Blockchain technology is disrupting the financial services industry and leading to extended big data applications in the banking sectors. Using blockchain and big data technology, banking industries can greatly improve decision-making, efficiency, and transparency. Nevertheless, there is a gap in research on the use of blockchain and big data technologies in banking systems from an academic viewpoint. To address the gap, we present a thorough overview of the impact of blockchain and big data technologies on banking systems. Although some banks have started blockchain development in small groups or isolation, this study was designed as a comprehensive exploration into a few facets of banking with blockchain technology to tackle the difficulties currently impeding the adoption of such technologies into banking systems throughout the world. This study shows that implementing big data and blockchain technology can significantly impact the security, speed and cost of transactions for banks. Further research could be conducted over a long-time span to capture the longitudinal impact of blockchain and big data technologies on banking in terms of the operating costs, profitability and scalability.

Citation: Mesbaul Haque Sazu, Sakila Akter Jahan. Impact of blockchain-enabled analytics as a tool to revolutionize the banking industry[J]. Data Science in Finance and Economics, 2022, 2(3): 275-293. doi: 10.3934/DSFE.2022014

Blockchain technology is disrupting the financial services industry and leading to extended big data applications in the banking sectors. Using blockchain and big data technology, banking industries can greatly improve decision-making, efficiency, and transparency. Nevertheless, there is a gap in research on the use of blockchain and big data technologies in banking systems from an academic viewpoint. To address the gap, we present a thorough overview of the impact of blockchain and big data technologies on banking systems. Although some banks have started blockchain development in small groups or isolation, this study was designed as a comprehensive exploration into a few facets of banking with blockchain technology to tackle the difficulties currently impeding the adoption of such technologies into banking systems throughout the world. This study shows that implementing big data and blockchain technology can significantly impact the security, speed and cost of transactions for banks. Further research could be conducted over a long-time span to capture the longitudinal impact of blockchain and big data technologies on banking in terms of the operating costs, profitability and scalability.

| [1] |

Al-Dmour H, Saad N (2021) The influence of the practices of big data analytics applications on bank performance: filed study. VINE J Inf Knowl Manage Syst. https://doi.org/10.1108/VJIKMS-08-2020-0151. doi: 10.1108/VJIKMS-08-2020-0151

|

| [2] | Allison I (2018) IBM and FX giant CLS team up to launch blockchain app store for banks. CoinDesk 15–24. Available from: https://www.coindesk.com/ibm-barclays-and-citi-team-up-to-launch-blockchain-app-store-for-banks |

| [3] | Amakobe M (2015) The Impact of Big Data Analytics on the Banking Industry. Colo Tech Univ. Available from: https://www.researchgate.net/profile/Moody-Amakobe/publication/280446380_The_Impact_of_Big_Data_Analytics_on_the_Banking_Industry/links/55b560c308aec0e5f436a9c6/The-Impact-of-Big-Data-Analytics-on-the-Banking-Industry.pdf |

| [4] |

Aversa J, Hernandez T, Doherty S (2021) Incorporating big data within retail organizations: A case study approach. J retailing consum serv 60. https://doi.org/10.1016/j.jretconser.2021.102447 doi: 10.1016/j.jretconser.2021.102447

|

| [5] |

Beck R (2018) Beyond bitcoin: The rise of blockchain world. Computer 51: 54–58. https://doi.org/10.1109/MC.2018.1451660. doi: 10.1109/MC.2018.1451660

|

| [6] | Bedeley RT, Iyer LS (2014) Big Data opportunities and challenges: the case of banking industry. Southern Association for Information Systems Conference. 1–6. |

| [7] | Biggs J (2018) Polish bank begins using a blockchain-based document management system. |

| [8] | BitPanda (2022) What are Smart Contracts and how do they work? May, 27. https://www.bitpanda.com/academy/en/lessons/what-are-smart-contracts-and-how-do-they-work/ |

| [9] | Bloomberg J (2018) Don't let blockchain cost savings hype fool you. Forbes. |

| [10] | Boumlik A, Bahaj M (2017) Big data and iot: A prime opportunity for banking industry. International Conference on Advanced Information Technology, Services and Systems. 396–407. |

| [11] |

Bresciani S, Ciampi F, Meli F, et.al. (2021) Using big data for co-innovation processes: Mapping the field of data-driven innovation, proposing theoretical developments and providing a research agenda. Int J Inf Manage 60: 102347. https://doi.org/10.1016/j.ijinfomgt.2021.102347 doi: 10.1016/j.ijinfomgt.2021.102347

|

| [12] | Buitenhek M (2016) Understanding and applying blockchain technology in banking: Evolution or revolution. J Digital Bank 1: 111–119. |

| [13] | Caplen B (2018) Blockchain: where it works, where it doesn't. |

| [14] | Carson B, Romanelli G, Walsh P, et al. (2018) Blockchain beyond the hype: What is the strategic business value. McKinsey Company. |

| [15] | Citi GPS (2018) Bank of The Future: The ABCs of Digital Disruption in Finance. Citi GPS: Global Perspectives Solutions. |

| [16] |

Cocco L, Pinna A, Marchesi M (2018) Banking on blockchain: Costs savings thanks to the blockchain technology. Future internet 9: 25. https://doi.org/10.3390/fi9030025 doi: 10.3390/fi9030025

|

| [17] | Collomb A, Sok K (2018) Blockchain/distributed ledger technology (DLT): What impact on the financial sector? Digiworld Econ J. |

| [18] | Daugherty P, Carrel-billiard M, Blitz M (2018) Redefine your company based on the company you keep. Intell Enterp Unleashed. |

| [19] |

Delgosha MS, Hajiheydari N, Fahimi SM (2020) Elucidation of big data analytics in banking: a four-stage Delphi study. J Enterp Inf Manage 34: 1577–1596. https://doi.org/10.1108/JEIM-03-2019-0097 doi: 10.1108/JEIM-03-2019-0097

|

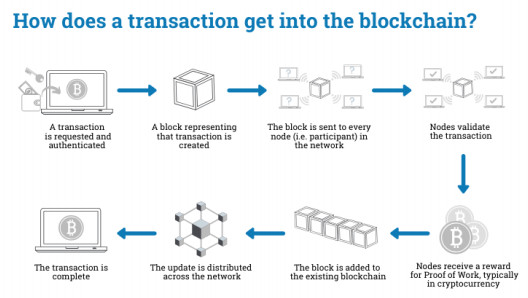

| [20] | Euromoney Learning (2022) How transactions get into the blockchain. https://www.euromoney.com/learning/blockchain-explained/how-transactions-get-into-the-blockchain |

| [21] | GeeksforGeeks (2022) BlockChain and KYC. https://www.geeksforgeeks.org/blockchain-and-kyc/ |

| [22] |

Ghasemaghaei M, Calic G (2020) Assessing the impact of big data on firm innovation performance: big data is not always better data. J Bus Res 108: 147–162. https://doi.org/10.1016/j.jbusres.2019.09.062 doi: 10.1016/j.jbusres.2019.09.062

|

| [23] |

Gupta T, Gupta N, Agrawal A, et al. (2019) Role of big data analytics in banking. International Conference on contemporary Computing and Informatics (IC3I), 222–227. https://doi.org/10.1109/IC3I46837.2019.9055616 doi: 10.1109/IC3I46837.2019.9055616

|

| [24] |

Hajiheydari N, Delgosha MS, Wang Y, et al. (2021) Exploring the paths to big data analytics implementation success in banking and financial service: an integrated approach. Ind Manage Data Syst 121: 2498–2529. https://doi.org/10.1108/IMDS-04-2021-0209 doi: 10.1108/IMDS-04-2021-0209

|

| [25] |

Hao S, Zhang H, Song M (2019) Big data, big data analytics capability, and sustainable innovation performance. Sustainability 11: 7145. https://doi.org/10.3390/su11247145 doi: 10.3390/su11247145

|

| [26] |

Harris WL, Wonglimpiyarat J (2019) Blockchain platform and future bank competition. Foresight 21: 625–639. https://doi.org/10.1108/FS-12-2018-0113 doi: 10.1108/FS-12-2018-0113

|

| [27] |

Hassani H, Huang X, Silva E (2018) Digitalisation and big data mining in banking. Big Data Cognit Comput 2: 18. https://doi.org/10.3390/bdcc2030018 doi: 10.3390/bdcc2030018

|

| [28] |

Indriasari E, Gaol FL, Matsuo T (2019) Digital banking transformation: Application of artificial intelligence and big data analytics for leveraging customer experience in the Indonesia banking sector. International Congress on Advanced Applied Informatics. https://doi.org/10.1109/IIAI-AAI.2019.00175 doi: 10.1109/IIAI-AAI.2019.00175

|

| [29] |

Keskar V, Yadav J, Kumar A (2021) Perspective of anomaly detection in big data for data quality improvement. Materi Today Proc 51: 532–537. https://doi.org/10.1016/j.matpr.2021.05.597 doi: 10.1016/j.matpr.2021.05.597

|

| [30] |

Lee Y, Son B, Park S, et al. (2021) A survey on security and privacy in blockchain-based central bank digital currencies. J Int Serv Inf Secur 11: 16–29. https://doi.org/10.22667/JISIS.2021.08.31.016 doi: 10.22667/JISIS.2021.08.31.016

|

| [31] |

Lekhwar S, Yadav S, Singh A (2019) Big data analytics in retail. Information and communication technology for intelligent systems, 469–477. https://doi.org/10.1007/978-981-13-1747-7_45 doi: 10.1007/978-981-13-1747-7_45

|

| [32] |

Munar A, Chiner E, Sales I (2014) A big data financial information management architecture for global banking. International Conference on Future Internet of Things and Cloud. 385–388. https://doi.org/10.1109/FiCloud.2014.68 doi: 10.1109/FiCloud.2014.68

|

| [33] | Mungai K, Bayat A (2018) The impact of big data on the South African banking industry. Intellectual Capital, Knowledge Management and Organisational Learning, ICICKM. Cape Town, 225–236. |

| [34] |

Nguyen QK (2016) Blockchain-a financial technology for future sustainable development. International conference on green technology and sustainable development. IEEE. 51–54. https://doi.org/10.1109/GTSD.2016.22 doi: 10.1109/GTSD.2016.22

|

| [35] |

Niebel T, Rasel F, Viete S (2019) BIG data–BIG gains? Understanding the link between big data analytics and innovation. Econ Innovation New Technol, 28: 296–316. https://doi.org/10.1080/10438599.2018.1493075 doi: 10.1080/10438599.2018.1493075

|

| [36] | Pradhan NR, Singh AP, Kumar V (2021) Blockchain-enabled traceable, transparent transportation system for blood bank. Advances in VLSI, Communication, and Signal Processing 313–324. |

| [37] | Radmehr E, M. Bazmara (2017) A Survey of Business Intelligence Solutions in Banking Industry and Big Data Applications. Int J Mechatron Electr Comput Technol 7. |

| [38] |

Santoro G, Fiano F, Bertoldi B, et al. (2018) Big data for business management in the retail industry. Management Decision 57: 1980–1992. https://doi.org/10.1108/MD-07-2018-0829 doi: 10.1108/MD-07-2018-0829

|

| [39] |

Shakya S, Smys S (2021) Big Data Analytics for Improved Risk Management and Customer Segregation in Banking Applications. J ISMAC 3: 235–249. https://doi.org/10.36548/jismac.2021.3.005 doi: 10.36548/jismac.2021.3.005

|

| [40] |

Silva ES, Hassani H, Madsen DØ (2020) Big Data in fashion: transforming the retail sector. J Bus Strategy 41: 21–27. https://doi.org/10.1108/JBS-04-2019-0062 doi: 10.1108/JBS-04-2019-0062

|

| [41] | Sproviero AF (2020) Integrated reporting and the epistemic authority of Big Data: an exploratory study from the banking industry. Financial reporting, http://digital.casalini.it/10.3280/FR2020-002004 |

| [42] |

Srivastava A, Singh SK, Tanwar S, et al. (2017) Suitability of big data analytics in Indian banking sector to increase revenue and profitability. International conference on advances in computing, communication & automation. 1–6. https://doi.org/10.1109/ICACCAF.2017.8344732 doi: 10.1109/ICACCAF.2017.8344732

|

| [43] |

Sun N, Morris JG, Xu J, et al. (2014) A framework for big data-based banking customer analytics. IBM J Res Development. https://doi.org/10.1147/JRD.2014.2337118 doi: 10.1147/JRD.2014.2337118

|

| [44] | Thiele F, Siegel D (2017) Blockchain @ Rethinking banking. https://www2.deloitte.com/content/dam/Deloitte/de/Documents/Innovation/Blockchain-Banking-Whitepaper-Deloitte-2017.pdf |

| [45] | Treat D, Brodersen C, Blain C, et al. (2017) Banking on Blockchain: A value analysis for investment banks. Accenture Consulting. |

| [46] |

Wang F, Wu D, Yu H, et al. (2021) Understanding the role of big data analytics for coordination of electronic retail service supply chain. Journal of Enterprise Information Management. https://doi.org/10.1108/JEIM-12-2020-0548 doi: 10.1108/JEIM-12-2020-0548

|

| [47] |

Wang R, Lin Z, Luo H (2019) Blockchain, bank credit and SME financing. Qual Quant 53: 1127–1140. https://doi.org/10.1007/s11135-018-0806-6 doi: 10.1007/s11135-018-0806-6

|

| [48] | Wise, Jason. (2022) How much data is created every day in, 2022? https://earthweb.com/ |

| [49] |

Wong KY, Wong RK (2020) Big data quality prediction on banking applications. International Conference on Data Science and Advanced Analytics (DSAA). 791–792. https://doi.org/10.1109/DSAA49011.2020.00119 doi: 10.1109/DSAA49011.2020.00119

|

| [50] |

Wright LT, Robin R, Stone M, et al. (2019) Adoption of big data technology for innovation in B2B marketing. J Bus Bus Mark 26: 281–293. https://doi.org/10.1080/1051712X.2019.1611082 doi: 10.1080/1051712X.2019.1611082

|

| [51] |

Wu, T, Liang X (2017) Exploration and practice of inter-bank application based on blockchain. international conference on computer science and education. IEEE, 219–224. https://doi.org/10.1109/ICCSE.2017.8085492 doi: 10.1109/ICCSE.2017.8085492

|

| [52] |

Ying S, Sindakis S, Aggarwal S, et al. (2021) Managing big data in the retail industry of Singapore: Examining the impact on customer satisfaction and organizational performance. Eur Manage J 39: 390–400. https://doi.org/10.1016/j.emj.2020.04.001 doi: 10.1016/j.emj.2020.04.001

|

| [53] |

Yu TR, Song X (2021) Big Data and Artificial Intelligence in the Banking Industry. Financial econometrics, Mathematics, Statistics, and Machine Learning 4025–4041. https://doi.org/10.1142/9789811202391_0117 doi: 10.1142/9789811202391_0117

|

| [54] |

Zhang J, Tian R, Cao Y, et al. (2021) A hybrid model for central bank digital currency based on blockchain. IEEE Access 9: 53589–53601. https://doi.org/10.1109/ACCESS.2021.3071033 doi: 10.1109/ACCESS.2021.3071033

|

Figures(5)

Mesbaul Haque Sazu, Sakila Akter Jahan. Impact of blockchain-enabled analytics as a tool to revolutionize the banking industry[J]. Data Science in Finance and Economics, 2022, 2(3): 275-293. doi: 10.3934/DSFE.2022014

DownLoad:

DownLoad: