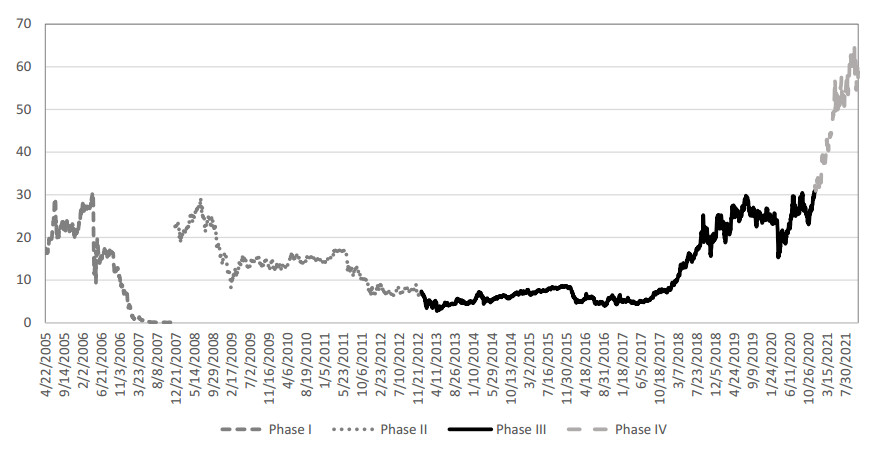

This paper explores the role of European Union Allowances (EUAs) as a safe haven for a range of assets and analyses the effect of safe-haven flows on the European carbon futures market. In particular, we demonstrate that EUAs can be considered a refuge against fluctuations in corporate bonds, gold and volatility-related assets in periods of market turmoil. Furthermore, we have shown that extremely bearish and bullish movements in those assets for which the EUA acts as a safe haven induce excess volatility in carbon markets, higher carbon trading volume and larger than normal EUA bid-ask spreads. These findings support the idea that some traders, by considering carbon futures as a refuge asset, induce safe-haven flows into the carbon market. The presence of these flows provides additional insights into the financialisation of the European carbon futures market.

Citation: Fernando Palao, Ángel Pardo. Carbon and safe-haven flows[J]. Green Finance, 2022, 4(4): 474-491. doi: 10.3934/GF.2022023

This paper explores the role of European Union Allowances (EUAs) as a safe haven for a range of assets and analyses the effect of safe-haven flows on the European carbon futures market. In particular, we demonstrate that EUAs can be considered a refuge against fluctuations in corporate bonds, gold and volatility-related assets in periods of market turmoil. Furthermore, we have shown that extremely bearish and bullish movements in those assets for which the EUA acts as a safe haven induce excess volatility in carbon markets, higher carbon trading volume and larger than normal EUA bid-ask spreads. These findings support the idea that some traders, by considering carbon futures as a refuge asset, induce safe-haven flows into the carbon market. The presence of these flows provides additional insights into the financialisation of the European carbon futures market.

| [1] |

Ahmad W, Sadorsky P, Sharma A (2018) Optimal hedge ratios for clean energy equities. Econ Model 72: 278–295. https://doi.org/10.1016/j.econmod.2018.02.008 doi: 10.1016/j.econmod.2018.02.008

|

| [2] | Baur DG, Dimpfl T, Kuck K (2021) Safe Haven Assets-The Bigger Picture. Available from: http://dx.doi.org/10.2139/ssrn.3800872 |

| [3] |

Baur DG, Lucey BM (2010) Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold. Finan Rev 45: 217–229. https://doi.org/10.1111/j.1540-6288.2010.00244.x doi: 10.1111/j.1540-6288.2010.00244.x

|

| [4] |

Baur DG, McDermott TK (2010) Is gold a safe haven? International evidence. J Bank Financ 34: 1886–1898. https://doi.org/10.1016/j.jbankfin.2009.12.008 doi: 10.1016/j.jbankfin.2009.12.008

|

| [5] | Carchano Ó, Medina V, Pardo Á (2014) Assessing rollover criteria for EUAs and CERs. Int J Econ Financ Issues 4: 669–676. https://dergipark.org.tr/en/pub/ijefi/issue/31963/352037?publisher=http-www-cag-edu-tr-ilhan-ozturk |

| [6] |

Chevallier J (2009a) Energy risk management with carbon assets. Int J Global Energy 32: 328–349. https://doi.org/10.1504/IJGEI.2009.032335 doi: 10.1504/IJGEI.2009.032335

|

| [7] |

Chevallier J (2009b) Carbon futures and macroeconomic risk factors: A view from the EU ETS. Energ Econ 31: 614–625. https://doi.org/10.1016/j.eneco.2009.02.008 doi: 10.1016/j.eneco.2009.02.008

|

| [8] |

Conlon T, McGee R (2020) Safe haven or risky hazard? Bitcoin during the COVID-19 bear market. Finan Res Lett 35: 101607. https://doi.org/10.1016/j.frl.2020.101607 doi: 10.1016/j.frl.2020.101607

|

| [9] | Davino C, Furno M, Vistocco D (2014) Quantile regression: Theory and Applications. JWS, West Sussex. |

| [10] |

Demiralay S, Gencer HG, Bayraci S (2022) Carbon credit futures as an emerging asset: Hedging, diversification and downside risks. Energ Econ 113: 106196. https://doi.org/10.1016/j.eneco.2022.106196 doi: 10.1016/j.eneco.2022.106196

|

| [11] |

Dutta A, Das D, Jana RK, et al. (2020) COVID-19 and oil market crash: Revisiting the safe haven property of gold and Bitcoin. Resour Policy 69: 101816. https://doi.org/10.1016/j.resourpol.2020.101816 doi: 10.1016/j.resourpol.2020.101816

|

| [12] | ESMA (2021) Emission Allowances and Derivatives Thereof. Paris, Preliminary Report, 15 November 2021. Available from: https://www.esma.europa.eu/sites/default/files/library/esma70-445-7_preliminary_report_on_emission_allowances.pdf |

| [13] |

Gronwald M, Ketterer J, Trück S (2011) The relationship between carbon, commodity and financial markets: A copula analysis. Energ Econ 87: 105–124. https://doi.org/10.1111/j.1475-4932.2011.00748.x doi: 10.1111/j.1475-4932.2011.00748.x

|

| [14] |

Kaul A, Sapp S (2006) Y2K fears and safe haven trading of the US dollar. J Int Money Financ 25: 760–779. https://doi.org/10.1016/j.jimonfin.2006.04.003 doi: 10.1016/j.jimonfin.2006.04.003

|

| [15] |

Koenker R, Bassett G (1978) Regression Quantiles. Econometrica 46: 33–50. https://doi.org/10.2307/1913643 doi: 10.2307/1913643

|

| [16] |

Lovcha Y, Perez-Laborda A, Sikora I (2022) The determinants of CO2 prices in the EU emission trading system. Appl Energ 305: 117903. https://doi.org/10.1016/j.apenergy.2021.117903 doi: 10.1016/j.apenergy.2021.117903

|

| [17] |

Luo C, Wu D (2016) Environment and economic risk: An analysis of carbon emission market and portfolio management. Environ Res 149: 297–301. https://doi.org/10.1016/j.envres.2016.02.007 doi: 10.1016/j.envres.2016.02.007

|

| [18] |

Mansanet-Bataller M, Pardo Á (2011) CO2 prices and portfolio management. Int J Global Energy 35: 158–177. https://doi.org/10.1504/IJGEI.2011.045028 doi: 10.1504/IJGEI.2011.045028

|

| [19] |

Palao F, Pardo Á (2021) The inconvenience yield of carbon futures. Energ Econ 101: 105461. https://doi.org/10.1016/j.eneco.2021.105461 doi: 10.1016/j.eneco.2021.105461

|

| [20] |

Palao F, Pardo Á, Roig M (2020) Is the leadership of the Brent-WTI threatened by China's new crude oil futures market? J Asian Econ 70: 101237. https://doi.org/10.1016/j.asieco.2020.101237 doi: 10.1016/j.asieco.2020.101237

|

| [21] |

Pardo Á (2021) Carbon and inflation. Finan Res Lett 38: 101519. https://doi.org/10.1016/j.frl.2020.101519 doi: 10.1016/j.frl.2020.101519

|

| [22] | Parkinson M (1980) The extreme value method for estimating the variance of the rate of return. J Bus 53: 61–65. http://www.jstor.org/stable/2352357 |

| [23] | Quemin S, Pahle M (2022) Financials threaten to undermine the functioning of emissions markets. Available from: http://dx.doi.org/10.2139/ssrn.3985079 |

| [24] |

Reboredo JC (2013) Modeling EU allowances and oil market interdependence. Implications for portfolio management. Energ Econ 36: 471–480. https://doi.org/10.1016/j.eneco.2012.10.004 doi: 10.1016/j.eneco.2012.10.004

|

| [25] |

Smales LA (2019) Bitcoin as a safe haven: Is it even worth considering? Financ Res Lett 30: 385–393. https://doi.org/10.1016/j.frl.2018.11.002 doi: 10.1016/j.frl.2018.11.002

|

| [26] |

Uddin GS, Hernandez JA, Shahzad SJH, et al. (2018) Multivariate dependence and spillover effects across energy commodities and diversification potentials of carbon assets. Energ Econ 71: 35–46. https://doi.org/10.1016/j.eneco.2018.01.035 doi: 10.1016/j.eneco.2018.01.035

|

| [27] |

Yang L, Hamori S (2021) The role of the carbon market in relation to the cryptocurrency market: Only diversification or more? Int Rev Financ Anal 77: 101864. https://doi.org/10.1016/j.irfa.2021.101864 doi: 10.1016/j.irfa.2021.101864

|

| [28] |

Wen F, Tong X, Ren X (2022) Gold or Bitcoin, which is the safe haven during the COVID-19 pandemic? Int Rev Financ Anal 81: 102121. https://doi.org/10.1016/j.irfa.2022.102 doi: 10.1016/j.irfa.2022.102

|

Figures(1) / Tables(5)

Fernando Palao, Ángel Pardo. Carbon and safe-haven flows[J]. Green Finance, 2022, 4(4): 474-491. doi: 10.3934/GF.2022023

DownLoad:

DownLoad: