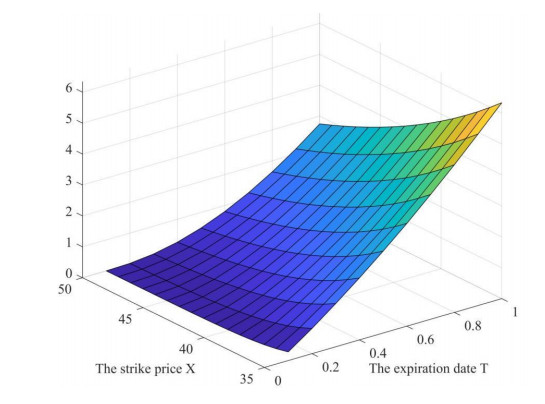

This paper proposes a pricing model for equity warrants under the sub-mixed fractional Brownian motion regime with the interest rate following the Merton short rate model. By using the delta hedging strategy, the corresponding partial differential equations for equity warrants are obtained. Moreover, the explicit pricing formula for equity warrants and some numerical results are given.

Citation: Xinyi Wang, Jingshen Wang, Zhidong Guo. Pricing equity warrants under the sub-mixed fractional Brownian motion regime with stochastic interest rate[J]. AIMS Mathematics, 2022, 7(9): 16612-16631. doi: 10.3934/math.2022910

This paper proposes a pricing model for equity warrants under the sub-mixed fractional Brownian motion regime with the interest rate following the Merton short rate model. By using the delta hedging strategy, the corresponding partial differential equations for equity warrants are obtained. Moreover, the explicit pricing formula for equity warrants and some numerical results are given.

| [1] |

B. Lauterbach, P. Schultz, Pricing warrants: an empirical study of the Black-Scholes model and its alternatives, J. Financ., 45 (1990), 1181-1209. https://doi.org/10.1111/j.1540-6261.1990.tb02432.x doi: 10.1111/j.1540-6261.1990.tb02432.x

|

| [2] |

D. Galai, M. Schneller, Pricing of warrants and the value of the firm, J. Financ., 33 (1978), 1333-1342. https://doi.org/10.1111/j.1540-6261.1978.tb03423.x doi: 10.1111/j.1540-6261.1978.tb03423.x

|

| [3] | F. Black, M. Scholes, The pricing of options and corporate liabilities, J. Polit. Econ., 81 (1973), 637-654. |

| [4] | C. Necula, Option pricing in a fractional Brownian motion environment, SSRN, working paper 2002. https://doi.org/10.2139/ssrn.1286833 |

| [5] |

B. Mandelbrot, J. Van Ness, Fractional Brownian motions, fractional noises and applications, SIAM Rev., 10 (1968), 422-437. https://doi.org/10.1137/1010093 doi: 10.1137/1010093

|

| [6] |

W. Xiao, W. Zhang, W. Xu, X. Zhang, The valuation of equity warrants in a fractional Brownian environment, Physica A, 391 (2012), 1742-1752. https://doi.org/10.1016/j.physa.2011.10.024 doi: 10.1016/j.physa.2011.10.024

|

| [7] |

W. Zhang, W. Xiao, C. He, Equity warrants pricing model under fractional Brownian motion and an empirical study, Expert Syst. Appl., 36 (2009), 3056-3065. https://doi.org/10.1016/j.eswa.2008.01.056 doi: 10.1016/j.eswa.2008.01.056

|

| [8] |

W. Xiao, W. Zhang, X. Zhang, X. Zhang, Pricing model for equity warrants in a mixed fractional Brownian environment and its algorithm, Physica A, 391 (2012), 6418-6431. https://doi.org/10.1016/j.physa.2012.07.041 doi: 10.1016/j.physa.2012.07.041

|

| [9] |

L. Rogers, Arbitrage with fractional Brownian motion, Math. Financ., 7 (1997), 95-105. https://doi.org/10.1111/1467-9965.00025 doi: 10.1111/1467-9965.00025

|

| [10] |

X. Zhang, W. Xiao, Arbitrage with fractional Gaussian processes, Physica A, 471 (2017), 620-628. https://doi.org/10.1016/j.physa.2016.12.064 doi: 10.1016/j.physa.2016.12.064

|

| [11] |

T. Bojdecki, L. Gorostiza, A. Talarczyk, Sub-fractional Brownian motion and its relation to occupation times, Stat. Probabil. Lett., 69 (2004), 405-419. https://doi.org/10.1016/j.spl.2004.06.035 doi: 10.1016/j.spl.2004.06.035

|

| [12] |

W. Wang, G. Cai, X. Tao, Pricing geometric Asian power options in the sub-fractional Brownian motion environment, Chaos Soliton. Fract., 145 (2021), 110754. https://doi.org/10.1016/J.CHAOS.2021.110754 doi: 10.1016/J.CHAOS.2021.110754

|

| [13] |

L. Bian, Z. Li, Fuzzy simulation of European option pricing using sub-fractional Brownian motion, Chaos Soliton. Fract., 153 (2021), 111442. https://doi.org/10.1016/J.CHAOS.2021.111442 doi: 10.1016/J.CHAOS.2021.111442

|

| [14] |

E. Charles, Z. Mounir, On the sub-mixed fractional Brownian motion, Appl. Math. J. Chin. Univ., 30 (2015), 27-43. https://doi.org/10.1007/s11766-015-3198-6 doi: 10.1007/s11766-015-3198-6

|

| [15] | C. Tubor, Sub-fractional Brownian motion as a model in finance, University of Bucharest, working paper 2008. |

| [16] |

C. Tubor, Some properties of the sub-fractional Brownian motion, Stochastics, 79 (2007), 431-448. https://doi.org/10.1080/17442500601100331 doi: 10.1080/17442500601100331

|

| [17] |

C. Bender, T. Sottinen, E. Valkeila, Pricing by hedging and no-arbitrage beyond semimartingales, Finance Stoch., 12 (2008), 441-468. https://doi.org/10.1007/s00780-008-0074-8 doi: 10.1007/s00780-008-0074-8

|

| [18] |

F. Xu, S. Zhou, Pricing of perpetual American put option with sub-mixed fractional Brownian motion, FCAA, 22 (2019), 1145-1154. https://doi.org/10.1515/fca-2019-0060 doi: 10.1515/fca-2019-0060

|

| [19] |

A. Araneda, N. Bertschinger, The sub-fractional CEV model, Physica A, 573 (2021), 125974. https://doi.org/10.1016/J.PHYSA.2021.125974 doi: 10.1016/J.PHYSA.2021.125974

|

| [20] |

X. He, S. Zhu, A closed-form pricing formula for European options under the Heston model with stochastic interest rate, J. Comput. Appl. Math., 335 (2018), 323-333. https://doi.org/10.1016/j.cam.2017.12.011 doi: 10.1016/j.cam.2017.12.011

|

| [21] |

X. He, W. Chen, An approximation formula for the price of credit default swaps under the fast-mean reversion volatility model, Appl. Math., 64 (2019), 367-382. https://doi.org/10.21136/AM.2019.0313-17 doi: 10.21136/AM.2019.0313-17

|

| [22] |

X. He, S. Lin, A fractional Black-Scholes model with stochastic volatility and European option pricing, Expert Syst. Appl., 178 (2021), 114983. https://doi.org/10.1016/J.ESWA.2021.114983 doi: 10.1016/J.ESWA.2021.114983

|

| [23] |

X. He, W. Chen, Pricing foreign exchange options under a hybrid Heston-Cox-Ingersoll-Ross model with regime switching, IMA. J. Manag. Math., 33 (2022), 255-272. https://doi.org/10.1093/IMAMAN/DPAB013 doi: 10.1093/IMAMAN/DPAB013

|

| [24] | X. He, S. Lin, An analytical approximation formula for barrier option prices under the Heston model, Comput. Econ., in press. https://doi.org/10.1007/s10614-021-10186-7 |

| [25] |

X. He, W. Chen, A closed-form pricing formula for European options under a new stochastic volatility model with a stochastic long-term mean, Math. Finan. Econ., 15 (2021), 381-396. https://doi.org/10.1007/s11579-020-00281-y doi: 10.1007/s11579-020-00281-y

|

| [26] |

R. Merton, On the pricing of corporate debt: the risk structure of interest rates, J. Financ., 29 (1974), 449-470. https://doi.org/10.1111/j.1540-6261.1974.tb03058.x doi: 10.1111/j.1540-6261.1974.tb03058.x

|

| [27] |

Z. Guo, Option pricing under the Merton model of the short rate in subdiffusive Brownian motion regime, J. Stat. Comput. Sim., 87 (2017), 519-529. https://doi.org/10.1080/00949655.2016.1218880 doi: 10.1080/00949655.2016.1218880

|

| [28] |

J. Liu, L. Li, L. Yan, Sub-fractional model for credit risk pricing, Int. J. Nonlin. Sci. Num., 11 (2010), 231-236. https://doi.org/10.1515/IJNSNS.2010.11.4.231 doi: 10.1515/IJNSNS.2010.11.4.231

|

| [29] |

A. Ukhov, Warrant pricing using observable variables, J. Financ. Res., 27 (2004), 329-339. https://doi.org/10.1111/j.1475-6803.2004.00100.x doi: 10.1111/j.1475-6803.2004.00100.x

|

Figures(5) / Tables(3)

Xinyi Wang, Jingshen Wang, Zhidong Guo. Pricing equity warrants under the sub-mixed fractional Brownian motion regime with stochastic interest rate[J]. AIMS Mathematics, 2022, 7(9): 16612-16631. doi: 10.3934/math.2022910

DownLoad:

DownLoad: