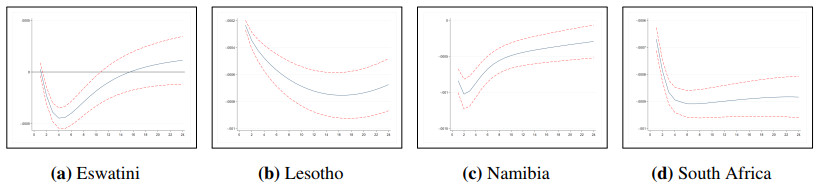

The Common Monetary Area (CMA) agreement has effectively granted the South African government sole discretion over monetary policy and implementation in the region. The effectiveness of this arrangement has long been under discussion given the heterogeneity of member countries. This paper uses a structural vector autoregressive (SVAR) to examine the efficacy of the interest rate channel in the CMA. Specifically, our analysis uses data from 2000M1-2018M12 to examine how economic output, inflation, money supply, domestic credit, and lending rate spread for each member country respond to shocks in the South African repo rate. The main findings indicate that a positive shock to the South African repo rate has a statistically significant negative impact on economic output and a positive effect on inflation at the 10 percent level for all countries in the CMA. The results also show that money supply, domestic credit, and lending rate spread respond asymmetrically across members countries.

Citation: Bonang N. Seoela. 2022: Efficacy of monetary policy in a currency union? Evidence from Southern Africa's Common Monetary Area, Quantitative Finance and Economics, 6(1): 35-53. doi: 10.3934/QFE.2022002

The Common Monetary Area (CMA) agreement has effectively granted the South African government sole discretion over monetary policy and implementation in the region. The effectiveness of this arrangement has long been under discussion given the heterogeneity of member countries. This paper uses a structural vector autoregressive (SVAR) to examine the efficacy of the interest rate channel in the CMA. Specifically, our analysis uses data from 2000M1-2018M12 to examine how economic output, inflation, money supply, domestic credit, and lending rate spread for each member country respond to shocks in the South African repo rate. The main findings indicate that a positive shock to the South African repo rate has a statistically significant negative impact on economic output and a positive effect on inflation at the 10 percent level for all countries in the CMA. The results also show that money supply, domestic credit, and lending rate spread respond asymmetrically across members countries.

| [1] |

Ajilore T, Ikhide S (2013) Monetary policy shocks, output and prices in South Africa: a test of policy irrelevance proposition. J Dev Areas 47: 363–386. https://doi.org/10.1353/jda.2013.0039 doi: 10.1353/jda.2013.0039

|

| [2] | Arestis P, Sawyer M (2003) Can Monetary Policy Affect The Real Economy? Levy Economics Institute https://doi.org/10.2139/ssrn.335620 |

| [3] |

Aron J, Muellbauer J (2007) Review of Monetary Policy in South Africa since 1994. J Afr Econ 16: 705–744. https://doi.org/10.1093/jae/ejm013 doi: 10.1093/jae/ejm013

|

| [4] | Aslanidi, O (2007) The Optimal Monetary Policy and the Channels of Monetary Transmission Mech511 anism in CIS-7 Countries: The Case of Georgia. Available from: https://www.cerge-ei.cz/pdf/wbrf_papers/O_Aslanidi_WBRF_Paper.pdf. |

| [5] |

Bernanke B, Gertler M (1995) Inside the Black Box: The Credit Channel of Monetary Policy Transmission. J Econ Perspect 9: 27–48. https://doi.org/10.1257/jep.9.4.27 doi: 10.1257/jep.9.4.27

|

| [6] |

Bernanke BS (1986) Alternative explanations of the money-income correlation. Carnegie-Rochester Confer Series on Public Policy 25: 49–99. https://doi.org/10.1016/0167-2231(86)90037-0 doi: 10.1016/0167-2231(86)90037-0

|

| [7] | Blanchard O, Watson M (1984) Are Business Cycles All Alike? Nat Bur Econ Res. https://doi.org/10.3386/w1392 |

| [8] |

Bonga-Bonga L (2010) Monetary Policy And Long-Term Interest Rates In South Africa. Int Bus Econ Res J 9: 43–54. https://doi.org/10.19030/iber.v9i10.638 doi: 10.19030/iber.v9i10.638

|

| [9] | Bonga-Bonga L, Kabundi A (2015) Monetary Policy Instrument and Inflation in South Africa: Structural Vector Error Correction Model Approach. Available from: https://mpra.ub.uni-muenchen.de/63731/. |

| [10] | Buigut S (2009) Monetary Policy Transmission Mechanism: Implications for the Proposed East African. Available from: https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.410.6867&rep=rep1&type=pdf. |

| [11] |

Can U, Bocuoglu ME, Can ZG (2020) How does the monetary transmission mechanism work? Evidence from Turkey. Borsa Istanb Rev 20: 375–382. https://doi.org/10.1016/j.bir.2020.05.004 doi: 10.1016/j.bir.2020.05.004

|

| [12] |

Cheng KC (2006) A VAR Analysis of Kenya's Monetary Policy Transmission Mechanism: How Does the Central Bank's REPO Rate Affect the Economy? IMF Working Paper 2006: 1–26. https://doi.org/10.5089/9781451865608.001 doi: 10.5089/9781451865608.001

|

| [13] |

Chow GC, Lin AL (1971) Best Linear Unbiased Interpolation, Distribution, and Extrapolation of Time Series by Related Series. Rev Econ Stat 53: 372–375. https://doi.org/10.2307/1928739 doi: 10.2307/1928739

|

| [14] | Corden WM (1972) Monetary Integration, Essays in International Finance. Princeton University. |

| [15] | Davoodi HR, Dixit S, Pinter G (2013) Monetary Transmission Mechanism in the East African Community: An Empirical Investigation. Available from: https://www.imf.org/en/publications. |

| [16] |

Denton FT (1971) Adjustment of Monthly or Quarterly Series to Annual Totals: An Approach Based on Quadratic Minimization. J Am Stat Assoc 66: 99–102. https://doi.org/10.1080/01621459.1971.10482227 doi: 10.1080/01621459.1971.10482227

|

| [17] | Dlamini B, Skosana S (2017) Relationship and Causality between Interest Rates and Macroeconomic Variables in Swaziland. Central Bank of Swaziland Research Bulletin 1: 4–25. |

| [18] |

Dodge D (2002) The interaction between monetary and fiscal policies. Can Public Pol 28: 187–202. https://doi.org/10.2307/3552324 doi: 10.2307/3552324

|

| [19] | Gumata N, Kabundi A, Ndou E (2013) Important channels of transmission monetary policy shock in South Africa. Econ Res Southern Africa. Available from: https://www.econrsa.org/system/files/publications. |

| [20] | Herrera AM, Pesavento E (2013) Unit Roots, Cointegration and Pre-Testing in VAR Models. Adv Econom 32: 81–115. |

| [21] | Ikhide S, Uanguta E (2010) Impact of South Africa's Monetary Policy on the LNS Economies. J Econ Integr 25: 324–352. |

| [22] |

Iwata S, Wu S (2006) Estimating monetary policy effects when interest rates are close to zero. J Monetary Econ 53: 1395–1408. https://doi.org/10.1016/j.jmoneco.2005.05.009 doi: 10.1016/j.jmoneco.2005.05.009

|

| [23] |

Kabundi A, Ngwenya N (2011) Assessing monetary policy in South Africa in a data-rich environment. South Afr J Econ 79: 91–107. https://doi.org/10.1111/j.1813-6982.2011.01265.x doi: 10.1111/j.1813-6982.2011.01265.x

|

| [24] | Karan A (2013) Quarterly Output Indicator Series for Fiji. Available from: https://citeseerx.ist.psu.edu/viewdoc/downloaddoi=10.1.1.1049.3224&rep=rep1&type=pdf. |

| [25] |

Kim S, Roubini N (2000) Exchange rate anomalies in the industrial countries: A solution with a structural VAR approach. J Monetary Econ 45: 561–586. https://doi.org/10.1016/S0304-3932(00)00010-6 doi: 10.1016/S0304-3932(00)00010-6

|

| [26] |

Kunroo MH (2016) Theory of Optimum Currency Areas: A Literature Survey. Rev Mark Integr 7: 87–116. https://doi.org/10.1177/0974929216631381 doi: 10.1177/0974929216631381

|

| [27] |

Leeper EM, Sims CA, Zha T (1996) What Does Monetary Policy Do? Brookings Papers on Economic Activity 1996: 1–78. https://doi.org/10.2307/2534619 doi: 10.2307/2534619

|

| [28] |

Litterman RB (1983) A Random Walk, Markov Model for the Distribution of Time Series. J Bus Econ Stat 1: 169–173. https://doi.org/10.1177/0974929216631381 doi: 10.1177/0974929216631381

|

| [29] | Loayza N, Schmidt-Hebbel K (2002) Monetary Policy Functions and Transmission Mechanisms: An Overview. Monetary policy: Rules and transmission mechanisms 1: 1–20. |

| [30] | Lütkepohl H, Krätzig M (2004) Applied time series econometrics. Cambridge University Press. https://doi.org/10.1017/CBO9780511606885 |

| [31] | Maturu B, Ndirangu L (2010) Monetary Policy Transmission Mechanism in Kenya: A Bayesian Vector Auto-regression (BVAR) Approach. Available from: https://www.centralbank.go.ke/images/docs/Research/Discussion-Papers/monetarypolicytransmissionmechanismkenya.pdf. |

| [32] | Meyer D, De Jongh J, Van Wyngaard D (2018) An Assessment of the Effectiveness of Monetary Policy in South Africa. Acta Univ Danubius: Oeconomica 14: 281–295. https://doaj.org/article/37362829786d407bbf336c541d5fcb62 |

| [33] |

Mishkin F (1995) Symposium on the Monetary Transmission Mechanism. J Econ Perspect 9: 3–10. https://doi.org/10.1257/jep.9.4.3 doi: 10.1257/jep.9.4.3

|

| [34] | Mkhonta SF (2018) Discount Rate Differential Monetary Policy Decisions in the CMA and Portfolio Investment Assets: The Efficacy of Namibia and Swaziland Monetary Policy. Central Bank of Swaziland Research Bulletin 2: 16–23. |

| [35] | Mosikari TJ, Eita JH(2018) Estimating threshold level of inflation in Swaziland: inflation and growth. MPRA. Available from: https://mpra.ub.uni-muenchen.de/88728/. |

| [36] | Mundell RA (1973) Uncommon Arguments for Common Currencies. In Johnson H, Swoboda A, The economics of common currencies (collected works of harry johnson), 1 Eds., London: Routledge, 114–132. https://doi.org/10.4324/9780203427477 |

| [37] | Mundell RA (1961) The Theory of Optimum Currency Areas. Am Econ Rev 51: 657–665. https://www.jstor.org/stable/1812792 |

| [38] | Ncube M, Ndou E(2013) Effects of Monetary Policy on Output. In Ncube M, Ndou E, In the Monetary policy and the economy of South Africa, London: Palgrave Macmillan, 9–24. https://doi.org/10.1057/9781137334152 |

| [39] | Peersman G, Smets F (2001) The monetary transmission mechanism in the euro area: more 564 evidence from VAR analysis. http://dx.doi.org/10.2139/ssrn.356269 |

| [40] |

Rafiq MS, Mallick SK (2008) The effect of monetary policy on output in EMU3: A sign restriction approach. J Macroecon 30: 1756–1791. https://doi.org/10.1016/j.jmacro.2007.12.003 doi: 10.1016/j.jmacro.2007.12.003

|

| [41] |

Sax C, Steiner P (2013) Temporal Disaggregation of Time Series. R J 5: 80–87. https://doi.org/10.32614/RJ-2013-028 doi: 10.32614/RJ-2013-028

|

| [42] | Seleteng M (2016) Effects of South African Monetary Policy Implementation on the CMA: A Panel Vector Autoregression Approach. Economic Research Southern Africa, 1–30. |

| [43] | Seleteng M (2005) Inflation and Economic Growth: An estimate of an optimal level of inflation in Lesotho. Central Bank of Lesotho. |

| [44] |

Sheefeni JPS, Ocran MK (2012) Monetary policy transmission in Namibia: A review of the interest rate channel. J Stud in Econ Econom 36: 47–63. https://doi.org/10.1080/10800379.2012.12097243 doi: 10.1080/10800379.2012.12097243

|

| [45] |

Smets F, Wouters R (2003) An Estimated Stochastic Dynamic General Equilibrium Model of the Euro Area. J Eur Econ Assoc 1: 1123–1175. https://doi.org/10.1162/154247603770383415 doi: 10.1162/154247603770383415

|

| [46] |

Tavlas GS (2009) The benefits and costs of monetary union in Southern Africa: A critical survey of the literature. J Econ Surv 23: 1–43. https://doi.org/10.1111/j.1467-6419.2008.00555.x doi: 10.1111/j.1467-6419.2008.00555.x

|

| [47] |

Taylor JB (1995) The Monetary Transmission Mechanism: An Empirical Framework. J Econ Perspect 9: 11–26. https://doi.org/10.1257/jep.9.4.11 doi: 10.1257/jep.9.4.11

|

| [48] | Wang JY, Masha I, Shirono K, et al. (2007) The Common Monetary Area in Southern Africa: Shocks, Adjustment, and Policy Challenges. Available from: https://www.imf.org/en/publications. |

QFE-06-01-002-s001.pdf QFE-06-01-002-s001.pdf |

|

Figures(5)

Bonang N. Seoela. 2022: Efficacy of monetary policy in a currency union? Evidence from Southern Africa's Common Monetary Area, Quantitative Finance and Economics, 6(1): 35-53. doi: 10.3934/QFE.2022002

DownLoad:

DownLoad: