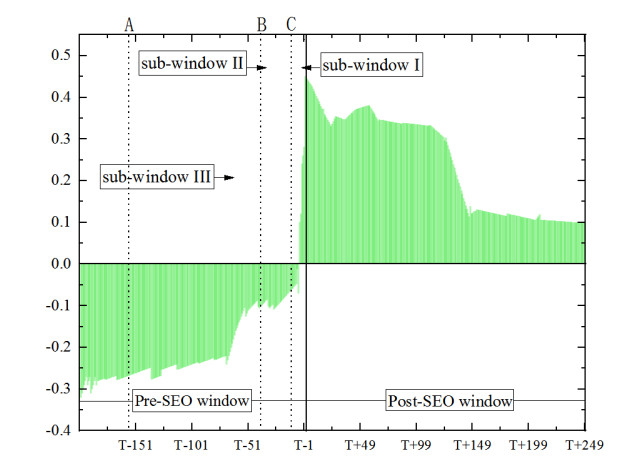

Seasoned equity offerings attract a great deal of attention from investors in China's stock market, and they provide natural experimental environment for examining relationship between investor sentiment and asset pricing. We measure the investor sentiment on the individual stock level and examine its impact on stock pricing by using seasoned equity offerings (SEO) samples in the China's stock market from 2006 to 2019. The study shows that investor sentiment gradually rises during the Pre-SEO window and stays at a relatively high level after the new equity issuance. Meanwhile, investor sentiment is a significant pricing factor during the SEO window. However, the role of investor sentiment is different during different stages of SEO events, with a negative and positive impact on the Pre-SEO window and Post-SEO window respectively. Overall, this study identifies the pricing mechanism of investor sentiment in Chinese SEO market and provides some policy implications for portfolio management and market regulation.

Citation: Changqing Luo, Zijing Li, Lan Liu. Does investor sentiment affect stock pricing? Evidence from seasoned equity offerings in China[J]. National Accounting Review, 2021, 3(1): 115-136. doi: 10.3934/NAR.2021006

Seasoned equity offerings attract a great deal of attention from investors in China's stock market, and they provide natural experimental environment for examining relationship between investor sentiment and asset pricing. We measure the investor sentiment on the individual stock level and examine its impact on stock pricing by using seasoned equity offerings (SEO) samples in the China's stock market from 2006 to 2019. The study shows that investor sentiment gradually rises during the Pre-SEO window and stays at a relatively high level after the new equity issuance. Meanwhile, investor sentiment is a significant pricing factor during the SEO window. However, the role of investor sentiment is different during different stages of SEO events, with a negative and positive impact on the Pre-SEO window and Post-SEO window respectively. Overall, this study identifies the pricing mechanism of investor sentiment in Chinese SEO market and provides some policy implications for portfolio management and market regulation.

| [1] |

Adam S (2015) Forecasting returns with fundamentals-removed investor sentiment. Int J Financ Stud 3: 319–341. doi: 10.3390/ijfs3030319

|

| [2] |

Antoniou C, Doukas JA, Subrahmanyam A (2013) Cognitive dissonance, sentiment and momentum. J Financ Quant Anal 48: 245–275. doi: 10.1017/S0022109012000592

|

| [3] |

Antoniou C, Doukas J, Subrahmanyam A (2015) Investor sentiment, beta and the cost of equity capital. Manage Sci 62: 347–367. doi: 10.1287/mnsc.2014.2101

|

| [4] |

Baker M, Stein JC, Wurgler J (2003) When Does the Market Matter? stock pricess and the Investment of Equity-Dependent Firms. Q J Econ 118: 969–1005. doi: 10.1162/00335530360698478

|

| [5] |

Baker M, Stein JC (2004) Market liquidity as a sentiment indicator. J Financ Mark 7: 271–299. doi: 10.1016/j.finmar.2003.11.005

|

| [6] |

Baker M, Wurgler J (2006) Investor sentiment and the cross-section of stock returns. J Financ 61: 1645–1680. doi: 10.1111/j.1540-6261.2006.00885.x

|

| [7] |

Baker M, Wurgler J (2007) Investor sentiment in the stock market. J Econ Perspect 21: 129–151. doi: 10.1257/jep.21.2.129

|

| [8] |

Baker M, Wurgler J, Yuan Y (2012) Global, local, and contagious investor sentiment. J Financ Econ 104: 272–287. doi: 10.1016/j.jfineco.2011.11.002

|

| [9] |

Barberis N, Shleifer A, Vishny R (1998) A Model of Investor Sentiment. J Financ Econ 49: 307–343. doi: 10.1016/S0304-405X(98)00027-0

|

| [10] |

Barberis N, Huang M (2008) Stocks as lotteries: The implications of probability weighting for security prices. Am Econ Rev 98: 2066–2100. doi: 10.1257/aer.98.5.2066

|

| [11] |

Barberis N, Mukherjee A, Wang B (2016) Prospect theory and stock returns: An empirical test. Rev Financ Stud 29: 3068–3107. doi: 10.1093/rfs/hhw049

|

| [12] |

Bathia D, Bredin D (2013) An examination of investor sentiment effect on G7 stock market returns. Eur J Financ 19: 909–937. doi: 10.1080/1351847X.2011.636834

|

| [13] |

Bollen J, Mao H, Zeng X (2011) Twitter mood predicts the stock market. J Comput Sci 2: 1–8. doi: 10.1016/j.jocs.2010.12.007

|

| [14] |

Chan K, Chan YC (2014) Price informativeness and stock return synchronicity: Evidence from the pricing of seasoned equity offerings. J Financ Econ 114: 36–53. doi: 10.1016/j.jfineco.2014.07.002

|

| [15] | Chen YW, Chou RK, Lin CB (2019) Investor sentiment, SEO market timing, and stock prices performance. Int J Financ Stud 51: 28–43. |

| [16] |

Chen R, Yu J, Jin C (2019) Internet finance investor sentiment and return comovement. Pac-Basin Financ J 56: 151–161. doi: 10.1016/j.pacfin.2019.05.010

|

| [17] | Choi KH, Yoon SM (2020) Investor Sentiment and Herding Behavior in the Korean Stock Market. Int J Financ Stud 8: 34. |

| [18] | Chung SL, Hung CH, Yeh CY (2012) When does investor sentiment predict stock returns? J Empir Financ 19: 217–240. |

| [19] |

Clinton S, White JT, Woidtke T (2014) Differences in the information environment prior to seasoned equity offerings under relaxed disclosure regulation. J Account Econ 58: 59–78. doi: 10.1016/j.jacceco.2014.05.002

|

| [20] | Donadelli M, Kizys R, Riedel M (2017) Dangerous infectious diseases: Bad news for main street, good news for wall street? J Financ Mark 35: 84–103. |

| [21] |

Ebert S, Strack P (2015) Until the Bitter End: On Prospect Theory in a Dynamic Context. Am Econ Rev 105: 1618–1633. doi: 10.1257/aer.20130896

|

| [22] |

Fama EF, French KR (1993) Common risk factors in the returns on stocks and bonds. J Financ Econ 33: 3–56. doi: 10.1016/0304-405X(93)90023-5

|

| [23] |

Fama E, French K (1992) The Cross-section of Expected Stock Returns. J Financ 47: 427–466. doi: 10.1111/j.1540-6261.1992.tb04398.x

|

| [24] |

Fama EF, French KR (2015) A five-factor asset pricing model. J Financ Econ 116: 1–22. doi: 10.1016/j.jfineco.2014.10.010

|

| [25] |

Fisher KL, Statman M (2006) Market timing in regressions and reality. J Financ Res 29: 293–304. doi: 10.1111/j.1475-6803.2006.00179.x

|

| [26] |

Frazzini A, Lamont OA (2008) Dumb Money: Mutual Fund Flows and the Cross-Section of Stock Returns. J Financ Econ 88: 299–322. doi: 10.1016/j.jfineco.2007.07.001

|

| [27] |

Frugier A (2016) Returns, volatility and investor sentiment: Evidence from European stock markets. Res Int Bus Financ 38: 45–55. doi: 10.1016/j.ribaf.2016.03.007

|

| [28] |

Gerard B, Nanda V (1993) Trading and manipulation around seasoned equity offerings. J Financ 48: 213–245. doi: 10.1111/j.1540-6261.1993.tb04707.x

|

| [29] |

Griffith J, Najand M, Shen J (2020) Emotions in the stock market. J Behav Financ 21: 42–56. doi: 10.1080/15427560.2019.1588275

|

| [30] |

Han X, Li Y (2017) Can investor sentiment be a momentum time-series predictor? Evidence from China. J Empir Financ 42: 212–239. doi: 10.1016/j.jempfin.2017.04.001

|

| [31] |

Hao Y, Chou RK, Ko KC, et al. (2018) The 52-week high, momentum, and investor sentiment. Int Rev Financ Anal 57: 167–183. doi: 10.1016/j.irfa.2018.01.014

|

| [32] |

He Y, Wang J, Wei KJ (2014) A comprehensive study of liquidity before and after SEOs and SEO underpricing. J Financ Mark 20: 61–78. doi: 10.1016/j.finmar.2014.03.004

|

| [33] |

Hertzel MG, Smith RL (1993) Market discounts and shareholder gains for placing equity privately. J Financ 48: 459–485. doi: 10.1111/j.1540-6261.1993.tb04723.x

|

| [34] |

Hirshleifer D, Shumway T (2003) Good day sunshine: Stock returns and the weather. J Financ 58: 1009–1032. doi: 10.1111/1540-6261.00556

|

| [35] | Hong Y, Li Y (2020) Housing Prices and Investor Sentiment Dynamics: Evidence from China using a wavelet approach. Financ Res Lett 35: 101300. |

| [36] |

Huang H, Jin G, Chen J (2016) Investor sentiment, property nature and corporate investment efficiency. China Financ Rev Int 6: 56–76. doi: 10.1108/CFRI-09-2015-0123

|

| [37] |

Huang H, Li R, Bai Y (2019) Investor sentiment, market competition and trade credit supply. China Financ Rev Int 9: 284–306. doi: 10.1108/CFRI-07-2018-0060

|

| [38] |

Huang Y, Uchida K, Zha DL (2016) Market timing of seasoned equity offerings with long regulative process. J Corp Financ 39: 278–294. doi: 10.1016/j.jcorpfin.2016.05.001

|

| [39] |

Hung PH (2016) Investor sentiment, order submission, and investment performance on the Taiwan Stock Exchange. Pac-Basin Financ J 39: 124–140. doi: 10.1016/j.pacfin.2016.06.005

|

| [40] |

Joseph K, Wintoki MB, Zhang ZL (2011) Forecasting abnormal stock returns and trading volume using investor sentiment: Evidence from online search. Int J Forecasting 27: 1116–1127. doi: 10.1016/j.ijforecast.2010.11.001

|

| [41] |

Kahneman D, Tversky A (1979) Prospect theory: An analysis of decision making under risk. Econometrica 47: 263–291. doi: 10.2307/1914185

|

| [42] | Kaplanski G, Levy H (2010a) Exploitable predictable irrationality: The FIFA world cup effect on the U.S. stock market. J Financ Quant Anal 45: 535–553. |

| [43] |

Kaplanski G, Levy H (2010b) Sentiment and stock pricess: The case of aviation distasters. J Financ Econ 95: 174–201. doi: 10.1016/j.jfineco.2009.10.002

|

| [44] |

Kaplanski G, Levy H (2014) Sentiment, irrationality and market efficiency: The case of the 2010 FIFA World Cup. J Behav Exp Econ 49: 35–43. doi: 10.1016/j.socec.2014.02.007

|

| [45] |

Kim JS, Ryu D, Seo SW (2015) Investor Sentiment and Return Predictability of Disagreement. J Bank Financ 42: 166–178. doi: 10.1016/j.jbankfin.2014.01.017

|

| [46] |

Kima B, Suhb S (2018) Sentiment-based Momentum Strategy. Int Rev Financ Anal 58: 52–68. doi: 10.1016/j.irfa.2018.04.004

|

| [47] |

Kothari SP, Shanken J (1997) Book-to-market, Dividend Yield, and Expected Market Returns: A Time Series Analysis. J Financ Econ 44: 169–203. doi: 10.1016/S0304-405X(97)00002-0

|

| [48] |

Lakonishok J, Shleifer A, Vishny RW (1994) Contrarian Investment, Extrapolation and Risk. J Financ 49: 1541–1578. doi: 10.1111/j.1540-6261.1994.tb04772.x

|

| [49] | Li Y, Ran J (2020) Investor Sentiment and stock prices Premium Validation with Siamese Twins from China. J Multinatl Financ Manage, 100655. |

| [50] |

Li Y, Yang L (2013) Prospect Theory, the Disposition Effect, and Asset Prices. J Financ Econ 107: 715–739. doi: 10.1016/j.jfineco.2012.11.002

|

| [51] |

López-Cabarcos MÁ, Pérez-Pico AM, Vázquez-Rodríguez P, et al. (2020) Investor sentiment in the theoretical field of behavioural finance. Econ Res-Ekonomska Istraživanja 33: 2101–2119. doi: 10.1080/1331677X.2018.1559748

|

| [52] |

Luo CQ, Ouyang ZS (2014) Estimating IPO Pricing Efficiency by Bayesian Stochastic Frontier Analysis: the ChiNext Market Case. Econ Model 40:152–157. doi: 10.1016/j.econmod.2014.03.030

|

| [53] |

Maqsood H, Mehmood I, Maqsood M, et al. (2020) A local and global event sentiment based efficient stock exchange forecasting using deep learning. Int J Inf Manage 50: 432–451. doi: 10.1016/j.ijinfomgt.2019.07.011

|

| [54] |

McGurk Z, Nowak A, Hall JC (2020) Stock returns and investor sentiment: textual analysis and social media. J Econ Financ 44: 458–485. doi: 10.1007/s12197-019-09494-4

|

| [55] |

Ni ZX, Wang DZ, Xue WJ (2015) Investor sentiment and its nonlinear effect on stock returns-New evidence from the Chinese stock market based on panel quantile regression model. Econ Model 50: 266–274. doi: 10.1016/j.econmod.2015.07.007

|

| [56] | Novy-Marx R (2012) Is momentum really momentum? J Financ Econ 103: 429–453. |

| [57] | Piñeiro-Chousa J, López-Cabarcos MA, Pérez-Pico AM, et al. (2018) Does social network sentiment influence the relationship between the S & P 500 and gold returns? Int Rev Financ Anal 57: 57–64. |

| [58] |

Renault T (2017) Intraday online investor sentiment and return patterns in the US stock market. J Bank Financ 84: 25–40. doi: 10.1016/j.jbankfin.2017.07.002

|

| [59] | Shi J, Yu C, Guo S, et al. (2020) Market effects of private equity placement: Evidence from Chinese equity and bond markets. North Am J Econ Financ 53: 101214. |

| [60] |

Smales LA (2014) News sentiment and the investor fear gauge. Financ Res Lett 11: 122–130. doi: 10.1016/j.frl.2013.07.003

|

| [61] |

Sprenger TO, Tumasjan A, Sandner PG, et al. (2014) Tweets and trades: The information content of stock microblogs. Eur Financ Manage 20: 926–957. doi: 10.1111/j.1468-036X.2013.12007.x

|

| [62] |

Wu PC, Liu SY, Chen CY (2016) Re-examining risk premiums in the Fama–French model: The role of investor sentiment. North Am J Econ Financ 36: 154–171. doi: 10.1016/j.najef.2015.12.002

|

| [63] | Yang C, Wu H (2019) Chasing investor sentiment in stock market. North Am J Econ Financ 50: 100975. |

| [64] | Yang C, Yan W (2011) Dose high sentiment cause negative excess return? Int J Digital Content Technol Appl 5: 211–217. |

| [65] |

Yang CP, Zhou LY (2016) Individual stock crowded trades, individual stock investor sentiment and excess returns. North Am J Econ Financ 38: 39–53. doi: 10.1016/j.najef.2016.06.001

|

| [66] |

Zeng H (2020) Volatility Modelling of Chinese Stock Market Monthly Return and Investor Sentiment Using Multivariate GARCH Models. Int J Account Financ Rev 5: 123–133. doi: 10.46281/ijafr.v5i1.643

|

| [67] |

Zhao YF, Xia XP, Tang XX, et al. (2015) Private placements, cash dividends and interests transfer: Empirical evidence from Chinese listed firms. Int Rev Econ Financ 36: 107–118. doi: 10.1016/j.iref.2014.11.011

|

| [68] |

Zhou L, Yang C (2019) Stochastic investor sentiment, crowdedness and deviation of asset prices from fundamentals. Econ Model 79: 130–140. doi: 10.1016/j.econmod.2018.10.008

|

| [69] |

Zhu B, Niu F (2016) Investor sentiment, accounting information and stock prices: Evidence from China. Pac-Basin Financ J 38: 125–134. doi: 10.1016/j.pacfin.2016.03.010

|

| [70] |

Wang L, Zhang Z, Wang Y (2015) A prospect theory-based interval dynamic reference point method for emergency decision making. Expert Syst Appl 42: 9379–9388. doi: 10.1016/j.eswa.2015.07.056

|

| [71] | Wang W (2020) Institutional investor sentiment, beta, and stock returns. Financ Res Lett 37: 101374. |

| [72] |

Werner K, Zank H (2019) A revealed reference point for prospect theory. Econ Theory 67: 731–773. doi: 10.1007/s00199-017-1096-2

|

| [73] |

Wang T, Li H, Zhang L, et al. (2020) A three-way decision model based on cumulative prospect theory. Inf Sci 519: 74–92. doi: 10.1016/j.ins.2020.01.030

|

Figures(3) / Tables(9)

Changqing Luo, Zijing Li, Lan Liu. Does investor sentiment affect stock pricing? Evidence from seasoned equity offerings in China[J]. National Accounting Review, 2021, 3(1): 115-136. doi: 10.3934/NAR.2021006

DownLoad:

DownLoad: