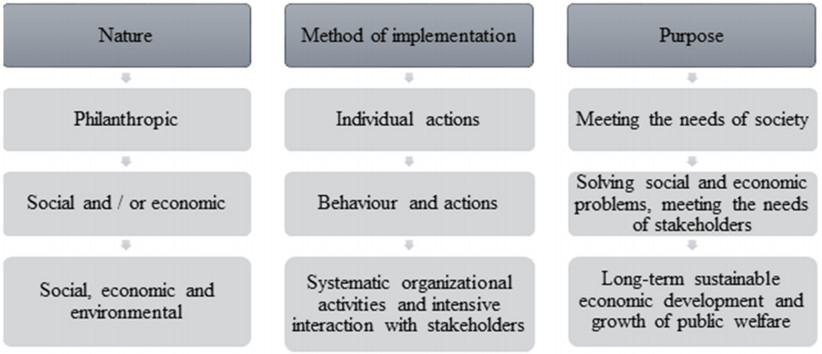

The purpose of the paper is to analyse the development of the concept of corporate social responsibility (CSR) between two the most drastic crisis periods that have shaken the world society, i.e., the Great Depression and the COVID-19 pandemic. The concept of CSR has expanded from its perception as philanthropic actions to the systematic corporate activities and intensive interaction with stakeholders based on social, economic, and environmental interests aimed at long-term sustainable economic development and public welfare. With the rapid spread of the COVID-19 around the world, the companies have faced the challenge of moving to a new environment. Our findings suggest that CSR activities are implemented by the companies around the world as a response to the COVID-19, regardless of the country's level of development. The companies with many years of CSR experience act responsibly towards their communities and society. The concept of CSR is still evolving, but the main goal remains the same at any stage of development—to contribute to public safety and well-being. The results show that the companies, analysed in the paper, contribute to the implementation of CSR goals through socially responsible activities even in the crisis period.

Citation: Valentinas Navickas, Rima Kontautiene, Jurgita Stravinskiene, Yuriy Bilan. Paradigm shift in the concept of corporate social responsibility: COVID-19[J]. Green Finance, 2021, 3(2): 138-152. doi: 10.3934/GF.2021008

The purpose of the paper is to analyse the development of the concept of corporate social responsibility (CSR) between two the most drastic crisis periods that have shaken the world society, i.e., the Great Depression and the COVID-19 pandemic. The concept of CSR has expanded from its perception as philanthropic actions to the systematic corporate activities and intensive interaction with stakeholders based on social, economic, and environmental interests aimed at long-term sustainable economic development and public welfare. With the rapid spread of the COVID-19 around the world, the companies have faced the challenge of moving to a new environment. Our findings suggest that CSR activities are implemented by the companies around the world as a response to the COVID-19, regardless of the country's level of development. The companies with many years of CSR experience act responsibly towards their communities and society. The concept of CSR is still evolving, but the main goal remains the same at any stage of development—to contribute to public safety and well-being. The results show that the companies, analysed in the paper, contribute to the implementation of CSR goals through socially responsible activities even in the crisis period.

| [1] | Aguinis H (2011) Organizational responsibility: doing good and doing well, In: Zedeck S. APA Handbook of Industrial and Organizational Psychology. Eds., Washington: American Psychological Association, 855–879. |

| [2] |

Anderson CL, Bieniaszewska RL (2005) The role of corporate social responsibility in an oil company's expansion into new territories. Corp Soc Responsib Environ Manage 12: 1–9. doi: 10.1002/csr.71

|

| [3] |

Berle AA (1932) For whom corporate managers are trustees: A note. Harvard Law Rev 45: 1365–1372. doi: 10.2307/1331920

|

| [4] |

Bird R, Hall AD, Momente F, et al. (2007) What corporate social responsibility activities are valued by the market? J Bus Ethics 76: 189–206. doi: 10.1007/s10551-006-9268-1

|

| [5] |

Blowfield M, Frynas JG (2005) Editorial setting new agendas: critical perspectives on corporate social responsibility in the developing world. Int Affair 81: 499–513. doi: 10.1111/j.1468-2346.2005.00465.x

|

| [6] | Boal KB, Peery N (1985) The cognitive structure of corporate social responsibility. J Manage 11: 71–82. |

| [7] | Bowen HR (2013) Social Responsibilities of the Businessman, Iowa: University of Iowa Press. |

| [8] |

Bryane M (2003) Corporate social responsibility in international development: An overview and critique. Corp Soc Responsib Environ Manage 10: 115–128. doi: 10.1002/csr.41

|

| [9] | Carlsen L (2021) Responsible consumption and production in the European Union. A partial order analysis of Eurostat SDG 12 data. Green Financ 3: 28–45. |

| [10] |

Carroll AB (1979) A three-dimensional conceptual model of corporate performance. Acad Manage Rev 4: 497–505. doi: 10.5465/amr.1979.4498296

|

| [11] | Carroll AB (1991) The pyramid of corporate social responsibility: toward the moral management of organizational stakeholders. Bus Horiz 34: 39–48. |

| [12] |

Carroll AB (1999) Corporate social responsibility: evolution of a definitional construct. Bus Soc 38: 268–295. doi: 10.1177/000765039903800303

|

| [13] |

Carroll AB, Shabana KM (2010) The business case for corporate social responsibility: a review of concepts, research and practice. Int J Manage Rev 12: 85–105. doi: 10.1111/j.1468-2370.2009.00275.x

|

| [14] |

Chalmers DM (1959) The muckrakers and the growth of corporate power: a study in constructive journalism. Am J Econ Sociol 18: 295–311. doi: 10.1111/j.1536-7150.1959.tb00326.x

|

| [15] | Chakraborty UK (2015) Developments in the concept of corporate social responsibility (CSR). J Res 1: 23–45. |

| [16] | Crane A, McWilliams A, Matten D, et al. (2008) The corporate social responsibility agenda, In: Crane A, McWilliams A, Matten D, Moon J, Siegel D, The Oxford Handbook of Corporate Social Responsibility Eds., Oxford: Oxford University Press, 3–18. |

| [17] | Crane A, Matten D (2020) COVID-19 and the future of CSR research. J Manage Stud. |

| [18] |

Dahlsrud A (2008) How corporate social responsibility is defined: an analysis of 37 definitions. Corp Soc Responsib Environ Manage 15: 1–13. doi: 10.1002/csr.132

|

| [19] | Davis K (1960) Can business afford to ignore social responsibilities? Calif Manage Rev 2: 70–76. |

| [20] | Davis K (1973) The case for and against business assumption of social responsibilities. Acad Manage J 16: 312–322. |

| [21] |

Devinney TM (2009) Is the socially responsible corporation a myth? The good, the bad, and the ugly of corporate social responsibility. Acad Manage Perspect 23: 44–56. doi: 10.5465/amp.2009.39985540

|

| [22] |

Dobers P, Springett D (2010) Corporate social responsibility: discourse, narratives and communication. Corp Soc Responsib Environ Manage 17: 63–69. doi: 10.1002/csr.231

|

| [23] | Dunbar C, Li ZF, Shi Y (2020) CEO risk-taking incentives and corporate social responsibility. J Corp Financ 64: 1–21. |

| [24] | Dunbar C, Li ZF, Shi Y (2021) Corporate social (ir) responsibility and firm risk: the role of corporate governance. Available from: http://dx.doi.org/10.2139/ssrn.3791594. |

| [25] |

Eells R (1958) Corporate giving: theory and policy. Calif Manage Rev 1: 37–46. doi: 10.2307/41165333

|

| [26] | Euronews (2020) COVID-19: World economy in 2020 to suffer worst year since 1930s Great Depression, says IMF. Available from: https://www.euronews.com/2020/04/14/watch-live-international-monetary-fund-gives-world-economic-outlook-briefing-on-covid-19. |

| [27] | Frederick WC (2006) Corporation be Good! The Story of Corporate Social Responsibility, Indianapolis: Dog Ear Publishing. |

| [28] | Friedman M (2002) Capitalism and Freedom, Chicago: University of Chicago Press. |

| [29] |

Gavin JF, Maynard WS (1975) Perceptions of corporate social responsibility. Personnel Psychol 28: 377–387. doi: 10.1111/j.1744-6570.1975.tb01545.x

|

| [30] |

Ghosh S (2020) Asymmetric impact of COVID-19 induced uncertainty on inbound Chinese tourists in Australia: insights from nonlinear ARDL model. Quant Financ Econ 4: 343–364. doi: 10.3934/QFE.2020016

|

| [31] |

Gjolberg M (2009) Measuring the immeasurable? Constructing an index of CSR practices and CSR performance in 20 countries. Scand J Manage 25: 10–22. doi: 10.1016/j.scaman.2008.10.003

|

| [32] | Graham JR, Narasimhan K (2004). Corporate survival and managerial experiences during the Great Depression. Available from: https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.217.8670&rep=rep1&type=pdf. |

| [33] |

Jeris SS, Nath RD (2020) Covid-19, oil price and UK economic policy uncertainty: evidence from the ARDL approach. Quant Financ Econ 4: 503–514. doi: 10.3934/QFE.2020023

|

| [34] | Johnson HL (1971) Business in Contemporary Society: Framework and Issues, Belmont: Wadsworth Pub. Co. |

| [35] |

Jones TM (1980) Corporate social responsibility revisited, redefined. Calif Manage Rev 22: 59–67. doi: 10.2307/41164877

|

| [36] |

Halme M, Roome N, Dobers P (2009) Corporate responsibility: reflections on context and consequences. Scand J Manage 25: 1–9. doi: 10.1016/j.scaman.2008.12.001

|

| [37] |

Hediger W (2010) Welfare and capital-theoretic foundations of corporate social responsibility and corporate sustainability. J Socio Econ 39: 518–526. doi: 10.1016/j.socec.2010.02.001

|

| [38] |

Hong M, Drakeford B, Zhang K (2020) The impact of mandatory CSR disclosure on green innovation: evidence from China. Green Financ 2: 302–322. doi: 10.3934/GF.2020017

|

| [39] | Ketola T (2007) Responsible communication as an integrator: discourses linking values to actions, In: Parrish LA, Business Ethics in Focus. Eds., New York: Nova Science Publishers, 289–303. |

| [40] |

Ketola T (2010) Five leaps to corporate sustainability through corporate responsibility portfolio matrix. Corp Soc Responsib Environ Manage 17: 320–336. doi: 10.1002/csr.219

|

| [41] |

Kolk A, van Tulder R (2009) International business, corporate social responsibility and sustainable development. Int Bus Rev 19: 119–125. doi: 10.1016/j.ibusrev.2009.12.003

|

| [42] | Korhonen J (2003) Should we measure corporate social responsibility? Corp Soc Responsib Environ Manage 10: 25–39. |

| [43] | Lee MDP (2008) A review of the theories of corporate social responsibility: its evolutionary path and the road ahead. Int J Manage Rev 10: 57–73. |

| [44] | Levitt T (1958) The dangers of social responsibility. Harvard Bus Rev 36: 41–50. |

| [45] | Li K, Liu X, Mai F, et al. (2020) The role of corporate culture in bad times: evidence from the COVID-19 pandemic, In: Wyplosz C, Covid Economics, Vetted and Real-Time Papers, The Centre for Economic Policy Research (CEPR), 61–109. |

| [46] | Li ZF (2018) A survey of corporate social responsibility and corporate governance, In: Boubaker S, Cumming D, Nguyen DK, Research Handbook of Finance and Sustainability, Eds., Cheltenham: Edward Elgar Publishing, 126–138. |

| [47] | Li ZF, Patel S, Ramani S (2020) The role of mutual funds in corporate social responsibility. J Bus Ethics. Available from: https://link.springer.com/content/pdf/10.1007%2Fs10551-020-04618-x.pdf. |

| [48] |

Lim JS, Greenwood CA (2017) Communicating corporate social responsibility (CSR): stakeholder responsiveness and engagement strategy to achieve CSR goals. Public Relations Rev 43: 768–776. doi: 10.1016/j.pubrev.2017.06.007

|

| [49] |

Maignan I, Ralston D (2002) Corporate social responsibility in Europe and the US: insights from businesses' self-presentation. J Int Bus Stud 33: 498–514. doi: 10.1057/palgrave.jibs.8491028

|

| [50] |

Malik AS (2019) Cost-Benefit analysis in the context of long horizon projects-a need for a social and holistic approach. Green Financ 1: 249–263. doi: 10.3934/GF.2019.3.249

|

| [51] | Manne HG, Wallich HC (1972) The Modern Corporation and Social Responsibility, Washington: American Enterprise Institute for Public Policy Research. |

| [52] |

McWilliams A, Siegel DS (2001) Corporate social responsibility: a theory of firm perspective. Acad Manage Rev 26: 117–127. doi: 10.5465/amr.2001.4011987

|

| [53] |

Melo T, Garrido-Morgado A (2012) Corporate reputation: a combination of social responsibility and industry. Corp Soc Responsib Environ Manage 19: 11–31. doi: 10.1002/csr.260

|

| [54] |

Nijhof A, Fisscher O, Looise JK (2002) Inclusive innovation: a research project on the inclusion of social responsibility. Corp Soc Responsib Environ Manage 9: 83–90. doi: 10.1002/csr.10

|

| [55] | Pappas N (2014) Marketing hospitality industry in an era of crisis. Tourism Plan Dev12: 333–349. |

| [56] | Porter ME, Kramer MR (2006) Strategy and society: The link between competitive advantage and corporate social responsibility. Harvard Bus Rev 84: 78–92. |

| [57] | Preston LE, Post JE (1975) Private Management and Public Policy: The Principle of Public Responsibility, Englewood Cliffs: Prentice-Hall. |

| [58] | Report of the World Commission on Environment and Development: Our common future, 1987. Available from: https://sustainabledevelopment.un.org/content/documents/5987our-common-future.pdf. |

| [59] |

Sadler D, Lloyda D (2009) Neo-liberalising corporate social responsibility: a political economy of corporate citizenship. Geoforum 40: 613–622. doi: 10.1016/j.geoforum.2009.03.008

|

| [60] |

Sethi SP (1975) Dimensions of corporate social performance: an analytical framework. Calif Manage Rev 17: 58–64. doi: 10.2307/41162149

|

| [61] |

Şimsek H, Ozturk G (2021) Evaluation of the relationship between environmental accounting and business performance: the case of Istanbul province. Green Financ 3: 46–58. doi: 10.3934/GF.2021004

|

| [62] | Steiner GA (1971) Business and Society. New York: Random House. |

| [63] |

Sukharev O (2020) Economic crisis as a consequence COVID-19 virus attack: risk and damage assessment. Quant Financ Econ 4: 274–293. doi: 10.3934/QFE.2020013

|

| [64] |

Utomo MN, Rahayu S, Kaujan K, et al. (2020) Environmental performance, environmental disclosure, and firm value: empirical study of non-financial companies at Indonesia Stock Exchange. Green Financ 2: 100–113. doi: 10.3934/GF.2020006

|

| [65] | Vogel D (2006) The market for virtue: The Potential and Limits of Corporate Social Responsibility, Washington: Publisher Brookings Institution Press. |

| [66] |

Wartick SL, Cochran PL (1985) The evolution of the corporate social performance model. Acad Manage Rev10: 758–769. doi: 10.5465/amr.1985.4279099

|

| [67] | WBCSD Report: Corporate Social Responsibility. The WBCSD's journey, 2002. Available from: https://www.globalhand.org/system/assets/f65fb8b06bddcf2f2e5fef11ea7171049f223d85/original/Corporate_Social_Responsability_WBCSD_2002.pdf. |

| [68] |

Wood DJ (1991) Corporate social performance revisited. Acad Manage Rev 16: 691–718. doi: 10.5465/amr.1991.4279616

|

| [69] |

Zenisek TJ (1979) Corporate social responsibility: a conceptualization based on organizational literature. Acad Manage Rev 4: 359–368. doi: 10.5465/amr.1979.4289095

|

| [70] |

Zink KJ (2005) Stakeholder orientation and corporate social responsibility as a precondition for sustainability. Total Qual Manage 16: 1041–1052. doi: 10.1080/14783360500163243

|

Figures(1) / Tables(1)

Valentinas Navickas, Rima Kontautiene, Jurgita Stravinskiene, Yuriy Bilan. Paradigm shift in the concept of corporate social responsibility: COVID-19[J]. Green Finance, 2021, 3(2): 138-152. doi: 10.3934/GF.2021008

DownLoad:

DownLoad: