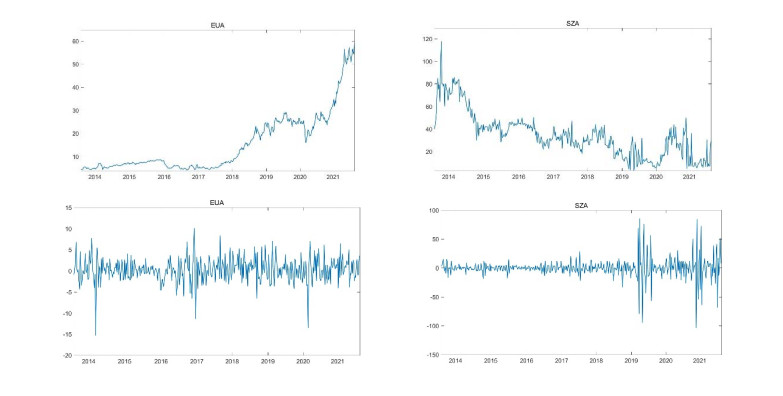

This study explores the dynamic relationship between the European carbon emission price (EUA) and the Shenzhen carbon emission price (SZA) in the time and frequency domain. Since they represent major carbon emission rights prices in the markets, they show a close correlation and tail correlation between them. Given the current global implementation to reduce carbon economy and China's implementation of a dual-carbon policy, it is of great value to explore the dynamic relationship between the two major carbon markets. Firstly, this paper uses a wavelet method to decompose the returned sequence into different frequency components to certify the dependent construction under different time scales. Secondly, this paper uses a wide range of static and time-varying link functions to describe the tail-dependent. The empirical results show that under different time scales, the dependence construction between EUA and SZA has significant time variation. The results of this study have important policy implications for understanding the transmission of carbon prices between different markets, as well as for investors and policy makers.

Citation: Juan Meng, Sisi Hu, Bin Mo. Dynamic tail dependence on China's carbon market and EU carbon market[J]. Data Science in Finance and Economics, 2021, 1(4): 393-407. doi: 10.3934/DSFE.2021021

This study explores the dynamic relationship between the European carbon emission price (EUA) and the Shenzhen carbon emission price (SZA) in the time and frequency domain. Since they represent major carbon emission rights prices in the markets, they show a close correlation and tail correlation between them. Given the current global implementation to reduce carbon economy and China's implementation of a dual-carbon policy, it is of great value to explore the dynamic relationship between the two major carbon markets. Firstly, this paper uses a wavelet method to decompose the returned sequence into different frequency components to certify the dependent construction under different time scales. Secondly, this paper uses a wide range of static and time-varying link functions to describe the tail-dependent. The empirical results show that under different time scales, the dependence construction between EUA and SZA has significant time variation. The results of this study have important policy implications for understanding the transmission of carbon prices between different markets, as well as for investors and policy makers.

| [1] |

Abakah EJA, Tiwari AK, Alagidede IP, et al. (2021) Re-examination of risk-return dynamics in international equity markets and the role of policy uncertainty, geopolitical risk and VIX: Evidence using Markov-switching copulas. Financ Res Lett, 102535. doi: 10.1016/j.frl.2021.102535

|

| [2] |

Bollerslev T, Engle RF, Wooldridge JM (1988) A capital asset pricing model with time-varying covariances. J Polit Econ 96: 116-131. doi: 10.1086/261527

|

| [3] |

Boute A, Zhang H (2019) Fixing the emissions trading scheme: Carbon price stability in the EU and China. Eur Law J 25: 333-347. doi: 10.1111/eulj.12307

|

| [4] |

Chevallier J (2011) A model of carbon price interactions with macroeconomic and energy dynamics. Energy Econ 33: 1295-1312. doi: 10.1016/j.eneco.2011.07.012

|

| [5] |

Christoffersen P, Errunza V, Jacobs K, et al. (2012) Is the potential for international diversification disappearing? A dynamic copula approach. Rev Financ Stud 25: 3711-3751. doi: 10.1093/rfs/hhs104

|

| [6] |

Engle RF (1982) Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50: 987-1007. doi: 10.2307/1912773

|

| [7] |

Farouq IS, Sambo NU, Ahmad AU, et al. (2021) Does financial globalization uncertainty affect CO2 emissions? Empirical evidence from some selected SSA countries. Quant Financ Econ 5: 247-263. doi: 10.3934/QFE.2021011

|

| [8] |

Güngör A, Taştan H (2021) On macroeconomic determinants of co-movements among international stock markets: evidence from DCC-MIDAS approach. Quant Financ Econ 5: 19-39. doi: 10.3934/QFE.2021002

|

| [9] |

Hanif W, Hernandez JA, Mensi W, et al. (2021) Nonlinear dependence and connectedness between clean/renewable energy sector equity and European emission allowance prices. Energy Econ 101: 105409. doi: 10.1016/j.eneco.2021.105409

|

| [10] |

Jiang Y, Jiang C, Nie H, et al. (2019) The time-varying linkages between global oil market and China's commodity sectors: Evidence from DCC-GJR-GARCH analyses. Energy 166: 577-586. doi: 10.1016/j.energy.2018.10.116

|

| [11] |

Jiang Y, Lao J, Mo B, et al. (2018) Dynamic linkages among global oil market, agricultural raw material markets and metal markets: an application of wavelet and copula approaches. Phys A 508: 265-279. doi: 10.1016/j.physa.2018.05.092

|

| [12] |

Jiang Y, Nie H, Monginsidi JY (2017) Co-movement of ASEAN stock markets: New evidence from wavelet and VMD-based copula tests. Econ Model 64: 384-398. doi: 10.1016/j.econmod.2017.04.012

|

| [13] |

Jiang Y, Tian G, Mo B (2020) Spillover and quantile linkage between oil price shocks and stock returns: new evidence from G7 countries. Financ Innovation 6: 1-26. doi: 10.1186/s40854-020-00208-y

|

| [14] |

Koop G, Tole L (2013) Forecasting the European carbon market. J R Stat Soc Ser A 176: 723-741. doi: 10.1111/j.1467-985X.2012.01060.x

|

| [15] |

Kumar S, Tiwari AK, Raheem ID, et al. (2021) Time-varying dependence structure between oil and agricultural commodity markets: A dependence-switching CoVaR copula approach. Resour Policy 72: 102049. doi: 10.1016/j.resourpol.2021.102049

|

| [16] |

Li M, Duan M (2012) Exploring linkage opportunities for China's emissions trading system under the Paris targets——EU-China and Japan-Korea-China cases. Energy Econ 102: 105528. doi: 10.1016/j.eneco.2021.105528

|

| [17] |

Liu J, Tang S, Chang CP (2021) Spillover effect between carbon spot and futures market: evidence from EU ETS. Environ Sci Pollut Res 28: 15223-15235. doi: 10.1007/s11356-020-11653-8

|

| [18] |

Mabrouk AB (2020) Wavelet-based systematic risk estimation: application on GCC stock markets: the Saudi Arabia case. Quant Financ Econ 4: 542-595. doi: 10.3934/QFE.2020026

|

| [19] |

Ma Y, Wang J (2021) Time-varying spillovers and dependencies between iron ore, scrap steel, carbon emission, seaborne transportation, and China's steel stock prices. Resour Policy 74: 102254. doi: 10.1016/j.resourpol.2021.102254

|

| [20] |

Meng J, Nie H, Mo B, et al. (2020) Risk spillover effects from global crude oil market to China's commodity sectors. Energy 202: 117208. doi: 10.1016/j.energy.2020.117208

|

| [21] |

Muteba Mwamba JW, Mwambi SM (2021) Assessing Market Risk in BRICS and Oil Markets: An Application of Markov Switching and Vine Copula. Int J Financ Stud 9: 30. doi: 10.3390/ijfs9020030

|

| [22] |

Naeem MA, Bouri E, Costa MD, et al. (2021) Energy markets and green bonds: A tail dependence analysis with time-varying optimal copulas and portfolio implications. Resour Policy 74: 102418. doi: 10.1016/j.resourpol.2021.102418

|

| [23] | Nelsen RB (1991) Copulas and association. In Dall'Aglio G, Kotz S, Salinetti G, Advances in probability distributions with given marginals, Springer, Dordrecht, 51-74. |

| [24] |

Patton AJ (2006) Modelling asymmetric exchange rate dependence. Int Econ Rev 47: 527-556. doi: 10.1111/j.1468-2354.2006.00387.x

|

| [25] |

Sun G, Chen T, Wei Z, et al. (2016) A carbon price forecasting model based on variational mode decomposition and spiking neural networks. Energies 9: 54. doi: 10.3390/en9010054

|

| [26] |

Xu Y (2021) Risk spillover from energy market uncertainties to the Chinese carbon market. Pac-Basin Financ J 67: 101561. doi: 10.1016/j.pacfin.2021.101561

|

| [27] |

Yang J, Luo P (2020) Review on international comparison of carbon financial market. Green Financ 2: 55-74. doi: 10.3934/GF.2020004

|

| [28] |

Zeng S, Jia J, Su B, et al. (2021) The volatility spillover effect of the European Union (EU) carbon financial market. J Clean Prod 282: 124394. doi: 10.1016/j.jclepro.2020.124394

|

| [29] |

Zhang M, Liu Y, Su Y (2017) Comparison of carbon emission trading schemes in the European Union and China. Climate 5: 70. doi: 10.3390/cli5030070

|

| [30] |

Zhang YJ, Sun YF (2016) The dynamic volatility spillover between European carbon trading market and fossil energy market. J Clean Prod 112: 2654-2663. doi: 10.1016/j.jclepro.2015.09.118

|

| [31] |

Zhang YJ, Zhang KB (2018) The linkage of CO2 emissions for China, EU, and USA: evidence from the regional and sectoral analyses. Environ Sci Pollut Res 25: 20179-20192. doi: 10.1007/s11356-018-1965-7

|

| [32] |

Zhu B, Wang P, Chevallier J, et al. (2015) Carbon price analysis using empirical mode decomposition. Comput Econ 45: 195-206. doi: 10.1007/s10614-013-9417-4

|

Figures(4) / Tables(5)

Juan Meng, Sisi Hu, Bin Mo. Dynamic tail dependence on China's carbon market and EU carbon market[J]. Data Science in Finance and Economics, 2021, 1(4): 393-407. doi: 10.3934/DSFE.2021021

DownLoad:

DownLoad: