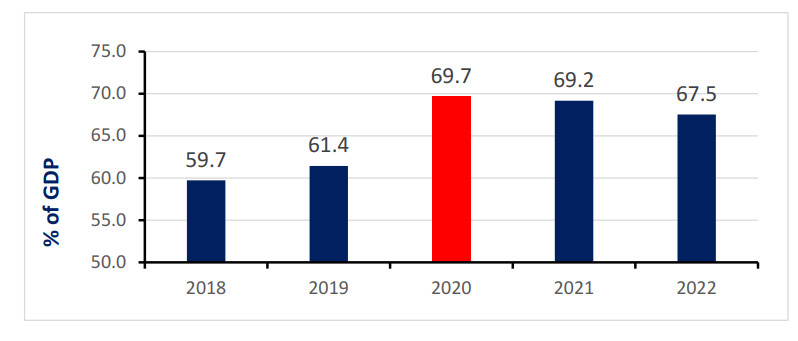

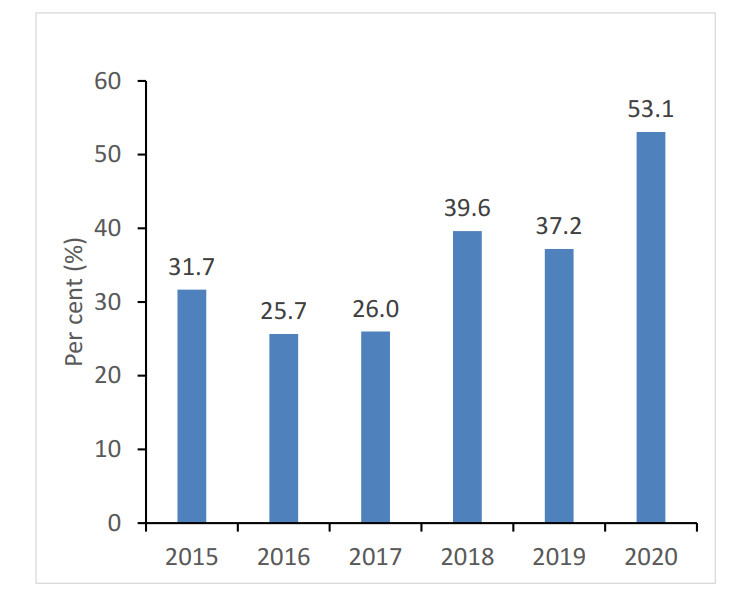

Commodity-linked bond, a type of state contingent claims, presents an innovative tool for African countries to mobilize resources on the international capital markets. Given their colossal financing needs, which has been worsened by the COVID-19 pandemic, African countries need to put in place innovative financing mechanisms to support their development frameworks for building back better. The issuing of this type of bond could provide an opportunity for commodity-producing African countries to hedge against fluctuations in their export earnings. The results show that the value of a commodity-linked bond increases as the price of the commodity indexed to the bond rises, suggesting that African countries should issue debt contracts that are tied to their export commodities so that their debt declines with plummeting export prices (or export revenues). A simple portfolio rule derived suggests that countries should issue more commodity-linked bonds than conventional debt if the variance of the portfolio is greater than twice the spread between the expected total return of the conventional debt and the commodity-linked bond. This rule supports the view that African countries' debt-service payments, for debt issued in the form of commodity-linked bonds, would decline whenever the price of their export commodities decline thus lightening their debt load.

Citation: Joseph Atta-Mensah. Commodity-linked bonds as an innovative financing instrument for African countries to build back better[J]. Quantitative Finance and Economics, 2021, 5(3): 516-541. doi: 10.3934/QFE.2021023

Commodity-linked bond, a type of state contingent claims, presents an innovative tool for African countries to mobilize resources on the international capital markets. Given their colossal financing needs, which has been worsened by the COVID-19 pandemic, African countries need to put in place innovative financing mechanisms to support their development frameworks for building back better. The issuing of this type of bond could provide an opportunity for commodity-producing African countries to hedge against fluctuations in their export earnings. The results show that the value of a commodity-linked bond increases as the price of the commodity indexed to the bond rises, suggesting that African countries should issue debt contracts that are tied to their export commodities so that their debt declines with plummeting export prices (or export revenues). A simple portfolio rule derived suggests that countries should issue more commodity-linked bonds than conventional debt if the variance of the portfolio is greater than twice the spread between the expected total return of the conventional debt and the commodity-linked bond. This rule supports the view that African countries' debt-service payments, for debt issued in the form of commodity-linked bonds, would decline whenever the price of their export commodities decline thus lightening their debt load.

| [1] | Adeniran A, Ekeruche M, Bodunrin S, et al. (2018) Africa's Rising Debt: Implications for Development Financing and Sustainable Debt Management Approach. Global Economic Governance Discussion Paper. |

| [2] | Asonuma T, Chamon M, Erce A, et al. (2020) Costs of Sovereign Defaults: Restructuring Strategies and the Credit-Investment Channel. Available from: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3557035. |

| [3] | Asonuma T, Chamon M, Erce A, et al. (2019) Costs of Sovereign Defaults: Restructuring Strategies, Bank Distress and the Capital Inflow-Credit Channel. IMF Working Paper WP/19/69. Available from: https://www.imf.org/en/Publications/WP/Issues/2019/03/25/Costs-of-Sovereign-Defaults-Restructuring-Strategies-Bank-Distress-and-the-Capital-Inflow-46678. |

| [4] | Atta-Mensah J (1992) The Valuation of Commodity-Linked Bonds, Unpublished PhD thesis, Simon Fraser University. |

| [5] |

Atta-Mensah J, Ibrahim M (2020) Explaining Africa's Debt: The Journey So Far and the Arithmetic of the Policymaker. Theor Econ Lett 10: 409-441. doi: 10.4236/tel.2020.102027

|

| [6] | Błach J (2020) Barriers to Financial Innovation—Corporate Finance Perspective. J Risk Financ Manage 273. |

| [7] |

Black F, Scholes M (1973) The Pricing of Options and Corporate Liabilities. J Polit Econ 81: 637-659. doi: 10.1086/260062

|

| [8] |

Borensztein E, Mauro P (2004) The case for GDP‐indexed bonds. Econ Policy 19: 166-216. doi: 10.1111/j.1468-0327.2004.00121.x

|

| [9] | Brooke M, Mendes R, Alex Pienkowski, et al. (2013) Sovereign Default and State-Contingent Debt. Bank of Canada Discussion Paper 2013-13. Available from: https://www.bankofcanada.ca/wp-content/uploads/2013/11/dp2013-03.pdf. |

| [10] | Budd N (1983) The Future of Commodity-Indexed Financing. Harvard Bus Rev. |

| [11] |

Caballero R (2003) The Future of the IMF. Am Econ Rev 93: 31-38. doi: 10.1257/000282803321946769

|

| [12] | Cohen C, Abbas S, Anthony M, et al. (2020) The Role of State-Contingent Debt Instruments in Sovereign Debt Restructurings. IMF Staff Discussion Notes No. 2020/006. Available from: https://www.imf.org/en/Publications/Staff-Discussion-Notes/Issues/2020/11/13/The-Role-of-State-Contingent-Debt-Instruments-in-Sovereign-Debt-Restructurings-49732. |

| [13] |

Consiglio A, Zenios S (2018) Pricing and hedging GDP-linked bonds in incomplete markets. J Econ Dyn Control 88: 137-155. doi: 10.1016/j.jedc.2018.01.001

|

| [14] |

Demertzis M, Zenios S (2019) State Contingent Debt as Insurance for Euro Area Sovereigns. J Financ Regula 5: 64-90. doi: 10.1093/jfr/fjz003

|

| [15] | Dornbusch R (1988) Our African Counties Debts, In: The United States in the World Economy, edited by M. Feldstein. Chicago Press: NBER. |

| [16] | Fall M (1986) Commodity-Indexed Bonds. Unpublished Masters' Thesis, M.I.T Sloan School of Management, Cambridge. |

| [17] |

Failler P, Montocchio C, Borot de Battisti A, et al. (2019) Sustainable financing of marine protected areas: the case of the Martinique regional marine reserve of "Le Prêcheur". Green Financ 1: 110-129. doi: 10.3934/GF.2019.2.110

|

| [18] | Fischer S (2002) Financial Crises and the Reform of the International Financial System. NBER Working Paper No. 9297. |

| [19] | GFDRR (2018) Building Back Better: Achieving resilience through stronger, faster, and more inclusive post-disaster reconstruction. |

| [20] |

Froot K, Scharfstein D, Stein J (1989) African Country Debt: Forgiveness, Indexation and Investment Incentives. J Financ 44: 1335-1350. doi: 10.1111/j.1540-6261.1989.tb02656.x

|

| [21] | Kenen P (1990) Organizing Debt Relief: The Need for A New Institution. J Econ Perspect. |

| [22] | Kim J, Ostry J (2018) Boosting Fiscal Space: The Roles of GDP-Linked Debt and Longer Maturities. IMF Research Department Paper No.18/04, Washington, DC. Available from: https://www.imf.org/en/Publications/Departmental-Papers-Policy-Papers/Issues/2018/03/14/Boosting-Fiscal-Space-The-Roles-of-GDP-Linked-Debt-and-Longer-Maturities-45132. |

| [23] |

Kletzer K, Wright B (2000) Sovereign Debt as Intertemporal Barter. Am Econ Rev 90: 621-639. doi: 10.1257/aer.90.3.621

|

| [24] | Krueger A (2003) Sovereign Debt Restructuring: Messy or Messier? Am Econ Rev 93: 70-74. |

| [25] |

Krugman P (1988) Financing versus Forgiving a Debt Overhang. J Dev Econ 29: 253-268. doi: 10.1016/0304-3878(88)90044-2

|

| [26] | Krugman P (1989) Market-Based Debt-Reduction Schemes, In: Analytical Issues in Debt, edited by Frenkel J, Dooley M and Wickman P, Washington: IMF. |

| [27] | Meltzer A (2000) Report to the International Financial Institution Advisory Commission, Washington, DC: US Government Printing Office. |

| [28] | Krumm K (2018) The External Debt of Sub-Saharan Africa: Origins, Magnitude and Implications for Action. World Bank Staff Working Paper, 741. Available from: http://documents.worldbank.org/curated/en/958551468768269528/pdf/multi0page.pdf. |

| [29] |

Merton R (1973) An Intertemporal Assets Pricing Model. Econometrica 41: 867-887. doi: 10.2307/1913811

|

| [30] |

Merton R (1971) Optimum Consumption and Portfolio Rules in a Continuous-Time Model. J Econ Theory 3: 373-413. doi: 10.1016/0022-0531(71)90038-X

|

| [31] |

Miura R, Yamauchi H (1998) The Pricing Formula for Commodity-Linked Bonds with Stochastic Convenience Yields and Default Risk. Asia-Pacific Financ Mark 5: 129-158. doi: 10.1023/A:1010034115552

|

| [32] | Mustapha S, Prizzon A (2018) Africa's rising debt: How to avoid a new crisis. Briefing Note. London: Overseas Development Institute. |

| [33] |

Myers R, Thompson S (1989) Optimal Portfolios of External Debt in Developing Countries: The Potential Role of Commodity-Linked Bonds. Am J Agric Econ 71: 517-522. doi: 10.2307/1241625

|

| [34] | OECD (2020) Building Back Better: A Sustainable, Resilient Recovery after COVID-19. |

| [35] |

O'Hara M (1984) Commodity Bonds and Consumption Risks. J Financ 39: 193-206. doi: 10.1111/j.1540-6261.1984.tb03868.x

|

| [36] | Privolos T, Duncan R (1991) Commodity Risk Management and Finance, Washington, DC: World Bank. |

| [37] | Sachs J (1988) Comprehensive Debt Retirement: The Bolivian Example. Brookings Pap Econ Activity 2: 705-713. |

| [38] |

Schwartz E (1982) The Pricing of Commodity Linked Bonds. J Financ 37: 525-539. doi: 10.1111/j.1540-6261.1982.tb03573.x

|

| [39] | UNSG Report (2020) Shared Responsibility, Global Solidarity: Responding to the socio-economic impacts of COVID-19. Available from: https://unsdg.un.org/sites/default/files/2020-03/SG-Report-Socio-Economic-Impact-of-Covid19.pdf. |

| [40] |

Vasicek O (1977) An Equilibrium Characterization of the Term Structure. J Financ Econ 5: 177-188. doi: 10.1016/0304-405X(77)90016-2

|

| [41] | Williamson J (2000) The Role of the IMF: A Guide to the Reports. Institute for International Economics, International Economics Policy Briefs No. 00-5. |

| [42] | Zenios S, Consiglio A, Athanasopoulou M, et al. (2021) Risk Management for Sustainable Sovereign Debt Financing. Oper Res. Available from: https://doi.org/10.1287/opre.2020.2055. |

QFE-05-03-023-s001.pdf QFE-05-03-023-s001.pdf |

|

Figures(2)

Joseph Atta-Mensah. Commodity-linked bonds as an innovative financing instrument for African countries to build back better[J]. Quantitative Finance and Economics, 2021, 5(3): 516-541. doi: 10.3934/QFE.2021023

DownLoad:

DownLoad: