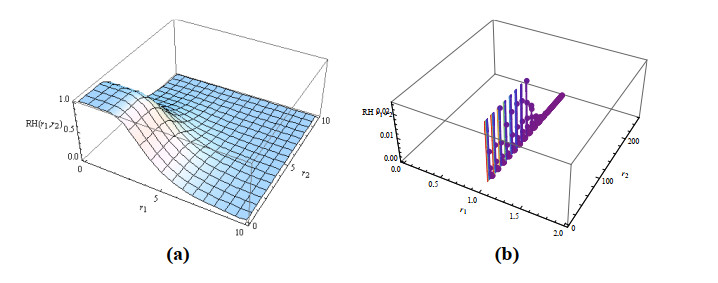

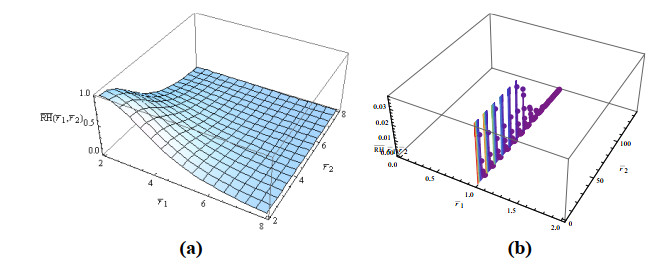

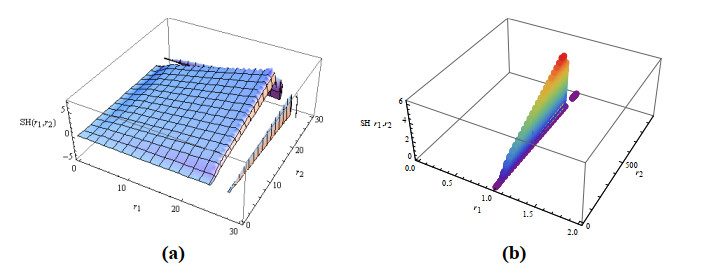

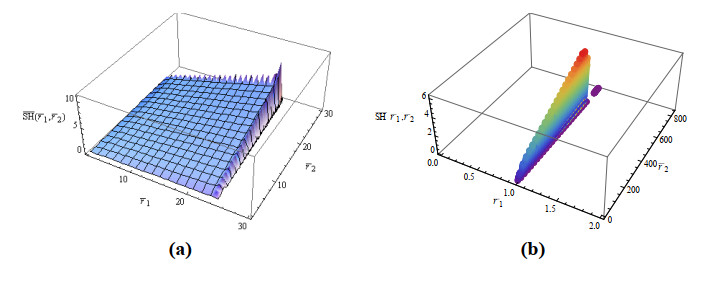

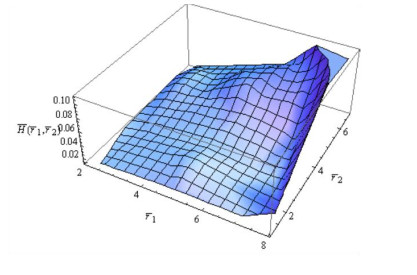

We developed a multivariate discrete range distribution derived from the Wiener process to model high-low price dynamics of multiple assets observed at discrete times and subject to market imposed bounds. The model provides closed-form expressions for the joint PMF, CDF, survival and hazard functions, reversed and second order failure rates, moments, stress-strength reliability, and a full system of multivariate order statistics. A truncated version of the distribution was also established to account for realistic price limit regimes, showing how probability mass redistributes within constrained domains. These theoretical properties were supplemented by a numerical study based on real high-low data and confirmed that the model can capture clustered volatility, attenuation of tail risk, and joint range behavior more precisely than unconstrained formulations. The proposed framework offers a mathematically coherent and computationally practical tool for the analysis of range-based behavior in constrained financial markets.

Citation: Sana Abdulkream Alharbi, Mohamed Abd Allah El-Hadidy. A multivariate discrete Wiener range distribution with truncation: Theory, reliability properties, and applications to constrained financial markets[J]. AIMS Mathematics, 2026, 11(2): 3563-3593. doi: 10.3934/math.2026146

We developed a multivariate discrete range distribution derived from the Wiener process to model high-low price dynamics of multiple assets observed at discrete times and subject to market imposed bounds. The model provides closed-form expressions for the joint PMF, CDF, survival and hazard functions, reversed and second order failure rates, moments, stress-strength reliability, and a full system of multivariate order statistics. A truncated version of the distribution was also established to account for realistic price limit regimes, showing how probability mass redistributes within constrained domains. These theoretical properties were supplemented by a numerical study based on real high-low data and confirmed that the model can capture clustered volatility, attenuation of tail risk, and joint range behavior more precisely than unconstrained formulations. The proposed framework offers a mathematically coherent and computationally practical tool for the analysis of range-based behavior in constrained financial markets.

| [1] | M. Parkinson, The extreme value method for estimating the variance of the rate of return, J. Bus., 53 (1980), 61–65. |

| [2] | M. Garman, M. Klass, On the estimation of security price volatilities from historical data, J. Bus., 53 (1980), 67–78. |

| [3] |

R. Cont, Empirical properties of asset returns: stylized facts and statistical issues, Quant. Finance, 1 (2001), 223–236. https://doi.org/10.1080/713665670 doi: 10.1080/713665670

|

| [4] |

A. J. Patton, Modelling asymmetric exchange rate dependence, Int. Econ. Rev., 47 (2006), 527–556. https://doi.org/10.1111/j.1468-2354.2006.00387.x doi: 10.1111/j.1468-2354.2006.00387.x

|

| [5] | A. J. McNeil, R. Frey, P. Embrechts, Quantitative Risk Management: Concepts, Techniques and Tools, Princeton: Princeton University Press, 2015. |

| [6] |

K. A. Kim, S. G. Rhee, Price limit performance: Evidence from the Tokyo stock exchange, J. Finance, 52 (1997), 885–901. https://doi.org/10.2307/2329504 doi: 10.2307/2329504

|

| [7] | W. Feller, The asymptotic distribution of the range of sums of independent random variables, Ann. Math. Stat., 22 (1951), 427–432. |

| [8] |

C. Withers, S. Nadarajah, The distribution and quantiles of the range of a Wiener process, Appl. Math. Comput., 232 (2014), 766–770. https://doi.org/10.1016/j.amc.2014.01.147 doi: 10.1016/j.amc.2014.01.147

|

| [9] |

A. Teamah, M. El-Hadidy, M. El-Ghoul, On bounded range distribution of a Wiener process, Commun. Stat. Theory Methods, 51 (2022), 919–942. https://doi.org/10.1080/03610926.2016.1267766 doi: 10.1080/03610926.2016.1267766

|

| [10] |

W. Kemp, Characterization of a discrete normal distribution, J. Stat. Plan. Inference, 63 (1997), 223–229. https://doi.org/10.1016/S0378-3758(97)00020-7 doi: 10.1016/S0378-3758(97)00020-7

|

| [11] |

D. Roy, The discrete normal distribution, Commun. Stat. Theory Methods, 32 (2003), 1871–1883. https://doi.org/10.1081/STA-120023256 doi: 10.1081/STA-120023256

|

| [12] | T. Nakagawa, S. Osaki, The discrete Weibull distribution, IEEE Trans. Reliab., 24 (1975), 300–301. |

| [13] |

K. Jayakumar, M. Girish Babu, Discrete Weibull geometric distribution and its properties, Commun. Stat. Theory Methods, 47 (2018), 1767–1783. https://doi.org/10.1080/03610926.2017.1327074 doi: 10.1080/03610926.2017.1327074

|

| [14] |

M. El-Hadidy, Discrete distribution for the stochastic range of a Wiener process and its properties, Fluct. Noise Lett., 18 (2019), 1950024. https://doi.org/10.1142/S021947751950024X doi: 10.1142/S021947751950024X

|

| [15] |

M. El-Hadidy, A. Alfreedi, Internal truncated distributions: Applications to Wiener process range distribution when deleting a minimum stochastic volatility interval from its domain, J. Taibah Univ. Sci., 13 (2019), 201–215. https://doi.org/10.1080/16583655.2018.1555020 doi: 10.1080/16583655.2018.1555020

|

| [16] | C. Alexander, Market Models: A Guide to Financial Data Analysis, Hoboken: John Wiley & Sons, 2001. |

| [17] |

R. Alraddadi, M. El-Hadidy, A multivariate model for the Wiener process range, with statistical properties under stochastic volatility, AIMS Math., 10 (2025), 22023–22052. https://doi.org/10.3934/math.2025980 doi: 10.3934/math.2025980

|

| [18] |

D. Pan, J. B. Liu, F. Huang, J. Cao, A. Alsaedi, A Wiener process model with truncated normal distribution for reliability analysis, Appl. Math. Model., 50 (2017), 333–346. https://doi.org/10.1016/j.apm.2017.05.049 doi: 10.1016/j.apm.2017.05.049

|

| [19] | V. Sharma, Variance of some information measures for truncated random variables with applications, PhD thesis, RGIPT, India, 2024. |

| [20] |

A. Aljadani, M. M. Mansour, H. M. Yousof, A novel model for finance and reliability applications, Pak. J. Stat. Oper. Res., 20 (2024), 489–515. https://doi.org/10.18187/pjsor.v20i3.4439 doi: 10.18187/pjsor.v20i3.4439

|

| [21] |

S. J. Koopman, A. Lucas, M. Scharth, A. Opschoor, Dynamic discrete copula models for high-frequency stock price changes, J. Appl. Econom., 33 (2018), 966–985. https://doi.org/10.1002/jae.2645 doi: 10.1002/jae.2645

|

| [22] |

J. G. Skellam, The frequency distribution of the difference between two Poisson variates belonging to different populations, J. R. Stat. Soc. Ser. A, 109 (1946), 296. https://doi.org/10.1111/j.2397-2335.1946.tb04670.x doi: 10.1111/j.2397-2335.1946.tb04670.x

|

| [23] | R. S. Tsay, Analysis of Financial Time Series, 3 Eds., Hoboken: John Wiley & Sons, 2010. https://doi.org/10.1002/9780470644560 |

| [24] |

A. Subrahmanyam, Circuit breakers and market volatility: A theoretical perspective, J. Finance, 49 (1994), 237–254. https://doi.org/10.2307/2329142 doi: 10.2307/2329142

|

| [25] | A. W. Marshall, I. Olkin, Life Distributions, Berlin: Springer, 2007. |

| [26] |

M. Shaked, J. G. Shanthikumar, J. B. Valdez-Torres, Discrete hazard rate functions, Comput. Oper. Res., 22 (1995), 391–402. https://doi.org/10.1016/0305-0548(94)00048-D doi: 10.1016/0305-0548(94)00048-D

|

| [27] | R. E. Barlow, F. Proschan, Mathematical Theory of Reliability, Philadelphia: SIAM, 1996. |

| [28] | M. Shaked, J. G. Shanthikumar, Stochastic Orders, Berlin: Springer, 2007. https://doi.org/10.1007/978-0-387-34675-5 |

| [29] |

D. Roy, R. P. Gupta, Characterizations and model selections through reliability measures in the discrete case, Stat. Probab. Lett., 43 (1999), 197–206. https://doi.org/10.1016/S0167-7152(98)00260-0 doi: 10.1016/S0167-7152(98)00260-0

|

| [30] | F. J. Samaniego, System Signatures and Their Applications in Engineering Reliability, Berlin: Springer, 2007. https://doi.org/10.1007/978-0-387-71797-5 |

| [31] | S. Kotz, N. Balakrishnan, N. L. Johnson, Continuous Multivariate Distributions, Hoboken: Wiley, 2000. |

| [32] | N. L. Johnson, S. Kotz, N. Balakrishnan, Discrete Multivariate Distributions, Hoboken: Wiley, 1994. |

| [33] | H. S. Wilf, Generatingfunctionology, Singapore: Academic Press, 2006. https://doi.org/10.1016/C2009-0-02369-1 |

| [34] | F. W. J. Olver, NIST Handbook of Mathematical Functions, Cambridge: Cambridge University Press, 2010. |

| [35] | H. A. David, H. N. Nagaraja, Order Statistics, 3 Eds., Hoboken: Wiley, 2003. |

| [36] | B. C. Arnold, N. Balakrishnan, H. N. Nagaraja, A First Course in Order Statistics, Philadelphia: SIAM, 2008. |

| [37] | N. Balakrishnan, V. B. Nevzorov, A Primer on Statistical Distributions, Hoboken: Wiley, 2003. |

| [38] | S. Kotz, Y. Lumelskii, M. Pensky, The Stress-Strength Model and and Its Generalizations, Singapore: World Scientific, 2003. https://doi.org/10.1142/5015 |

| [39] |

O. Mnari, B. Faouel, Price limit bands, risk-return trade-off and asymmetric volatility, Econ. Bus. Rev., 10 (2024), 142–162. https://doi.org/10.18559/ebr.2024.3.1604 doi: 10.18559/ebr.2024.3.1604

|

| [40] |

M. Fałdziński, P. Fiszeder, P. Molnár, Improving volatility forecasts: Evidence from range-based models, N. Am. J. Econ. Finance, 69 (2024), 102019. https://doi.org/10.1016/j.najef.2023.102019 doi: 10.1016/j.najef.2023.102019

|

| [41] |

T. Bollerslev, J. Li, Q. Li, Optimal nonparametric range-based volatility estimation, J. Econ., 238 (2024), 105548. https://doi.org/10.1016/j.jeconom.2023.105548 doi: 10.1016/j.jeconom.2023.105548

|

| [42] | J. Zito, D. R. Kowal, A dynamic copula model for probabilistic forecasting of non-Gaussian multivariate time series, preprint paper, 2025. https://doi.org/10.48550/arXiv.2502.16874 |

| [43] | MDPI Mathematics, Application of survival analysis in economics, finance and insurance, Special issue, 2024. |

Figures(17) / Tables(2)

Sana Abdulkream Alharbi, Mohamed Abd Allah El-Hadidy. A multivariate discrete Wiener range distribution with truncation: Theory, reliability properties, and applications to constrained financial markets[J]. AIMS Mathematics, 2026, 11(2): 3563-3593. doi: 10.3934/math.2026146

DownLoad:

DownLoad: