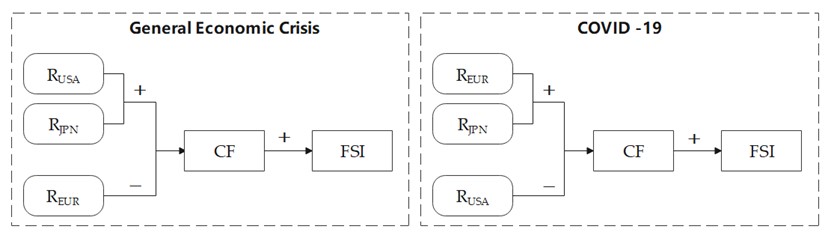

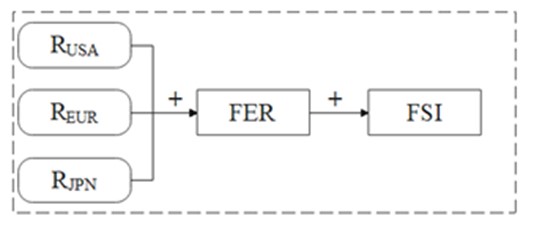

This study analyzes the impact of global financial integration and monetary policies from the United States, European Union and Japan on China's financial markets post-pandemic. Using TVP-FAVAR (Time-Varying Parameter Factor Augmented Vector Autoregression) and TVP-VAR-DY (Time-Varying Parameter Vector Autoregression DY) models, a Chinese financial market stress index was developed, showing that developed nations' monetary policies influence China's financial stress. The impact varies based on the economy's size and policy effectiveness. The spillovers occur mainly through accelerated short-term capital flows and foreign exchange reserve fluctuations. These effects have evolved over two decades, particularly noticeable during economic crises and the COVID-19 pandemic, highlighting the need for emerging economies, like China, to protect against international financial spillovers.

Citation: Cunyi Yang, Li Chen, Bin Mo. The spillover effect of international monetary policy on China's financial market[J]. Quantitative Finance and Economics, 2023, 7(4): 508-537. doi: 10.3934/QFE.2023026

This study analyzes the impact of global financial integration and monetary policies from the United States, European Union and Japan on China's financial markets post-pandemic. Using TVP-FAVAR (Time-Varying Parameter Factor Augmented Vector Autoregression) and TVP-VAR-DY (Time-Varying Parameter Vector Autoregression DY) models, a Chinese financial market stress index was developed, showing that developed nations' monetary policies influence China's financial stress. The impact varies based on the economy's size and policy effectiveness. The spillovers occur mainly through accelerated short-term capital flows and foreign exchange reserve fluctuations. These effects have evolved over two decades, particularly noticeable during economic crises and the COVID-19 pandemic, highlighting the need for emerging economies, like China, to protect against international financial spillovers.

| [1] |

Ahiadorme JW, Adenutsi DE (2023) Central bank policy formulation under COVID-19 in Ghana: A fit-for-purpose? J Econ Anal 2: 20. https://doi.org/10.58567/jea02010007 doi: 10.58567/jea02010007

|

| [2] |

Albality MS (2011) Impact of the Monetary Policy Instruments on Islamic Stock Market Index Return. Economics discussion paper. https://doi.org/10.2139/ssrn.1973469 doi: 10.2139/ssrn.1973469

|

| [3] |

Ammer J, Pooter M, Erceg C, et al. (2016) International Spillovers of Monetary Policy. IFDP Notes. https://doi.org/10.17016/2573-2129.15 doi: 10.17016/2573-2129.15

|

| [4] |

Antonakakis N, Gabauer D, Gupta R (2019) International Monetary Policy Spillovers: Evidence from a Time-Varying Parameter Vector Autoregression. Int Rev Financ Anal 65: 101382. https://doi.org/10.1016/j.irfa.2019.101382 doi: 10.1016/j.irfa.2019.101382

|

| [5] |

Beirne J, Fratzscher M (2012) The Pricing of Sovereign Risk and Contagion During the European Sovereign Debt Crisis. J Int Money Financ 34: 60–82. https://doi.org/10.1016/j.jimonfin.2012.11.004 doi: 10.1016/j.jimonfin.2012.11.004

|

| [6] |

Bekaert G, Hoerova M, Duca ML (2013) Risk, Uncertainty and Monetary Policy. J Monetary Econ 60: 771–788. https://doi.org/10.1016/j.jmoneco.2013.06.003 doi: 10.1016/j.jmoneco.2013.06.003

|

| [7] |

Belke A, Dubova I, Volz U (2018) Bond Yield Spillovers from Major Advanced Economies to Emerging Asia. Pacific Econ Rev 23: 109–126. https://doi.org/10.1111/1468-0106.12256 doi: 10.1111/1468-0106.12256

|

| [8] |

Benchimol J, Fourçans A (2017) Money and Monetary Policy in the Eurozone: An Empirical Analysis During Crises. Macroecon Dyn 21: 677–707. https://doi.org/10.1017/S1365100515000644 doi: 10.1017/S1365100515000644

|

| [9] |

Berger AN, Bouwman CH (2017) Bank Liquidity Creation, Monetary Policy, and Financial Crises. J Financ Stabil 30: 139–155. https://doi.org/10.1016/j.jfs.2017.05.001 doi: 10.1016/j.jfs.2017.05.001

|

| [10] |

Berisha E, Meszaros J, Olson E (2018) Income Inequality, Equities, Household Debt, and Interest Rates: Evidence from a Century of Data. J Int Money Financ 80: 1–14. https://doi.org/10.1016/j.jimonfin.2017.09.012 doi: 10.1016/j.jimonfin.2017.09.012

|

| [11] |

Bhar R, Malliaris A, Malliaris M (2015) The Impact of Large-Scale Asset Purchases on the S & P 500 Index, Long-Term Interest Rates and Unemployment. Appl Econ 47: 6010–6018. https://doi.org/10.1080/00036846.2015.1061646 doi: 10.1080/00036846.2015.1061646

|

| [12] |

Bouakez H, Eyquem A (2015) Government Spending, Monetary Policy, and the Real Exchange Rate. J Int Money Financ 56: 178–201. https://doi.org/10.1016/j.jimonfin.2014.09.010 doi: 10.1016/j.jimonfin.2014.09.010

|

| [13] |

Chandrasekhar CP, Ghosh J (2018) A Decade of Speculation. Econ Labour Relat Re 29: 410–427. https://doi.org/10.1177/1035304618812673 doi: 10.1177/1035304618812673

|

| [14] |

Chen L, Zhu J, Yang C (2022) Forecasting parameters in the SABR model. J Econ Anal 1:66-78. https://doi.org/10.58567/jea01010005 doi: 10.58567/jea01010005

|

| [15] |

Claus E, Claus I, Krippner L (2016) Monetary Policy Spillovers across the Pacific when Interest Rates Are at the Zero Lower Bound. Asian Econ Pap 15: 1–27. https://doi.org/10.1162/ASEP_a_00448 doi: 10.1162/ASEP_a_00448

|

| [16] |

Coeure B (2016) The Internationalisation of Monetary Policy. J Int Money Financ 67: 8–12. https://doi.org/10.1016/j.jimonfin.2015.06.007 doi: 10.1016/j.jimonfin.2015.06.007

|

| [17] |

Coibion O, Gorodnichenko Y, Kueng L, et al. (2017) Innocent Bystanders? Monetary Policy and Inequality. J Monetary Econ 88: 70–89. https://doi.org/10.1016/j.jmoneco.2017.05.005 doi: 10.1016/j.jmoneco.2017.05.005

|

| [18] |

Cook D, Devereux MB (2016) Exchange Rate Flexibility under the Zero Lower Bound. J Int Econ 101: 52–69. https://doi.org/10.1016/j.jinteco.2016.03.011 doi: 10.1016/j.jinteco.2016.03.011

|

| [19] |

Cronin D (2014) The Interaction between Money and Asset Markets: A Spillover Index Approach. J Macroecon 39: 185–202. https://doi.org/10.1016/j.jmacro.2013.09.006 doi: 10.1016/j.jmacro.2013.09.006

|

| [20] |

Devereux MB, Yetman J (2010) Leverage Constraints and the International Transmission of Shocks. J Money Credit Bank 42: 71–105. https://doi.org/10.1111/j.1538-4616.2010.00330.x doi: 10.1111/j.1538-4616.2010.00330.x

|

| [21] |

Diebold FX, Yilmaz K (2009) Measuring Financial Asset Return and Volatility Spillovers, with Application to Global Equity Markets. Econ J 119: 158–171. https://doi.org/10.1111/j.1468-0297.2008.02208.x doi: 10.1111/j.1468-0297.2008.02208.x

|

| [22] |

Diebold FX, Yilmaz K (2012) Better to Give Than to Receive: Predictive Directional Measurement of Volatility Spillovers. Int J Forecast 28: 57–66. https://doi.org/10.1016/j.ijforecast.2011.02.006 doi: 10.1016/j.ijforecast.2011.02.006

|

| [23] |

Diebold FX, Yilmaz K (2016) Trans-Atlantic Equity Volatility Connectedness: US and European Financial Institutions, 2004–2014. J Financ Econometrics 14: 81–127. https://doi.org/10.2139/ssrn.3680198 doi: 10.2139/ssrn.3680198

|

| [24] | Edwards S (2018) Finding Equilibrium: On the Relation between Exchange Rates and Monetary Policy. Comp Polit Econ: Monetary Policy eJournal. |

| [25] |

Eser F, Schwaab B (2016) Evaluating the Impact of Unconventional Monetary Policy Measures: Empirical Evidence from the ECB's Securities Markets Programme. J Financ Econ 119: 147–167. https://doi.org/10.1016/j.jfineco.2015.06.003 doi: 10.1016/j.jfineco.2015.06.003

|

| [26] |

Filho JRC, Neto A (2023) Is democracy affecting the economic policy responses to COVID-19? A cross-country analysis. Econ Anal Lett 3: 44. https://doi.org/10.58567/eal03010001 doi: 10.58567/eal03010001

|

| [27] |

Gai P, Kapadia S (2010) Contagion in Financial Networks. P Royal Soc A-Math Phy 466: 2401–2423. https://doi.org/10.1098/rspa.2009.0410 doi: 10.1098/rspa.2009.0410

|

| [28] |

Galariotis E, Makrichoriti P, Spyrou S (2018) The Impact of Conventional and Unconventional Monetary Policy on Expectations and Sentiment. J Bank Financ 86: 1–20. https://doi.org/10.1016/j.jbankfin.2017.08.014 doi: 10.1016/j.jbankfin.2017.08.014

|

| [29] |

Garcia-de-Andoain C, Kremer M (2017) Beyond Spreads: Measuring Sovereign Market Stress in the Euro Area. Econ Lett 159: 153–156. https://doi.org/10.1016/j.econlet.2017.06.042 doi: 10.1016/j.econlet.2017.06.042

|

| [30] |

Ge T (2019) Time-varying Transmission Efficiency of China's Monetary Policy. China Econ J 12: 32–51. https://doi.org/10.1080/17538963.2018.1556421 doi: 10.1080/17538963.2018.1556421

|

| [31] | Gul H, Mughal K, Rahim S (2012) Linkage between Monetary Instruments and Economic Growth. Univ J Manage Soc Sci 2: 69–76. |

| [32] |

Gupta R, Lau CK, Liu R, et al. (2018) Price Jumps in Developed Stock Markets: The Role of Monetary Policy Committee Meetings. J Econ Financ 43: 298–312. https://doi.org/10.1007/s12197-018-9444-z doi: 10.1007/s12197-018-9444-z

|

| [33] |

Hausman J, Wongswan J (2011) Global Asset Prices and FOMC Announcements. J Int Money Financ 30: 547–571. https://doi.org/10.1016/j.jimonfin.2011.01.008 doi: 10.1016/j.jimonfin.2011.01.008

|

| [34] |

He D, Wang H (2012) Dual-track Interest Rates and the Conduct of Monetary Policy in China. China Econ Rev 23: 928–947. https://doi.org/10.1016/j.chieco.2012.04.013 doi: 10.1016/j.chieco.2012.04.013

|

| [35] |

He Q, Leung PH, Chong TTL (2013) Factor-augmented VAR Analysis of the Monetary Policy in China. China Econ Rev 25: 88–104. https://doi.org/10.1016/j.chieco.2013.03.001 doi: 10.1016/j.chieco.2013.03.001

|

| [36] |

Koivu T (2009) Has the Chinese Economy Become More Sensitive to Interest Rates? Studying Credit Demand in China. China Econ Rev 20: 455–470. https://doi.org/10.1016/j.chieco.2008.03.001 doi: 10.1016/j.chieco.2008.03.001

|

| [37] |

Koop G, Korobilis D (2014) A New Index of Financial Conditions. Eur Econ Rev 71: 101–116. https://doi.org/10.1016/j.euroecorev.2014.07.002 doi: 10.1016/j.euroecorev.2014.07.002

|

| [38] |

Lee HC, Hsu CH, Chien CY (2016) Spillovers of International Interest Rate Swap Markets and Stock Market Volatility. Manag Financ 42: 943–962. https://doi.org/10.1108/MF-08-2015-0221 doi: 10.1108/MF-08-2015-0221

|

| [39] |

Lenza M, Pill H, Reichlin L (2010) Monetary Policy in Exceptional Times. Econ Policy 25: 295–339. https://doi.org/10.1111/j.1468-0327.2010.00240.x doi: 10.1111/j.1468-0327.2010.00240.x

|

| [40] |

Li B, Liu Q (2017) On the Choice of Monetary Policy Rules for China: A Bayesian DSGE Approach. China Econ Rev 44: 166–185. https://doi.org/10.1016/j.chieco.2017.04.004 doi: 10.1016/j.chieco.2017.04.004

|

| [41] |

Li J, Li Z, Liu M (2022) Bank competition, interest rate pass-through and the impact of the global financial crisis: evidence from Hong Kong and Macao. China Financ Rev Int 12: 646–666. https://doi.org/10.1108/CFRI-08-2021-0172 doi: 10.1108/CFRI-08-2021-0172

|

| [42] |

Li Z, Yang C, Huang Z (2022) How does the fintech sector react to signals from central bank digital currencies? Financ Res Lett 50: 103308. https://doi.org/10.1016/j.frl.2022.103308 doi: 10.1016/j.frl.2022.103308

|

| [43] |

Luciani M (2015) Monetary Policy and the Housing Market: A Structural Factor Analysis. J Appl Econometrics 30: 199–218. https://doi.org/10.1002/jae.2318 doi: 10.1002/jae.2318

|

| [44] | Maynard J (2016) General Theory of Employment, Interest, and Money. DESERT. |

| [45] |

Mehrotra AN (2007) Exchange and Interest Rate Channels During a Deflationary Era—Evidence from Japan, Hong Kong and China. J Comparative Econ 35: 188–210. https://doi.org/10.1016/j.jce.2006.10.004 doi: 10.1016/j.jce.2006.10.004

|

| [46] |

Meinusch A, Tillmann P (2016) The Macroeconomic Impact of Unconventional Monetary Policy Shocks. J Macroecon 47: 58–67. https://doi.org/10.1016/j.jmacro.2015.11.002 doi: 10.1016/j.jmacro.2015.11.002

|

| [47] |

Mendoza EG, Quadrini V, Rios-Rull JV (2009) Financial Integration, Financial Development, and Global Imbalances. J Polit Econ 117: 371–416. https://doi.org/10.1086/599706 doi: 10.1086/599706

|

| [48] | Nakajima J (2011) Time-Varying Parameter VAR Model with Stochastic Volatility: An Overview of Methodology and Empirical Applications. Monetary Econ Stud 29: 107–142. |

| [49] |

Nguyen L, Hoang D (2021). Ex-ante risk management and financial stability during the COVID-19 pandemic: a study of Vietnamese firms. China Financ Rev Int 11: 349–371. https://doi.org/10.1108/CFRI-12-2020-0177 doi: 10.1108/CFRI-12-2020-0177

|

| [50] |

Nsafoah D, Serletis A (2019) International Monetary Policy Spillovers. Open Econ Rev 30: 87–104. https://doi.org/10.1007/s11079-018-9505-0 doi: 10.1007/s11079-018-9505-0

|

| [51] |

Obstfeld M (2001) Mundell-Fleming Iecture - International Macroeconomics: Beyond the Mundell-Fleming Model. Imf Staff Papers 47: 1–39. https://doi.org/10.3386/w8369 doi: 10.3386/w8369

|

| [52] |

Ostry JD, Ghosh AR (2016) On the Obstacles to International Policy Coordination. J Int Money Financ 67: 25–40. https://doi.org/10.1016/j.jimonfin.2015.06.008 doi: 10.1016/j.jimonfin.2015.06.008

|

| [53] |

Pan WF, Wang X, Wu G, et al. (2021) The COVID-19 pandemic and sovereign credit risk. China Finance Review International 11: 287-301. https://doi.org/10.1108/CFRI-01-2021-0010 doi: 10.1108/CFRI-01-2021-0010

|

| [54] |

Rogers JH, Scotti C, Wright JH (2014) Evaluating Asset-Market Effects of Unconventional Monetary Policy: A Multi-Country Review. Econ Policy 29: 749–799. https://doi.org/10.1111/1468-0327.12042 doi: 10.1111/1468-0327.12042

|

| [55] |

Rousseau PL, Wachtel P (2011) What Is Happening to The Impact of Financial Deepening on Economic Growth? Econ Inquiry 49: 276–288. https://doi.org/10.1111/j.1465-7295.2009.00197.x doi: 10.1111/j.1465-7295.2009.00197.x

|

| [56] |

Seidl C (2023) Inflation: Thruway of ECB's Monetary Policy. J Econ Anal 2: 14. https://doi.org/10.58567/jea02010001 doi: 10.58567/jea02010001

|

| [57] |

Sims C (1980) Macroeconomis and Reality. Econometrica 48: 1–48. https://doi.org/10.2307/1912017 doi: 10.2307/1912017

|

| [58] |

Sowmya S, Prasanna K, Bhaduri S (2016) Linkages in the Term Structure of Interest Rates Across Sovereign Bond Markets. Emerg Mark Rev 27: 118–139. https://doi.org/10.1016/j.ememar.2016.05.001 doi: 10.1016/j.ememar.2016.05.001

|

| [59] | Taylor J (2013) International Monetary Policy Coordination: Past, Present and Future. SIEPR Discussion Paper No 12-0 3 4. |

| [60] |

Van Wincoop E (2013) International Contagion through Leveraged Financial Institutions. Am Econ J Macroecon 5: 152–189. https://doi.org/10.1257/mac.5.3.152 doi: 10.1257/mac.5.3.152

|

| [61] |

Wang S, Xu F, Chen S (2018) Constructing a Dynamic Financial Conditions Indexes by TVP-FAVAR Model. Appl Econ Lett 25: 183–186. https://doi.org/10.1080/13504851.2017.1307929 doi: 10.1080/13504851.2017.1307929

|

| [62] |

Wongswan J (2006) Transmission of Information Across International Equity Markets. Rev Financ Stud 19: 1157–1189. https://doi.org/10.1093/rfs/hhj033 doi: 10.1093/rfs/hhj033

|

| [63] |

Yang Z, Zhou Y (2017) Quantitative Easing and Volatility Spillovers Across Countries and Asset Classes. Manage Sci 63: 333–354. https://doi.org/10.1287/mnsc.2015.2305 doi: 10.1287/mnsc.2015.2305

|

| [64] | Zhang C (2012) Inflation, Economic Growth and Money Supply: A Return to Monetarism? J World Econ 8: 3–21. |

| [65] |

Zhang D, Hu M, Ji Q (2020) Financial Markets Under the Global Pandemic of COVID-19. Financ Res Lett 36: 101528. https://doi.org/10.1016/j.frl.2020.101528 doi: 10.1016/j.frl.2020.101528

|

| [66] |

Zhao Y, Zeng Y (2023) Optimal commissions and subscriptions in mutual aid platforms. ASTIN Bulletin: The Journal of the IAA 53: 658-83. https://doi.org/10.1017/asb.2023.21 doi: 10.1017/asb.2023.21

|

| [67] |

Zhu J, Yang C (2022) Analysis of Stock Market Information Leakage by RDD. Econ Anal Lett 1: 5. https://doi.org/10.58567/eal01010005 doi: 10.58567/eal01010005

|

Figures(18) / Tables(3)

Cunyi Yang, Li Chen, Bin Mo. The spillover effect of international monetary policy on China's financial market[J]. Quantitative Finance and Economics, 2023, 7(4): 508-537. doi: 10.3934/QFE.2023026

DownLoad:

DownLoad: