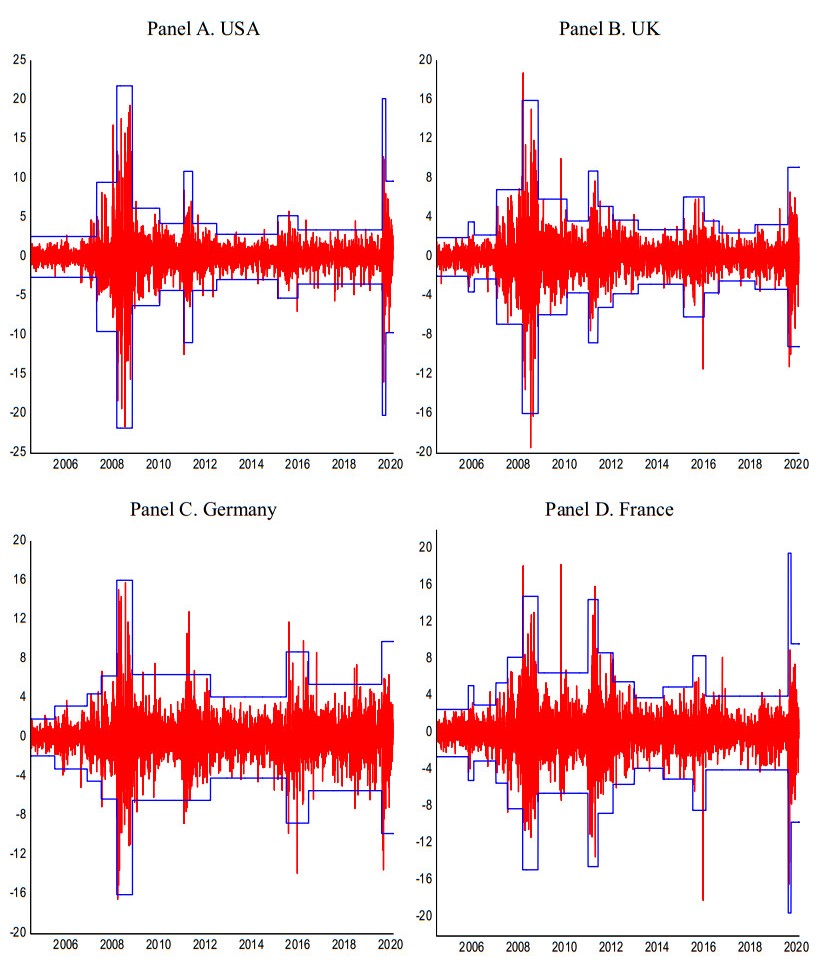

This paper quantitatively reveals the meaning of structural breaks for risk management by analyzing US and major European banking sector stocks. Applying newly extended Glosten-Jagannathan-Runkle generalized autoregressive conditional heteroscedasticity models, we supply the following new evidence. First, we find that incorporating structural breaks is always effective in estimating banking stock volatilities. Second, we clarify that structural breaks partially explain the tail fatness of banking stock returns. Third, we find that when incorporating structural breaks, the estimated volatilities more accurately capture their downside risk, proving that structural breaks matter for risk management. Fourth, our news impact curve and model parameter analyses also uncover that when incorporating structural breaks, the asymmetry in volatility responses to return shocks is more accurately captured. This proves why the estimated volatilities by incorporating structural breaks better explain downside risk. In addition, we further reveal that the estimated volatilities obtained through incorporating structural breaks increase sharply during momentous events such as the Lehman crisis, the European debt crisis, Brexit, and the recent COVID-19 crisis. Moreover, we also clarify that the volatility spreads between models with and without structural breaks rise during the Lehman and COVID-19 crises. Finally, based on our findings, we derive many significant and beneficial interpretations, implications, and innovative views for risk management using artificial intelligence in the post-COVID-19 era.

Citation: Chikashi Tsuji. The meaning of structural breaks for risk management: new evidence, mechanisms, and innovative views for the post-COVID-19 era[J]. Quantitative Finance and Economics, 2022, 6(2): 270-302. doi: 10.3934/QFE.2022012

This paper quantitatively reveals the meaning of structural breaks for risk management by analyzing US and major European banking sector stocks. Applying newly extended Glosten-Jagannathan-Runkle generalized autoregressive conditional heteroscedasticity models, we supply the following new evidence. First, we find that incorporating structural breaks is always effective in estimating banking stock volatilities. Second, we clarify that structural breaks partially explain the tail fatness of banking stock returns. Third, we find that when incorporating structural breaks, the estimated volatilities more accurately capture their downside risk, proving that structural breaks matter for risk management. Fourth, our news impact curve and model parameter analyses also uncover that when incorporating structural breaks, the asymmetry in volatility responses to return shocks is more accurately captured. This proves why the estimated volatilities by incorporating structural breaks better explain downside risk. In addition, we further reveal that the estimated volatilities obtained through incorporating structural breaks increase sharply during momentous events such as the Lehman crisis, the European debt crisis, Brexit, and the recent COVID-19 crisis. Moreover, we also clarify that the volatility spreads between models with and without structural breaks rise during the Lehman and COVID-19 crises. Finally, based on our findings, we derive many significant and beneficial interpretations, implications, and innovative views for risk management using artificial intelligence in the post-COVID-19 era.

| [1] |

Abakah EJA, Gil-Alana LA, Madigu G, et al. (2020) Volatility persistence in cryptocurrency markets under structural breaks. Int Rev Econ Financ 69: 680-691. https://doi.org/10.1016/j.iref.2020.06.035 doi: 10.1016/j.iref.2020.06.035

|

| [2] |

Adesina T (2017) Estimating volatility persistence under a Brexit-vote structural break. Financ Res Lett 23: 65-68. https://doi.org/10.1016/j.frl.2017.03.004 doi: 10.1016/j.frl.2017.03.004

|

| [3] |

Adrian T, Boyarchenko N (2018) Liquidity policies and systemic risk. J Finan Intermed 35: 45-60. https://doi.org/10.1016/j.jfi.2017.08.005 doi: 10.1016/j.jfi.2017.08.005

|

| [4] |

Ahmad AH, Aworinde OB (2016) The role of structural breaks, nonlinearity and asymmetric adjustments in African bilateral real exchange rates. Int Rev Econ Financ 45: 144-159. https://doi.org/10.1016/j.iref.2016.05.004 doi: 10.1016/j.iref.2016.05.004

|

| [5] | Bank of England (2020) PRA statement on deposit takers' approach to dividend payments, share buybacks and cash bonuses in response to Covid-19, London, UK. Available from: https://www.bankofengland.co.uk/prudential-regulation/publication/2020/pra-statement-on-deposit-takers-approach-to-dividend-payments-share-buybacks-and-cash-bonuses. |

| [6] |

Bauwens L, Laurent S (2005) A new class of multivariate skew densities, with application to generalized autoregressive conditional heteroscedasticity models. J Bus Econ Stat 23: 346-354. https://doi.org/10.1198/073500104000000523 doi: 10.1198/073500104000000523

|

| [7] |

Benartzi S, Thaler RH (1995) Myopic loss aversion and the equity premium puzzle. Q J Econ 110: 73-92. https://doi.org/10.2307/2118511 doi: 10.2307/2118511

|

| [8] | Borri N, di Giorgio G (2022) Systemic risk and the COVID challenge in the European banking sector. J Bank Financ.[In press]. https://doi.org/10.1016/j.jbankfin.2021.106073 |

| [9] |

Bulkley G, Giordani P (2011) Structural breaks, parameter uncertainty, and term structure puzzles. J Financ Econ 102: 222-232. https://doi.org/10.1016/j.jfineco.2011.05.009 doi: 10.1016/j.jfineco.2011.05.009

|

| [10] |

Buston CS (2016) Active risk management and banking stability. J Bank Financ 72: s203-s215. https://doi.org/10.1016/j.jbankfin.2015.02.004 doi: 10.1016/j.jbankfin.2015.02.004

|

| [11] |

Butaru F, Chen Q, Clark B, Das S, et al. (2016) Risk and risk management in the credit card industry. J Bank Financ 72: 218-239. https://doi.org/10.1016/j.jbankfin.2016.07.015 doi: 10.1016/j.jbankfin.2016.07.015

|

| [12] |

Cardona E, Mora-Valencia A, Velásquez-Gaviria D (2019) Testing expected shortfall: An application to emerging market stock indices. Risk Manage 21: 153-182. https://doi.org/10.1057/s41283-018-0046-z doi: 10.1057/s41283-018-0046-z

|

| [13] |

Cerqueti R, Costantini M (2011) Testing for rational bubbles in the presence of structural breaks: Evidence from nonstationary panels. J Bank Financ 35: 2598-2605. https://doi.org/10.1016/j.jbankfin.2011.02.011 doi: 10.1016/j.jbankfin.2011.02.011

|

| [14] |

Chowdhury K (2012) Modelling the dynamics, structural breaks and the determinants of the real exchange rate of Australia. Int Financ Mark Inst Money 22: 343-358. https://doi.org/10.1016/j.intfin.2011.10.004 doi: 10.1016/j.intfin.2011.10.004

|

| [15] |

Davydov D, Vähämaa S, Yasar S (2021) Bank liquidity creation and systemic risk. J Bank Financ 123: 106031. https://doi.org/10.1016/j.jbankfin.2020.106031 doi: 10.1016/j.jbankfin.2020.106031

|

| [16] |

Duffie D, Pan J (1997) An overview of value at risk. J Deriv 4: 7-49. https://doi.org/10.3905/jod.1997.407971 doi: 10.3905/jod.1997.407971

|

| [17] |

Engle RF, Ng VK (1993) Measuring and testing the impact of news on volatility. J Financ 48: 1749-1778. https://doi.org/10.2307/2329066 doi: 10.2307/2329066

|

| [18] |

Esteve V, Navarro-Ibáñez M, Prats MA (2013) The Spanish term structure of interest rates revisited: Cointegration with multiple structural breaks, 1974-2010. Int Rev Econ Financ 25: 24-34. https://doi.org/10.1016/j.iref.2012.04.007 doi: 10.1016/j.iref.2012.04.007

|

| [19] | European Central Bank (2020) Recommendation of the European Central Bank of 27 March 2020 on dividend distributions during the COVID-19 pandemic and repealing Recommendation ECB/2020/1 (ECB/2020/19), Frankfurt, Germany. Available from: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52020HB0019&qid=1652583624238. |

| [20] |

Ewing BT, Malik F (2005) Re-examining the asymmetric predictability of conditional variances: The role of sudden changes in variance. J Bank Financ 29: 2655-2673. https://doi.org/10.1016/j.jbankfin.2004.10.002 doi: 10.1016/j.jbankfin.2004.10.002

|

| [21] |

Ewing BT, Malik F (2016) Volatility spillovers between oil prices and the stock market under structural breaks. Glob Financ J 29: 12-23. https://doi.org/10.1016/j.gfj.2015.04.008 doi: 10.1016/j.gfj.2015.04.008

|

| [22] | Federal Reserve Board (2020) Federal Reserve Board releases results of stress tests for 2020 and additional sensitivity analyses conducted in light of the coronavirus event, Washington, USA. Available from: https://www.federalreserve.gov/newsevents/pressreleases/bcreg20200625c.htm. |

| [23] |

Georgiopoulos N (2020) Liability-driven investments of life insurers under investment credit risk. Risk Manage 22: 83-107. https://doi.org/10.1057/s41283-019-00055-x doi: 10.1057/s41283-019-00055-x

|

| [24] |

Glosten LR, Jagannathan R, Runkle DE (1993) On the relation between expected value and the volatility of the nominal excess return on stocks. J Financ 48: 1779-1801. https://doi.org/10.1111/j.1540-6261.1993.tb05128.x doi: 10.1111/j.1540-6261.1993.tb05128.x

|

| [25] |

Granger CWJ, Hyung N (2004) Occasional structural breaks and long memory with an application to the S & P 500 absolute stock returns. J Empir Financ 11: 399-421. https://doi.org/10.1016/j.jempfin.2003.03.001 doi: 10.1016/j.jempfin.2003.03.001

|

| [26] |

Li W, Cheng Y, Fang Q (2020) Forecast on silver futures linked with structural breaks and day-of-the-week effect. North Am J Econ Financ 53: 101192. https://doi.org/10.1016/j.najef.2020.101192 doi: 10.1016/j.najef.2020.101192

|

| [27] |

Lv Z, Chu AMY, Wong WK, et al. (2021) The maximum-return-and-minimum-volatility effect: Evidence from choosing risky and riskless assets to form a portfolio. Risk Manage 23: 97-122. https://doi.org/10.1057/s41283-021-00069-4 doi: 10.1057/s41283-021-00069-4

|

| [28] |

Malik M, Shafie R, Ismail KNIK (2021) Do risk management committee characteristics influence the market value of firms? Risk Manage 23: 172-191. https://doi.org/10.1057/s41283-021-00073-8 doi: 10.1057/s41283-021-00073-8

|

| [29] |

Matallín-Sáez JC, Soler-Domínguez A, de Mingo-López DV (2021) On management risk and price in the mutual fund industry: Style and performance distribution analysis. Risk Manage 23: 150-171. https://doi.org/10.1057/s41283-021-00072-9 doi: 10.1057/s41283-021-00072-9

|

| [30] |

Maveyraud-Tricoire S, Rous P (2009) RIP and the shift toward a monetary union: Looking for a "euro effect" by a structural break analysis with panel data. Int Fin Mark Inst Money 19: 336-350. https://doi.org/10.1016/j.intfin.2008.01.005 doi: 10.1016/j.intfin.2008.01.005

|

| [31] |

Mensi W, Al-Yahyaee KH, Kang SH (2019) Structural breaks and double long memory of cryptocurrency prices: A comparative analysis from Bitcoin and Ethereum. Financ Res Let 29: 222-230. https://doi.org/10.1016/j.frl.2018.07.011 doi: 10.1016/j.frl.2018.07.011

|

| [32] |

Pérez-Rodríguez JV (2020) Another look at the implied and realised volatility relation: A copula-based approach. Risk Manage 22: 38-64. https://doi.org/10.1057/s41283-019-00054-y doi: 10.1057/s41283-019-00054-y

|

| [33] |

Rockafellar RT, Uryasev S (2000) Optimization of conditional value-at-risk. J Risk 2: 21-41. https://doi.org/10.21314/JOR.2000.038 doi: 10.21314/JOR.2000.038

|

| [34] |

Ross SA (1989) Information and volatility: The no-arbitrage martingale approach to timing and resolution irrelevancy. J Financ 44: 1-17. https://doi.org/10.1111/j.1540-261.1989.tb02401.x doi: 10.1111/j.1540-261.1989.tb02401.x

|

| [35] |

Safi A, Yi X, Wahab S, et al. (2021) CEO overconfidence, firm-specific factors, and systemic risk: Evidence from China. Risk Manage 23: 30-47. https://doi.org/10.1057/s41283-021-00066-7 doi: 10.1057/s41283-021-00066-7

|

| [36] |

Smith SC (2017) Equity premium estimates from economic fundamentals under structural breaks. Int Rev Financ Anal 52: 49-61. https://doi.org/10.1016/j.irfa.2017.04.011 doi: 10.1016/j.irfa.2017.04.011

|

| [37] |

Sun J, Zhou M, Ai W, et al. (2019) Dynamic prediction of relative financial distress based on imbalanced data stream: From the view of one industry. Risk Manage 21: 215-242. https://doi.org/10.1057/s41283-018-0047-y doi: 10.1057/s41283-018-0047-y

|

| [38] | Tsuji C (2016) Does the fear gauge predict downside risk more accurately than econometric models? Evidence from the US stock market. Cogent Econ Financ 4: 1220711, 1-42. http://dx.doi.org/10.1080/23322039.2016.1220711 |

| [39] |

Tsuji C (2018) Return transmission and asymmetric volatility spillovers between oil futures and oil equities: New DCC-MEGARCH analyses. Econ Model 74: 167-185. https://doi.org/10.1016/j.econmod.2018.05.007 doi: 10.1016/j.econmod.2018.05.007

|

| [40] |

Tsuji C (2020) Correlation and spillover effects between the US and international banking sectors: New evidence and implications for risk management. Int Rev Financ Anal 70: 101392. https://doi.org/10.1016/j.irfa.2019.101392 doi: 10.1016/j.irfa.2019.101392

|

| [41] |

Varotto S, Zhao L (2018) Systemic risk and bank size. J Int Money Financ 82: 45-70. https://doi.org/10.1016/j.jimonfin.2017.12.002 doi: 10.1016/j.jimonfin.2017.12.002

|

| [42] |

Villanueva OM (2007) Spot-forward cointegration, structural breaks and FX market unbiasedness. Int Fin Mark Inst Money 17: 58-78. https://doi.org/10.1016/j.intfin.2005.08.007 doi: 10.1016/j.intfin.2005.08.007

|

| [43] |

Wen F, Weng K, Zhou WX (2020) Measuring the contribution of Chinese financial institutions to systemic risk: An extended asymmetric CoVaR approach. Risk Manage 22: 310-337. https://doi.org/10.1057/s41283-020-00064-1 doi: 10.1057/s41283-020-00064-1

|

| [44] |

Xing H, Sun N, Chen Y (2012) Credit rating dynamics in the presence of unknown structural breaks. J Bank Financ 36: 78-89. https://doi.org/10.1016/j.jbankfin.2011.06.005 doi: 10.1016/j.jbankfin.2011.06.005

|

| [45] |

Yin A (2019) Out-of-sample equity premium prediction in the presence of structural breaks. Int Rev Financ Anal 65: 101385. https://doi.org/10.1016/j.irfa.2019.101385 doi: 10.1016/j.irfa.2019.101385

|

| [46] |

Zeb S, Rashid A (2019) Systemic risk in financial institutions of BRICS: Measurement and identification of firm-specific determinants. Risk Manage 21: 243-264. https://doi.org/10.1057/s41283-018-00048-2 doi: 10.1057/s41283-018-00048-2

|

| [47] |

Zhu X, Ao X, Qin Z, et al. (2021) Intelligent financial fraud detection practices in post-pandemic era. The Innovation 2: 100176. https://doi.org/10.1016/j.xinn.2021.100176 doi: 10.1016/j.xinn.2021.100176

|

Figures(5) / Tables(8)

Chikashi Tsuji. The meaning of structural breaks for risk management: new evidence, mechanisms, and innovative views for the post-COVID-19 era[J]. Quantitative Finance and Economics, 2022, 6(2): 270-302. doi: 10.3934/QFE.2022012

DownLoad:

DownLoad: