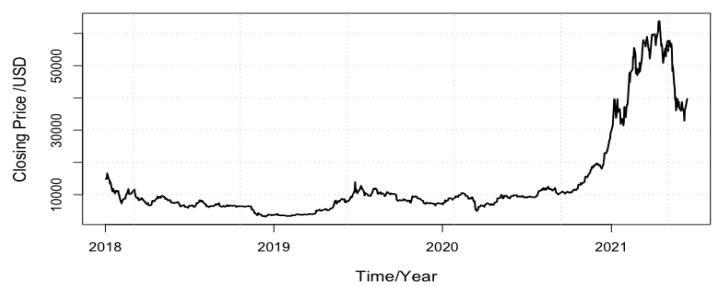

The Bitcoin futures market is growing and, as such, becoming more sophisticated. A small change in price may therefore have a large impact on the market. This paper investigates the propensity of 18 different competing GARCH family models and error distributions to model and forecast the volatility of Bitcoin futures returns. The study employs two different time periods (from January 2, 2018 to June 14, 2021; and March 11, 2020 to June 14, 2021). From the results, iGARCH(1, 1)-Students't-distribution (STD) is selected as the best performing model among the constructed models for the first period. By fitting the best three models from the first period to the second period, the iGARCH(1, 1)-STD is again selected as the optimal model. However, the iGARCH(1, 1)-normal inverse Gaussian (NIG) provides a significant variance forecast when used for in-sample and out-of-sample forecasts before the financial crisis and during the financial crisis, respectively. Our results indicate the impacts of past squared shocks on squared returns of Bitcoin futures and the ability of iGARCH(1, 1)-STD to capture such innovations and the propensity of iGARCH(1, 1)-NIG to optimally forecast the variance of Bitcoin futures returns.

Citation: Samuel Asante Gyamerah, Collins Abaitey. Modelling and forecasting the volatility of bitcoin futures: the role of distributional assumption in GARCH models[J]. Data Science in Finance and Economics, 2022, 2(3): 321-334. doi: 10.3934/DSFE.2022016

The Bitcoin futures market is growing and, as such, becoming more sophisticated. A small change in price may therefore have a large impact on the market. This paper investigates the propensity of 18 different competing GARCH family models and error distributions to model and forecast the volatility of Bitcoin futures returns. The study employs two different time periods (from January 2, 2018 to June 14, 2021; and March 11, 2020 to June 14, 2021). From the results, iGARCH(1, 1)-Students't-distribution (STD) is selected as the best performing model among the constructed models for the first period. By fitting the best three models from the first period to the second period, the iGARCH(1, 1)-STD is again selected as the optimal model. However, the iGARCH(1, 1)-normal inverse Gaussian (NIG) provides a significant variance forecast when used for in-sample and out-of-sample forecasts before the financial crisis and during the financial crisis, respectively. Our results indicate the impacts of past squared shocks on squared returns of Bitcoin futures and the ability of iGARCH(1, 1)-STD to capture such innovations and the propensity of iGARCH(1, 1)-NIG to optimally forecast the variance of Bitcoin futures returns.

| [1] | Cheng E, Cme to launch bitcoin futures in three weeks after green light from regulator; bitcoin jumps, 2017. Available from: https://www.cnbctv18.com/market/cme-to-launch-bitcoin-futures-in-3-weeks-after-green-light-from-regulator-bitcoin-jumps-16131.htm |

| [2] |

Baur DG, Dimpfl T (2019) Price discovery in bitcoin spot or futures? J Futures Mark 39: 803–817. https://doi.org/10.1002/fut.22004 doi: 10.1002/fut.22004

|

| [3] | Shiller RJ (2017) what is bitcoin really worth? don't even ask. N Y Times. |

| [4] |

Katsiampa P (2017) Volatility estimation for bitcoin: A comparison of garch models. Econ Lett 158: 3–6. https://doi.org/10.1016/j.econlet.2017.06.023 doi: 10.1016/j.econlet.2017.06.023

|

| [5] |

Naimy VY, Hayek MR (2018) Modelling and predicting the bitcoin volatility using garch models. Int J Math Model Numer Optim 8: 197–215. https://doi.org/10.1504/IJMMNO.2018.088994 doi: 10.1504/IJMMNO.2018.088994

|

| [6] |

Gyamerah SA (2019) Modelling the volatility of bitcoin returns using garch models. Quant Financ Econ 3: 739–753. https://doi.org/10.3934/QFE.2019.4.739 doi: 10.3934/QFE.2019.4.739

|

| [7] |

Guo ZY (2021a) Risk management of bitcoin futures with garch models. Financ Res Lett 45: 102197. https://doi.org/10.1016/j.frl.2021.102197 doi: 10.1016/j.frl.2021.102197

|

| [8] |

Guo ZY (2021b) Price volatilities of bitcoin futures. Financ Res Lett 43: 102022. https://doi.org/10.1016/j.frl.2021.102022 doi: 10.1016/j.frl.2021.102022

|

| [9] |

Venter PJ, Maré E (2021) Univariate and multivariate garch models applied to bitcoin futures option pricing, J Risk Financ Manage 14: 261. https://doi.org/10.3390/jrfm14060261 doi: 10.3390/jrfm14060261

|

| [10] |

Nelson DB (1991) Conditional heteroskedasticity in asset returns: A new approach. Econometrica: J Econ Soc 347–370. https://doi.org/10.2307/2938260 doi: 10.2307/2938260

|

| [11] |

Ding Z, Granger CW, Engle RF (1993) A long memory property of stock market returns and a new model. J empirical financ 1: 83–106. https://doi.org/10.1016/0927-5398(93)90006-D doi: 10.1016/0927-5398(93)90006-D

|

| [12] |

Glosten LR, Jagannathan R, Runkle DE (1993) On the relation between the expected value and the volatility of the nominal excess return on stocks. J Financ 48: 1779–1801. https://doi.org/10.1111/j.1540-6261.1993.tb05128.x doi: 10.1111/j.1540-6261.1993.tb05128.x

|

| [13] |

Bollerslev T (1987) A conditionally heteroskedastic time series model for speculative prices and rates of return. Review Econ Stat 69: 542–547. https://doi.org/10.2307/1925546 doi: 10.2307/1925546

|

| [14] |

Kuhe DA (2018) Modeling volatility persistence and asymmetry with exogenous breaks in the nigerian stock returns. CBN J Appl Stat 9: 167–196. Available from: https://dc.cbn.gov.ng/jas/vol9/iss1/7 doi: 10.11114/aef.v2i1.608

|

| [15] |

Thalassinos I, Ugurlu E, Muratoglu Y, et al. (2015) Comparison of forecasting volatility in the czech republic stock market, Appl Econ Financ 2: 11–18. https://doi.org/10.11114/aef.v2i1.608 doi: 10.11114/aef.v2i1.608

|

| [16] |

Wilhelmsson A (2006) Garch forecasting performance under different distribution assumptions. J Forecast 25: 561–578. https://doi.org/10.1002/for.1009 doi: 10.1002/for.1009

|

DSFE-02-03-016-s001.pdf DSFE-02-03-016-s001.pdf |

|

Figures(3) / Tables(9)

Samuel Asante Gyamerah, Collins Abaitey. Modelling and forecasting the volatility of bitcoin futures: the role of distributional assumption in GARCH models[J]. Data Science in Finance and Economics, 2022, 2(3): 321-334. doi: 10.3934/DSFE.2022016

DownLoad:

DownLoad: