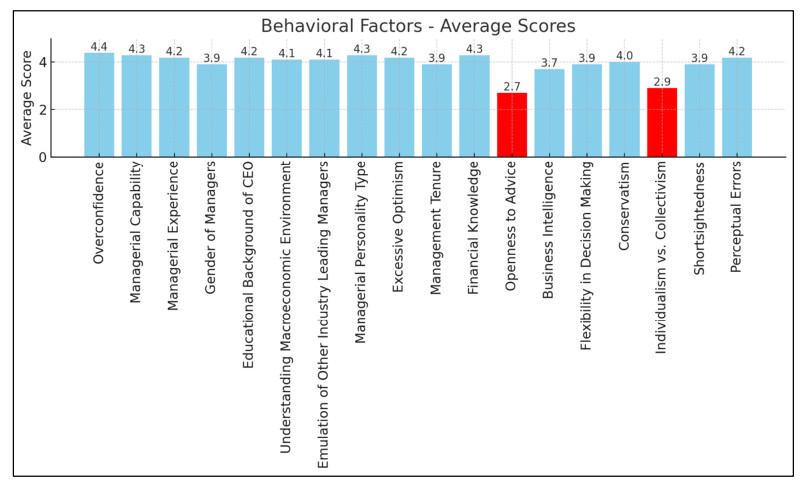

Our objective of this research was to identify and rank the factors that influence the capital structure decisions of Iranian companies, focusing on the role of behavioral elements as intermediaries. To construct the research framework, we employed a two-phase, mixed-method design that encompassed both qualitative insights and quantitative methodologies. In the qualitative phase, experts in the capital market are consulted using a snowball sampling technique, and key research factors were identified through coding analysis. Subsequently, for the quantitative phase, managers from leading Tehran Stock Exchange–listed companies were surveyed to prioritize the model components via the Analytic Hierarchy Process (AHP). Moreover, Factor Analysis with expert feedback using structural equation modeling (SEM) were performed in the model. Initially, we identified 63 concepts, later refined to 58 after expert consultation, and categorized them into behavioral, macroeconomic, political, socio-cultural, corporate characteristics, and governance factors. Quantitative analysis revealed that macroeconomic factors exhibit the highest influence (0.266), followed by behavioral factors (0.230), corporate governance (0.201), company-specific characteristics (0.141), political factors (0.103), and socio-cultural factors (0.059) in shaping financial structures. This research thus offers a more detailed examination of how behavioral biases and broader market conditions are converged to influence capital structure, underscoring the importance of integrating cognitive perspectives—particularly those of financial managers—into corporate decision-making processes. Future investigations can be benefited from integrating broader market data, such as share price movements, to further refine insights into the dynamic interplay of behavior and capital structure.

Citation: Ehsan Ahmadi, Parastoo Mohammadi, Farimah Mokhatab Rafei, Shib Sankar Sana. Behavioral factors and capital structure: identification and prioritization of influential factors[J]. Data Science in Finance and Economics, 2025, 5(1): 76-104. doi: 10.3934/DSFE.2025005

Our objective of this research was to identify and rank the factors that influence the capital structure decisions of Iranian companies, focusing on the role of behavioral elements as intermediaries. To construct the research framework, we employed a two-phase, mixed-method design that encompassed both qualitative insights and quantitative methodologies. In the qualitative phase, experts in the capital market are consulted using a snowball sampling technique, and key research factors were identified through coding analysis. Subsequently, for the quantitative phase, managers from leading Tehran Stock Exchange–listed companies were surveyed to prioritize the model components via the Analytic Hierarchy Process (AHP). Moreover, Factor Analysis with expert feedback using structural equation modeling (SEM) were performed in the model. Initially, we identified 63 concepts, later refined to 58 after expert consultation, and categorized them into behavioral, macroeconomic, political, socio-cultural, corporate characteristics, and governance factors. Quantitative analysis revealed that macroeconomic factors exhibit the highest influence (0.266), followed by behavioral factors (0.230), corporate governance (0.201), company-specific characteristics (0.141), political factors (0.103), and socio-cultural factors (0.059) in shaping financial structures. This research thus offers a more detailed examination of how behavioral biases and broader market conditions are converged to influence capital structure, underscoring the importance of integrating cognitive perspectives—particularly those of financial managers—into corporate decision-making processes. Future investigations can be benefited from integrating broader market data, such as share price movements, to further refine insights into the dynamic interplay of behavior and capital structure.

| [1] |

Ahmad M (2024) The role of cognitive heuristic-driven biases in investment management activities and market efficiency: a research synthesis. Int J of Emer Mark 19: 273-321. https://doi.org/10.1108/IJOEM-07-2020-0749 doi: 10.1108/IJOEM-07-2020-0749

|

| [2] |

Ah Mand A, Janor H, Abdul RR, Sarmidi T (2023) Herding behavior and stock market conditions. PSU Res Rev 7: 105-116. https://doi.org/10.1108/PRR-10-2020-0033 doi: 10.1108/PRR-10-2020-0033

|

| [3] |

Aibar-Guzmán B, García-Sánchez IM, Aibar-Guzmán C, et al. (2022) Sustainable product innovation in agri-food industry: Do ownership structure and capital structure matter? J Innov Knowl 7: 100160. https://doi.org/10.1016/j.jik.2021.100160 doi: 10.1016/j.jik.2021.100160

|

| [4] |

Al‐Zoubi HA, O’Sullivan JA, Al‐Maghyereh AI, et al. (2022) Disentangling sentiment from cyclicality in firm capital structure. ABACUS 59: 570-605. https://doi.org/10.1111/abac.12274 doi: 10.1111/abac.12274

|

| [5] |

Alves P, Couto EB, Francisco PM (2015) Board of directors' composition and capital structure. Res Int Bus Financ 35: 1–32. https://doi.org/10.1016/j.ribaf.2015.03.005 doi: 10.1016/j.ribaf.2015.03.005

|

| [6] |

Badheka GT, Pandya K (2022) Behavioural Capital Structure: A Systematic Literature Review on the Role of Psychological Factors in Determining the Capital Structure. Int J Financ Manag 12: 1–9. doi: 10.22495/rcgv6i4c1art13 doi: 10.22495/rcgv6i4c1art13

|

| [7] |

Banerjee S, Humphery-Jenner M, Nanda V (2018) Does CEO bias escalate repurchase activity? J Bank Financ 93: 105–126. https://doi.org/10.1016/j.jbankfin.2018.02.003 doi: 10.1016/j.jbankfin.2018.02.003

|

| [8] |

Barton SL, Gordon PJ (1988) Corporate strategy and capital structure. Strategic Manage J 9: 623–632. https://doi.org/10.1002/smj.4250090608 doi: 10.1002/smj.4250090608

|

| [9] |

Baker M, Wurgler J (2002) Market timing and capital structure. J Financ 57: 1–32. https://doi.org/10.1111/1540-6261.00414 doi: 10.1111/1540-6261.00414

|

| [10] | Bokpin GA(2010) Financial market development and corporate financing: evidence from emerging market economies. J of Eco Stud 37: 96-116. http://dx.doi.org/10.1108/01443581011012270 |

| [11] |

Bradley M, Jarrell GA, Kim EH (1984) On the existence of an optimal capital structure: Theory and evidence. J Financ 39: 857–878. https://doi.org/10.2307/2327950 doi: 10.2307/2327950

|

| [12] |

Çam İ, Özer G (2022) The influence of country governance on the capital structure and investment financing decisions of firms: An international investigation. Borsa Istanb Rev 22: 257–271. https://doi.org/10.1016/j.bir.2021.04.008 doi: 10.1016/j.bir.2021.04.008

|

| [13] |

Carrizosa R, Gaertner FB, Lynch D (2020) Debt and Taxes? The Effect of TCJA Interest Limitations on Capital Structure. Available at SSRN. http://dx.doi.org/10.2139/ssrn.3397285 doi: 10.2139/ssrn.3397285

|

| [14] |

Carrizosa RD, Gaertner FB, Lynch DP (2023) Debt and taxes? The effect of Tax Cuts & Jobs Act of 2017 interest limitations on capital structure. J Am Tax Assoc 45: 35–55. https://doi.org/10.2308/JATA-2021-010 doi: 10.2308/JATA-2021-010

|

| [15] |

Chauhan Y, Jaiswall M, Goyal V (2022) Does societal trust affect corporate capital structure? Emerg Mark Rev 51: 100845. https://doi.org/10.1016/j.ememar.2021.100845 doi: 10.1016/j.ememar.2021.100845

|

| [16] |

Choi PMS, Choi JH, Chung CY, et al. (2020) Corporate governance and capital structure: Evidence from sustainable institutional ownership. Sustainability 12: 4190. https://doi.org/10.3390/su12104190 doi: 10.3390/su12104190

|

| [17] |

Chua M, Ab Razak NH, Nassir AM, et al. (2022) Dynamic capital structure in Indonesia: does the education and experience of CEOs matter? Asia Pac Manag Rev 27: 58–68. https://doi.org/10.1016/j.apmrv.2021.05.003 doi: 10.1016/j.apmrv.2021.05.003

|

| [18] |

Costa DF, de Melo Carvalho F, de Melo Moreira BC, et al. (2017) Bibliometric analysis on the association between behavioral finance and decision making with cognitive biases such as overconfidence, anchoring effect and confirmation bias. Scientometrics 111: 1775–1799. https://doi.org/10.1007/s11192-017-2371-5 doi: 10.1007/s11192-017-2371-5

|

| [19] |

Danso A, Fosu S, Owusu‐Agyei S, et al. (2021) Capital structure revisited. Do crisis and competition matter in a Keiretsu corporate structure? Int J Financ Econ 26: 5073–5092. https://doi.org/10.1002/ijfe.2055 doi: 10.1002/ijfe.2055

|

| [20] | Faysal S, Salehi M, Moradi M (2020) Impact of corporate governance mechanisms on the cost of equity capital in emerging markets. J of Pub Affairs 21: e2166. 16 pages. https://doi.org/10.1002/pa.2166 |

| [21] |

Fama EF (1970) Efficient capital markets. J Financ 25: 383–417. https://doi.org/10.7208/9780226426983-007 doi: 10.7208/9780226426983-007

|

| [22] |

Fama EF, French KR (1998) Taxes, financing decisions, and firm value. J Financ 53: 819–843. https://doi.org/10.1111/0022-1082.00036 doi: 10.1111/0022-1082.00036

|

| [23] |

Fornell C, Larcker DF (1981) Evaluating structural equation models with unobservable variables and measurement error. J Mark Res 18: 39–50. https://doi.org/10.1177/002224378101800104 doi: 10.1177/002224378101800104

|

| [24] |

Frank MZ, Goyal VK (2003) Testing the pecking order theory of capital structure. J Financ Econ 67: 217–248. https://doi.org/10.1016/S0304-405X(02)00252-0 doi: 10.1016/S0304-405X(02)00252-0

|

| [25] |

Frank MZ, Goyal VK (2009) Capital structure decisions: which factors are reliably important? Financ Manage 38: 1–37. https://doi.org/10.1111/j.1755-053X.2009.01026.x doi: 10.1111/j.1755-053X.2009.01026.x

|

| [26] |

Frankfurter GM, McGoun EG (2002) Resistance is futile: the assimilation of behavioral finance. J Econ Behav Organ 48: 375–389. https://doi.org/10.1016/S0167-2681(01)00241-4 doi: 10.1016/S0167-2681(01)00241-4

|

| [27] |

Graham JR, Harvey CR, Puri M (2013) Managerial attitudes and corporate actions. J Financ Econ 109: 103–121. https://doi.org/10.1016/j.jfineco.2013.01.010 doi: 10.1016/j.jfineco.2013.01.010

|

| [28] |

Guenzel M, Malmendier U (2020) Behavioral corporate finance: The life cycle of a CEO career (No. w27635). Natl Bureau Econ Res. https://doi.org/10.3386/w27635. doi: 10.3386/w27635

|

| [29] |

Guizani M, Ajmi AN (2021) The financial determinants of corporate cash holdings: Does sharia-compliance. Mont J of Eco 17: 157-168. http://dx.doi.org/10.14254/1800-5845/2021.17-3.13 doi: 10.14254/1800-5845/2021.17-3.13

|

| [30] |

Heaton JB (2002) Managerial optimism and corporate finance. FINANCIAL MANAGEMENT-TAMPA, 31: 33–46. https://doi.org/10.1515/9781400829125-022 doi: 10.1515/9781400829125-022

|

| [31] | Jensen MC, Meckling WH (2019) Theory of the firm: Managerial behavior, agency costs and ownership structure. In: Corporate Governance, 77–132. Gower. https://doi.org/10.1016/0304-405X(76)90026-X |

| [32] |

Jansen K, Michiels A, Voordeckers W et al. (2023) Financing decisions in private family firms: a family firm pecking order. Small Bus Econ 61: 495–515 . https://doi.org/10.1007/s11187-022-00711-9 doi: 10.1007/s11187-022-00711-9

|

| [33] |

Jiang W, Li J, Sun G (2021) Economic policy uncertainty and stock markets: A multifractal cross-correlations analysis. Fluct and Noi Lett 22: Article no. 2150018. https://doi.org/10.1142/S0219477521500188 doi: 10.1142/S0219477521500188

|

| [34] |

Lapinski MK, Kerr JM, Miller Ⅲ HW, et al. (2024) Persuasive Communication, Financial Incentives, and Social Norms: Interactions and Effects on Behaviors. Curr Opin Psychol 101851. https://doi.org/10.1016/j.copsyc.2024.101851 doi: 10.1016/j.copsyc.2024.101851

|

| [35] |

Liu Y, Liu Y, Wei Z (2022) Property rights protection, financial constraint, and capital structure choices: Evidence from a Chinese natural experiment. J Corp Financ 73: 102167. https://doi.org/10.1016/j.jcorpfin.2022.102167 doi: 10.1016/j.jcorpfin.2022.102167

|

| [36] |

Li X, Chen K, Yuan GX, et al. (2021) The decision‐making of optimal equity and capital structure based on dynamical risk profiles: A Langevin system framework for SME growth. Int J Intell Syst 36: 3500–3523. https://doi.org/10.1002/int.22424 doi: 10.1002/int.22424

|

| [37] |

Mapela L, Chipeta C (2023) Managerial confidence and capital structure announcement effects on share prices on the Johannesburg Share Exchange. South African J Econ Manag Sci 26: 4849. https://doi.org/10.4102/sajems.v26i1.4849 doi: 10.4102/sajems.v26i1.4849

|

| [38] |

Miller EM (1977) Risk, uncertainty, and divergence of opinion. J Financ 32: 1151–1168. https://doi.org/10.1111/j.1540-6261.1977.tb03317.x doi: 10.1111/j.1540-6261.1977.tb03317.x

|

| [39] | Modigliani F, Miller M H (1958) The cost of capital, corporation finance and the theory of investment. The Amer Eco Rev 48: 261-296. https://www.jstor.org/stable/1809766 |

| [40] |

Mogha V, Williams B (2021) Culture and capital structure: What else to the puzzle? Int Rev Financ Anal 73: 101614. https://doi.org/10.1016/j.irfa.2020.101614 doi: 10.1016/j.irfa.2020.101614

|

| [41] |

Mundi HS (2022) CEO social capital and capital structure complexity. J Behav Exp Financ 35: 100719. https://doi.org/10.1016/j.jbef.2022.100719 doi: 10.1016/j.jbef.2022.100719

|

| [42] |

Muhammad AUR (2022) The impact of investor sentiment on returns, cash flows, discount rates, and performance. Borsa Istanbul Revi 22: 352–362. https://doi.org/10.1016/j.bir.2021.06.005 doi: 10.1016/j.bir.2021.06.005

|

| [43] |

Myers SC (1984) The Capital Structure Puzzle. J Financ 39: 574–592. https://doi.org/10.1111/j.1540-6261.1984.tb03646.x doi: 10.1111/j.1540-6261.1984.tb03646.x

|

| [44] |

Oprean C (2014) Effects of behavioural factors on human financial decisions. Procedia Econ Financ 16: 458–463. https://doi.org/10.1016/S2212-5671(14)00825-9 doi: 10.1016/S2212-5671(14)00825-9

|

| [45] |

Orlova S, Harper JT, Sun L (2020) Determinants of capital structure complexity. J Econ Bus 110: 105905. https://doi.org/10.1016/j.jeconbus.2020.105905 doi: 10.1016/j.jeconbus.2020.105905

|

| [46] |

Pérez J, Reyna M, Vera-Martinez J (2019) Capital structure construct: a new approach to behavioral finance. Invest Manage Financ Innov 16: 86–97. https://doi.org/10.21511/imfi.16(4).2019.08 doi: 10.21511/imfi.16(4).2019.08

|

| [47] |

Rashid M, Hj DSNKP, Izadi S (2023) National culture and capital structure of the Shariah compliant firms: Evidence from Malaysia, Saudi Arabia and Pakistan. Int Rev Econ Financ 86: 949–964. https://doi.org/10.1016/j.iref.2020.10.006 doi: 10.1016/j.iref.2020.10.006

|

| [48] |

Sajid M, Mushtaq R, Murtaza G, et al. (2024) Financial literacy, confidence and well-being: The mediating role of financial behavior. J Bus Res 182: 114791. https://doi.org/10.1016/j.jbusres.2024.114791 doi: 10.1016/j.jbusres.2024.114791

|

| [49] |

Salam A Z, Shourkashti R (2019) Capital structure and firm performance in emerging market: An empirical analysis of Malaysian companies. Int J of Acad Res in Accou, Finan and Manag Sci 9: 70–82. http://dx.doi.org/10.6007/IJARAFMS/v9-i3/6334 doi: 10.6007/IJARAFMS/v9-i3/6334

|

| [50] |

Singh BP, Kannadhasan M (2020) Corruption and capital structure in emerging markets: A panel quantile regression approach. J Behav Expe Financ 28: 100417. https://doi.org/10.1016/j.jbef.2020.100417 doi: 10.1016/j.jbef.2020.100417

|

| [51] |

Shahmi MA (2023) Interaction of variable macroeconomic shock and monetary interventions on the profitability of Sharia commercial banking in Indonesia. Imara:J Riset Ekon Islam 7: 11-19. http://dx.doi.org/10.31958/imara.v7i1.9360 doi: 10.31958/imara.v7i1.9360

|

| [52] |

Sunitha K (2024) Targeting Behavior and Capital Structure Theories: An Empirical Analysis of Gulf Cooperation Council Countries. J Behav Expe Financ 100944. https://doi.org/10.1016/j.jbef.2024.100944 doi: 10.1016/j.jbef.2024.100944

|

| [53] |

Tenenhaus A, Tenenhaus M (2011) Regularized generalized canonical correlation analysis. Psychometrika 76: 257–284. https://doi.org/10.1007/s11336-011-9206-8 doi: 10.1007/s11336-011-9206-8

|

| [54] |

Thaler RH (1999) The end of behavioral finance. Financ Anal J 55: 12–17. https://doi.org/10.2469/faj.v55.n6.2310 doi: 10.2469/faj.v55.n6.2310

|

| [55] |

Ting IWK, Lean HH, Kweh QL, et al. (2016) Managerial overconfidence, government intervention and corporate financing decision. Int J Manag Financ 12: 4–24. https://doi.org/10.1108/IJMF-04-2014-0041 doi: 10.1108/IJMF-04-2014-0041

|

| [56] |

Titman S, Wessels R (1988) The determinants of capital structure choice. J Financ 43: 1–19. https://doi.org/10.1111/j.1540-6261.1988.tb02585.x doi: 10.1111/j.1540-6261.1988.tb02585.x

|

| [57] | Wang R, Zhou L (2025) Capital structure deviation and corporate technological innovation: Empirical evidence from the perspective of ESG responsibility fulfillment. Available at SSRN: https://ssrn.com/abstract=5163595 or http://dx.doi.org/10.2139/ssrn.5163595 |

| [58] |

Xing Y (2020) The impact of behavioral bias on individual investors and corporation capital structure. Acad J Bus Manag 2: 112–121. https://doi.org/10.25236/AJBM.2020.020401. doi: 10.25236/AJBM.2020.020401

|

| [59] |

Xia C, Chan KC, Cao C, et al. (2021) Generalized trust, personalized trust, and dynamics of capital structure: Evidence from China. China Econ Rev 68: 101640. https://doi.org/10.1016/j.chieco.2021.101640 doi: 10.1016/j.chieco.2021.101640

|

| [60] |

Yang B, Gan L, Wen C (2021). Moral hazard, debt overhang and capital structure. North Am J Econ Financ 58, 101538. https://doi.org/10.1016/j.najef.2021.101538 doi: 10.1016/j.najef.2021.101538

|

| [61] | Zou Y, Bai Q (2022) The impact of dividend policies and financing strategies on the speed of firms’ capital structure adjustment. Discr Dyna in Nat and Soc 2022: Article ID 3209502, 12 pages. https://doi.org/10.1155/2022/3209502 |

Figures(12) / Tables(8)

Ehsan Ahmadi, Parastoo Mohammadi, Farimah Mokhatab Rafei, Shib Sankar Sana. Behavioral factors and capital structure: identification and prioritization of influential factors[J]. Data Science in Finance and Economics, 2025, 5(1): 76-104. doi: 10.3934/DSFE.2025005

DownLoad:

DownLoad: