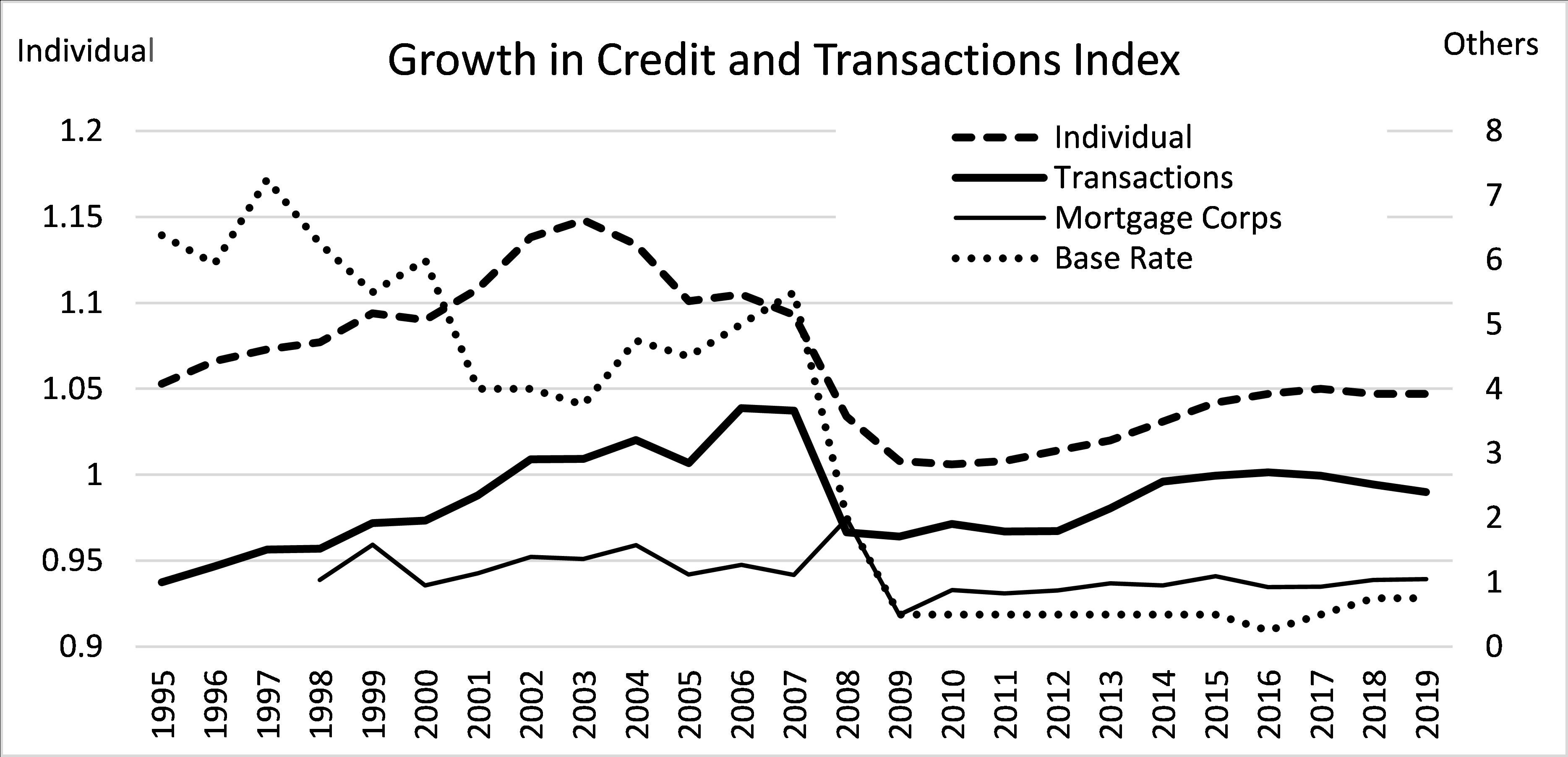

This paper considers housing activity transmission across space using local indicators of spatial association. Activity does not diffuse like a ripple across England and Wales. Elevated activity appears to be associated with a south east-north west divide. The south east grows more quickly than the north west for a period of time, after which there is a switch in rank order. It is argued that changes in activity is associated with changing credit conditions to which the south east is more sensitive. Furthermore, it is proposed that activity features a type of participant induced on to the market by favourable price changes and credit conditions. It is argued that the reduced activity associated with 'missing mortgage movers' post-2007 reflects the lack of mortgage mover participation, which could have negative consequences for the macroeconomy.

Citation: David Gray. Housing market activity diffusion in England and Wales[J]. National Accounting Review, 2023, 5(2): 125-144. doi: 10.3934/NAR.2023008

This paper considers housing activity transmission across space using local indicators of spatial association. Activity does not diffuse like a ripple across England and Wales. Elevated activity appears to be associated with a south east-north west divide. The south east grows more quickly than the north west for a period of time, after which there is a switch in rank order. It is argued that changes in activity is associated with changing credit conditions to which the south east is more sensitive. Furthermore, it is proposed that activity features a type of participant induced on to the market by favourable price changes and credit conditions. It is argued that the reduced activity associated with 'missing mortgage movers' post-2007 reflects the lack of mortgage mover participation, which could have negative consequences for the macroeconomy.

| [1] |

Aikman D, Haldane A, Nelson B (2015) Curbing the Credit Cycle. Econ J 125: 1072–1109. https://doi.org/10.1111/ecoj.12113 doi: 10.1111/ecoj.12113

|

| [2] |

Alexander C, Barrow M (1994) Seasonality and Cointegration of Regional House Prices in the UK. Urban Stud 31: 1667–1689. https://doi.org/10.1080/00420989420081571 doi: 10.1080/00420989420081571

|

| [3] |

Allen F, Gale D (2000) Bubbles and crises. Econ J 110: 236–255. https://doi.org/10.1111/1468-0297.00499 doi: 10.1111/1468-0297.00499

|

| [4] |

Andrew M, Geoffrey M (2008) House Price Appreciation, Transactions and Structural Change in the British Housing Market: A Macroeconomic Perspective. Real Estate Econ 31: 99–116. https://doi.org/10.1111/j.1080-8620.2003.00059.x doi: 10.1111/j.1080-8620.2003.00059.x

|

| [5] |

Anselin L (1995) Local Indicators of Spatial Association—LISA. Geogr Anal 27: 96–115. https://doi.org/10.1111/j.1538-4632.1995.tb00338.x doi: 10.1111/j.1538-4632.1995.tb00338.x

|

| [6] |

Aoki K, Proudmand J, Vlieghe G (2004) House prices, consumption and monetary policy: a financial accelerator approach. J Financial Intermediation 13: 414–435. https://doi.org/10.1016/j.jfi.2004.06.003 doi: 10.1016/j.jfi.2004.06.003

|

| [7] | Balcilar M, Beyene A, Gupta R, Seleteng M (2013) Ripple Effects in South African House Prices. Urban Stud 50: 876–894. |

| [8] | Benito A, Wood R (2005) How Important is Housing Market Activity for Durables Spending? Bank Engl Q Bull 45: 153–159. |

| [9] |

Berkovec J, Goodman J (1996) Turnover as a measure of demand for existing homes. Real Estate Econ 24: 421–440. https://doi.org/10.1111/1540-6229.00698 doi: 10.1111/1540-6229.00698

|

| [10] | Bernanke B, Gertler M (1989) Agency Costs, Net Worth, and Business Fluctuations. Am Econ Rev 79: 14–31. |

| [11] |

Blake J, Gharleghi B (2018) The ripple effect at an inter-suburban level in the Sydney metropolitan area. Int J Hous Mark Anal 11: 2–33. https://doi.org/10.1108/IJHMA-05-2017-0054 doi: 10.1108/IJHMA-05-2017-0054

|

| [12] |

Cook S (2012) β-Convergence and the cyclical dynamics of UK regional house prices. Urban Stud 49: 203–218. https://doi.org/10.1177/0042098011399595 doi: 10.1177/0042098011399595

|

| [13] |

Cook S, Thomas C (2003) An Alternative Approach to Examining the Ripple Effect in UK House Prices. Appl Econ Lett 10: 849–851. https://doi.org/10.1080/1350485032000143119 doi: 10.1080/1350485032000143119

|

| [14] | Drehmann M. Borio C, Tstasaronis K (2012) Characterising the Financial Cycle: don't lose sight of the Medium Term! BIS Working Papers. Available from: https://www.bis.org/publ/work380.pdf. |

| [15] |

Duca J, Muellbauer J, Murphy A (2021) What Drives House Price Cycles? International Experience and Policy Issues. J Econ Lit 59: 773–864. https://doi.org/10.1257/jel.20201325 doi: 10.1257/jel.20201325

|

| [16] |

Edelstein R, Qian W (2014) Short-Term Buyers and Housing Market Dynamics. J Real Estate Finan Econ 49: 654–689. https://doi.org/10.1007/s11146-012-9395-7 doi: 10.1007/s11146-012-9395-7

|

| [17] | Genesove D, Mayer C (2001) Loss aversion and seller behavior: Evidence from the housing market. Q J Econ 87: 1233–1260. |

| [18] |

Gray D (2012) District House Price Movements in England and Wales 1997–2007: An Exploratory Spatial Data Analysis Approach. Urban Stud 49: 1411–1434. https://doi.org/10.1177/0042098011417020 doi: 10.1177/0042098011417020

|

| [19] |

Gray D (2020) The Size-Growth Relationship: A Test of House Price Growth across the Regions of the British Isles. J Eur Real Estate Res 13: 243–256. https://doi.org/10.1108/JERER-10-2019-0033 doi: 10.1108/JERER-10-2019-0033

|

| [20] |

Gray D (2023) What Can District Migration Rates Tell Us about London's Functional Urban Area? J Risk Financial Manag 16: 89. https://doi.org/10.3390/jrfm16020089 doi: 10.3390/jrfm16020089

|

| [21] |

Gueye G (2021) Pitfalls in the cointegration analysis of housing prices with the macroeconomy: Evidence from OECD countries. J Hous Econ 51: 101748. https://doi.org/10.1016/j.jhe.2021.101748 doi: 10.1016/j.jhe.2021.101748

|

| [22] | Guillain R, Le Gallo J, Boiteux-Orain C (2006) Changes in Spatial and Sectoral Patterns of Employment in Ile-de-France, 1978–97. Urban Stud 43: 2075–2098. |

| [23] |

Gupta R, Marfatia H, Pierdzioch C, Salisu A (2022) Machine Learning Predictions of Housing Market Synchronization across US States: The Role of Uncertainty. J Real Estate Finan Econ 64: 523–545. https://doi.org/10.1007/s11146-020-09813-1 doi: 10.1007/s11146-020-09813-1

|

| [24] | Holmes M, Otero J (2022) The Spatio-Temporal Dynamics of House Prices Across London. Real Estate Financ 38: 243–55. |

| [25] | Hudson N, Green B (2017) Missing Movers: A Long-Term Decline in Housing Transactions? Council of Mortgage Lenders. Available from: https://thinkhouse.org.uk/site/assets/files/1756/cmlmissing.pdf. |

| [26] |

Kiyotaki N, Moore J (1997) Credit Cycles. J Polit Econ 105: 211–248. https://doi.org/10.1086/262072 doi: 10.1086/262072

|

| [27] |

Le Gallo J, Ertur C (2003) Exploratory spatial data analysis of the distribution of regional per capita GDP in Europe, 1980–1995. Papers Reg Sci 82: 175–201. https://doi.org/10.1007/s101100300145 doi: 10.1007/s101100300145

|

| [28] | Leamer E (2007) Housing is the Business Cycle. Available from: https://www.nber.org/system/files/working_papers/w13428/w13428.pdf. |

| [29] |

Lo Cascio I (2021) A wavelet analysis of the ripple effect in UK regional housing markets. Int Rev Econ Finance 76: 1093–1105. https://doi.org/10.1016/j.iref.2021.08.001 doi: 10.1016/j.iref.2021.08.001

|

| [30] |

McClennan D, Muellbauer J, Stephens M (1998) Asymmetries in Housing and Financial Market Institution and EMU. Oxford Rev Econ Policy 14: 54–80. https://doi.org/10.1093/oxrep/14.3.54 doi: 10.1093/oxrep/14.3.54

|

| [31] |

Meen G (1999) Regional House Prices and the Ripple Effect: A New Interpretation. Housing Stud 14: 733–753. https://doi.org/10.1080/02673039982524 doi: 10.1080/02673039982524

|

| [32] |

Mian A, Sufi A (2018) Finance and Business Cycles: The Credit-Driven Household Demand Channel. J Econ Perspect 3: 31–58. https://doi.org/10.3386/w24322 doi: 10.3386/w24322

|

| [33] | Miles D, Monro V (2021) UK house prices and three decades of decline in the risk-free real interest rate. 36: 627–684. https://doi.org/10.1093/epolic/eiab006 |

| [34] |

Oikarinen E (2004) The Diffusion of Housing Price Movements from Center to Surrounding Areas. J Hous Res 15: 3–28. https://doi.org/10.1080/10835547.2004.12091958 doi: 10.1080/10835547.2004.12091958

|

| [35] |

Ortalo-Magné F, Rady S (2004) Housing transactions and macroeconomic fluctuations: a case study of England and Wales. J Hous Econ 13: 287–303. https://doi.org/10.1016/j.jhe.2004.09.005 doi: 10.1016/j.jhe.2004.09.005

|

| [36] |

Palley T (2011) A Theory of Minsky Super-cycles and Financial Crises. Contrib Polit Econ 30: 31–46. https://doi.org/10.1093/cpe/bzr004 doi: 10.1093/cpe/bzr004

|

| [37] |

Pyhrr S, Roulac S, Born W (1999) Real Estate Cycles and their Strategic Implications for Investors and Portfolio Managers in the Global Economy. J Real Estate Res 18: 7–68. https://doi.org/10.1080/10835547.1999.12090986 doi: 10.1080/10835547.1999.12090986

|

| [38] |

Shi S, Young M, Hargreaves B (2009) The ripple effect of local house price movements in New Zealand. J Prop Res 26: 1–24. https://doi.org/10.1080/09599910903289880 doi: 10.1080/09599910903289880

|

| [39] | Siegel S, Castellan N (1988) Nonparametric Statistics, McGraw-Hill, New York. |

| [40] |

Stevenson S (2004) House Price Diffusion and Inter-Regional and Cross-Border House Price Dynamics. J Prop Res 21: 301–320. https://doi.org/10.1080/09599910500151228 doi: 10.1080/09599910500151228

|

| [41] |

Tsai IC (2014) Ripple effect in house prices and trading volume in the UK housing market: New viewpoint and evidence. Econ Model 40: 68–75. https://doi.org/10.1016/j.econmod.2014.03.026 doi: 10.1016/j.econmod.2014.03.026

|

| [42] |

Tsai IC (2015) Spillover Effect between the Regional and the National Housing Markets in the UK. Reg Stud 49: 1957–1976. https://doi.org/10.1080/00343404.2014.883599 doi: 10.1080/00343404.2014.883599

|

| [43] |

Tsai IC (2018) The cause and outcomes of the ripple effect: housing prices and transaction volume. Ann Reg Sci 61: 351–373. https://doi.org/10.1007/s00168-018-0870-9 doi: 10.1007/s00168-018-0870-9

|

| [44] |

Tsai IC (2020) Market integration and volatility transmission in England's housing markets. Manch Sch 88: 119–155. https://doi.org/10.1111/manc.12272 doi: 10.1111/manc.12272

|

| [45] | Wheaton W, Lee N (2009) The Co-Movement of Housing Sales and Housing Prices: Empirics and Theory. Available from: https://economics.mit.edu/sites/default/files/2022-09/The%20co-movement%20of%20Housing%20Sales%20%26%20Housing%20Prices%20.pdf. |

Figures(4) / Tables(1)

David Gray. Housing market activity diffusion in England and Wales[J]. National Accounting Review, 2023, 5(2): 125-144. doi: 10.3934/NAR.2023008

DownLoad:

DownLoad: