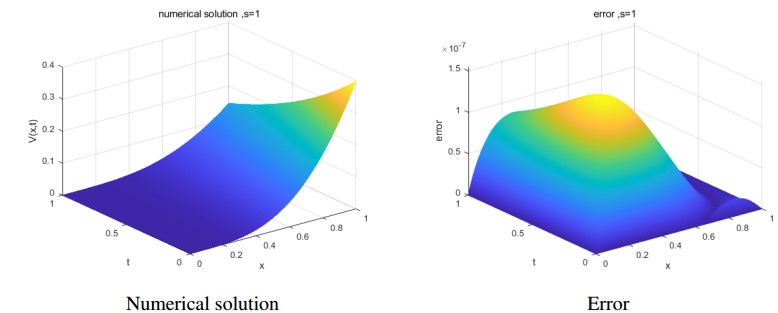

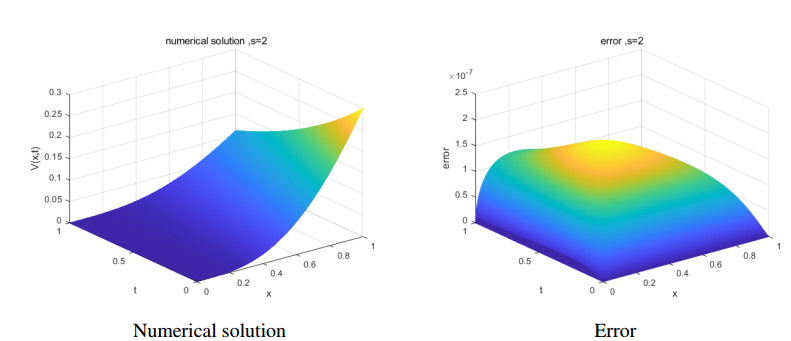

Fractional regime-switching option models have recently attracted much attention because they can capture the sudden state movement of the market, and deal with the non-stationary behavior. A second-order numerical scheme is proposed to solve the regime-switching option pricing models with fractional derivatives in space. The sufficient conditions of the stability and convergence of the proposed scheme are studied in details. An alternating direction implicit (ADI) method is implemented to accelerate the computation in every time layer. Numerical experiments are presented to verify the convergence and efficiency of the proposed method, compared with classical Krylov subspace solvers.

Citation: Ming-Kai Wang, Cheng Wang, Jun-Feng Yin. A second-order ADI method for pricing options under fractional regime-switching models[J]. Networks and Heterogeneous Media, 2023, 18(2): 647-663. doi: 10.3934/nhm.2023028

Fractional regime-switching option models have recently attracted much attention because they can capture the sudden state movement of the market, and deal with the non-stationary behavior. A second-order numerical scheme is proposed to solve the regime-switching option pricing models with fractional derivatives in space. The sufficient conditions of the stability and convergence of the proposed scheme are studied in details. An alternating direction implicit (ADI) method is implemented to accelerate the computation in every time layer. Numerical experiments are presented to verify the convergence and efficiency of the proposed method, compared with classical Krylov subspace solvers.

| [1] |

F. Black, M. Scholes, The pricing of options and corporate liabilities, J Polit Econ, 81 (1973), 637–654. https://doi.org/10.1086/260062 doi: 10.1086/260062

|

| [2] |

R. C. Merton, Option pricing when underlying stock returns are discontinuous, J Financ Econ, 3 (1976), 125–144. https://doi.org/10.1016/0304-405X(76)90022-2 doi: 10.1016/0304-405X(76)90022-2

|

| [3] |

Y. H. Kwon, Y. Lee, A second-order finite difference method for option pricing under jump-diffusion models, SIAM J Numer Anal, 49 (2011), 2598–2617. https://doi.org/10.1137/090777529 doi: 10.1137/090777529

|

| [4] | A. D. White, J. C. Hull, The pricing of options on assets with stochastic volatilities, J Finance, 42 (1987), 281–300. |

| [5] |

I. T. Koponen, Analytic approach to the problem of convergence of truncated Lévy flights towards the gaussian stochastic process, Phys. Rev. E, 52 (1995), 1197. https://doi.org/10.1103/PhysRevE.52.1197 doi: 10.1103/PhysRevE.52.1197

|

| [6] |

P. Carr, L. Wu, The finite moment log stable process and option pricing, J Finance, 58 (2003), 753–777. https://doi.org/10.1111/1540-6261.00544 doi: 10.1111/1540-6261.00544

|

| [7] |

P. Carr, H. Geman, D. B. Madan, M. Yor, Stochastic volatility for Lévy processes, Math Financ, 13 (2003), 345–382. https://doi.org/10.1111/1467-9965.00020. doi: 10.1111/1467-9965.00020

|

| [8] |

J. Buffington, R. J. Elliott, American options with regime switching, Int. J. Theor. Appl. Finance, 5 (2002), 497–514. https://doi.org/10.1142/S0219024902001523 doi: 10.1142/S0219024902001523

|

| [9] |

S. Heidari, H. Azari, A front-fixing finite element method for pricing American options under regime-switching jump-diffusion models, Comput. Appl. Math., 37 (2018), 3691–3707. https://doi.org/10.1007/s40314-017-0540-z doi: 10.1007/s40314-017-0540-z

|

| [10] |

R. J. Elliott, C. J. U. Osakwe, Option pricing for pure jump processes with Markov switching compensators, Finance Stoch., 10 (2006), 250–275. https://doi.org/10.1007/s00780-006-0004-6 doi: 10.1007/s00780-006-0004-6

|

| [11] |

X. T. Gan, J. F. Yin, Pricing American options under regime-switching model with a Crank-Nicolson fitted finite volume method, East Asian J Applied Math, 10 (2020), 499–519. https://10.4208/eajam.170919.221219 doi: 10.4208/eajam.170919.221219

|

| [12] |

X. Chen, D. Ding, S. L. Lei, W. F. Wang, An implicit-explicit preconditioned direct method for pricing options under regime-switching tempered fractional partial differential models, Numer Algorithms, 87 (2021), 939–965. https://doi.org/10.1007/s11075-020-00994-7 doi: 10.1007/s11075-020-00994-7

|

| [13] |

A. Cartea, D. del Castillo-Negrete, Fractional diffusion models of option prices in markets with jumps, Physica A, 374 (2007), 749–763. https://doi.org/10.1016/j.physa.2006.08.071 doi: 10.1016/j.physa.2006.08.071

|

| [14] |

S. L. Lei, W. F. Wang, X. Chen, D. Ding, A fast preconditioned penalty method for American options pricing under regime-switching tempered fractional diffusion models, J Sci Comput, 75 (2018), 1633–1655. https://doi.org/10.1007/s10915-017-0602-9 doi: 10.1007/s10915-017-0602-9

|

| [15] | P. Tankov, Financial modelling with jump processes, William Hall: CRC Press, 2003. |

| [16] | L. X. Zhang, R. F. Peng, J. F. Yin, A second order numerical scheme for fractional option pricing models, East Asian J Applied Math, 11 (2021), 326–348. https://10.4208/eajam.020820.121120 |

| [17] | I. Podlubny, Fractional Differential Equations: An Introduction to Fractional Derivatives, Fractional Differential Equations, to Methods of Their Solution and Some of Their Applications, London: Academic Press, 1999. |

| [18] |

M. M. Meerschaert, C. Tadjeran, Finite difference approximations for fractional advection–dispersion flow equations, J. Comput. Appl. Math., 172 (2004), 65–77. https://doi.org/10.1016/j.cam.2004.01.033 doi: 10.1016/j.cam.2004.01.033

|

| [19] |

W. Y. Tian, H. Zhou, W. H. Deng, A class of second order difference approximation for solving space fractional diffusion equations, Math. Comput., 84 (2012), 1703–1727. https://doi.org/10.1090/S0025-5718-2015-02917-2 doi: 10.1090/S0025-5718-2015-02917-2

|

| [20] | W. Chen, Numerical methods for fractional Black-Scholes equations and variational inequalities governing option pricing, Doctoral Thesis of University of Western Australia Perth, Australia, 2014. |

| [21] |

D. W. Peaceman, H. H. Rachford, The numerical solution of parabolic and elliptic differential equations, J Soc Ind Appl Math, 3 (1955), 28–41. https://doi.org/10.1137/0103003 doi: 10.1137/0103003

|

| [22] | H. M. Zhang, F. W. Liu, S. Z. Chen, M. Shen, A fast and high accuracy numerical simulation for a fractional Black-Scholes model on two assets, Ann Appl Math, 36 (2020), 91–110. |

| [23] |

W. Chen, S. Wang, A 2nd-order ADI finite difference method for a 2D fractional Black–Scholes equation governing European two asset option pricing, Math Comput Simul, 171 (2020), 279–293. https://doi.org/10.1016/j.matcom.2019.10.016 doi: 10.1016/j.matcom.2019.10.016

|

| [24] |

S. L. Lei, Y. C. Huang, Fast algorithms for high-order numerical methods for space-fractional diffusion equations, Int J Comput Math, 94 (2017), 1062–1078. https://doi.org/10.1080/00207160.2016.1149579 doi: 10.1080/00207160.2016.1149579

|

| [25] |

K. J. in 't Hout, J. Toivanen, Adi schemes for valuing european options under the bates model, Appl Numer Math, 130 (2018), 143–156. https://doi.org/10.1016/j.apnum.2018.04.003 doi: 10.1016/j.apnum.2018.04.003

|

| [26] |

L. Boen, K. J. in 't Hout, Operator splitting schemes for American options under the two-asset merton jump-diffusion model, Appl Numer Math, 153 (2020), 114–131. https://doi.org/10.1016/j.apnum.2020.02.004 doi: 10.1016/j.apnum.2020.02.004

|

| [27] |

M. K. Wang, C. Wang, J. F. Yin, A class of fourth-order Padé schemes for fractional exotic options pricing model, Electronic Research Archive, 30 (2022), 874–897, https://10.3934/era.2022046 doi: 10.3934/era.2022046

|

Figures(3) / Tables(5)

Ming-Kai Wang, Cheng Wang, Jun-Feng Yin. A second-order ADI method for pricing options under fractional regime-switching models[J]. Networks and Heterogeneous Media, 2023, 18(2): 647-663. doi: 10.3934/nhm.2023028

DownLoad:

DownLoad: