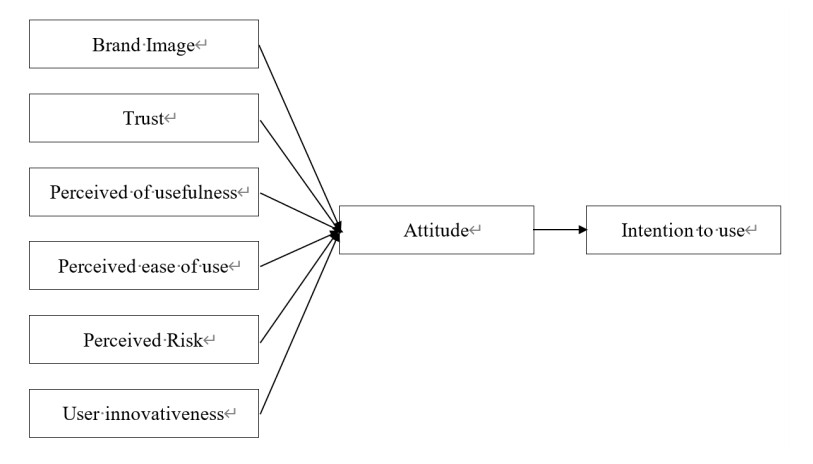

In recent years, the number of fintech startups has increased substantially, especially those that offer financial services in areas considered as traditional advantage of commercial banks such as payment, deposit or lending services. This paper examines the cooperation in the provision of financial services between banks and Fintech from consumers' perspective, which is the customers' adoption of financial services offered by the partnership between banks and Fintechs. The study employs SEM utilizing data of 234 customers using financial services in Vietnam to identify the factors influence their behaviors and intention to use financial services offered by banks and fintechs partnerships. The findings indicate that perceived usefulness, brand image, user innovativeness and trust have positive effects on customers' attitude and consequently on their intention to use. However, there is no evidence regarding the impact of perceived ease of use and perceived risks on behavior and intention to use of customers. The findings also provide more evidence on the factors that influence the intention of customers' technology acceptance in the traditional Technology Acceptance Model (TAM).

Citation: Yen H. Hoang, Duong T.T. Nguyen, Linh H.T. Tran, Nhung T.H. Nguyen, Ngoc B. Vu. Customers' adoption of financial services offered by banks and fintechs partnerships: evidence of a transitional economy[J]. Data Science in Finance and Economics, 2021, 1(1): 77-95. doi: 10.3934/DSFE.2021005

In recent years, the number of fintech startups has increased substantially, especially those that offer financial services in areas considered as traditional advantage of commercial banks such as payment, deposit or lending services. This paper examines the cooperation in the provision of financial services between banks and Fintech from consumers' perspective, which is the customers' adoption of financial services offered by the partnership between banks and Fintechs. The study employs SEM utilizing data of 234 customers using financial services in Vietnam to identify the factors influence their behaviors and intention to use financial services offered by banks and fintechs partnerships. The findings indicate that perceived usefulness, brand image, user innovativeness and trust have positive effects on customers' attitude and consequently on their intention to use. However, there is no evidence regarding the impact of perceived ease of use and perceived risks on behavior and intention to use of customers. The findings also provide more evidence on the factors that influence the intention of customers' technology acceptance in the traditional Technology Acceptance Model (TAM).

| [1] |

Abbad MM (2013) E-banking in Jordan. Behav Inform Technol 32: 681-694. doi: 10.1080/0144929X.2011.586725

|

| [2] | Aboelmaged MGG, Gebba TR (2013) Mobile banking adoption: an examination of technology acceptance model and theory of planned behavior. Int J Bus Res Dev 2: 35-50. |

| [3] |

Ajzen I (1991) The theory of planned behaviour. Organ Behav Hum Decis Process 50: 179-211. doi: 10.1016/0749-5978(91)90020-T

|

| [4] |

Ajzen I (2011) The theory of planned behaviour: reactions and reflections. Psychol Health 26: 1113-1127. doi: 10.1080/08870446.2011.613995

|

| [5] | Alaeddin O, Altounjy R (2018) Trust, technology awareness and satisfaction effect into the intention to use cryptocurrency among generation Z in Malaysia. Int J Eng Technol 7: 8-10. |

| [6] |

Aldás-Manzano J, Lassala-Navarre C, Ruiz-Mafe C, et al. (2009) The role of consumer innovativeness and perceived risk in online banking usage. Int J Bank Mark 27: 53-75. doi: 10.1108/02652320910928245

|

| [7] | Anderson JC, Gerbing DW (1988) Structural equation modeling in practice: A review and recommended two-step approach. Psychol Bull 103: 411. |

| [8] | Azjen I, Fishbein M (1980) Understanding attitudes and predicting social behavior, Englewood Cliffs, NJ: Prentice-Hall. |

| [9] |

Bailey AA, Pentina I, Mishra AS, et al. (2017) Mobile payments adoption by US consumers: an extended TAM. Int J Retail Distrib Manage 45: 626-640. doi: 10.1108/IJRDM-08-2016-0144

|

| [10] | Bansal S, Bansal A, Blake MB (2010) Trust-based dynamic web service composition using social network analysis, 2010 IEEE International Workshop on: Business Applications of Social Network Analysis (BASNA), 1-8. |

| [11] |

Bentler PM, Bonett DG (1980) Significance tests and goodness of fit in the analysis of covariance structures. Psychol Bull 88: 588-606. doi: 10.1037/0033-2909.88.3.588

|

| [12] | Carmines EG, McIver JP (1983) An introduction to the analysis of models with unobserved variables. Political Methodol 9: 51-102. |

| [13] | Cham TH, Low SC, Lim CS, et al. (2018) Preliminary study on consumer attitude towards fintech products and services in Malaysia. Int J Eng Technol 7: 166-169. |

| [14] | Chang YP, Lan LY, Zhu DH (2018) Understanding the intention to continue use a mobile payment. Int J Bus Inform 12: 363-390. |

| [15] |

Chau PY, Hu PJ (2002) Examining a model of information technology acceptance by individual professionals: an exploratory study. J Manage Inform Syst 18: 191-229. doi: 10.1080/07421222.2002.11045699

|

| [16] |

Chen JF, Chang JF, Kao CW, et al. (2016) Integrating ISSM into TAM to enhance digital library services. Electron Lib 34: 58-73. doi: 10.1108/EL-01-2014-0016

|

| [17] |

Cheng TE, Lam DY, Yeung AC (2006) Adoption of internet banking: an empirical study in Hong Kong. Decis Support Syst 42: 1558-1572. doi: 10.1016/j.dss.2006.01.002

|

| [18] |

Chong A, Ooi K, Lin B, et al. (2010) Online banking adoption: an empirical analysis. Int J Bank Mark 28: 267-287. doi: 10.1108/02652321011054963

|

| [19] |

Chua CJ, Lim CS, Aye AK (2019) Factors affecting the consumer acceptance towards fintech products and services in Malaysia. Int J Asian Soc Sci 9: 59-65. doi: 10.18488/journal.1.2019.91.59.65

|

| [20] | Chuang LM, Liu CC, Kao HK (2016) The adoption of fintech service: TAM perspective. Int J Manage Admin Sci 3: 1-15. |

| [21] | Chuen DLK (2015) Handbook of Digital Currency: Bitcoin, Innovation, Financial Instruments, and Big Data, Academic Press. |

| [22] |

Datta PA (2011) Preliminary study of ecommerce adoption in developing countries. Inform Syst J 21: 3-32. doi: 10.1111/j.1365-2575.2009.00344.x

|

| [23] |

Davis FD, Bagozzi RP, Warshaw PR (1989) User acceptance of computer technology: a comparison of two theoretical models. Manage Sci 35: 982-1003. doi: 10.1287/mnsc.35.8.982

|

| [24] |

Demoulin NTM, Djelassi S (2016) An integrated model of self-service technology (SST) usage in a retail context. Int J Retail Distrib Manage 44: 540-559. doi: 10.1108/IJRDM-08-2015-0122

|

| [25] |

Devlin JF (1997) Adding value to retail financial services. J Mark Pract 3: 251-267. doi: 10.1108/EUM0000000004461

|

| [26] |

Donner J, Tellez CA (2008) Mobile banking and economic development: Linking adoption, impact, and use. Asian J Commun 18: 318-332. doi: 10.1080/01292980802344190

|

| [27] |

Dulcic Z, Pavlic D, Silic I (2012) Evaluating the intended use of decision support system (DSS) by applying technology acceptance model (TAM) in business organizations in Croatia. Procedia-Soc Behav Sci 58: 1565-1575. doi: 10.1016/j.sbspro.2012.09.1143

|

| [28] | 2020 Fintech Vietnam Report and Startup Map: Fintech startups Tripled since 2017, 2020. Fintech Singapore, 2020. Available from: https://fintechnews.sg/45354/vietnam/2020-fintech-vietnam-report-and-startup-map/. |

| [29] | Fishbein M, Ajzen I (1977) Belief, attitude, intention, and behavior: an introduction to theory and research. Contemp Sociol 6 : 244. |

| [30] |

Forsythe SM, Shi B (2003) Consumer patronage and risk perceptions in Internet shopping. J Bus Res 56: 867-875. doi: 10.1016/S0148-2963(01)00273-9

|

| [31] | FSB (2019) Financial Stability Implications from Fintech. Financial Stability Board. |

| [32] | Global Innovation Index 2020. World Intellectual Property Organization, 2020. Available from: https://www.wipo.int/global_innovation_index/en/2020/. |

| [33] |

Grabner-Kräuter S, Faullant R (2008) Consumer acceptance of Internet banking: the influence of internet trust. Int J Bank Mark 26: 483-504. doi: 10.1108/02652320810913855

|

| [34] | Group VMW (2018) Report "Application of Financial Technology (Fintech) in Microfinance activities towards Universal Finance in Vietnam", Vietnam. |

| [35] |

Gupta A, Arora N (2017) Consumer adoption of m-banking: a behavioral reasoning theory perspective. Int J Bank Mark 35: 733-747. doi: 10.1108/IJBM-11-2016-0162

|

| [36] | Ha H (2004) Factors influencing consumer perceptions of brand trust online J Prod Brand Manage 13: 329-342. |

| [37] | Hair JF (1998) Multivariate data analysis, Upper Saddle River, N.J., Prentice Hall. |

| [38] |

Halilovic S, Cicic M (2013) Antecedents of information systems user behavior-extended expectation-confirmation model. Behav Inform Technol 32: 359-370. doi: 10.1080/0144929X.2011.554575

|

| [39] |

Hamidi H, Safareeyeh M (2019) A model to analyze the effect of mobile banking adoption on customer interaction and satisfaction: a case study of m-banking in Iran. Telematics Inform 38: 166-181. doi: 10.1016/j.tele.2018.09.008

|

| [40] |

Hanafizadeh P, Behboudi M, Koshksaray AA, et al. (2014) Mobile-banking adoption by Iranian bank clients. Telematics Inform 31: 62-78. doi: 10.1016/j.tele.2012.11.001

|

| [41] | Hu Z, Ding S, Li S, et al. (2019) Adoption intention of fintech services for bank users: An empirical examination with an extended technology acceptance model. Symmetry 11: 340. |

| [42] |

Huh HJ, Kim TT, Law R (2009) A comparison of competing theoretical models for understanding acceptance behavior of information systems in upscale hotels. Int J Hosp Manage 28: 121-134. doi: 10.1016/j.ijhm.2008.06.004

|

| [43] | Jiwasiddi A, Adhikara C, Adam M, et al. (2019) Attitude toward using Fintech among Millennials. The 1st Workshop on Multimedia Education, Learning, Assessment and its Implementation in Game and Gamification in conjunction with COMDEV 2018, European Alliance for Innovation (EAI). |

| [44] | Jonker N (2019) What drives the adoption of crypto-payments by online retailers? Electron Comm Res Appl 35: 100848. |

| [45] |

Kapoor K, Dwivedi Y, Piercy NC, et al. (2014) RFID integrated systems in libraries: extending TAM model for empirically examining the use. J Enterp Inform Manage 27: 731-758. doi: 10.1108/JEIM-10-2013-0079

|

| [46] |

Kesharwani A, Singh Bisht S (2012) The impact of trust and perceived risk on internet banking adoption in India: An extension of technology acceptance model. Int J Bank Mark 30: 303-322. doi: 10.1108/02652321211236923

|

| [47] |

Khedmatgozar HR, Shahnazi A (2018) The role of dimensions of perceived risk in adoption of corporate internet banking by customers in Iran. Electron Comm Res 18: 389-412. doi: 10.1007/s10660-017-9253-z

|

| [48] | Khodabandeh A, Lindh C (2020) The importance of brands, commitment, and influencers on purchase intent in the context of online relationships. Australas Mark J. |

| [49] |

Kim S (2012) Factors affecting the use of social software: TAM perspectives. Electron Lib 30: 690-706. doi: 10.1108/02640471211275729

|

| [50] |

Kim YG, Woo E (2016) Consumer acceptance of a quick response (QR) code for the food traceability system: application of an extended technology acceptance model (TAM). Food Res Int 85: 266-272. doi: 10.1016/j.foodres.2016.05.002

|

| [51] |

Kim YJ, Park YJ, Choi J, et al. (2015) An empirical study on the adoption of "fintech" service: focused on mobile payment services. Adv Sci Technol Lett 114: 136-140. doi: 10.14257/astl.2015.114.26

|

| [52] |

Koksal MH (2016) The intentions of Lebanese consumers to adopt mobile banking. Int J Bank Mark 34: 327-346. doi: 10.1108/IJBM-03-2015-0025

|

| [53] |

Koufaris M (2002) Applying the technology acceptance model and flow theory to online consumer behavior. Inform Syst Res 13: 205-223. doi: 10.1287/isre.13.2.205.83

|

| [54] |

Lee DY, Lehto MR (2013) User acceptance of YouTube for procedural learning: an extension of the technology acceptance model. Comput Educ 61: 193-208. doi: 10.1016/j.compedu.2012.10.001

|

| [55] |

Lee MKO, Turban E (2001) A trust model for consumer internet shopping. Int J Electron Comm 6: 75-91. doi: 10.1080/10864415.2001.11044227

|

| [56] |

Leicht T, Chtourou A, Youssef KB (2018) Consumer innovativeness and intentioned autonomous car adoption. J High Technol Manage Res 29: 1-11. doi: 10.1016/j.hitech.2018.04.001

|

| [57] |

Liebermann Y, Stashevsky S (2002) Perceived risks as barriers to Internet and e-commerce usage. Qual Mark Res 5: 291-300. doi: 10.1108/13522750210443245

|

| [58] |

Lien NTK, Thi Doan TT, Bui TN (2020) Fintech and banking: evidence from Vietnam. J Asian Financ Econ Bus 7: 419-426. doi: 10.13106/jafeb.2020.vol7.no9.419

|

| [59] |

Lin WR, Wang YH, Hung YM (2020) Analyzing the factors influencing adoption intention of internet banking: Applying DEMATEL-ANP-SEM approach. PlOS ONE 15: e0227852. doi: 10.1371/journal.pone.0227852

|

| [60] |

López-Nicolás C, Molina-Castillo FJ, Bouwman H (2008) An assessment of advanced mobile services acceptance: Contributions from TAM and diffusion theory models. Inform Manage 45: 359-364. doi: 10.1016/j.im.2008.05.001

|

| [61] |

Lockett A, Littler D (1997) The adoption of direct banking services. J Mark Manage 13: 791-811. doi: 10.1080/0267257X.1997.9964512

|

| [62] |

Malaquias RF, Hwang Y (2016) An empirical study on trust in mobile banking: A developing country perspective. Comput Hum Behav 54: 453-461. doi: 10.1016/j.chb.2015.08.039

|

| [63] |

Mallat N, Rossi M, Tuunainen VK (2009) The impact of use context on mobile services acceptance: The case of mobile ticketing. Inform Manage 46: 190-195. doi: 10.1016/j.im.2008.11.008

|

| [64] |

Manrai LA, Manrai AK (2007) A field study of customers' switching behavior for bank services. J Retailing Consum Serv 14: 208-215. doi: 10.1016/j.jretconser.2006.09.005

|

| [65] |

Marakarkandy B, Yajnik N, Dasgupta C (2017) Enabling internet banking adoption: an empirical examination with an augmented technology acceptance model (Tam). J Enterp Inform Manage 30: 263-294. doi: 10.1108/JEIM-10-2015-0094

|

| [66] |

Martins C, Oliveira T, Popovič A (2014) Understanding the Internet banking adoption: A unified theory of acceptance and use of technology and perceived risk application. Int J Inform Manage 34: 1-13. doi: 10.1016/j.ijinfomgt.2013.06.002

|

| [67] |

McKnight DH, Chervany NL (2001) What trust means in e-commerce customer relationships: An interdisciplinary conceptual typology. Int J Electron Comm 6: 35-59. doi: 10.1080/10864415.2001.11044235

|

| [68] |

Meyliana M, Fernando E, Surjandy S (2019) The influence of perceived risk and trust in adoption of fintech services in Indonesia. CommIT J 13: 31-37. doi: 10.21512/commit.v13i1.5708

|

| [69] | Miller K (2005) Communication theories, USA: Macgraw-Hill. |

| [70] |

Moon JW, Kim YG (2001) Extending the TAM for a World-Wide-Web context. Inform Manage 38: 217-230. doi: 10.1016/S0378-7206(00)00061-6

|

| [71] | Munoz-Leiva F, Climent-Climent S, Liébana-Cabanillas F (2017) Determinants of intention to use the mobile banking apps: An extension of the classic TAM model. Span J Mark-ESIC 21: 25-38. |

| [72] |

Ng AW, Kwok BKB (2017) Emergence of Fintech and cybersecurity in a global financial centre: Strategic approach by a regulator. J Financ Regul Compliance 25: 422-434. doi: 10.1108/JFRC-01-2017-0013

|

| [73] |

Olson JM, Zanna MP (1993) Attitudes and attitude change. Annu Rev Psycho 44: 117-154. doi: 10.1146/annurev.ps.44.020193.001001

|

| [74] |

Patel KJ, Patel HJ (2018) Adoption of internet banking services in Gujarat: An extension of TAM with perceived security and social influence. Int J Bank Mark 36: 147-169. doi: 10.1108/IJBM-08-2016-0104

|

| [75] | Pauline R (2003) Inter-Organizational-Trust in Business to Business E-Commerce: A Case Study in Customs Clearance. J Glob Inform Manage 11: 1-19. |

| [76] |

Phan DTT, Nguyen TTH, Bui TA (2019) Going beyond border? Intention to use international bank cards in Vietnam. J Asian Financ Econ Bus 6: 315-325. doi: 10.13106/jafeb.2019.vol6.no3.315

|

| [77] |

Qiu LY, Li D (2008) Applying TAM in B2C E-commerce research: An extended model. Tsinghua Sci Technol 13: 265-272. doi: 10.1016/S1007-0214(08)70043-9

|

| [78] | Ratnasingam P (2003) Inter-organizational-trust in business to business e-commerce: A case study in customs clearance. J Glob Inform Manage 11: 1-19. |

| [79] | Ratten V (2014) A US-China comparative study of cloud computing adoption behavior: The role of consumer innovativeness, performance expectations and social influence. J Entrepreneurship Emerg Econ 6: 53-71. |

| [80] |

Riquelme EH, Rios RE (2010) The moderating effect of gender in the adoption of mobile banking. Int J Bank Mark 28: 328-341. doi: 10.1108/02652321011064872

|

| [81] | Romānova I, Kudinska M (2016) Banking and fintech: A challenge or opportunity? Contemp Stud Econ Financ Anal 98: 21-35. |

| [82] |

Ruparelia N, White L, Hughes K (2010) Drivers of brand trust in internet retailing. J Prod Brand Manage 19: 250-260. doi: 10.1108/10610421011059577

|

| [83] |

Sánchez-Torres JA, Canada FJA, Sandoval AV, et al. (2018) E-banking in Colombia: factors favouring its acceptance, online trust and government support. Int J Bank Mark 36: 170-183. doi: 10.1108/IJBM-10-2016-0145

|

| [84] |

Shaikh IM, Qureshi MA, Noordin K, et al. (2020) Acceptance of Islamic financial technology (FinTech) banking services by Malaysian users: an extension of technology acceptance model. Foresight 22: 367-383. doi: 10.1108/FS-12-2019-0105

|

| [85] | Smith AA, Synowka DP, Smith AD (2014) E-commerce quality and adoptive elements of e-ticketing for entertainment and sporting events. Int J Bus Inform Syst 15: 450-487. |

| [86] |

Steiger JH (1990) Structural model evaluation and modification: an interval estimation approach. Multivar Behav Res 25: 173-180. doi: 10.1207/s15327906mbr2502_4

|

| [87] |

Stewart H, Jürjens J (2018) Data security and consumer trust in FinTech innovation in Germany. Inform Comput Secur 26: 109-128. doi: 10.1108/ICS-06-2017-0039

|

| [88] |

Stocchi L, Michaelidou N, Micevski M (2019) Drivers and outcomes of branded mobile app usage intention. J Prod Brand Manage 28: 28-49. doi: 10.1108/JPBM-02-2017-1436

|

| [89] |

Teo T, Lee BC, Chai CS, et al. (2009) Assessing the intention to use technology among pre-service teachers in Singapore and Malaysia: A multigroup invariance analysis of the Technology Acceptance Model (TAM). Comput Educ 53: 1000-1009. doi: 10.1016/j.compedu.2009.05.017

|

| [90] |

Thakur R, Srivastava M (2015) A study on the impact of consumer risk perception and innovativeness on online shopping in India. Int J Retail Distrib Manage 43: 148-166. doi: 10.1108/IJRDM-06-2013-0128

|

| [91] |

Venkatesh V, Davis FD (2000) A theoretical extension of the technology acceptance model: Four longitudinal field studies. Manage Sci 46: 186-204. doi: 10.1287/mnsc.46.2.186.11926

|

| [92] |

Venkatesh V, Morris MG, Davis GB, et al. (2003) User acceptance of information technology: toward a unified view. MIS Quart 27: 425-478. doi: 10.2307/30036540

|

| [93] | Vietnam Fintech Report 2020. Fintech Singapore, 2020. Available from: https://fintechnews.sg/wp-content/uploads/2020/11/Vietnam-Fintech-Report-2020.pdf. |

| [94] | Vietnam Microfinance Working Group. Annual Report, 2018. Available from: https://microfinance.vn/wp-content/uploads/2019/06/gg.pdf. |

| [95] |

Wallace LG, Sheetz SD (2014) The adoption of software measures: A technology acceptance model (TAM) perspective. Inform Manage 51: 249-259. doi: 10.1016/j.im.2013.12.003

|

| [96] |

Wang WT, Li HM (2012) Factors influencing mobile services adoption: A brand-equity perspective. Internet Res 22: 142-179. doi: 10.1108/10662241211214548

|

| [97] |

Wang Y, Wang Y, Lin H, et al. (2003) Determinants of user acceptance of Internet banking: An empirical study. Int J Serv Ind Manage 14: 501-519. doi: 10.1108/09564230310500192

|

| [98] |

Wonglimpiyarat J (2017) FinTech banking industry: a systemic approach. Foresight 19: 590-603. doi: 10.1108/FS-07-2017-0026

|

| [99] |

Wu JH, Wang SC (2005) What drives mobile commerce?: An empirical evaluation of the revised technology acceptance model. Inform Manage 42: 719-729. doi: 10.1016/j.im.2004.07.001

|

| [100] |

Yang HD, Yoo Y (2004) It's all about attitude: revisiting the technology acceptance model. Decis Support Syst 38: 19-31. doi: 10.1016/S0167-9236(03)00062-9

|

| [101] | Zhang T, Lu C, Kizildag M (2018) Banking "on-the-go": examining consumers' adoption of mobile banking services. Int J Qual Serv Sci 10: 279-295. |

| [102] | Zhou L, Yang D (2011) An enterprise mobile e-business system model based on pushmail, 2011 IEEE 2nd International Conference on Software Engineering and Service Science, 730-733. |

DSFE-01-01-005-s001.pdf DSFE-01-01-005-s001.pdf |

|

Figures(1) / Tables(3)

Yen H. Hoang, Duong T.T. Nguyen, Linh H.T. Tran, Nhung T.H. Nguyen, Ngoc B. Vu. Customers' adoption of financial services offered by banks and fintechs partnerships: evidence of a transitional economy[J]. Data Science in Finance and Economics, 2021, 1(1): 77-95. doi: 10.3934/DSFE.2021005

DownLoad:

DownLoad: