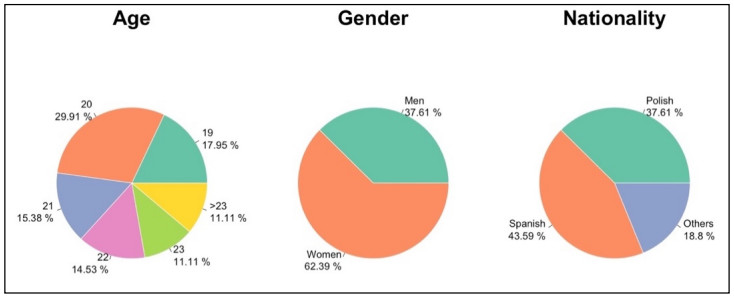

Green taxes are an instrument for the development of many destinations where overtourism generates different externalities, helping to alleviate them and create sustainable tourism. Funds raised through green taxes can be used to finance conservation, environmental restoration, and sustainable development initiatives. However, these taxes are often unknown to tourists visiting a city and can often generate mistrust and even discomfort when they are forced to pay them. In terms of the management implications for destinations, green taxes should be seen and conveyed as a means to achieve both economic and environmental sustainability of destinations and not yet another tax to be borne by the tourist. For this reason, the aim of this study is to explore the factors that affect both the positive attitude and the willingness to pay these taxes. Thus, the opinion about green taxes of 120 university students from different countries were collected to use a structural equation model (SEM) to try to provide answers to the different hypotheses put forward. Young people represent a growing part of the tourism market, shaping the trends and practices of the sector, making them central to the future of tourism. The study seeks to deepen theoretical knowledge on this subject and to provide a series of conclusions and recommendations for education regarding green taxes. In addition, our study on green taxes has a direct relationship with the sustainable development goals promulgated by the United Nations, as both seek to promote balanced economic, social, and environmental development.

Citation: Cristina Ortega-Rodríguez, Julio Vena-Oya, Jesús Barreal, Barbara Józefowicz. How to finance sustainable tourism: Factors influencing the attitude and willingness to pay green taxes among university students[J]. Green Finance, 2024, 6(4): 649-665. doi: 10.3934/GF.2024025

Green taxes are an instrument for the development of many destinations where overtourism generates different externalities, helping to alleviate them and create sustainable tourism. Funds raised through green taxes can be used to finance conservation, environmental restoration, and sustainable development initiatives. However, these taxes are often unknown to tourists visiting a city and can often generate mistrust and even discomfort when they are forced to pay them. In terms of the management implications for destinations, green taxes should be seen and conveyed as a means to achieve both economic and environmental sustainability of destinations and not yet another tax to be borne by the tourist. For this reason, the aim of this study is to explore the factors that affect both the positive attitude and the willingness to pay these taxes. Thus, the opinion about green taxes of 120 university students from different countries were collected to use a structural equation model (SEM) to try to provide answers to the different hypotheses put forward. Young people represent a growing part of the tourism market, shaping the trends and practices of the sector, making them central to the future of tourism. The study seeks to deepen theoretical knowledge on this subject and to provide a series of conclusions and recommendations for education regarding green taxes. In addition, our study on green taxes has a direct relationship with the sustainable development goals promulgated by the United Nations, as both seek to promote balanced economic, social, and environmental development.

| [1] | Ahmed N, Sheikh AA, Hamid Z, et al. (2022) Exploring the causal relationship among green taxes, energy intensity, and energy consumption in nordic countries: Dumitrescu and Hurlin causality approach. Energies 15: 5199. https://doi.org/10.3390/en15145199 |

| [2] | Bashir MF, Benjiang MA, Shahbaz M, et al. (2021) Unveiling the heterogeneous impacts of environmental taxes on energy consumption and energy intensity: empirical evidence from OECD countries. 226: 120366. https://doi.org/10.1016/j.energy.2021.120366 |

| [3] |

Becken S (2004) How tourists and tourism experts perceive climate change and carbon-offsetting schemes. J Sustain Tour 12: 332–345. https://doi.org/10.1080/09669580408667241 doi: 10.1080/09669580408667241

|

| [4] |

Behera P, Sethi N (2022) Nexus between environment regulation, FDI, and green technology innovation in OECD countries. Environ Sci Pollut R 29: 52940–52953. https://doi.org/10.1007/s11356-022-19458-7 doi: 10.1007/s11356-022-19458-7

|

| [5] |

Bentler PM, Bonett DG (1980) Significance tests and goodness of fit in the analysis of covariance structures. Psychol Bull 88: 588–606. https://doi.org/10.1037/0033-2909.88.3.588 doi: 10.1037/0033-2909.88.3.588

|

| [6] |

Berezan O, Raab C, Yoo M, et al. (2013) Sustainable hotel practices and nationality: The impact on guest satisfaction and guest intention to return. Int J Hosp Manag 34: 227–233. https://doi.org/10.1016/j.ijhm.2013.03.010 doi: 10.1016/j.ijhm.2013.03.010

|

| [7] |

Bhandari AK, Heshmati A (2010) Willingness to pay for biodiversity conservation. J Travel Tour Mark 27: 612–623. https://doi.org/10.1080/10548408.2010.507156 doi: 10.1080/10548408.2010.507156

|

| [8] | Browne MW (1993) Alternative ways of assessing model fit. Testing structural equation models. |

| [9] |

Cárdenas-García PJ, Sánchez-Rivero M, Pulido-Fernández JI (2015) Does Tourism Growth Influence Economic Development? J Travel Res 54: 206–221. https://doi.org/10.1177/0047287513514297 doi: 10.1177/0047287513514297

|

| [10] |

Cetin G, Alrawadieh Z, Dincer MZ, et al. (2017) Willingness to pay for tourist tax in destinations: Empirical evidence from Istanbul. Economies 5: 21. https://doi.org/10.3390/economies5020021 doi: 10.3390/economies5020021

|

| [11] | Chen G, Cheng M, Edwards D, et al. (2022) COVID-19 pandemic exposes the vulnerability of the sharing economy: a novel accounting framework. In Platform-Mediated Tourism, 213–230. Routledge. https://doi.org/10.4324/9781003230618-12 |

| [12] |

Chen JJ, Qiu RT, Jiao X, et al. (2023) Tax deduction or financial subsidy during crisis? Effectiveness of fiscal policies as pandemic mitigation and recovery measures. Annal Tourism Res Empir Insights 4: 100106. https://doi.org/10.1016/j.annale.2023.100106 doi: 10.1016/j.annale.2023.100106

|

| [13] |

Chen JM, Zhang J, Nijkamp P (2016) A regional analysis of willingness-to-pay in Asian cruise markets. Tourism Econ 22: 809–824. https://doi.org/10.1177/1354816616654254 doi: 10.1177/1354816616654254

|

| [14] |

Christensen N, Rothberger H, Wood W, et al. (2004) Social norms and identity relevance: a motivational approach to normative behaviour. Pers Soc Psychol B Pers Soc Psychol B 30: 1295–1309. https://doi.org/10.1177/0146167204264480 doi: 10.1177/0146167204264480

|

| [15] |

Chwialkowska A, Bhatti WA, Glowik M (2020) The influence of cultural values on pro-environmental behavior. J Clean Prod 268: 122305. https://doi.org/10.1016/j.jclepro.2020.122305 doi: 10.1016/j.jclepro.2020.122305

|

| [16] | Cohen J (1998) Statistical power analysis for the behavioural sciences, xxi. Hillsdale, NJ: L Erlbaum Associates. |

| [17] |

Do Valle PO, Pintassilgo P, Matias A (2012) Tourist attitudes towards an accommodation tax earmarked for environmental protection: A survey in the Algarve. Tourism Manage 33: 1408–1416. https://doi.org/10.1016/j.tourman.2012.01.003 doi: 10.1016/j.tourman.2012.01.003

|

| [18] |

Dolnicar S (2010) Identifying tourists with smaller environmental footprints. J Sustain Tour 18: 717–734. https://doi.org/10.1080/09669581003668516 doi: 10.1080/09669581003668516

|

| [19] |

Durán-Román JL, Cárdenas-García PJ, Pulido-Fernández JI (2020) Tourist tax to improve sustainability and the experience in mass tourism destinations: The case of andalusia (spain). Sustainability (Switzerland) 13: 1–20. https://doi.org/10.3390/su13010042 doi: 10.3390/su13010042

|

| [20] |

Durán-Román JL, Cárdenas-García PJ, Pulido-Fernández JI (2021) Tourists' willingness to pay to improve sustainability and experience at destination. J Destin Mark Manage 19: 100540. https://doi.org/10.1016/j.jdmm.2020.100540 doi: 10.1016/j.jdmm.2020.100540

|

| [21] | Durán-Román JL, Pulido-Fernández JI, Rey-Carmona FJ, et al. (2022) Willingness to Pay by Tourist Companies for Improving Sustainability and Competitiveness in a Mature Destination. Leisure Sci, 1–22. https://doi.org/10.1080/01490400.2022.2123072 |

| [22] |

Fairbrother M (2019) When will people pay to pollute? Environmental taxes, political trust and experimental evidence from Britain. Brit J Polit Sci 49: 661–682. https://doi.org/10.1017/S0007123416000727 doi: 10.1017/S0007123416000727

|

| [23] | Farhar BC, Houston AH (1996) Willingness to pay for electricity from renewable energy (No. NREL/TP-460-21216) National Renewable Energy Lab.(NREL), Golden, CO (United States). https://doi.org/10.2172/399985 |

| [24] |

Fekadu Z, Kraft P (2001) Self-identity in planned behavior perspective: Past behavior and its moderating effects on self-identity-intention relations. Soc Behav Personal 29: 671–685. https://doi.org/10.2224/sbp.2001.29.7.671 doi: 10.2224/sbp.2001.29.7.671

|

| [25] |

Filimonau V, Matute J, Mika M, et al. (2022) Predictors of patronage intentions towards 'green'hotels in an emerging tourism market. Int J Hosp Manag 103: 103221. https://doi.org/10.1016/j.ijhm.2022.103221 doi: 10.1016/j.ijhm.2022.103221

|

| [26] |

Foss AW, Ko Y (2019) Barriers and opportunities for climate change education: The case of Dallas-Fort Worth in Texas. J Environ Edu 50: 145–159. https://doi.org/10.1080/00958964.2019.1604479 doi: 10.1080/00958964.2019.1604479

|

| [27] | Gago A, Labandeira X, Picos F, et al. (2009) Specific and general taxation of tourism activities. Evidence from Spain. Tourism Manage 30: 381–392. https://doi.org/10.1016/j.tourman.2008.08.004 |

| [28] |

Glover P (2011) International students: Linking education and travel. J Travel Tour Mark 28: 180–195. https://doi.org/10.1080/10548408.2011.546210 doi: 10.1080/10548408.2011.546210

|

| [29] |

Göktaş L, Çetin G (2023) Tourist tax for sustainability: Determining willingness to pay. Eur J Tourism Res 35: 3503–3503. https://doi.org/10.54055/ejtr.v35i.2813 doi: 10.54055/ejtr.v35i.2813

|

| [30] | González-Rodríguez MR, Diaz-Fernandez MC, Font X (2019) Factors influencing willingness of customers of environmentally friendly hotels to pay a price premium. International. Int J Contemp Hosp M 32: 60–80. https://doi.org/10.1108/IJCHM-02-2019-0147 |

| [31] |

Gupta M (2016) Willingness to pay for carbon tax: A study of Indian road passenger transport. Transport Policy 45: 46–54. https://doi.org/10.1016/j.tranpol.2015.09.001 doi: 10.1016/j.tranpol.2015.09.001

|

| [32] |

Hair Jr JF, Matthews LM, Matthews RL, et al. (2017) PLS-SEM or CB-SEM: updated guidelines on which method to use. Int J Multivariate Data Anal 1: 107–123. https://doi.org/10.1504/IJMDA.2017.087624 doi: 10.1504/IJMDA.2017.087624

|

| [33] |

Han H, Hsu LTJ, Lee J S (2009) Empirical investigation of the roles of attitudes toward green behaviors, overall image, gender, and age in hotel customers' eco-friendly decision-making process. Int J Hosp Manag 28: 519–528. https://doi.org/10.1016/j.ijhm.2009.02.004 doi: 10.1016/j.ijhm.2009.02.004

|

| [34] |

Higueras-Castillo E, Liébana-Cabanillas FJ, Muñoz-Leiva F, et al. (2019) The role of collectivism in modeling the adoption of renewable energies: A cross-cultural approach. Int J Environ Sci Te 16: 2143–2160. https://doi.org/10.1007/s13762-019-02235-4 doi: 10.1007/s13762-019-02235-4

|

| [35] | Hofstede G (1980) Culture's consequences: International differences in work-related values (Vol. 5) sage. |

| [36] |

Hofstede G, Bond MH (1984) Hofstede's culture dimensions: An independent validation using Rokeach's Value Survey. J Cross-Cult Psychol 15: 417–433. https://doi.org/10.1177/0022002184015004003 doi: 10.1177/0022002184015004003

|

| [37] | Hofstede G, Hofstede GJ, Minkov M (2010) Cultures and organizations: Software of the mind (Vol. 2) New York: Mcgraw-hill. |

| [38] |

Ilić B, Stojanovic D, Djukic G (2019) Green economy: mobilization of international capital for financing projects of renewable energy sources. Green Financ 1: 94–109. https://doi.org/10.3934/GF.2019.2.94 doi: 10.3934/GF.2019.2.94

|

| [39] |

Ivanov S, Seyitoğlu F, Webster C (2024) Tourism, automation and responsible consumption and production: a horizon 2050 paper. Tourism Rev. https://doi.org/10.1108/TR-12-2023-0898 doi: 10.1108/TR-12-2023-0898

|

| [40] |

Johnson D (2002) Environmentally sustainable cruise tourism: A reality check. Marine Policy 26: 261–270. https://doi.org/10.1016/S0308-597X(02)00008-8 doi: 10.1016/S0308-597X(02)00008-8

|

| [41] |

Kato A, Kwak S, Mak J (2011) Using the property tax to appropriate gains from tourism. J Travel Res 50: 144–153. https://doi.org/10.1177/0047287510362783 doi: 10.1177/0047287510362783

|

| [42] |

Khan O, Varaksina N, Hinterhuber A (2024) The influence of cultural differences on consumers' willingness to pay more for sustainable fashion. J Clean Prod 442: 141024. https://doi.org/10.1016/j.jclepro.2024.141024 doi: 10.1016/j.jclepro.2024.141024

|

| [43] | Kline RB (2023) Principles and practice of structural equation modeling. Guilford publications. |

| [44] | Kumar R, Philip PJ, Sharma C (2014) Attitude–value construct: A review of green buying behaviour. Pac Bus Rev Int 6: 25–30. |

| [45] |

Li Y, Zhou M, Sun H, et al. (2023) Assessment of environmental tax and green bonds impacts on energy efficiency in the European Union. Econ Chang Restruct 56: 1063–1081. https://doi.org/10.1007/s10644-022-09465-6 doi: 10.1007/s10644-022-09465-6

|

| [46] |

Logar I (2010) Sustainable tourism management in Crikvenica, Croatia: An assessment of policy instruments. Tourism Manage 31: 125–135. https://doi.org/10.1016/j.tourman.2009.02.005 doi: 10.1016/j.tourman.2009.02.005

|

| [47] |

Malerba D (2022) The effects of social protection and social cohesion on the acceptability of climate change mitigation policies: what do we (not) know in the context of low-and middle-income countries? Eur J Dev Res 34: 1358. https://doi.org/10.1057/s41287-022-00537-x doi: 10.1057/s41287-022-00537-x

|

| [48] |

McCarty JA, Shrum LJ (2001) The influence of individualism, collectivism, and locus of control on environmental beliefs and behavior. J Public Policy Market 20: 93–104. https://doi.org/10.1509/jppm.20.1.93.1729 doi: 10.1509/jppm.20.1.93.1729

|

| [49] |

Mehmetoglu M (2010) Factors influencing the willingness to behave environmentally friendly at home and holiday settings. Scand J Hosp Tour 10: 430–447. https://doi.org/10.1080/15022250.2010.520861 doi: 10.1080/15022250.2010.520861

|

| [50] |

Meo M, Karim M (2022) The role of green finance in reducing CO2 emissions: An empirical analysis. Borsa Istanb Rev 22: 169–178. https://doi.org/10.1016/j.bir.2021.03.002 doi: 10.1016/j.bir.2021.03.002

|

| [51] |

Mihalič T (2000) Environmental management of a tourist destination: A factor of tourism competitiveness. Tourism Manage 21: 65–78. https://doi.org/10.1016/S0261-5177(99)00096-5 doi: 10.1016/S0261-5177(99)00096-5

|

| [52] |

Milfont TL, Duckitt J (2010) The environmental attitudes inventory: A valid and reliable measure to assess the structure of environmental attitudes. J Environ Psychol 30: 80–94. https://doi.org/10.1016/j.jenvp.2009.09.001 doi: 10.1016/j.jenvp.2009.09.001

|

| [53] | Nunnally JC (1994) The assessment of reliability. Psychometric theory. |

| [54] |

Oklevik O, Gössling S, Hall CM, et al. (2019) Overtourism, optimisation, and destination performance indicators: a case study of activities in Fjord Norway. J Sustain Tour 27: 1804–1824. https://doi.org/10.1080/09669582.2018.1533020 doi: 10.1080/09669582.2018.1533020

|

| [55] |

Oliver JD (2013) Promoting sustainability by marketing green products to non-adopters. Gestion 2000 30: 77–86. https://doi.org/10.3917/g2000.303.0077 doi: 10.3917/g2000.303.0077

|

| [56] |

Owen AL, Videras J (2006) Civic cooperation, pro-environment attitudes, and behavioral intentions. Ecol Econ 58: 814–829. https://doi.org/10.1016/j.ecolecon.2005.09.007 doi: 10.1016/j.ecolecon.2005.09.007

|

| [57] | Perman R, Ma Y, McGilvray J, et al. (1999) Natural resource and environmental economics. Pearson Education. |

| [58] | Raisová M (2012) The implementation of green taxes into the economics. Proc. of the 12th International Multidisciplinary Scientific Geoconference, IV, 1153–1160. |

| [59] |

Reynisdottir M, Song H, Agrusa J (2008) Willingness to pay entrance fees to natural attractions: An Icelandic case study. Tourism Manage 29: 1076–1083. https://doi.org/10.1016/j.tourman.2008.02.016 doi: 10.1016/j.tourman.2008.02.016

|

| [60] |

Ripinga BB, Mazenda A, Bello FG (2024) Tourism levy collection for 'Marketing South Africa'. Cogent Social Sci 10: 2364765. https://doi.org/10.1080/23311886.2024.2364765 doi: 10.1080/23311886.2024.2364765

|

| [61] |

Rotaris L, Carrozzo M (2019) Tourism taxes in Italy: A sustainable perspective. J Global Bus Insights 4: 92–105. https://doi.org/10.5038/2640-6489.4.2.1079 doi: 10.5038/2640-6489.4.2.1079

|

| [62] | Rotaris L (2022) Tourist taxes in Italy: The choices of the policy makers and the preferences of tourists. Scienze Regionali 21: 199–228. |

| [63] | Ru X, Qin H, Wang S (2019) Young people's behaviour intentions towards reducing PM2. 5 in China: Extending the theory of planned behaviour. Resour Conserv Recy 141: 99–108. https://doi.org/10.1016/j.resconrec.2018.10.019 |

| [64] |

Rustam A, Wang Y, Zameer H (2020) Environmental awareness, firm sustainability exposure and green consumption behaviors. J Clean Prod 268, 122016. https://doi.org/10.1016/j.jclepro.2020.122016 doi: 10.1016/j.jclepro.2020.122016

|

| [65] |

Ryan C, Zhang Z (2007) Chinese students: holiday behaviours in New Zealand. J Vacat Market 13: 91–105. https://doi.org/10.1177/1356766707074734 doi: 10.1177/1356766707074734

|

| [66] | Sabiote-Ortiz CM (2010) Valor percibido global del proceso de decisión de compra online de un producto turístico. Efecto moderador de la cultura (Doctoral dissertation, Universidad de Granada). |

| [67] |

Schuhmann PW, Skeete R, Waite R, et al. (2019) Visitors' willingness to pay marine conservation fees in Barbados. Tourism Manage 71: 315–326. https://doi.org/10.1016/j.tourman.2018.10.011 doi: 10.1016/j.tourman.2018.10.011

|

| [68] | Sharma MN, Singh S (2022) Role of Collectivism and Consumer Trust in Making Consumer Attitude Towards Green Products. J Positive School Psychol 6: 3580–3588. |

| [69] | Shehawy YM, Agag G, Alamoudi HO, et al. (2024) Cross-national differences in consumers' willingness to pay (WTP) more for green hotels. J Retail Consum Serv 77: 103665. |

| [70] |

Sineviciene L, Sotnyk I, Kubatko O (2017) Determinants of energy efficiency and energy consumption of Eastern Europe post-communist economies. Energ Environ 28: 870–884. https://doi.org/10.1177/0958305X17734386 doi: 10.1177/0958305X17734386

|

| [71] |

Sullivan JH, Warkentin M, Wallace L (2021) So many ways for assessing outliers: What really works and does it matter? J Bus Res 132: 530–543. https://doi.org/10.1016/j.jbusres.2021.03.066 doi: 10.1016/j.jbusres.2021.03.066

|

| [72] |

Sundt S, Rehdanz K (2015) Consumers' willingness to pay for green electricity: A meta-analysis of the literature. Energ Econ 51: 1–8. https://doi.org/10.1016/j.eneco.2015.06.005 doi: 10.1016/j.eneco.2015.06.005

|

| [73] |

Taghizadeh-Hesary F, Yoshino N (2019) The way to induce private participation in green finance and investment. Financ Res Lett 31: 98–103. https://doi.org/10.1016/j.frl.2019.04.016 doi: 10.1016/j.frl.2019.04.016

|

| [74] |

Taylor R, Shanka T, Pope J (2004) Investigating the significance of VFR visits to international students. J Market High Educ 14: 61–77. https://doi.org/10.1300/J050v14n01_04 doi: 10.1300/J050v14n01_04

|

| [75] |

Tran MN, Moore K, Shone MC (2018) Interactive mobilities: Conceptualising VFR tourism of international students. J Hosp Tourism Manage 35: 85–91. https://doi.org/10.1016/j.jhtm.2018.04.002 doi: 10.1016/j.jhtm.2018.04.002

|

| [76] |

Tsai WT (2024) Green finance for mitigating greenhouse gases and promoting renewable energy development: Case study in Taiwan. Green Financ 6: 249–264. https://doi.org/10.3934/GF.2024010 doi: 10.3934/GF.2024010

|

| [77] | United Nations (2022) Department of Economic and Social Affairs. Sustainable Development. Available from: https://sdgs.un.org/goals/goal12. |

| [78] |

Wang Y, Liu J, Yang X, et al. (2023) The mechanism of green finance's impact on enterprises' sustainable green innovation. Green Financ 5: 452–478. https://doi.org/10.3934/GF.2023018 doi: 10.3934/GF.2023018

|

| [79] |

Whitmarsh L, O'Neill S (2010) Green identity, green living? The role of pro-environmental self-identity in determining consistency across diverse pro-environmental behaviours. J Environ Psychol 30: 305–314. https://doi.org/10.1016/j.jenvp.2010.01.003 doi: 10.1016/j.jenvp.2010.01.003

|

| [80] |

Xiong W, Huang M, Leung XY, et al. (2023) How environmental emotions link to responsible consumption behavior: tourism agenda 2030. Tourism Rev 78: 517–530. https://doi.org/10.1108/TR-01-2022-0010 doi: 10.1108/TR-01-2022-0010

|

| [81] |

Yang M, Chen H, Long R, et al. (2022) The impact of different regulation policies on promoting green consumption behavior based on social network modeling. Sustain Prod Consump 32: 468–478. https://doi.org/10.1016/j.spc.2022.05.007 doi: 10.1016/j.spc.2022.05.007

|

| [82] |

Zaman K, Awan U, Islam T, et al. (2016) Econometric applications for measuring the environmental impacts of biofuel production in the panel of worlds' largest region. Int J Hydrogen Energ 41: 4305–4325. https://doi.org/10.1016/j.ijhydene.2016.01.053 doi: 10.1016/j.ijhydene.2016.01.053

|

| [83] |

Zaman KAU (2023) Financing the SDGs: How Bangladesh May Reshape Its Strategies in the Post-COVID Era? Eur J Dev Res 35: 51. https://doi.org/10.1057/s41287-022-00556-8 doi: 10.1057/s41287-022-00556-8

|

Figures(2) / Tables(3)

Cristina Ortega-Rodríguez, Julio Vena-Oya, Jesús Barreal, Barbara Józefowicz. How to finance sustainable tourism: Factors influencing the attitude and willingness to pay green taxes among university students[J]. Green Finance, 2024, 6(4): 649-665. doi: 10.3934/GF.2024025

DownLoad:

DownLoad: