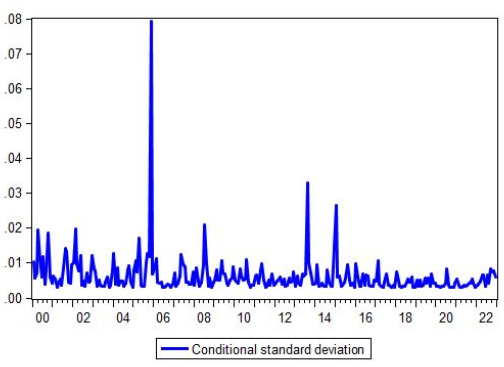

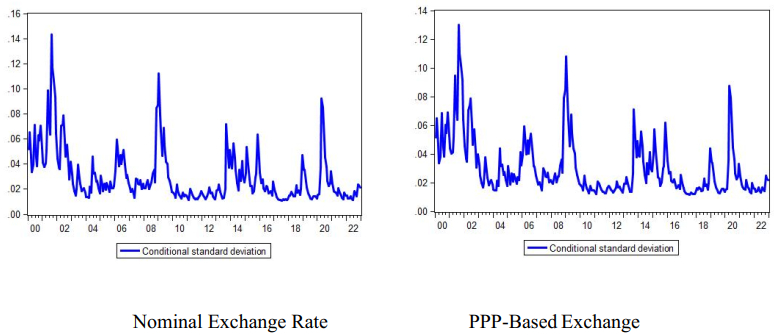

Low and stable inflation and exchange rates are the main objectives of inflation-targeting monetary policy. The internal and external stabilities are prerequisites for promoting economic growth. Using a two-stage GARCH, we investigated the effect of inflation instability and exchange rate unpredictability on the economic growth uncertainty in the case of Indonesia over the period 2000(1)– 2022(12). It was evident that both inflation instability and exchange rate unpredictability hurt output growth. The impact of inflation instability was higher than that of exchange rate unpredictability. While the output growth was higher in the post inflation-targeting regime adoption, the effect of real exchange rate instability was greater than that of nominal exchange rate unpredictability. Those findings suggested that the monetary authority should strengthen their commitment to achieve the inflation target range. The sharper focus on the inflation stability might avoid the monetary authority conducting twofold targets of inflation and exchange rate stability to stimulate economic growth.

Citation: Haryo Kuncoro, Fafurida Fafurida, Izaan Azyan Bin Abdul Jamil. Growth volatility in the inflation-targeting regime: Evidence from Indonesia[J]. Quantitative Finance and Economics, 2024, 8(2): 235-254. doi: 10.3934/QFE.2024009

Low and stable inflation and exchange rates are the main objectives of inflation-targeting monetary policy. The internal and external stabilities are prerequisites for promoting economic growth. Using a two-stage GARCH, we investigated the effect of inflation instability and exchange rate unpredictability on the economic growth uncertainty in the case of Indonesia over the period 2000(1)– 2022(12). It was evident that both inflation instability and exchange rate unpredictability hurt output growth. The impact of inflation instability was higher than that of exchange rate unpredictability. While the output growth was higher in the post inflation-targeting regime adoption, the effect of real exchange rate instability was greater than that of nominal exchange rate unpredictability. Those findings suggested that the monetary authority should strengthen their commitment to achieve the inflation target range. The sharper focus on the inflation stability might avoid the monetary authority conducting twofold targets of inflation and exchange rate stability to stimulate economic growth.

| [1] |

Abdurohman, Resosudarmo BP (2017) The behavior of fiscal policy in Indonesia in response to economic cycle. Sing Econ Rev 62: 377–401. https://doi.org/10.1142/S0217590816500041 doi: 10.1142/S0217590816500041

|

| [2] |

Adler G, Chang KS, Wang Z (2021) Patterns of foreign exchange intervention under inflation targeting. Latin Am J Central Bank 2: 1–25. https://doi.org/10.1016/j.latcb.2021.100045 doi: 10.1016/j.latcb.2021.100045

|

| [3] |

Alper AE (2017) Exchange rate volatility and trade flows. Fiscaoeconomia 1: 1–26. https://doi.org/10.25295/fsecon.307331 doi: 10.25295/fsecon.307331

|

| [4] |

Aman Q, Ullah I, Khan MI, et al. (2017) Linkages between exchange rate and economic growth in Pakistan, an econometric approach. Eur J Law Econ 44: 157–164. https://doi.org/10.1007/s10657-013-9395-y doi: 10.1007/s10657-013-9395-y

|

| [5] | Ambaw DT, Pundit M, Ramayandi A, et al. (2022) Real Exchange Rate Misalignment and Business Cycle Fluctuations in Asia and the Pacific, Working Paper Series, No. 651, March, ADB Economics. https://doi.org/10.22617/WPS220066-2 |

| [6] |

Baharumshah AZ, Slesman L, Wohar ME (2016) Inflation, inflation uncertainty, and economic growth in emerging and developing countries: panel data evidence. Econ Syst 40: 638–657. https://doi.org/10.1016/j.ecosys.2016.02.009 doi: 10.1016/j.ecosys.2016.02.009

|

| [7] |

Barguellil A, Salha OB, Zmami M (2018) Exchange rate volatility and economic growth. J Econ Integr 33: 1302–1336. http://dx.doi.org/10.11130/jei.2018.33.2.1302 doi: 10.11130/jei.2018.33.2.1302

|

| [8] | Barro R, Sala-i-Martin X (1995) Economic Growth, New York: McGraw-Hill. |

| [9] |

Benchimol J, El-Shagi M (2020) Forecast performance in times of terrorism. Econ Model 91: 386–402. https://doi.org/10.1016/j.econmod.2020.05.018 doi: 10.1016/j.econmod.2020.05.018

|

| [10] |

Benchimol J, Fourçans A (2019) Central bank losses and monetary policy rules: A DSGE investigation. Int Rev Econ Financ 61: 289–303. https://doi.org/10.1016/j.iref.2019.01.010 doi: 10.1016/j.iref.2019.01.010

|

| [11] |

Benchimol J, Caspi I, Kazinnik S (2023) Measuring communication quality of interest rate announcements. Econ Voice 20: 43–53. https://doi.org/10.1515/ev-2022-0023 doi: 10.1515/ev-2022-0023

|

| [12] |

Benchimol J, Caspi I, Levin Y (2022) The COVID-19 Inflation Weighting in Israel. Econ Voice 19: 5–14. https://doi.org/10.1515/ev-2021-0023 doi: 10.1515/ev-2021-0023

|

| [13] |

Benchimol J, Ivashchenko S (2021) Switching volatility in a nonlinear open economy. J Int Money Financ, 110. https://doi.org/10.1016/j.jimonfin.2020.102287 doi: 10.1016/j.jimonfin.2020.102287

|

| [14] |

Benchimol J, Saadon Y, Segev N (2023) Stock market reactions to monetary policy surprises under uncertainty. Int Rev Financ Anal 89: 102783. https://doi.org/10.1016/j.irfa.2023.102783 doi: 10.1016/j.irfa.2023.102783

|

| [15] |

Berganza JC, Broto C (2012) Flexible inflation targets, forex interventions, and exchange rate volatility in emerging countries. J Int Money Financ 31: 428–444. https://doi.org/10.1016/j.jimonfin.2011.12.002 doi: 10.1016/j.jimonfin.2011.12.002

|

| [16] |

Bhandari P, Frankel J (2017) Nominal GDP targeting for developing countries. Res Econ 71: 491–506. https://doi.org/10.1016/j.rie.2017.06.001 doi: 10.1016/j.rie.2017.06.001

|

| [17] |

Blanchard OJ, Simon JA (2001) The long and large decline in U.S. output volatility. Brookings Pap Econ Ac 32: 135–164. http://dx.doi.org/10.2139/ssrn.277356 doi: 10.2139/ssrn.277356

|

| [18] |

Bollerslev T (1986) Generalized autoregressive conditional heteroskedasticity. J Econometrics 31: 307–327. https://doi.org/10.1016/0304-4076(86)90063-1 doi: 10.1016/0304-4076(86)90063-1

|

| [19] |

Bostan I, Firtescu BN (2019) Exchange rate effects on international commercial trade competitiveness. J Risk Financ Manage 11: 19. https://doi.org/10.3390/jrfm11020019 doi: 10.3390/jrfm11020019

|

| [20] |

Cabral R, Carneiro FG, Mollick AV (2020) Inflation targeting and exchange rate volatility in emerging markets. Empir Econ 58: 605–626. https://doi.org/10.1007/s00181-018- 1478-8 doi: 10.1007/s00181-018-1478-8

|

| [21] |

Cerra V, Panizza U, Saxena S (2013) International evidence on recovery from recessions. Contemp Econ Policy 31: 424–439. https://doi.org/10.1111/j.1465-7287.2012.00313.x doi: 10.1111/j.1465-7287.2012.00313.x

|

| [22] | Chiṭu L, Quint D (2018) Emerging market vulnerabilities – a comparison with previous crises, ECB Econ Bull 8. |

| [23] | Dixit AK, Dixit RK, Pindyck RS (1994) Investment under Uncertainty, Princeton: Princeton University Press. https://doi.org/10.1515/9781400830176 |

| [24] |

Dotsey M, Sarte PD (2000) Inflation uncertainty and growth in a cash-in-advance economy. J Monetary Econ 45: 631–655. https://doi.org/10.1016/S0304-3932(00)00005-2 doi: 10.1016/S0304-3932(00)00005-2

|

| [25] | Ebeke C, Azangue AF (2015) Inflation Targeting and Exchange Rate Regimes in Emerging Markets, (Working Paper WP/15/228), IMF. https://doi.org/10.5089/9781513586267.001 |

| [26] |

Edwards S, Yeyati EL (2005) Flexible exchange rates as shock absorbers. Eur Econ Rev 49: 2079–2105. https://doi.org/10.1016/j.euroecorev.2004.07.002 doi: 10.1016/j.euroecorev.2004.07.002

|

| [27] |

Engle RF (1982) Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50: 987–1007. https://doi.org/10.2307/1912773 doi: 10.2307/1912773

|

| [28] | Fielding D (2008) Inflation Volatility and Economic Development: Evidence from Nigeria. (Economics Discussion Papers No. 0807). University of Otago. Available from: https://www.otago.ac.nz/data/assets/pdf_file/0035/327599/inflation-volatility-and-economic-development-evidence-from-nigeria-077111.pdf. |

| [29] |

Furceri D, Zdzienicka A (2011) The real effect of financial crises in the European transition economies. Econ Transit 19: 1–25. https://doi.org/10.1111/j.1468-0351.2010.00395.x doi: 10.1111/j.1468-0351.2010.00395.x

|

| [30] |

Glüzmann PA, Yeyati EL, Sturzenegger F (2012) Exchange rate undervaluation and economic growth: Díaz Alejandro (1965) revisited. Econ Lett 33: 666–672. https://doi.org/10.1016/j.econlet.2012.07.022 doi: 10.1016/j.econlet.2012.07.022

|

| [31] | Ha J, Kose MA, Ohnsorge F (2019) Inflation in Emerging Inflation in Emerging and Developing Economies and Developing Economies, Evolution, Drivers, and Policies, World Bank: Washington DC. https://doi.org/10.1596/1813-9450-8761 |

| [32] |

Habib M, Mileva E, Stracca L (2017) The real exchange rate and economic growth: revisiting the case using external instruments. J Int Money Financ 73: 386–398. https://doi.org/10.1016/j.jimonfin.2017.02.014 doi: 10.1016/j.jimonfin.2017.02.014

|

| [33] |

Insukindro I, Sahadewo GA (2010) Inflation dynamics in Indonesia: equilibrium correction and forward-looking Phillips curve approaches. Gadjah Mada Int J Bus 12: 117–133. https://doi.org/10.22146/gamaijb.5515 doi: 10.22146/gamaijb.5515

|

| [34] | Jamil M, Streissler EW, Kunst RM (2012) Exchange rate volatility and its impact on industrial production, before and after the introduction of common currency in Europe. Int J Econ Financ 2: 85–109. |

| [35] | Kumo WL (2015) Inflation Targeting Monetary Policy, Inflation Volatility and Economic Growth in South Africa. (Working Paper Series No. 216), African Development Bank. Available from: https://www.afdb.org/fileadmin/uploads/afdb/Documents/Publications/WPS_No_216_Inflation_Targeting_Monetary_Policy_Inflation_Volatility_and_Economic_Growth_in_South_Africa_B.pdf. |

| [36] | Kuncoro H (2015) Inflation targeting, exchange rate pass-through, and monetary policy rule in Indonesia. Int J Bus Econ Law 7: 14–25. |

| [37] |

Kuncoro H (2020) Interest rate policy and exchange rates volatility, lessons from Indonesia. J Central Bank Theory Pract 9: 19–42. https://doi.org/10.2478/jcbtp-2020-0012 doi: 10.2478/jcbtp-2020-0012

|

| [38] |

Kuncoro H, Fafuruda F (2023) Current account imbalances and exchange rate volatility: empirical evidence from Indonesia. Econ Horizons 25: 17–30. https://doi.org/10.5937/ekonhor2301019K doi: 10.5937/ekonhor2301019K

|

| [39] |

Kusumatrisna AL, Sugema I, Pasaribu SH (2022) Threshold effect in the relationship between inflation rate and economic growth in Indonesia. Bull Monetary Econ Bank 25: 117–132. https://doi.org/10.21098/bemp.v25i1.1045 doi: 10.21098/bemp.v25i1.1045

|

| [40] |

Mandeya SMT, Ho SY (2022) Inflation, inflation uncertainty, and the economic growth nexus: a review of the literature. Folia Oeconomica Stetinensia 22: 172–190. https://doi.org/10.2478/foli-2022-0009 doi: 10.2478/foli-2022-0009

|

| [41] |

Mohd SH, Baharumshah AZ, Fountas S (2013) Inflation, inflation uncertainty, and output growth: recent evidence from ASEAN-5 countries. Sing Econ Rev 58: 1–17. https://doi.org/10.1142/S0217590813500306 doi: 10.1142/S0217590813500306

|

| [42] |

Nene ST, Ilesanmi KD, Sekome M (2022) The effect of inflation targeting policy on the inflation uncertainty and economic growth in selected African and European countries. Economies 10: 1–16. https://doi.org/10.3390/economies10020037 doi: 10.3390/economies10020037

|

| [43] |

Nugroho MN, Ibrahim I, Winarno T, et al. (2014) The impact of capital reversal and the threshold of current account deficit on Rupiah. Bull Monetary Econ Bank 16: 205–230. https://doi.org/10.21098/bemp.v16i3.445 doi: 10.21098/bemp.v16i3.445

|

| [44] |

Peón SBG, Brindis MAR (2014) Analyzing the exchange rate pass-through in Mexico: evidence post inflation targeting implementation. Ensayos Sobre Política Económica 32: 18–35. https://doi.org/10.1016/S0120-4483(14)70025-9 doi: 10.1016/S0120-4483(14)70025-9

|

| [45] |

Rapetti M (2020) The real exchange rate and economic growth: a survey. J Globalization Dev 11: 2019–0024. https://doi.org/10.1515/jgd-2019-0024 doi: 10.1515/jgd-2019-0024

|

| [46] |

Razzaque MA, Bidisha SH, Khondker BH (2017) Exchange rate and economic growth: an empirical assessment for Bangladesh. J South Asian Dev 12: 42–64. https://doi.org/10.1177/0973174117702712 doi: 10.1177/0973174117702712

|

| [47] |

Senadza B, Diaba DD (2018) Effect of exchange rate volatility on trade in sub-Saharan Africa. J African Trade 4: 20–36. https://doi.org/10.1016/j.joat.2017.12.002 doi: 10.1016/j.joat.2017.12.002

|

| [48] |

Schnabl G (2008) Exchange rate volatility and growth in small open economies at the EMU periphery. EcoN Syst 32: 70–91. https://doi.org/10.1016/j.ecosys.2007.06.006 doi: 10.1016/j.ecosys.2007.06.006

|

| [49] |

Stevanovic S, Milenkovic I, Paunovic S (2022) Effects of the implementation of the inflation targeting regime on economic growth. Econ Horizons 24: 297–311. https://doi.org/10.5937/ekonhor2203297S doi: 10.5937/ekonhor2203297S

|

| [50] |

Svensson LE (1999) Inflation targeting as a monetary policy rule. J Monetary Econ 43: 607–654. https://doi.org/10.1016/S0304-3932(99)00007-0 doi: 10.1016/S0304-3932(99)00007-0

|

| [51] |

Thanh SD (2015) Threshold effects of inflation on growth in the ASEAN-5 countries: a panel smooth transition regression approach. J Econ Financ Admin Sci 20: 41–48. https://doi.org/10.1016/j.jefas.2015.01.003 doi: 10.1016/j.jefas.2015.01.003

|

| [52] |

Utomo FGR, Saadah S (2022) Exchange rate volatility and economic growth: managed floating and free-floating regime. Jurnal Keuangan dan Perbankan 26: 173–183. https://doi.org/10.26905/jkdp.v26i1.5878 doi: 10.26905/jkdp.v26i1.5878

|

| [53] |

Zhao Y, Haan J, Scholtens B, et al. (2014) Leading indicators of currency crises: are they the same in different exchange rate regimes? Open Econ Rev 25: 937–957. https://doi.org/10.1007/s11079-014-9315-y doi: 10.1007/s11079-014-9315-y

|

Figures(2) / Tables(7)

Haryo Kuncoro, Fafurida Fafurida, Izaan Azyan Bin Abdul Jamil. Growth volatility in the inflation-targeting regime: Evidence from Indonesia[J]. Quantitative Finance and Economics, 2024, 8(2): 235-254. doi: 10.3934/QFE.2024009

DownLoad:

DownLoad: