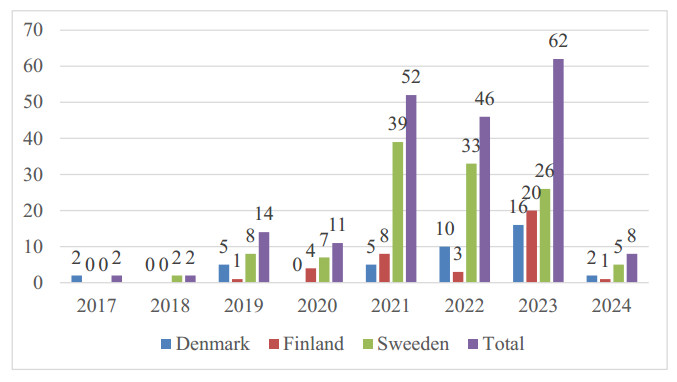

Green bond issues and markets are growing rapidly worldwide every year. Green bonds are used for financing environmentally friendly projects. Their issue is an important event in a company, with a huge impact not only on the protection of the environment but also on the management practice and financial performance of the company. This event is a signal to a stock market that is interpreted by shareholders differently: positively for eco-friendly investors and negatively for traditional investors, as it increases additional capital expenditures and financial risk. This paper aims to assess the short-term stock market reaction to the announcement of green bond issues in Nordic public companies and to determine whether the characteristics of green bond issues and issuers are significant determinants of stock cumulative abnormal return (CAR). The total sample was composed of 197 green bonds issued during 2017–2024. Sweden had the highest number of green bond issues (60.9%). Denmark and Finland had a very similar share, with 20.3% and 18.8%, respectively. The stock market reaction was assessed by applying an event study methodology. CAR dependence on the characteristics of green bond issues and issuers was determined using a heteroskedasticity-corrected regression model. The findings revealed a negative stock market reaction to the announcement of green bond issues. Such reaction may not only be due to increased capital expenditures and financial risk but also to the shift of investments from stocks to green bonds, as the majority of green bonds were issued during the COVID-19 pandemic and the Russian–Ukrainian war. We highlight that CAR is more sensitive to the characteristics of green bond issuers than those of issues.

Citation: Vilija Aleknevičienė, Raimonda Vilutytė. Short-term stock market reaction to the announcement of green bond issue: evidence from Nordic countries[J]. Green Finance, 2024, 6(4): 728-744. doi: 10.3934/GF.2024028

Green bond issues and markets are growing rapidly worldwide every year. Green bonds are used for financing environmentally friendly projects. Their issue is an important event in a company, with a huge impact not only on the protection of the environment but also on the management practice and financial performance of the company. This event is a signal to a stock market that is interpreted by shareholders differently: positively for eco-friendly investors and negatively for traditional investors, as it increases additional capital expenditures and financial risk. This paper aims to assess the short-term stock market reaction to the announcement of green bond issues in Nordic public companies and to determine whether the characteristics of green bond issues and issuers are significant determinants of stock cumulative abnormal return (CAR). The total sample was composed of 197 green bonds issued during 2017–2024. Sweden had the highest number of green bond issues (60.9%). Denmark and Finland had a very similar share, with 20.3% and 18.8%, respectively. The stock market reaction was assessed by applying an event study methodology. CAR dependence on the characteristics of green bond issues and issuers was determined using a heteroskedasticity-corrected regression model. The findings revealed a negative stock market reaction to the announcement of green bond issues. Such reaction may not only be due to increased capital expenditures and financial risk but also to the shift of investments from stocks to green bonds, as the majority of green bonds were issued during the COVID-19 pandemic and the Russian–Ukrainian war. We highlight that CAR is more sensitive to the characteristics of green bond issuers than those of issues.

| [1] |

Aleknevičienė V, Stralkutė S (2023) Impact of corporate social responsibility on cost of debt in Scandinavian public companies. Oecon Copern 14: 585–608. https://doi.org/10.24136/oc.2023.016 doi: 10.24136/oc.2023.016

|

| [2] |

Ammann M, Fehr M, Seiz R (2006) New evidence on the announcement effect of convertible and exchangeable bonds. J Multin Financ Manage 16: 43–63. https://doi.org/10.1016/j.mulfin.2005.03.001 doi: 10.1016/j.mulfin.2005.03.001

|

| [3] |

Baulkaran V (2019) Stock market reaction to green bond issuance. J Asset Manage 20: 331–340. https://doi.org/10.1057/s41260-018-00105-1 doi: 10.1057/s41260-018-00105-1

|

| [4] |

Björkholm L, Lehner OM (2021) Nordic green bond issuers' views on the upcoming EU Green Bond Standard. ACRN J Financ Risk Perspect 10: 222–279. https://doi.org/10.35944/jofrp.2021.10.1.012 doi: 10.35944/jofrp.2021.10.1.012

|

| [5] |

Cioli V, Colonna LA, Giannozzi A, et al. (2021) Corporate green bond and stock price reaction. Int J Bus Manage 16: 75–84. https://doi.org/10.5539/ijbm.v16n4p75 doi: 10.5539/ijbm.v16n4p75

|

| [6] |

Deschryver P, De Mariz F (2020) What future for the green bond market? How can policymakers, companies, and investors unlock the potential of the green bond market? J Risk Financ Manage 13: 61. https://doi.org/10.3390/jrfm13030061 doi: 10.3390/jrfm13030061

|

| [7] |

Fan R, Xiong X, Li Y, et al. (2023) Do green bonds affect stock returns and corporate environmental performance? Evidence from China. Econ Lett 232: 111322. https://doi.org/10.1016/j.econlet.2023.111322 doi: 10.1016/j.econlet.2023.111322

|

| [8] |

Fatica S, Panzica R, Rancan M (2021) The pricing of green bonds: are financial institutions special? J Financ Stab 54: 100873. https://doi.org/10.1002/bse.2771 doi: 10.1002/bse.2771

|

| [9] |

Flammer C (2021) Corporate green bonds. J Financ Econ 142: 499–516. https://doi.org/10.1016/j.jfineco.2021.01.010 doi: 10.1016/j.jfineco.2021.01.010

|

| [10] |

Friede G, Busch T, Bassen A (2015) ESG and financial performance: aggregated evidence from more than 2000 empirical studies. J Sustaint Financ Invest 5: 210–233. https://doi.org/10.1080/20430795.2015.1118917 doi: 10.1080/20430795.2015.1118917

|

| [11] |

Gyamerah SA, Asare C (2024) A critical review of the impact of uncertainties on green bonds. Green Financ 6: 78–91. https://doi.org/10.3934/GF.2024004 doi: 10.3934/GF.2024004

|

| [12] | Ul Haq I, Doumbia, D (2022) Structural loopholes in sustainability-linked bonds. World Bank Policy Research Working Paper Series. |

| [13] | Hemmingson C, Ydenius R (2017) The Convertible Bond Announcement Effect-An Event Study on the Nordic Markets. Available from: https://lup.lub.lu.se/luur/download?func=downloadFile&recordOId=8911937&fileOId=8911940. |

| [14] |

Hildingsson R, Kronsell A, Khan J (2019) The green state and industrial decarbonisation. Environ Politics 28: 909–928. https://doi.org/10.1080/09644016.2018.1488484 doi: 10.1080/09644016.2018.1488484

|

| [15] |

Jin J, Zhang J (2023) The stock performance of green bond issuers during COVID-19 pandemic: The case of China. Asia-Pacific Financ Mark 30: 211–230. https://doi.org/10.1007/s10690-022-09386-4 doi: 10.1007/s10690-022-09386-4

|

| [16] |

Khan J, Johansson B, Hildingsson R (2021). Strategies for greening the economy in three Nordic countries. Environ Policy Govern 31: 592–604. https://doi.org/10.1002/eet.1967 doi: 10.1002/eet.1967

|

| [17] | Kuchin I, Baranovsky G, Dranev Y, et al. (2019) Does green bonds placement create value for firms? Higher school of economics research paper No. WP BRP, 101. Available from: https://wp.hse.ru/data/2019/10/30/1532092144/101STI2019.pdf. |

| [18] |

Laborda J, Sánchez-Guerra Á (2021) Green bond finance in Europe and the stock market reaction. Stud Appl Econ 39: 1–22. https://doi.org/10.25115/eea.v39i3.4125 doi: 10.25115/eea.v39i3.4125

|

| [19] |

Lebelle M, Lajili Jarjir S, Sassi S (2020) Corporate green bond issuances: An international evidence. J Risk Financ Manage 13: 25. https://doi.org/10.3390/jrfm13020025 doi: 10.3390/jrfm13020025

|

| [20] |

Mitchell J, Sigurjonsson TO, Kavadis N, et al. (2024) Green bonds and sustainable business models in Nordic energy companies. Cur Res Environ Sustain 7: 100240. https://doi.org/10.1016/j.crsust.2023.100240 doi: 10.1016/j.crsust.2023.100240

|

| [21] |

Possebon EAG, Cippiciani FA, Savoia JRF, et al. (2024) ESG Scores and Performance in Brazilian Public Companies. Sustainability 16: 5650. https://doi.org/10.3390/su16135650 doi: 10.3390/su16135650

|

| [22] |

Roslen SNM, Yee LS, Ibrahim SAB (2017) Green Bond and shareholders' wealth: a multi-country event study. Int J Glob Small Bus 9: 61–69. https://doi.org/10.1504/IJGSB.2017.084701 doi: 10.1504/IJGSB.2017.084701

|

| [23] |

Tang DY, Zhang Y (2020) Do shareholders benefit from green bonds? J Corpor Financ 61: 101427. https://doi.org/10.1016/j.jcorpfin.2018.12.001 doi: 10.1016/j.jcorpfin.2018.12.001

|

| [24] |

Verma RK, Bansal R (2023) Stock market reaction on green-bond issue: Evidence from Indian green-bond issuers. Vision 27: 264–272. https://doi.org/10.1177/09722629211022523 doi: 10.1177/09722629211022523

|

| [25] |

Wang J, Chen X, Li X, et al. (2020) The market reaction to green bond issuance: Evidence from China. Pacific-Basin Financ J 60: 101294. https://doi.org/10.1016/j.pacfin.2020.101294 doi: 10.1016/j.pacfin.2020.101294

|

| [26] |

Wang H, Jiang S (2023) Green bond issuance and stock price informativeness. Econ Anal Policy 79: 120–133. https://doi.org/10.1016/j.eap.2023.06.011 doi: 10.1016/j.eap.2023.06.011

|

| [27] |

Zhang Y, Li Y, Chen X (2024) Does green bond issuance affect stock price crash risk? Evidence from China. Financ Res Lett 60: 104908. https://doi.org/10.1016/j.frl.2023.104908 doi: 10.1016/j.frl.2023.104908

|

| [28] |

Zhou X, Cui Y (2019) Green bonds, corporate performance, and corporate social responsibility. Sustainability 11: 6881. https://doi.org/10.3390/su11236881 doi: 10.3390/su11236881

|

Figures(1) / Tables(5)

Vilija Aleknevičienė, Raimonda Vilutytė. Short-term stock market reaction to the announcement of green bond issue: evidence from Nordic countries[J]. Green Finance, 2024, 6(4): 728-744. doi: 10.3934/GF.2024028

DownLoad:

DownLoad: