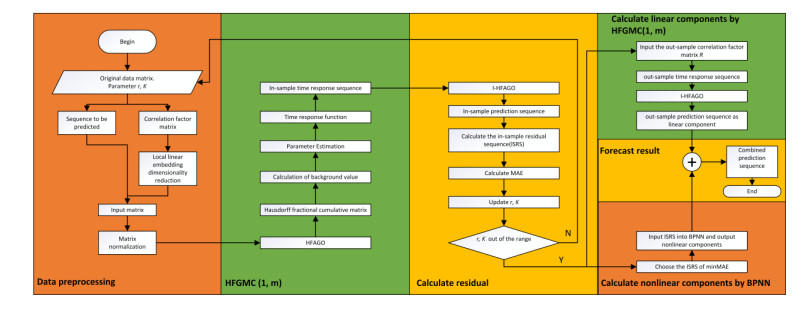

Forecast of stock prices can guide investors' investment decisions. Due to the high-dimensional and long-memory characteristics of stock data, it is difficult to predict. The fractional grey model with convolution (FGMC (1, m)) can be used to predict time series, because of its memory and ability to process high-dimensional data. However, the FGMC (1, m) model has some disadvantages, including complex calculation, loss of information, and approximate background values. In this paper, Hausdorff fractional derivative and Newton-Cotes formula are used to optimize these shortcomings and can get a Hausdorff fractional grey model with convolution (HFGMC (1, m)) model. The HFGMC (1, m)-LLE-BP model is proposed in this paper. HFGMC (1, m) provides a solution that can reduce the complexity of the cumulative generator matrix calculation and preserve the global information of the sequence. Newton-Cotes formula is used to calculate the background value, which can solve the shortcomings of approximate background values. The HFGMC (1, m) model is used to predict the linear component of the sequence, and the BP neural network is used to predict the nonlinear component of the sequence. In addition, because of the high-dimensional and nonlinear characteristics of stock data, a local linear embedding (LLE) algorithm is used to remove redundant information in high-dimensional non-linear data. The experimental results show that the HFGMC (1, m)-LLE-BP model is effective for predicting the stock price in different trends.

Citation: Wenhua Dong, Chunna Zhao. Stock price forecasting based on Hausdorff fractional grey model with convolution and neural network[J]. Mathematical Biosciences and Engineering, 2021, 18(4): 3323-3347. doi: 10.3934/mbe.2021166

Forecast of stock prices can guide investors' investment decisions. Due to the high-dimensional and long-memory characteristics of stock data, it is difficult to predict. The fractional grey model with convolution (FGMC (1, m)) can be used to predict time series, because of its memory and ability to process high-dimensional data. However, the FGMC (1, m) model has some disadvantages, including complex calculation, loss of information, and approximate background values. In this paper, Hausdorff fractional derivative and Newton-Cotes formula are used to optimize these shortcomings and can get a Hausdorff fractional grey model with convolution (HFGMC (1, m)) model. The HFGMC (1, m)-LLE-BP model is proposed in this paper. HFGMC (1, m) provides a solution that can reduce the complexity of the cumulative generator matrix calculation and preserve the global information of the sequence. Newton-Cotes formula is used to calculate the background value, which can solve the shortcomings of approximate background values. The HFGMC (1, m) model is used to predict the linear component of the sequence, and the BP neural network is used to predict the nonlinear component of the sequence. In addition, because of the high-dimensional and nonlinear characteristics of stock data, a local linear embedding (LLE) algorithm is used to remove redundant information in high-dimensional non-linear data. The experimental results show that the HFGMC (1, m)-LLE-BP model is effective for predicting the stock price in different trends.

| [1] | S. Z. Shi, W. L Liu, M. L Jin, Stock price forecasting based on a combined model of ARMA and BP neural network and Markov model, Inf. Process. Manage., 4 (2013), 215-221. |

| [2] |

M. Vijh, D. Chandola, V. A. Tikkiwal, A. Kumar, Stock closing price prediction using machine learning techniques, Proc. Comput. Sci., 167 (2020), 599-606. doi: 10.1016/j.procs.2020.03.326

|

| [3] |

G. Liu, X. J. Wang, A new metric for individual stock trend prediction, Eng. Appl. Artif. Intell., 82 (2019), 1-12. doi: 10.1016/j.engappai.2019.03.019

|

| [4] | E. Sin, L. Wang, Bitcoin price prediction using ensembles of neural networks, in 13th International Conference on Natural Computation, Fuzzy Systems and Knowledge Discovery, (2017), 666-671. |

| [5] | M. Zhu, L. Wang, Intelligent trading using support vector regression and multilayer perceptrons optimized with genetic algorithms, in The 2010 International Joint Conference on Neural Networks, (2010), 1-5. |

| [6] | G. Q. Dong, K. Fataliyev, L. Wang, One-step and multi-step ahead stock prediction using backpropagation neural networks, in The 9th International Conference on Information, Communications & Signal Processing, (2013), 1-5. |

| [7] |

D. H. Zhang, S. Lou, The application research of neural network and BP algorithm in stock price pattern classification and prediction, Futur. Gener. Comp. Syst., 115 (2021), 872-879. doi: 10.1016/j.future.2020.10.009

|

| [8] | K. K. Teo, L. Wang, Z. Liu, Wavelet packet multi-layer perceptron for chaotic time series prediction: effects of weight initialization, in International Conference on Computational Science, Springer, Berlin, Heidelberg, (2001), 310-317. |

| [9] | H. K. Sang, C. Cheong, S. M. Yoon, Long memory volatility in Chinese stock markets, Phys. A Stat. Mech. Appl., 389 (2020), 1425-1433. |

| [10] | S. L. Gao, Q. Zhao, The memory effect of fractional calculus, J. Leshan Normal University, 30 (2015), 1-4. |

| [11] |

W. Y. Wu, S. P. Chen, A prediction method using the grey model GMC (1, n) combined with the grey relational analysis: a case study on Internet access population forecast, Appl. Math. Comput., 169 (2005), 198-217. doi: 10.1016/j.amc.2004.10.087

|

| [12] | X. Ma, Z. B. Liu, The GMC (1, n) model with optimized parameters and its application, J. Grey Syst., 29 (2017), 122-138. |

| [13] |

T. L. Tien, A research on the grey prediction model GM (1, n), Appl. Math. Comput., 218 (2012), 4903-4916. doi: 10.1016/j.amc.2011.10.055

|

| [14] |

W. Q. Wu, X. Ma, B. Zeng, W. Y. Lv, Y. Wang, W. P. Li, A novel Grey Bernoulli model for short-term natural gas consumption forecasting, Appl. Math. Model., 84 (2020), 393-404. doi: 10.1016/j.apm.2020.04.006

|

| [15] |

Q. Z. Xiao, M. Y. Gao, X. P. Xiao, M. Goh, A novel grey Riccati-Bernoulli model and its application for the clean energy consumption prediction, Eng. Appl. Artif. Intell., 95 (2020), 103863. doi: 10.1016/j.engappai.2020.103863

|

| [16] |

X. Ma, Z. B. Liu, Y. Wang, Application of a novel nonlinear multivariate grey Bernoulli model to predict the tourist income of China, J. Comput. Appl. Math., 347 (2019), 84-94. doi: 10.1016/j.cam.2018.07.044

|

| [17] |

W. Q. Wu, X. Ma, B. Zeng, Y. Wang, W. Cai, Forecasting short-term renewable energy consumption of China using a novel fractional nonlinear grey Bernoulli model, Renew. Energy, 140 (2019), 70-87. doi: 10.1016/j.renene.2019.03.006

|

| [18] | U. Şahin, T. Şahin, Forecasting the cumulative number of confirmed cases of COVID-19 in Italy, UK and USA using fractional nonlinear grey Bernoulli model, Chaos Solitons Fractals, 138 (2020), 109948. |

| [19] |

X. Ma, Z. B. Liu, The kernel-based nonlinear multivariate grey model, Appl. Math. Model., 56 (2018), 217-238. doi: 10.1016/j.apm.2017.12.010

|

| [20] |

L. Z. Wu, S. H. Li, R. Q. Huang, Q. Xu, A new grey prediction model and its application to predicting landslide displacement, Appli. Soft Comput., 95 (2020), 106543. doi: 10.1016/j.asoc.2020.106543

|

| [21] |

X. Y. Zeng, S. L. Yan, F. L. He, Y. C. Shi, Multi-variable grey model based on dynamic background algorithm for forecasting the interval sequence, Appl. Math. Model., 80 (2020), 99-114. doi: 10.1016/j.apm.2019.11.032

|

| [22] |

W. Q. Wu, X. Ma, B. Zeng, Y. Wang, W. Cai, Application of the novel fractional grey model FAGMO (1, 1, k) to predict China's nuclear energy consumption, Energy, 165 (2018), 223-234. doi: 10.1016/j.energy.2018.09.155

|

| [23] |

W. L. Xie, C. X. Liu, W. Z. Wu, W. D. Li, C. Liu, Continuous grey model with conformable fractional derivative, Chaos Solitons Fractals, 139 (2020), 110285. doi: 10.1016/j.chaos.2020.110285

|

| [24] |

X. Ma, W. Q. Wu, B. Zeng, Y. Wang, X. X. Wu, The conformable fractional grey system model, ISA Trans., 96 (2020), 255-271. doi: 10.1016/j.isatra.2019.07.009

|

| [25] | X. Ma, M. Xie, W.Q. Wu, B. Zeng, Y. Wang, X. X Wu, The novel fractional discrete multivariate grey system model and its applications, Appl. Math. Model., 70 (2019) 402-424. |

| [26] | J. Wang, Y. Liang, L. Qiu, X. U. Yang, Improved machine learning technique for solving Hausdorff derivative diffusion equations, Fractals, 28 (2020), 160-169. |

| [27] | J. Wang, H. Shan, W.Q. Wang, X.F. Chen, P.Y. Li, Research on wind speed prediction based on hybrid gray theory, Acta Energiae Solaris Sinica, 39 (2018), 3544-3549. |

| [28] |

S. T. Roweis, L. K. Saul, Nonlinear dimensionality reduction by locally linear embedding, Science, 290 (2000), 2323-2326. doi: 10.1126/science.290.5500.2323

|

| [29] | G. E. Hinton, D. E. Rumelhart, J. L. Mcclelland, Disctributed representations, Parallel distributed processing: explorations in the microstructure of cognition, Language, 63 (1986), 45-76. |

| [30] |

Z. X. Yu, L. Qin, Y. J. Chen, M. D. Parmar, Stock price forecasting based on LLE-BP neural network model, Phys. A Stat. Mech. Appl., 553 (2020), 124197. doi: 10.1016/j.physa.2020.124197

|

| [31] |

J. Miśkiewicz, Economy with the time delay of information flow-The stock market case, Phys. A Stat. Mech. Appl., 391 (2012), 1388-1394. doi: 10.1016/j.physa.2011.09.024

|

| [32] | J. Wang, R. K. W. Wong, T. C.M. Lee, Locally linear embedding with additive noise, Pattern Recognit. Lett., 123 (2019), 45-52. |

| [33] |

S. Kadoury, M. D. Levine, Face detection in gray scale images using locally linear embeddings, Comput. Vis. Image Underst., 105 (2007), 1-20. doi: 10.1016/j.cviu.2006.06.009

|

| [34] |

E. Cadenas, R. Rivera, Wind speed forecasting in three different regions of Mexico, using a hybrid ARIMA-ANN model, Renew. Energy, 35 (2010), 2732-2738. doi: 10.1016/j.renene.2010.04.022

|

| [35] |

C. L. Xiao, W. L. Xia, J. J. Jiang, Stock price forecast based on combined model of ARI-MA-LS-SVM, Neural Comput. Appl., 32 (2020), 5379-5388. doi: 10.1007/s00521-019-04698-5

|

| [36] |

H. L. Niu, K. L. Xu, A hybrid model combining variational mode decomposition and an attention-GRU network for stock price index forecasting, Math. Biosci. Eng., 17 (2020), 7151-7166. doi: 10.3934/mbe.2020367

|

| [37] |

Y. L Wang, L. W. Wang, F. J. Yang, W. X. Di, Q. Chang, Advantages of direct input-to-output connections in neural networks: The Elman network for stock index forecasting, Inf. Sci., 547 (2021), 1066-1079. doi: 10.1016/j.ins.2020.09.031

|

| [38] |

Y. Lin, Y. Yan, J. L. Xu, Y. Liao, F. Ma, Forecasting stock index price using the CEEMDAN-LSTM model, N. Am. Econ. Financ., 57 (2021), 101421. doi: 10.1016/j.najef.2021.101421

|

| [39] |

S. Feuerriegel, J. Gordon, Long-term stock index forecasting based on text mining of regulatory disclosures, Decis. Support Syst., 112 (2018), 88-97. doi: 10.1016/j.dss.2018.06.008

|

mbe-18-04-166-supplementary.pdf mbe-18-04-166-supplementary.pdf |

|

Figures(9) / Tables(14)

Wenhua Dong, Chunna Zhao. Stock price forecasting based on Hausdorff fractional grey model with convolution and neural network[J]. Mathematical Biosciences and Engineering, 2021, 18(4): 3323-3347. doi: 10.3934/mbe.2021166

DownLoad:

DownLoad: