-cluster similarity and small inter-cluster similarity. The empirical evidence shows that the early warning model of credit risk for family farms and ranches is effective.

| [1] | Ministry of Agriculture and Rural Affairs of the People's Republic of China, Circular of the Ministry of Agriculture and Rural Affairs on the implementation of the action of upgrading new type of agricultural operating entities, 2022. Available from: http://www.moa.gov.cn/nybgb/2022/202204/202206/t20220607_6401742.htm. |

| [2] | H. Song, B. Shi, B. Wu, The new agricultural business entities: basic characteristics, financing needs and policy implication, Rural Econ., 10 (2020), 73–80. Available from: https://www.cnki.com.cn/Article/CJFDTOTAL-NCJJ202010010.htm. |

| [3] |

B. Shi, J. Wang, J. Qi, Y. Cheng, A novel imbalanced data classification approach based on Logistic regression and Fisher discriminant, Math. Probl. Eng., 2015 (2015), 945359. https://doi.org/10.1155/2015/945359 doi: 10.1155/2015/945359

|

| [4] |

Z. Li, L. Guo, Construction of credit evaluation index system for two-stage Bayesian discrimination: an empirical analysis of small Chinese enterprises, Math. Probl. Eng., 2021 (2021), 8837419. https://doi.org/10.1155/2021/8837419 doi: 10.1155/2021/8837419

|

| [5] |

Y. Lu, L. Yang, B. Shi, J. Li, M. Z. Abedin, A novel framework of credit risk feature selection for SMEs in Industry 4.0, Ann. Oper. Res., 2022 (2022), 1–28. https://doi.org/10.1007/s10479-022-04849-3 doi: 10.1007/s10479-022-04849-3

|

| [6] | S. Qian, Construction of financial credit risk evaluation system model based on analytic hierarchy process, in CSIA 2022: Cyber Security Intelligence and Analytics, (2022), 488–496. https://doi.org/10.1007/978-3-030-96908-0_61 |

| [7] |

Y. Sun, N. Chai, Y. Dong, B. Shi, Assessing and predicting small industrial enterprises' credit ratings: a fuzzy decision-making approach, Int. J. Forecasting, 38 (2022), 1158–1172. https://doi.org/10.1016/j.ijforecast.2022.01.006 doi: 10.1016/j.ijforecast.2022.01.006

|

| [8] |

N. Cai, B. Shi, Evaluating farmers' credit risk: a decision combination approach based on credit feature, Int. J. Financ. Eng., 9 (2022), 2250015. https://doi.org/10.1142/S2424786322500153 doi: 10.1142/S2424786322500153

|

| [9] |

Z. Li, Q. Zhang, Credit index screening model of family farms and family ranches based on fuzzy Bayesian theory of depth weighting, Complexity, 2022 (2022), 5381208. https://doi.org/10.1155/2022/5381208 doi: 10.1155/2022/5381208

|

| [10] | Y. Q. Cheng, Research on Evaluation and Decision of Small Amount Loans for Farmers Based on Support Vector Machines, MD. thesis, Dalian University of Technology, 2011. |

| [11] |

J. Cheng, X. Zhu, Research on performance validation of credit risk models, J. Shanxi Finance Econ. Univ., (2007), 86–92. https://doi.org/10.3969/j.issn.1007-9556.2007.02.016 doi: 10.3969/j.issn.1007-9556.2007.02.016

|

| [12] | D. Liu, Z. Li, X. Zheng, Selection model of credit index combination based on WOE-Probit stepwise regression and its application, Math. Pract. Theory, 48 (2018), 76–87. |

Figures(2) / Tables(8)

Zhanjiang Li, Yixiao Yuan, Tianning Sun, Pengfei Li. Early warning model of credit risk for family farms and ranches in Inner Mongolia based on Probit regression-Kmeans clustering[J]. Mathematical Biosciences and Engineering, 2023, 20(5): 8546-8560. doi: 10.3934/mbe.2023375

DownLoad:

DownLoad: