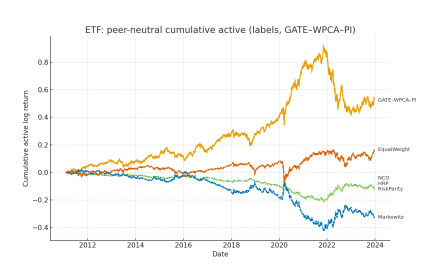

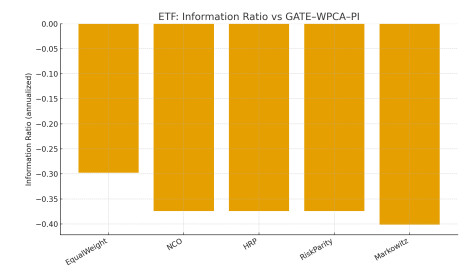

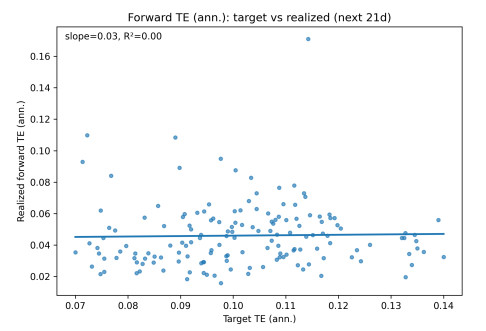

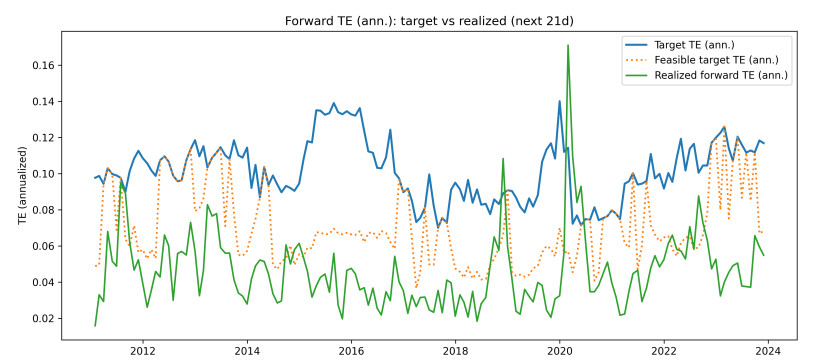

We introduced GATE-WPCA-PI—geometry-aware, tracking-error-controlled allocation with wavelet principle component analysis features and a proportional-integral controller—a practical portfolio construction framework that linked multi-scale market geometry to explicit, out-of-sample risk targeting. At each rebalance, the daily returns were embedded in a multi-resolution wavelet feature space and compressed via principal component analysis to form a similarity kernel. A simple discriminative-power score gated the optimizer: when the cross section was heterogeneous, the feature geometry was activated; when it was homogeneous, the method reverted to a correlation-only view. Allocations were obtained from an implementable mean–variance surrogate with (ⅰ) a geometry penalty that discouraged concentration in highly similar assets, (ⅱ) quadratic and absolute turnover costs, (ⅲ) an entropy floor, and (ⅳ) standard long-only, budget, and sleeve caps. A proportional-integral (PI) law treated the tracking error (TE) as a controllable state and steered realized TE toward a feasible band under trading frictions.

Citation: Muhammad Hilal Alkhudaydi, Yehya M. Althobaity. Graph aware adaptive tracking-error optimization with wavelet-principal component analysis features and proportional-integral control (GATE-WPCA-PI)[J]. AIMS Mathematics, 2026, 11(2): 3647-3702. doi: 10.3934/math.2026149

We introduced GATE-WPCA-PI—geometry-aware, tracking-error-controlled allocation with wavelet principle component analysis features and a proportional-integral controller—a practical portfolio construction framework that linked multi-scale market geometry to explicit, out-of-sample risk targeting. At each rebalance, the daily returns were embedded in a multi-resolution wavelet feature space and compressed via principal component analysis to form a similarity kernel. A simple discriminative-power score gated the optimizer: when the cross section was heterogeneous, the feature geometry was activated; when it was homogeneous, the method reverted to a correlation-only view. Allocations were obtained from an implementable mean–variance surrogate with (ⅰ) a geometry penalty that discouraged concentration in highly similar assets, (ⅱ) quadratic and absolute turnover costs, (ⅲ) an entropy floor, and (ⅳ) standard long-only, budget, and sleeve caps. A proportional-integral (PI) law treated the tracking error (TE) as a controllable state and steered realized TE toward a feasible band under trading frictions.

| [1] |

W. Lefebvre, G. Loeper, H. Pham, Mean-variance portfolio selection with tracking error penalization, Mathematics, 8 (2020), 1915. https://doi.org/10.3390/math8111915 doi: 10.3390/math8111915

|

| [2] |

G. De Nard, O. Ledoit, M. Wolf, Improved TE management for active and passive investing, J. Portfolio Manage., 51 (2024), 40–62. https://doi.org/10.3905/jpm.2024.1.665 doi: 10.3905/jpm.2024.1.665

|

| [3] |

M. Senneret, Y. Malevergne, P. Abry, G. Perrin, L. Jaffres, Covariance versus precision matrix estimation for efficient asset allocation, IEEE J.-STSP, 10 (2016), 982–993. https://doi.org/10.1109/JSTSP.2016.2577546 doi: 10.1109/JSTSP.2016.2577546

|

| [4] | Z. Zhao, O. Ledoit, H. Jiang, Risk reduction and efficiency increase in large portfolios: Leverage and shrinkage, University of Zurich, Department of Economics, Working Paper, 2019. https://doi.org/10.2139/ssrn.3421538 |

| [5] |

N. Amenc, F. Goltz, A. Lodh, L. Martellini, Diversifying the diversifiers and tracking the tracking error: Outperforming cap-weighted indices with limited risk of underperformance, J. Portfolio Manage., 38 (2012), 72–88. https://doi.org/10.3905/jpm.2012.38.3.072 doi: 10.3905/jpm.2012.38.3.072

|

| [6] |

P. Behr, A. Guettler, F. Miebs, On portfolio optimization: Imposing the right constraints, J. Bank. Financ., 37 (2013), 1232–1242. https://doi.org/10.1016/j.jbankfin.2012.11.020 doi: 10.1016/j.jbankfin.2012.11.020

|

| [7] |

C. Kirby, B. Ostdiek, It's all in the timing: Simple active portfolio strategies that outperform naive diversification, J. Financ. Quant. Anal., 47 (2012), 437–467. https://doi.org/10.1017/S0022109012000117 doi: 10.1017/S0022109012000117

|

| [8] |

W. Bessler, H. Opfer, D. Wolff, Multi-asset portfolio optimization and out-of-sample performance: An evaluation of Black–Litterman, mean-variance, and naïve diversification approaches, Eur. J. Financ., 23 (2017), 1–30. https://doi.org/10.1080/1351847X.2014.953699 doi: 10.1080/1351847X.2014.953699

|

| [9] | A. Ferramosca, D. Limon, I. Alvarado, T. Alamo, E. Camacho, MPC for tracking with optimal closed-loop performance, In: 2008 47th IEEE Conference on Decision and Control, IEEE, Mexico, 2008, 4055–4060. https://doi.org/10.1109/CDC.2008.4739089 |

| [10] | H. Tam, Minimum time closed-loop tracking of a specified path by robot, In: 29th IEEE Conference on Decision and Control, IEEE, USA, 1990, 3132–3137. https://doi.org/10.1109/CDC.1990.203368 |

| [11] |

S. Lam, On Lagrangian dynamics and its control formulations, Appl. Math. Comput., 91 (1998), 259–284. https://doi.org/10.1016/S0096-3003(97)10004-2 doi: 10.1016/S0096-3003(97)10004-2

|

| [12] | A. Alessandretti, A. P. Aguiar, C. N. Jones, Optimization based control for target estimation and tracking via highly observable trajectories: An application to motion control of autonomous robotic vehicles, Springer, Cham, 2015,495–504. https://doi.org/10.1007/978-3-319-10380-8_47 |

| [13] |

E. Sorensen, N. Alonso, D. Belanger, The use and misuse of tracking error, J. Portfolio Manage., 49 (2023), 12–23. https://doi.org/10.3905/jpm.2023.1.514 doi: 10.3905/jpm.2023.1.514

|

| [14] |

J. F. Hausner, G. van Vuuren, Portfolio performance under tracking error and benchmark volatility constraints, J. Econ. Financ. Adm. Sci., 26 (2021), 94–111. https://doi.org/10.1108/JEFAS-06-2019-0099 doi: 10.1108/JEFAS-06-2019-0099

|

| [15] |

O. Strub, P. Baumann, Optimal construction and rebalancing of index-tracking portfolios, Eur. J. Oper. Res., 264 (2018), 370–387. https://doi.org/10.1016/j.ejor.2017.06.055 doi: 10.1016/j.ejor.2017.06.055

|

| [16] |

N. C. P. Edirisinghe, Index-tracking optimal portfolio selection, Quant. Financ. Lett., 1 (2013), 16–20. https://doi.org/10.1080/21649502.2013.803789 doi: 10.1080/21649502.2013.803789

|

| [17] | H. E. Leland, Optimal asset rebalancing in the presence of transactions, 1997. |

| [18] | R. J. Martin, Optimal multifactor trading under proportional transaction costs, arXiv preprint, 2012. https://doi.org/10.48550/arXiv.1204.6488 |

| [19] | D. Bianchi, M. Bernardi, N. Bianco, Smoothing volatility targeting, SSRN Electron. J., 2022. |

| [20] |

M. Borkovec, I. Domowitz, B. Kiernan, V. Serbin, Portfolio optimization and the cost of trading, J. Invest., 19 (2010), 63–76. https://doi.org/10.3905/joi.2010.19.2.063 doi: 10.3905/joi.2010.19.2.063

|

| [21] |

N. Hautsch, S. Voigt, Large-scale portfolio allocation under transaction costs and model uncertainty, J. Econometrics, 212 (2019), 221–240. https://doi.org/10.1016/j.jeconom.2019.04.028 doi: 10.1016/j.jeconom.2019.04.028

|

| [22] |

R. Novy-Marx, M. Velikov, Comparing cost-mitigation techniques, Financ. Anal. J., 75 (2019), 85–102. https://doi.org/10.1080/0015198X.2018.1547057 doi: 10.1080/0015198X.2018.1547057

|

| [23] |

J. Ruf, K. Xie, The impact of proportional transaction costs on systematically generated portfolios, SIAM J. Financ. Math., 11 (2020), 881–896. https://doi.org/10.1137/19M1282313 doi: 10.1137/19M1282313

|

| [24] |

A. Kourtis, A stability approach to mean-variance optimization, Financ. Rev., 50 (2015), 301–330. https://doi.org/10.1111/fire.12068 doi: 10.1111/fire.12068

|

| [25] |

C. Han, F. C. Park, A geometric framework for covariance dynamics, J. Bank. Financ., 134 (2022), 106319. https://doi.org/10.1016/j.jbankfin.2021.106319 doi: 10.1016/j.jbankfin.2021.106319

|

| [26] |

M. L. Torrente, P. Uberti, Risk-adjusted geometric diversified portfolios, Qual. Quant., 58 (2023), 35–55. https://doi.org/10.1007/s11135-023-01631-w doi: 10.1007/s11135-023-01631-w

|

| [27] |

N. Koné, Regularized maximum diversification investment strategy, Econometrics, 9 (2021), 1. https://doi.org/10.3390/econometrics9010001 doi: 10.3390/econometrics9010001

|

| [28] |

F. A. Ibanez, Diversified spectral portfolios: An unsupervised learning approach to diversification, J. Financ. Data Sci., 5 (2023), 67–83. https://doi.org/10.3905/jfds.2023.1.118 doi: 10.3905/jfds.2023.1.118

|

| [29] |

T. Lim, C. S. Ong, Portfolio diversification using shape-based clustering, J. Financ. Data Sci., 3 (2020), 111–126. https://doi.org/10.3905/jfds.2020.1.054 doi: 10.3905/jfds.2020.1.054

|

| [30] |

M. F. C. Haddad, Sphere-sphere intersection for investment portfolio diversification—A new data-driven cluster analysis, MethodsX, 6 (2019), 1261–1278. https://doi.org/10.1016/j.mex.2019.05.025 doi: 10.1016/j.mex.2019.05.025

|

| [31] |

P. Jain, S. Jain, Can machine learning-based portfolios outperform traditional risk-based portfolios? The need to account for covariance misspecification, Risks, 7 (2019), 74. https://doi.org/10.3390/risks7030074 doi: 10.3390/risks7030074

|

| [32] | B. Himbert, J. Kapraun, M. Rudolf, A study of improved covariance matrix estimators for low and diversified volatility portfolio strategies, Working paper, 2018, 1–36. |

| [33] |

T. Raffinot, Hierarchical clustering-based asset allocation, J. Portfolio Manage., 44 (2017), 89–99. https://doi.org/10.3905/jpm.2018.44.2.089 doi: 10.3905/jpm.2018.44.2.089

|

| [34] | M. Mahrooghy, A. B. Ashraf, D. Daye, C. Mies, M. Feldman, M. Rosen, et al., Heterogeneity wavelet kinetics from DCE-MRI for classifying gene expression based breast cancer recurrence risk, Springer Berlin Heidelberg, 2013,295–302. |

| [35] |

M. Mahrooghy, A. B. Ashraf, D. Daye, E. S. McDonald, M. Rosen, C. Mies, et al., Pharmacokinetic tumor heterogeneity as a prognostic biomarker for classifying breast cancer recurrence risk, IEEE T. Bio.-Med. Eng., 62 (2015), 1585–1594. https://doi.org/10.1109/TBME.2015.2395812 doi: 10.1109/TBME.2015.2395812

|

| [36] |

J. W. Prescott, D. Zhang, J. Z. Wang, N. A. Mayr, W. T. Yuh, J. Saltz, et al., Temporal analysis of tumor heterogeneity and volume for cervical cancer treatment outcome prediction: preliminary evaluation, J. Digit. Imaging, 23 (2009), 342–357. https://doi.org/10.1007/s10278-009-9179-7 doi: 10.1007/s10278-009-9179-7

|

| [37] |

S. Kaewpijit, J. Le Moigne, T. El-Ghazawi, Automatic reduction of hyperspectral imagery using wavelet spectral analysis, IEEE T. Geosci. Remote, 41 (2003), 863–871. https://doi.org/10.1109/TGRS.2003.810712 doi: 10.1109/TGRS.2003.810712

|

| [38] |

D. Kwon, M. Vannucci, J. J. Song, J. Jeong, R. M. Pfeiffer, A novel waveletbased thresholding method for the preprocessing of mass spectrometry data that accounts for heterogeneous noise, Proteomics, 8 (2008), 3019–3029. https://doi.org/10.1002/pmic.200701010 doi: 10.1002/pmic.200701010

|

| [39] |

Y. Motai, N. A. Siddique, H. Yoshida, Heterogeneous data analysis: Online learning for medical-image-based diagnosis, Pattern Recogn., 63 (2017), 612–624. https://doi.org/10.1016/j.patcog.2016.09.035 doi: 10.1016/j.patcog.2016.09.035

|

| [40] | X. Shi, Q. Liu, W. Fan, P. S. Yu, R. Zhu, Transfer learning on heterogenous feature spaces via spectral transformation, In: 2010 IEEE International Conference on Data Mining, IEEE, 2010. https://doi.org/10.1109/ICDM.2010.65 |

| [41] |

E. M. Haghighi, S. Na, A multifeatured data-driven homogenization for heterogeneous elastic solids, Appl. Sci., 11 (2021), 9208. https://doi.org/10.3390/app11199208 doi: 10.3390/app11199208

|

| [42] |

T. W. Rauber, F. de A. Boldt, F. M. Varejao, Heterogeneous feature models and feature selection applied to bearing fault diagnosis, IEEE T. Ind. Elec., 62 (2015), 637–646. https://doi.org/10.1109/TIE.2014.2327589 doi: 10.1109/TIE.2014.2327589

|

| [43] |

C. Chu, A. L. Hsu, K. H. Chou, P. Bandettini, C. Lin, Does feature selection improve classification accuracy? Impact of sample size and feature selection on classification using anatomical magnetic resonance images, NeuroImage, 60 (2012), 59–70. https://doi.org/10.1016/j.neuroimage.2011.11.066 doi: 10.1016/j.neuroimage.2011.11.066

|

| [44] |

S. Giglio, Y. Liao, D. Xiu, Thousands of alpha tests, Rev. Financ. Stud., 34 (2018), 3456–3496. https://doi.org/10.1093/rfs/hhaa111 doi: 10.1093/rfs/hhaa111

|

| [45] |

A. Samaha, C.04.02 When the drugs stop working, Eur. Neuropsychopharm., 29 (2019), S620. https://doi.org/10.1016/j.euroneuro.2018.11.980 doi: 10.1016/j.euroneuro.2018.11.980

|

| [46] |

R. Sullivan, A. Timmermann, H. White, Data—snooping, technical trading rule performance, and the bootstrap, J. Finance, 54 (1999), 1647–1691. https://doi.org/10.1111/0022-1082.00163 doi: 10.1111/0022-1082.00163

|

| [47] |

A. W. Lo, A. C. MacKinlay, Data-snooping biases in tests of financial asset pricing models, Rev. Financ. Stud., 3 (1990), 431–467. https://doi.org/10.1093/rfs/3.3.431 doi: 10.1093/rfs/3.3.431

|

| [48] |

J. Conrad, M. Cooper, G. Kaul, Value versus Glamour, J. Finance, 58 (2003), 1969–1995. https://doi.org/10.1111/1540-6261.00594 doi: 10.1111/1540-6261.00594

|

| [49] |

R. Martin, K. Yu, Assessing performance of prediction rules in machine learning, Pharmacogenomics, 7 (2006), 543–550. https://doi.org/10.2217/14622416.7.4.543 doi: 10.2217/14622416.7.4.543

|

| [50] | C. L. Giles, S. Lawrence, Presenting and analyzing the results of AI experiments: Data averaging and data snooping, AAAI Press, California, 1997,362–367. |

| [51] |

B. Rossi, A. Inoue, Out-of-sample forecast tests robust to the choice of window size, J. Bus. Econ. Stat., 30 (2012), 432–453. https://doi.org/10.1080/07350015.2012.693850 doi: 10.1080/07350015.2012.693850

|

| [52] |

D. Berrar, I. Bradbury, W. Dubitzky, Avoiding model selection bias in small-sample genomic datasets, Bioinformatics, 22 (2006), 1245–1250. https://doi.org/10.1093/bioinformatics/btl407 doi: 10.1093/bioinformatics/btl407

|

| [53] |

D. G. Anghel, No pain, no gain: You should always incorporate trading costs for a bias-free evaluation of trading rule overperformance, Econ. Lett., 216 (2022), 110584. https://doi.org/10.1016/j.econlet.2022.110584 doi: 10.1016/j.econlet.2022.110584

|

| [54] |

P. R. Hansen, A test for superior predictive ability, J. Bus. Econ. Stat., 23 (2005), 365–380. https://doi.org/10.1198/073500105000000063 doi: 10.1198/073500105000000063

|

Figures(18) / Tables(31)

Muhammad Hilal Alkhudaydi, Yehya M. Althobaity. Graph aware adaptive tracking-error optimization with wavelet-principal component analysis features and proportional-integral control (GATE-WPCA-PI)[J]. AIMS Mathematics, 2026, 11(2): 3647-3702. doi: 10.3934/math.2026149

DownLoad:

DownLoad: