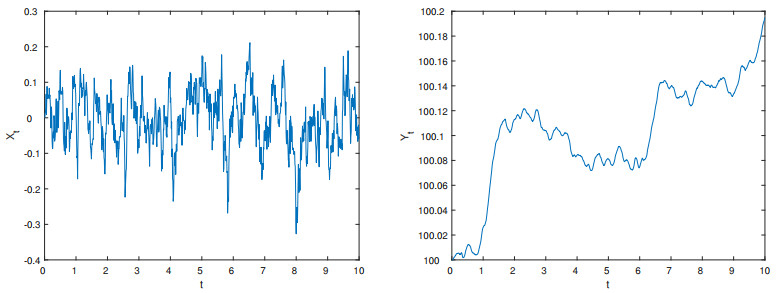

The integrals of diffusion processes are of significant importance in the field of finance, particularly in relation to stochastic volatility models, which are frequently employed to represent the temporal variability of stock prices. In this paper, we consider the strong consistency of the nonparametric kernel estimator of the transition density for second-order diffusion processes, using the moment inequalities of $ \rho $-mixing sequences to demonstrate the strong consistency under some regularity conditions. Furthermore, the asymptotic mean square error is provided based on the deviation and variance of the transition density kernel estimator. The optimal bandwidth is found and thus the convergence rate of the kernel estimator is obtained. At the same time, our results are compared with the conclusions of the univariate density function.

Citation: Yue Li, Yunyan Wang. Strong consistency of the nonparametric kernel estimator of the transition density for the second-order diffusion process[J]. AIMS Mathematics, 2024, 9(7): 19015-19030. doi: 10.3934/math.2024925

The integrals of diffusion processes are of significant importance in the field of finance, particularly in relation to stochastic volatility models, which are frequently employed to represent the temporal variability of stock prices. In this paper, we consider the strong consistency of the nonparametric kernel estimator of the transition density for second-order diffusion processes, using the moment inequalities of $ \rho $-mixing sequences to demonstrate the strong consistency under some regularity conditions. Furthermore, the asymptotic mean square error is provided based on the deviation and variance of the transition density kernel estimator. The optimal bandwidth is found and thus the convergence rate of the kernel estimator is obtained. At the same time, our results are compared with the conclusions of the univariate density function.

| [1] |

F. M. Bandi, P. C. B. Phillips, Fully nonparametric estimation of scalar diffusion models, Econometrica, 71 (2003), 241–283. https://doi.org/10.1111/1468-0262.00395 doi: 10.1111/1468-0262.00395

|

| [2] |

J. Fan, C. Zhang, A reexamination of diffusion estimators with applications to financial model validation, J. Am. Stat. Assoc., 98 (2003), 118–134. https://doi.org/10.1198/016214503388619157 doi: 10.1198/016214503388619157

|

| [3] |

F. Comte, V. G. Catalot, Y. Rozenholc, Penalized nonparametric mean square estimation of the coefficients of diffusion processes, Bernoulli, 13 (2007), 514–543. https://doi.org/10.3150/07-BEJ5173 doi: 10.3150/07-BEJ5173

|

| [4] |

J. Nicolau, Nonparametric estimation of second-order stochastic differential equations, Economet. Theor., 23 (2007), 880–898. https://doi.org/10.1017/S0266466607070375 doi: 10.1017/S0266466607070375

|

| [5] |

A. Gloter, Discrete sampling of an integrated diffusion process and parameter estimation of the diffusion coefficient, ESAIM-Probab. Stat., 4 (2000), 205–227. https://doi.org/10.1051/ps:2000105 doi: 10.1051/ps:2000105

|

| [6] |

A. Gloter, Parameter estimation for a discretely observed integrated diffusion process, Scand. J. Stat., 33 (2006), 83–104. https://doi.org/10.1111/j.1467-9469.2006.00465.x doi: 10.1111/j.1467-9469.2006.00465.x

|

| [7] |

J. Nicolau, Modeling financial time series through second-order stochastic differential equations, Stat. Probabil. Lett., 78 (2008), 2700–2704. https://doi.org/10.1016/j.spl.2008.03.024 doi: 10.1016/j.spl.2008.03.024

|

| [8] |

A. Carriero, T. E. Clark, M. Marcellino, Large Bayesian vector autoregressions with stochastic volatility and non-conjugate priors, J. Econometrics, 212 (2019), 137–154. https://doi.org/10.1016/j.jeconom.2019.04.024 doi: 10.1016/j.jeconom.2019.04.024

|

| [9] |

X. J. He, W. Chen, A closed-form pricing formula for European options under a new stochastic volatility model with a stochastic long-term mean, Math. Financ. Econ., 15 (2021), 381–396. https://doi.org/10.1007/s11579-020-00281-y doi: 10.1007/s11579-020-00281-y

|

| [10] | L. Rogers, W. David, Diffusions, Markov processes and martingales: Volume 2, Itô calculus, Cambridge University Press, 2 (2020). https://doi.org/10.1112/blms/21.1.106 |

| [11] |

P. D. Ditlevsen, S. Ditlevsen, K. K. Andersen, The fast climate fluctuations during the stadial and interstadial climate states, Ann. Glaciol., 35 (2002), 457–462. https://doi.org/10.3189/172756402781816870 doi: 10.3189/172756402781816870

|

| [12] |

H. C. Wang, Z. Y. Lin, Local linear estimation of second-order diffusion models, Commun. Stat.-Theor. M., 40 (2011), 394–407. https://doi.org/10.1080/03610920903391345 doi: 10.1080/03610920903391345

|

| [13] |

Y. Y. Wang, L. X. Zhang, M. T. Tang, Re-weighted functional estimation of second-order diffusion processes, Metrika, 75 (2012), 1129–1151. https://doi.org/10.1007/s00184-011-0372-6 doi: 10.1007/s00184-011-0372-6

|

| [14] |

M. T. Tang, Y. Y. Wang, Q. Q. Zhan, Non parametric bias reduction of diffusion coefficient in integrated diffusion processes, Commun. Stat.-Theor. M., 51 (2022), 6435–6446. https://doi.org/10.1080/03610926.2020.1861298 doi: 10.1080/03610926.2020.1861298

|

| [15] |

S. C. Yang, S. Zhang, G. D. Xing, X. Yang, Strong consistency of nonparametric kernel estimators for integrated diffusion process, Commun. Stat.-Theor. M., 53 (2024), 2792–2815. https://doi.org/10.1080/03610926.2022.2148540 doi: 10.1080/03610926.2022.2148540

|

| [16] |

L. C. Zhao, Z. J. Liu, Strong consistency of the kernel estimators of conditional density function, Acta Math., 1 (1985), 314–318. https://doi.org/10.1007/BF02564838 doi: 10.1007/BF02564838

|

| [17] | L. G. Xue, M. Z. Fan, Strong convergence rates of the double kernel estimates of conditional density (in Chinese), Chinese J. Eng. Math., 1 (2001), 89–93. |

| [18] |

S. Khardani, S. Semmar, Nonparametric conditional density estimation for censored data based on a recursive kernel, Electron. J. Stat., 8 (2015), 2541–2556. https://doi.org/10.1214/14-EJS960 doi: 10.1214/14-EJS960

|

| [19] |

A. Benkhaled, F. Madani, S. Khardani, Strong consistency of local linear estimation of a conditional density function under random censorship, Arab. J. Math, 9 (2020), 513–529. https://doi.org/10.1007/s40065-020-00282-1 doi: 10.1007/s40065-020-00282-1

|

| [20] |

N. Kadiri, M. Meghnafi, A. Rabhi, Strong uniform consistency rates of conditional density estimation in the single functional index model for functional data under random censorship, REVSTAT-Stat. J., 20 (2022), 221–249. https://doi.org/10.57805/revstat.v20i2.374 doi: 10.57805/revstat.v20i2.374

|

| [21] | H. Wang, W. X. Chen, B. J. Li, Large sample properties of maximum likelihood estimator using moving extremes ranked set sampling, J. Korean. Stat. Soc., 2024. https://doi.org/10.1007/s42952-023-00251-2 |

| [22] | B. Sayedana, M. Afshari, P. E. Caines, A. Mahajan, Strong consistency and rate of convergence of switched least squares system identification for autonomous markov jump linear systems, IEEE. T. Automat. Contr., 2024. https://doi.org/10.1109/TAC.2024.3351806 |

| [23] | Y. Li, Y. Y. Wang, M. T. Tang, Non parametric estimation of transition density for second-order diffusion processes, Commun. Stat.-Theor. M., 2023, 1–13. https://doi.org/10.1080/03610926.2023.2234521 |

| [24] | I. Karatzas, E. Shreve, Brownian motion and stochastic calculus, Springer, 2014. https://doi.org/10.1007/978-3-319-57511-7_2 |

| [25] | B. W. Silverman, Density estimation for statistics and data analysis, London: Chapman and Hall, 1986. https://doi.org/10.2307/2348849 |

| [26] |

R. J. Hyndman, D. M. Bashtannyk, G. K. Grunwald, Estimating and visualizing conditional densities, J. Comput. Graph. Stat., 5 (1996), 315–336. https://doi.org/10.1080/10618600.1996.10474715 doi: 10.1080/10618600.1996.10474715

|

| [27] | D. W. Scott, Multivariate density estimation and visualization, Handbook Comput. Stat., 2012,549–569. https://doi.org/10.1007/978-3-642-21551-3_19 |

| [28] |

E. Parzen, On the estimation of a probability density function and mode, Ann. Math. Stat., 33 (1962), 1065–1076. https://doi.org/10.2307/2237880 doi: 10.2307/2237880

|

| [29] |

S. C. Yang, Moment inequality for mixing sequences and nonparametric estimation, Acta Math. Sin., 40 (1997), 271–279. https://doi.org/10.12386/A1997sxxb0034 doi: 10.12386/A1997sxxb0034

|

Figures(2)

Yue Li, Yunyan Wang. Strong consistency of the nonparametric kernel estimator of the transition density for the second-order diffusion process[J]. AIMS Mathematics, 2024, 9(7): 19015-19030. doi: 10.3934/math.2024925

DownLoad:

DownLoad: