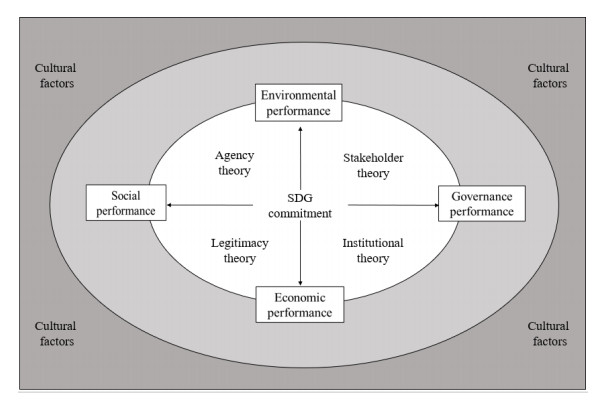

The collaboration of private companies in the fulfillment of the Sustainable Development Goals (SDGs) is key to address global challenges of climate change, social inequality and environmental degradation. This collaboration can also boost their own organizational performance. However, the research on the relationship between SDG commitment and organizational performance remains inconclusive. The diversity of findings could stem from cross-cultural differences in corporate environments. The aim of this study, therefore, was to analyze the interaction between SDG commitment and organizational performance and to examine how this interaction is influenced by cultural factors. Using simultaneous equation modeling on a sample of 3,420 companies from 30 countries for the period 2015 to 2020, our results show that engagement with SDGs has an impact on organizational performance levels which is further enhanced by the catalytic effect of certain cultural factors.

Citation: Ana Bellostas, Cristina Del Río, Karen González-Álvarez, Francisco J López-Arceiz. Cultural context, organizational performance and Sustainable Development Goals: A pending task[J]. Green Finance, 2023, 5(2): 211-239. doi: 10.3934/GF.2023009

The collaboration of private companies in the fulfillment of the Sustainable Development Goals (SDGs) is key to address global challenges of climate change, social inequality and environmental degradation. This collaboration can also boost their own organizational performance. However, the research on the relationship between SDG commitment and organizational performance remains inconclusive. The diversity of findings could stem from cross-cultural differences in corporate environments. The aim of this study, therefore, was to analyze the interaction between SDG commitment and organizational performance and to examine how this interaction is influenced by cultural factors. Using simultaneous equation modeling on a sample of 3,420 companies from 30 countries for the period 2015 to 2020, our results show that engagement with SDGs has an impact on organizational performance levels which is further enhanced by the catalytic effect of certain cultural factors.

| [1] | Ahmad N, Buniamin S (2021) The relationship between SDG engagement and corporate financial performance: Evidence from public listed companies in Malaysia. Global Bus Manage Res 13: 730–741. |

| [2] |

Anzola-Román P, Garcia-Marco T, Zouaghi F (2023) The Influence of CSR Orientation on Innovative Performance: Is the Effect Conditioned to the Implementation of Organizational Practices?. J Bus Ethics, 1–18. https://doi.org/10.1007/s10551-023-05406-z doi: 10.1007/s10551-023-05406-z

|

| [3] |

Atan R, Alam MM, Said J, et al. (2018) The impacts of environmental, social, and governance factors on firm performance: Panel study of Malaysian companies. Manage Environ Quality 29: 182–194. https://doi.org/10.1108/MEQ-03-2017-0033 doi: 10.1108/MEQ-03-2017-0033

|

| [4] |

Berrone P, Fosfuri A, Gelabert L, et al. (2013) Necessity as the mother of 'green' inventions: Institutional pressures and environmental innovations. Strat Manage J 34: 891–909. https://doi.org/10.1002/smj.2041 doi: 10.1002/smj.2041

|

| [5] | Bertelsmann S (2018) Culture and Conflict in Global Perspective, The Cultural Dimensions of Global Conflicts 1945–2007, Bertelsmann Stiftung (ed.), Verlag Bertelsmann Stiftung. |

| [6] |

Biermann F, Kanie N, Kim RE (2017) Global governance by goal-setting: The novel approach of the UN Sustainable Development Goals. Curr Opin Env Sust 26: 26–31. https://doi.org/10.1016/j.cosust.2017.01.010 doi: 10.1016/j.cosust.2017.01.010

|

| [7] |

Blodgett JG, Lu LC, Rose GM, et al. (2001) Ethical sensitivity to stakeholder interests: A cross-cultural comparison. J Acad Mark Sci 29: 190–202. https://doi.org/10.1177/03079459994551 doi: 10.1177/03079459994551

|

| [8] |

Bradley SW, Wiklund J, Shepherd DA (2010) Swinging a double-edged sword: The effect of slack on entrepreneurial management and growth. J Bus Venturing 26: 537–554. https://doi.org/10.1016/j.jbusvent.2010.03.002 doi: 10.1016/j.jbusvent.2010.03.002

|

| [9] |

Buallay A (2019) Between cost and value: Investigating the effects of sustainability reporting on a firm's performance. J Appl Account Res 20: 481–496.https://doi.org/10.1108/JAAR-12-2017-0137 doi: 10.1108/JAAR-12-2017-0137

|

| [10] |

Buhr N, Freedman M (2001) Culture, institutional factors and differences in environmental disclosure between Canada and the United States. Crit Perspect Accoun 12: 293–322. https://doi.org/10.1006/cpac.2000.0435 doi: 10.1006/cpac.2000.0435

|

| [11] |

Calabrese A, Costa R, Gastaldi M, et al. (2021) Implications for Sustainable Development Goals: A framework to assess company disclosure in sustainability reporting. J Clean Prod 319: 128624. https://doi.org/10.1016/j.jclepro.2021.128624 doi: 10.1016/j.jclepro.2021.128624

|

| [12] |

Campagnolo L, Eboli F, Farnia L, et al. (2018) Supporting the UN SDGs transition: Methodology for sustainability assessment and current worldwide ranking. Economics 12: 1–31. https://doi.org/10.5018/economics-ejournal.ja.2018-10 doi: 10.5018/economics-ejournal.ja.2018-10

|

| [13] |

Chen S, Bouvain P (2009) Is corporate responsibility converging? A comparison of corporate responsibility reporting in the USA, UK, Australia, and Germany. J Bus Ethics 87: 299–317. https://doi.org/10.1007/s10551-008-9794-0 doi: 10.1007/s10551-008-9794-0

|

| [14] |

Chu Z, Xu J, Lia F, et al. (2018) Institutional theory and environmental pressures: The moderating effect of market uncertainty on innovation and firm performance. IEEE T Eng Manage 65: 392–403. https://doi.org/10.1109/TEM.2018.2794453 doi: 10.1109/TEM.2018.2794453

|

| [15] |

Delmas MA, Toffel MW (2008) Organizational responses to environmental demands: Opening the black box. Strat Manage J 29: 1027–1055. https://doi.org/10.1002/smj.701 doi: 10.1002/smj.701

|

| [16] |

Diaz-Sarachaga JM (2021) Monetizing impacts of Spanish companies toward the Sustainable Development Goals. Corp Soc Resp Env Ma 28: 1313–1323. http://doi.org/10.1002/csr.2149 doi: 10.1002/csr.2149

|

| [17] |

DiMaggio PJ, Powell WW (1983) The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am Sociol Rev 48: 147–160. https://doi.org/10.2307/2095101 doi: 10.2307/2095101

|

| [18] | Doupnik TS, Salter SB (1995) External environment, culture, and accounting practice: A preliminary test of a general model of international accounting development. Int J Account 30: 189–207. |

| [19] |

Durugbo C, Amankwah‐Amoah J (2019) Global sustainability under uncertainty: How do multinationals craft regulatory policies? Corp Soc Resp Env Ma 26: 1500–1516. https://doi.org/10.1002/csr.1764 doi: 10.1002/csr.1764

|

| [20] | EIKON-Refinitiv (2019). Environmental, Social and Governance (ESG) Scores. Thomson Reuters. |

| [21] |

Elalfy A, Weber O, Geobey S (2021) The Sustainable Development Goals (SDGs): A rising tide lifts all boats? Global reporting implications in a post SDGs world. J Appl Account Res 22: 557–575. http://doi.org/10.1108/JAAR-06-2020-0116 doi: 10.1108/JAAR-06-2020-0116

|

| [22] |

Erin O, Bamigboye O, Arumona J (2020) Risk governance and financial performance: An empirical analysis. Bus Theory Practice 21: 758–768. https://doi.org/10.3846/btp.2020.10850 doi: 10.3846/btp.2020.10850

|

| [23] |

Erin OA, Bamigboye OA, Oyewo B (2022) Sustainable development goals (SDG) reporting: an analysis of disclosure. J Account Emerg Econ 12: 761–789. https://doi.org/10.1108/JAEE-02-2020-0037 doi: 10.1108/JAEE-02-2020-0037

|

| [24] | Eurostat (2023) https://ec.europa.eu/eurostat/statistics explained/index.php?title = Archive: Quality_of_life_in_Europe_-_facts_and_views_-_leisure_and_social_relations |

| [25] | Faisal F, Tower G, Rusmin R (2015) Legitimising corporate sustainability reporting throughout the world. Aust Account Bus Financ J 6: 19–34. |

| [26] |

Feng Y, Akram R, Hieu VM, et al. (2021) The impact of corporate social responsibility on the sustainable financial performance of Italian firms: Mediating role of firm reputation. Econ Research-Ekonomska Istraživanja, 1–19. https://doi.org/10.1080/1331677X.2021.2017318 doi: 10.1080/1331677X.2021.2017318

|

| [27] |

Florini A, Pauli M (2018) Collaborative governance for the Sustainable Development Goals. Asia Pacific Policy Stud 5: 583–598. https://doi.org/10.1002/app5.252 doi: 10.1002/app5.252

|

| [28] | Freeman RE (1984) Strategic management: A stakeholder approach, Boston: Pitman Publishing. |

| [29] | Frey M, Sabbatino A (2018) The role of the private sector in global sustainable development: The UN 2030 agenda, In: Grigore, G., Stancu, A., and McQueen, D. (eds), Corporate responsibility and digital communities: An international perspective towards sustainability, Cham: Palgrave Macmillan. https://doi.org/10.1007/978-3-319-63480-7_10 |

| [30] |

García-Meca E, Martínez-Ferrero J (2021) Is SDG reporting substantial or symbolic? An examination of controversial and environmentally sensitive industries. J Clean Prod 298: 126781. https://doi.org/10.1016/j.jclepro.2021.126781 doi: 10.1016/j.jclepro.2021.126781

|

| [31] |

Gaziulusoy AI, Brezet H (2015) Design for system innovations and transitions: A conceptual framework integrating insights from sustainability science and theories of system innovations and transitions. J Clean Prod 108: 558–568. https://doi.org/10.1016/j.jclepro.2015.06.066 doi: 10.1016/j.jclepro.2015.06.066

|

| [32] | Global UN. (2012). https://www.un.org/millenniumgoals/pdf/Think%20Pieces/2_culture.pdf |

| [33] |

Gneiting U, Mhlanga R (2021) The partner myth: Analysing the limitations of private sector contributions to the Sustainable Development Goals. Dev Pract 31: 920–926. https://doi.org/10.1080/09614524.2021.1938512 doi: 10.1080/09614524.2021.1938512

|

| [34] |

Hák T, Janoušková S, Moldan B (2016) Sustainable Development Goals: A need for relevant indicators. Col Indic 60: 565–573. https://doi.org/10.1016/j.ecolind.2015.08.003 doi: 10.1016/j.ecolind.2015.08.003

|

| [35] |

Hannan MP, Freeman JH (1977) The population ecology of organizations. Am J Soc 82: 929–964. https://doi.org/10.1086/226424 doi: 10.1086/226424

|

| [36] | Hawley A (1968) Human ecology, In: Sills, D.L. (ed.), International encyclopedia of the social sciences, New York: Macmillan. |

| [37] | Hofstede G (2001) Culture's consequences: Comparing values, behaviors, institutions and organizations across nations, 2 Eds., United States: Sage. |

| [38] |

Hofstede G (2011) Dimensionalizing cultures: The Hofstede model in context. Online Readings in Psychology and Culture 2. https://doi.org/10.9707/2307-0919.1014 doi: 10.9707/2307-0919.1014

|

| [39] | Hofstede G (2022) Hofstede insights. Available from: https://www.hofstede-insights.com/ [Accessed November 24th, 2022]. |

| [40] |

Jacob A (2017) Mind the gap: Analyzing the impact of data gap in Millennium Development Goals'(MDGs) indicators on the progress toward MDGs. World Dev 93: 260–278. http://dx.doi.org/10.1016/j.worlddev.2016.12.016 doi: 10.1016/j.worlddev.2016.12.016

|

| [41] |

Jensen JC, Berg N (2012) Determinants of traditional sustainability reporting versus integrated reporting. An Institutionalist Approach. Bus Strat Environ 21: 299–316. https://doi.org/10.1002/bse.740 doi: 10.1002/bse.740

|

| [42] |

Khaled R, Ali H, Mohamed EK (2021) The Sustainable Development Goals and corporate sustainability performance: Mapping, extent and determinants. J Clean Prod 311: 127599. http://dx.doi.org/10.1016/j.jclepro.2021.127599 doi: 10.1016/j.jclepro.2021.127599

|

| [43] |

Kücükgül E, Cerin P, Liu Y (2022) Enhancing the value of corporate sustainability: An approach for aligning multiple SDGs guides on reporting. J Clean Prod 333: 130005. https://doi.org/10.1016/j.jclepro.2021.130005 doi: 10.1016/j.jclepro.2021.130005

|

| [44] |

Lassala C, Orero-Blat M, Ribeiro-Navarrete S (2021) The financial performance of listed companies in pursuit of the Sustainable Development Goals (SDG). Econ Research-Ekonomska Istraživanja 34: 427–449. http://doi.org/10.1080/1331677X.2021.1877167 doi: 10.1080/1331677X.2021.1877167

|

| [45] | Lee KH, Herold DM (2018) Cultural relevance in Environmental and Sustainability Management Accounting (EMA) in the Asia-Pacific region: A Link between cultural values and accounting values towards EMA values, In: Lee, K.H., and Schaltegger, S. (eds), Accounting for sustainability: Asia Pacific perspectives, Cham: Springer, 11–37. https://doi.org/10.1007/978-3-319-70899-7_2 |

| [46] |

Li B, Wu K (2017) Environmental management system adoption and the operational performance of firm in the textile and apparel industry of China. Sustainability 9: 1–11. http://doi.org/10.3390/su9060992 doi: 10.3390/su9060992

|

| [47] |

Lior N, Radovanović M, Filipović S (2018) Comparing sustainable development measurement based on different priorities: Sustainable Development Goals, economics, and human well-being—Southeast Europe case. Sustainability Sci 13: 973–1000. http://dx.doi.org/10.1007/s11625-018-0557-2 doi: 10.1007/s11625-018-0557-2

|

| [48] |

López-Arceiz FJ, Bellostas AJ, Rivera MP (2017) Accessibility and transparency: Impact on social economy. Online Infor Rev 41: 35–52. https://doi.org/10.1108/OIR-09-2015-0296 doi: 10.1108/OIR-09-2015-0296

|

| [49] |

López-Arceiz FJ, Bellostas AJ, Rivera MP (2018) Twenty years of research on the relationship between economic and social performance: A meta-analysis approach. Soc Ind Res 140: 453–484. https://doi.org/10.1007/s11205-017-1791-1 doi: 10.1007/s11205-017-1791-1

|

| [50] |

López‐Arceiz FJ, Del Río C, Bellostas AJ (2020) Sustainability performance indicators: Definition, interaction, and influence of contextual characteristics. Corp Soc Resp Env Ma 27: 2615–2630. http://dx.doi.org/10.1002/csr.1986 doi: 10.1002/csr.1986

|

| [51] |

Ma JH, Choi SB, Ahn YH (2017) The impact of eco-friendly management on product quality, financial performance and environmental performance. J Distrib Sci 15: 17–28. https://doi.org/10.15722/jds.15.5.201705.17 doi: 10.15722/jds.15.5.201705.17

|

| [52] |

McArthur JW, Rasmussen K (2019) Classifying Sustainable Development Goal trajectories: A country-level methodology for identifying which issues and people are getting left behind. World Dev 123: 104608. https://doi.org/10.1016/j.worlddev.2019.06.031 doi: 10.1016/j.worlddev.2019.06.031

|

| [53] | Meyer JW (1979) The impact of the centralization of educational funding and control on state and local organizational governance. Stanford, CA: Institute for Research on Educational Finance and Governance, Stanford University, Program Report No. 79-B20. |

| [54] | Meyer JW, Rowan B (1991) Institutionalized organizations: Formal structure as myth and ceremony, In: Dimaggio, P and Powell, W. (Eds), The new institutionalism in organizational analysis, Chicago: The University of Chicago Press. |

| [55] |

Morioka SN, Bolis I, Carvalho MD (2018) From an ideal dream towards reality analysis: Proposing Sustainable Value Exchange Matrix (SVEM) from systematic literature review on sustainable business models and face validation. J Clean Prod 178: 76–88. http://doi.org/10.1016/j.jclepro.2017.12.078 doi: 10.1016/j.jclepro.2017.12.078

|

| [56] |

Muhmad SN, Muhamad R (2021) Sustainable business practices and financial performance during pre-and post-SDG adoption periods: A systematic review. J Sust Financ Invest 11: 291–309. https://doi.org/10.1080/20430795.2020.1727724 doi: 10.1080/20430795.2020.1727724

|

| [57] |

Muñoz-Torres MJ, Fernandez-Izquierdo MA, Rivera-Lirio JM, et al. (2019) Can environmental, social, and governance rating agencies favor business models that promote a more sustainable development? Corp Soc Resp Env Ma 26: 439–452. https://doi.org/10.1002/csr.1695 doi: 10.1002/csr.1695

|

| [58] |

Naciti V (2019) Corporate governance and board of directors: The effect of a board composition on firm sustainability performance. J Clean Prod 237: 117727. https://doi.org/10.1016/j.jclepro.2019.117727 doi: 10.1016/j.jclepro.2019.117727

|

| [59] |

Naomi P, Akbar I (2021) Beyond sustainability: empirical evidence from oecd countries on the connection among natural resources, ESG performances, and economic development. Econ Soc 14: 89–106. https://doi.org/10.14254/2071-789X.2021/14-4/5 doi: 10.14254/2071-789X.2021/14-4/5

|

| [60] |

Nicolò G, Zanellato G, Tiron-Tudor A, et al. (2022) Revealing the corporate contribution to Sustainable Development Goals through integrated reporting: A worldwide perspective. Soc Resp J. https://doi.org/10.1108/SRJ-09-2021-0373 doi: 10.1108/SRJ-09-2021-0373

|

| [61] |

Nurunnabi M (2015) The impact of cultural factors on the implementation of global accounting standards (IFRS) in a developing country. Adv Account 31: 136–149. http://dx.doi.org/10.1016/j.adiac.2015.03.015 doi: 10.1016/j.adiac.2015.03.015

|

| [62] |

Ordonez‐Ponce E (2023) The role of local cultural factors in the achievement of the sustainable development goals. Sust Dev 31: 1122–1134. https://doi.org/10.1002/sd.2445 doi: 10.1002/sd.2445

|

| [63] | Organisation for Economic Cooperation and Development (2017). Measuring distance to the SDG targets: An assessment of where OECD countries stand OECD. Paris: OECD. |

| [64] |

Ortas E, Moneva JM (2011) Sustainability stock exchange indexes and investor expectations: Multivariate evidence from DJSI-Stoxx. Spanish J Financ Account 40: 395–416. https://doi.org/10.1080/02102412.2011.10779706 doi: 10.1080/02102412.2011.10779706

|

| [65] |

Pizzi S, Del Baldo M, Caputo F, et al. (2022) Voluntary disclosure of Sustainable Development Goals in mandatory non‐financial reports: The moderating role of cultural dimension. J Int Financ Manage Account 33: 83–106. https://doi.org/10.1111/jifm.12139 doi: 10.1111/jifm.12139

|

| [66] |

Pizzi S, Caputo A, Corvino A, et al. (2020) Management research and the UN Sustainable Development Goals (SDGs): A bibliometric investigation and systematic review. J Clean Prod 276: 124033. https://doi.org/10.1016/j.jclepro.2020.124033 doi: 10.1016/j.jclepro.2020.124033

|

| [67] |

Pizzi S, Rosati F, Venturelli A (2021) The determinants of business contribution to the 2030 Agenda: Introducing the SDG reporting score. Bus Strat Environ 30: 404–421. http://doi.org/10.1002/bse.2628 doi: 10.1002/bse.2628

|

| [68] | Powell WW, DiMaggio PJ (1984) The new institutionalism in organizational analysis, Chicago: The University of Chicago Press. |

| [69] | Prexl A, Signitzer B (2008) When a new CEO is ahead: Leadership change processes in the light of change communication, personal public relations, and reputation management. Austria: Veröffentlicht. |

| [70] |

Ramos DL, Chen S, Rabeeu A, et al. (2022) Does SDG coverage influence firm performance? Sustainability 14: 4870. https://doi.org/10.3390/su14094870 doi: 10.3390/su14094870

|

| [71] |

Richard PJ, Devinney TM, Yip GS, et al. (2009) Measuring organizational performance: Towards methodological best practice. J Manage 35: 718–804. https://doi.org/10.1177/0149206308330560 doi: 10.1177/0149206308330560

|

| [72] | RobecoSAM (2022) The sustainability yearbook 2021. Switzerland: S & P Global. |

| [73] |

Rosati F, Faria L (2019a) Addressing the SDGs in sustainability reports: The relationship with institutional factors. J Clean Prod 215: 1312–1326. https://doi.org/10.1016/j.jclepro.2018.12.107 doi: 10.1016/j.jclepro.2018.12.107

|

| [74] |

Rosati F, Faria L (2019b) Business contribution to the Sustainable Development Agenda: organizational factors related to early adoption of SDG reporting. Corp Soc Resp Envir Ma 26: 588–597. https://doi.org/10.1002/csr.1705 doi: 10.1002/csr.1705

|

| [75] | Salem RB, Ayadi SD (2022) The impact of acculturation process and the institutional isomorphism on IFRS adoption. Euro Med J Bus, 1–23. |

| [76] |

Santos MJ, Bastos CS (2020) The adoption of Sustainable Development Goals by large Portuguese companies. Soc Resp J 17: 1079–1099. https://doi.org/10.1108/SRJ-07-2018-0184 doi: 10.1108/SRJ-07-2018-0184

|

| [77] |

Scheyvens R, Banks G, Hughes E (2016) The private sector and the SDGs: The need to move beyond 'business as usual'. Sust Dev 24: 371–382. https://doi.org/10.1002/sd.1623 doi: 10.1002/sd.1623

|

| [78] |

Schramade W (2017) Investing in the UN Sustainable Development Goals: Opportunities for companies and investors. J Appl Corp Financ 29: 87–99. https://doi.org/10.1111/jacf.12236 doi: 10.1111/jacf.12236

|

| [79] | Scott WR (2013) Institutions and organizations: Ideas, interests, and identities, USA: Sage. |

| [80] |

Sierra Garcia L, Bollas-Araya HM, Garcia Benau MA (2022) Sustainable development goals and assurance of non-financial information reporting in Spain. Sust Account Manage Policy J 13: 878–898. https://doi.org/10.1108/SAMPJ-04-2021-0131 doi: 10.1108/SAMPJ-04-2021-0131

|

| [81] |

Signorini P, Wiesemes R, Murphy R (2009) Developing alternative frameworks for exploring intercultural learning: a critique of Hofstede's cultural difference model. Teach Higher Edu 14: 253–264. https://doi.org/10.1080/13562510902898825 doi: 10.1080/13562510902898825

|

| [82] |

Stevens C, Kanie N (2016) The transformative potential of the Sustainable Development Goals (SDGs). Int Environ Agree 16: 393–396. https://doi.org/10.1007/s10784-016-9324-y doi: 10.1007/s10784-016-9324-y

|

| [83] |

Suchman MC (1995) Managing legitimacy: Strategic and institutional approaches. Acad Manage Rev 20: 571–610. https://doi.org/10.5465/amr.1995.9508080331 doi: 10.5465/amr.1995.9508080331

|

| [84] | United Nations (2015) Transforming our world: The 2030 Agenda for sustainable development. USA: United Nations. |

| [85] | United Nations (2021) SDG Compass. Available from: https://sdgcompass.org/. |

| [86] | United Nations Global Compact (2015) A global compact for sustainable development business and the SDGs: Acting responsibly and finding opportunities. Available from: https://www.unglobalcompact.org/library/2291. |

| [87] | United Nations Global Compact (2020) SDG Ambition. Activating ambitous action to achieve the SDGs. USA: United Nations. |

| [88] |

Van den Heiligenberg HA, Heimeriks GJ, Hekkert MP, et al. (2022) Pathways and harbours for the translocal diffusion of sustainability innovations in Europe. Environ Innov Soc Tr 42: 374–394. https://doi.org/10.1016/j.eist.2022.01.011 doi: 10.1016/j.eist.2022.01.011

|

| [89] | Van Tulder R (2018) Business and the sustainable development goals: A framework for effective corporate involvement, Rotterdam: Erasmus University Rotterdam. |

| [90] | Van Zanten JA, Huij J (2022) Corporate sustainability performance: Introducing an SDG score and testing its validity relative to ESG ratings. Available at SSRN 4186680. |

| [91] |

Van Zanten JA, Van Tulder R (2018) Multinational enterprises and the Sustainable Development Goals: An institutional approach to corporate engagement. J Int Bus Policy 1: 208–233. http://doi.org/10.1057/s42214-018-0008-x doi: 10.1057/s42214-018-0008-x

|

| [92] |

Vazquez-Brust D, Piao RS, de Melo MF, et al. (2020). The governance of collaboration for sustainable development: Exploring the "black box". Clean Prod 256: 120260. https://doi.org/10.1016/j.jclepro.2020.120260 doi: 10.1016/j.jclepro.2020.120260

|

| [93] |

Vildåsen SS (2018) Corporate sustainability in practice: An exploratory study of the sustainable development goals (SDGs). Bus Strat Dev 1: 256–264. https://doi.org/10.1002/bsd2.35 doi: 10.1002/bsd2.35

|

| [94] |

Vormedal IH, Ruud A (2009). Sustainability reporting in Norway - an assessment of performance in the context of legal demands and socio-political drivers. Bus Strat Environ 18: 207–222. https://doi.org/10.1002/bse.560 doi: 10.1002/bse.560

|

| [95] |

Wang Z, Reimsbach D, Braam G (2018) Political embeddedness and the diffusion of corporate social responsibility practices in China: A trade-off between financial and CSR performance? J Clean Prod 198: 1185–1197. https://doi.org/10.1016/j.jclepro.2018.07.116 doi: 10.1016/j.jclepro.2018.07.116

|

| [96] | World Business Council for Sustainable Development (2021) SDG Essentials for Business. World Business Council for Sustainable Development, Geneva. |

| [97] |

Zabala-Aguayo F, Ślusarczyk B (2020) Risks of banking services' digitalization: The practice of diversification and Sustainable Development Goals. Sustainability 12: 4040. http://doi.org/10.3390/su12104040 doi: 10.3390/su12104040

|

| [98] |

Zampone G, García‐Sánchez IM, Sannino G (2023) Imitation is the sincerest form of institutionalization: Understanding the effects of imitation and competitive pressures on the reporting of sustainable development goals in an international context. Bus Strat Environ. https://doi.org/10.1002/bse.3357 doi: 10.1002/bse.3357

|

| [99] |

Zhang KQ, Chen HH (2017) Environmental performance and financing decisions impact on sustainable financial development of Chinese environmental protection enterprises. Sustainability 9: 1–14. http://doi.org/10.3390/su9122260 doi: 10.3390/su9122260

|

GF-05-02-009-s001.pdf GF-05-02-009-s001.pdf |

|

Figures(3) / Tables(6)

Ana Bellostas, Cristina Del Río, Karen González-Álvarez, Francisco J López-Arceiz. Cultural context, organizational performance and Sustainable Development Goals: A pending task[J]. Green Finance, 2023, 5(2): 211-239. doi: 10.3934/GF.2023009

DownLoad:

DownLoad: