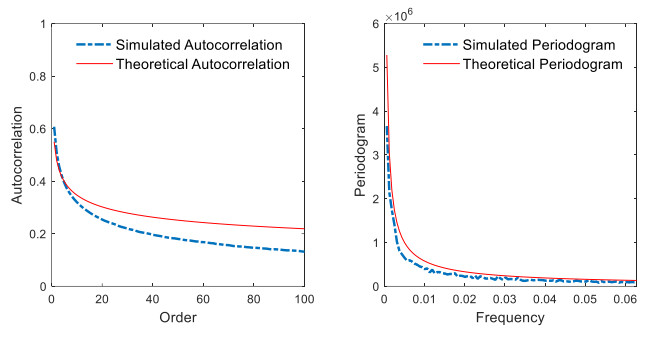

Long memory in test statistics can either originate from fractional integration or be spuriously induced by a short memory process with a structural break. This research estimated and detected long memory from the two causes by simulations and empirical analysis. The simulation results showed that fractional integration and structural break processes could demonstrate long memory properties. The 2ELW estimator was stable for fractional integration but not stable for time series with structural breaks. The modified W statistic based on 2ELW was efficient in discriminating fractional integration and structural breaks. Moreover, we found that six volatility time series of stock indexes and individual stocks in the Chinese market experience significant long memory and structural breaks, and the fractional differencing parameter is overestimated without controlling structural breaks.

Citation: Yirong Huang, Liang Ding, Yan Lin, Yi Luo. A new approach to detect long memory by fractional integration or short memory by structural break[J]. AIMS Mathematics, 2024, 9(6): 16468-16485. doi: 10.3934/math.2024798

Long memory in test statistics can either originate from fractional integration or be spuriously induced by a short memory process with a structural break. This research estimated and detected long memory from the two causes by simulations and empirical analysis. The simulation results showed that fractional integration and structural break processes could demonstrate long memory properties. The 2ELW estimator was stable for fractional integration but not stable for time series with structural breaks. The modified W statistic based on 2ELW was efficient in discriminating fractional integration and structural breaks. Moreover, we found that six volatility time series of stock indexes and individual stocks in the Chinese market experience significant long memory and structural breaks, and the fractional differencing parameter is overestimated without controlling structural breaks.

| [1] |

U. Hassler, J. Wolters, Long memory in inflation rates: International evidence, J. Bus. Econ. Stat., 13 (1995), 37–45. https://doi.org/10.2307/1392519 doi: 10.2307/1392519

|

| [2] |

K. Choi, E. Zivot, Long memory and structural changes in the forward discount: An empirical investigation, J. Int. Money Finan., 26 (2007), 342–363. https://doi.org/10.1016/j.jimonfin.2007.01.002 doi: 10.1016/j.jimonfin.2007.01.002

|

| [3] |

Y. W. Cheung, Long memory in foreign-exchange rates, J. Bus. Econ. Stat., 11 (1993), 93–101. https://doi.org/10.2307/1391309 doi: 10.2307/1391309

|

| [4] |

C. Velasco, Gaussian semiparametric estimation of non-stationary time series, J. Time Ser. Anal., 20 (1999), 87–127. https://doi.org/10.1111/1467-9892.00127 doi: 10.1111/1467-9892.00127

|

| [5] |

K. V. Chow, K. C. Denning, S. Ferris, G. Noronha, Long-term and short-term price memory in the stock market, Econ. Lett., 49 (1995), 287–293. https://doi.org/10.1016/0165-1765(95)00690-H doi: 10.1016/0165-1765(95)00690-H

|

| [6] |

G. Bhardwaj, N. R. Swanson, An empirical investigation of the usefulness of ARFIMA models for predicting macroeconomic and financial time series, J. Econom., 131 (2006), 539–578. https://doi.org/10.1016/j.jeconom.2005.01.016 doi: 10.1016/j.jeconom.2005.01.016

|

| [7] |

C. Floros, S. Jaffry, G. V. Lima, Long memory in the Portuguese stock market, Stud. Econ. Financ., 24 (2007), 220–232. https://doi.org/10.1108/10867370710817400 doi: 10.1108/10867370710817400

|

| [8] |

G. Duppati, A. S. Kumar, F. Scrimgeour, L. Li, Long memory volatility in Asian stock markets, Pac. Account. Rev., 29 (2017), 423–442. https://doi.org/10.1108/PAR-02-2016-0009 doi: 10.1108/PAR-02-2016-0009

|

| [9] |

Y. Luo, Y. Huang, A new combined approach on Hurst exponent estimate and its applications in realized volatility, Physica A, 492 (2018), 1364-1372. https://doi.org/10.1016/j.physa.2017.11.063 doi: 10.1016/j.physa.2017.11.063

|

| [10] |

Y. Luo, Y. Huang, Long memory or structural break? Empirical evidences from index volatility in stock market, China Financ. Rev. Int., 9 (2019), 324-337. https://doi.org/10.1108/CFRI-11-2017-0222 doi: 10.1108/CFRI-11-2017-0222

|

| [11] |

J. R. M. Hosking, Fractional differencing, Biometrika, 68 (1981), 165–176. https://doi.org/10.2307/2335817 doi: 10.2307/2335817

|

| [12] |

P. Perron, Z. Qu, Long-memory and level shifts in the volatility of stock market return indices, J. Bus. Econ. Stat., 28 (2010), 275–290. https://doi.org/10.1198/jbes.2009.06171 doi: 10.1198/jbes.2009.06171

|

| [13] |

P. M. Robinson, Gaussian semiparametric estimation of long range dependence, Ann. Statist., 23 (1995), 1630–1661. https://doi.org/10.1214/aos/1176324317 doi: 10.1214/aos/1176324317

|

| [14] |

J. Geweke, S. Porter-Hudak, The estimation and application of long memory time series models, J. Time Ser. Anal., 4 (1983), 221–238. https://doi.org/10.1111/j.1467-9892.1983.tb00371.x doi: 10.1111/j.1467-9892.1983.tb00371.x

|

| [15] |

C. M. Hurvich, B. K. Ray, Estimation of the memory parameter for nonstationary or noninvertible fractionally integrated processes, J. Time Ser. Anal., 16 (1995), 17–41. https://doi.org/10.1111/j.1467-9892.1995.tb00221.x doi: 10.1111/j.1467-9892.1995.tb00221.x

|

| [16] |

A. Ohanissian, J. R. Russell, R. S. Tsay, True or spurious long memory? A new test, J. Bus. Econ. Stat., 26 (2008), 161–175. https://doi.org/10.1198/073500107000000340 doi: 10.1198/073500107000000340

|

| [17] |

Z. Qu, A test against spurious long memory, J. Bus. Econ. Stat., 29 (2011), 423–438. https://doi.org/10.1198/jbes.2010.09153 doi: 10.1198/jbes.2010.09153

|

| [18] |

A. Jach, P. Kokoszka, Wavelet-domain test for long-range dependence in the presence of a trend, Statistics, 42 (2008), 101–113. https://doi.org/10.1080/02331880701597222 doi: 10.1080/02331880701597222

|

| [19] |

C. Baek, V. Pipiras, Statistical tests for a single change in mean against long-range dependence, J. Time Ser. Anal., 33 (2012), 131–151. https://doi.org/10.1111/j.1467-9892.2011.00747.x doi: 10.1111/j.1467-9892.2011.00747.x

|

| [20] |

A. Leccadito, O. Rachedi, G. Urga, True versus spurious long memory: Some theoretical results and a Monte Carlo comparison, Econom. Rev., 34 (2015), 452–479. https://doi.org/10.1080/07474938.2013.808462 doi: 10.1080/07474938.2013.808462

|

| [21] |

K. Shimotsu, P. C. B. Phillips, Exact local Whittle estimation of fractional integration, Ann. Stat., 33 (2005), 1890–1933. https://doi.org/10.1214/009053605000000309 doi: 10.1214/009053605000000309

|

| [22] |

F. X. Diebold, A. Inoue, Long memory and regime switching, J. Econom., 105 (2001), 131–159. https://doi.org/10.1016/S0304-4076(01)00073-2 doi: 10.1016/S0304-4076(01)00073-2

|

| [23] | P. C. B. Phillips, K. Shimotsu, Local Whittle estimation in nonstationary and unit root cases, Ann. Stat., 32 (2004), 656–692. Available from: http://www.jstor.org/stable/3448481. |

| [24] |

K. Shimotsu, Exact local Whittle estimation of fractional integration with unknown mean and time trend, Economet. Theor., 26 (2010), 501–540. https://doi.org/10.1017/S0266466609100075 doi: 10.1017/S0266466609100075

|

| [25] |

T. G. Andersen, T. Bollerslev, Answering the skeptics: Yes, standard volatility models do provide accurate forecasts, Int. Econ. Rev., 39 (1998), 885–905. https://doi.org/10.2307/2527343 doi: 10.2307/2527343

|

| [26] |

J. Bai, P. Perron, Computation and analysis of multiple structural change models, J. Appl. Econ., 18 (2003), 1–22. https://doi.org/10.1002/jae.659 doi: 10.1002/jae.659

|

| [27] |

J. Bai, P. Perron, Estimating and testing linear models with multiple structural changes, Econometrica, 66 (1998), 47–78. https://doi.org/10.2307/2998540 doi: 10.2307/2998540

|

| [28] | J. Liu, S. Wu, J. V. Zidek, On segmented multivariate regression, Stat. Sin., 7 (1997), 497–525. Available from: https://www.jstor.org/stable/24306090. |

| [29] |

Y. C. Yao, Estimating the number of change-points via Schwarz' criterion, Stat. Probab. Lett., 6 (1988), 181–189. https://doi.org/10.1016/0167-7152(88)90118-6 doi: 10.1016/0167-7152(88)90118-6

|

Figures(3) / Tables(8)

Yirong Huang, Liang Ding, Yan Lin, Yi Luo. A new approach to detect long memory by fractional integration or short memory by structural break[J]. AIMS Mathematics, 2024, 9(6): 16468-16485. doi: 10.3934/math.2024798

DownLoad:

DownLoad: