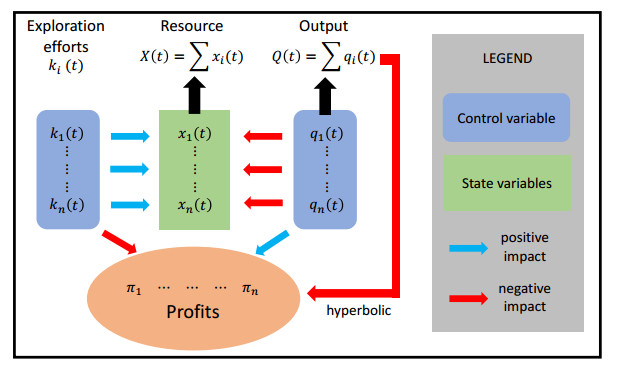

We consider a resource extraction model with the possibility of extending the resource stock by drilling efforts and an oligopolistic competition of symmetric firms. Assuming a hyperbolic market demand, we adopt the open-loop Nash equilibrium to analyze and compare the outcomes of a private vs a common resource pool. For both cases, the drilling efforts of the individual firms strongly depend on the market structure. For a low competition, the efforts increase the number of firms, and the opposite is true for a high competition. On the other hand, aggregate drilling efforts are different among the two types of pools and are opposite to Schumpeterian's hypothesis (i.e., they are either an inverted U-shaped (private pools) or strictly increasing (single pools)).

Citation: Gustav Feichtinger, Luca Lambertini, George Leitmann, Stefan Wrzaczek. Optimal drilling efforts and industry structure[J]. AIMS Environmental Science, 2024, 11(4): 610-627. doi: 10.3934/environsci.2024030

We consider a resource extraction model with the possibility of extending the resource stock by drilling efforts and an oligopolistic competition of symmetric firms. Assuming a hyperbolic market demand, we adopt the open-loop Nash equilibrium to analyze and compare the outcomes of a private vs a common resource pool. For both cases, the drilling efforts of the individual firms strongly depend on the market structure. For a low competition, the efforts increase the number of firms, and the opposite is true for a high competition. On the other hand, aggregate drilling efforts are different among the two types of pools and are opposite to Schumpeterian's hypothesis (i.e., they are either an inverted U-shaped (private pools) or strictly increasing (single pools)).

| [1] |

Aghion P, Akcigit U, Howitt P (2015) The Schumpeterian growth paradigm. Annu Rev Econ 7: 557–575. https://doi.org/10.1146/annurev-economics-080614-115412 doi: 10.1146/annurev-economics-080614-115412

|

| [2] |

Aghion P, Bloom N, Blundell R, et al. (2005) Competition and innovation: An inverted-U relationship. Q J Econ 120: 701–728. https://doi.org/10.1162/0033553053970214 doi: 10.1162/0033553053970214

|

| [3] | Arrow K (1962) Economic welfare and the allocation of resources for invention. in R. Nelson (ed.), The Rate and Direction of Inventive Activity, Princeton, Princeton University Press. https://doi.org/10.1515/9781400879762-024 |

| [4] |

Arrow KJ, Chang S (1982) Optimal pricing, use, and exploration of uncertain resource stocks. J Environ Econ Manag 9: 1–10. https://doi.org/10.1016/0095-0696(82)90002-X doi: 10.1016/0095-0696(82)90002-X

|

| [5] |

Boyce J, Vojtassak L (2008) An 'Oil'igopoly theory of exploration. Resour Energy Econo 30: 428–454. https://doi.org/10.1016/j.reseneeco.2007.10.001 doi: 10.1016/j.reseneeco.2007.10.001

|

| [6] |

Cairns RD, Quyen NV (1998) Optimal exploration for and exploitation of heterogeneous mineral deposits. J Environ Econ Manag 35: 164–189. https://doi.org/10.1006/jeem.1998.1027 doi: 10.1006/jeem.1998.1027

|

| [7] |

Cellini R, Lambertini L (2002) A differential game approach to investment in product differentiation. J Econ Dyn Control 27: 51–62. https://doi.org/10.1016/S0165-1889(01)00026-4 doi: 10.1016/S0165-1889(01)00026-4

|

| [8] |

Dasgupta P, Gilbert R, Stiglitz J (1983) Strategic considerations in invention and innovation: The case of natural resources. Econometrica 51: 1439–1448. https://doi.org/10.2307/1912283 doi: 10.2307/1912283

|

| [9] |

Davison R (1978) Optimal depletion of an exhaustible resource with research and development towards an alternative technology. Rev Econ Stud 45: 335–367. https://doi.org/10.2307/2297350 doi: 10.2307/2297350

|

| [10] |

Delbono F, Lambertini L (2022) Innovation and product market concentration: Schumpeter, Arrow and the inverted-U Shape curve. Oxford Econ Pap 74: 297–311. https://doi.org/10.1093/oep/gpaa044 doi: 10.1093/oep/gpaa044

|

| [11] |

Deshmuk SD, Pliska SR (1980) Optimal consumption and exploration of nonrenewable resources under uncertainty. Econometrica 48: 177–200. https://doi.org/10.2307/1912024 doi: 10.2307/1912024

|

| [12] |

Dixit AK (1986) Comparative statics for oligopoly. Int Econ Rev 27: 103–122. https://doi.org/10.2307/2526609 doi: 10.2307/2526609

|

| [13] |

Feichtinger G, Hartl RF, Kort PM, et al. (2022) Asymmetric information in a capital accumulation differential game with spillover and learning effects. J Optimiz Theory Appl 194: 878–895. https://doi.org/10.1007/s10957-022-02054-7 doi: 10.1007/s10957-022-02054-7

|

| [14] | Gilbert R (2006) Looking for Mr Schumpeter: Where are we in the competition-innovation debate?. in J. Lerner and S. Stern (eds), Innov Policy Econ NBER, MIT Press. https://doi.org/10.1086/ipe.6.25056183 |

| [15] |

Harris C, Vickers J (1995) Innovation and natural resources: A dynamic game with uncertainty. RAND J Econ 26: 418–430. https://doi.org/10.2307/2555996 doi: 10.2307/2555996

|

| [16] | Hausman JA (1981) Exact consumer's surplus and deadweight loss Am Econ Rev 71: 662–476. |

| [17] |

Hoel M (1978) Resource extraction, substitute production, and monopoly. J Econ Theory 19: 28–77. https://doi.org/10.1016/0022-0531(78)90053-4 doi: 10.1016/0022-0531(78)90053-4

|

| [18] |

Hoel M (1983) Monopoly resource extractions under the presence of predetermined substitute production. J Econ Theory 30: 201–212. https://doi.org/10.1016/0022-0531(83)90102-3 doi: 10.1016/0022-0531(83)90102-3

|

| [19] |

Lambertini L (2010) Oligopoly with hyperbolic demand: A differential game approach. J Optimiz Theory Appl 145: 108–119. https://doi.org/10.1007/s10957-009-9627-z doi: 10.1007/s10957-009-9627-z

|

| [20] | Lambertini L (2013) Oligopoly, the Environment and Natural Resources, London, Routledge. |

| [21] |

Lambertini L (2014) Exploration for nonrenewable resources in a dynamic oligopoly: An Arrovian result. Int Game Theory Rev 16: 1–11. https://doi.org/10.2139/ssrn.2197196 doi: 10.2139/ssrn.2197196

|

| [22] |

Loury G (1986) A Theory of 'Oil'igopoly: Cournot equilibrium in exhaustible resource market with fixed supplies. Int Econ Rev 27: 285–301. https://doi.org/10.2307/2526505 doi: 10.2307/2526505

|

| [23] |

Mohr E (1988) Appropriation of common access natural resources through exploration: The relevance of the open-loop concept. Int Econ Rev 29: 307–320. https://doi.org/10.2307/2526668 doi: 10.2307/2526668

|

| [24] |

Olsen TE (1988) Strategic considerations in invention and innovation: The case of natural resources revisited. Econometrica 56: 841–849. https://doi.org/10.2307/1912701 doi: 10.2307/1912701

|

| [25] |

Peterson FM (1978) A model of mining and exploration for exhaustible resources. J Environ Stud Manag 5: 236–251. https://doi.org/10.1016/0095-0696(78)90011-6 doi: 10.1016/0095-0696(78)90011-6

|

| [26] |

Polasky S (1992) Do oil firms act as 'Oil'igopolists? J Environ Econ Manag 23: 216–247. https://doi.org/10.1016/0095-0696(92)90002-E doi: 10.1016/0095-0696(92)90002-E

|

| [27] |

Polasky S (1996) Exploration and extraction in a duopoly-exhaustible resource market. Can J Econ 29: 473–492. https://doi.org/10.2307/136300 doi: 10.2307/136300

|

| [28] | Quyen NV (1988) The optimal depletion and exploration of a nonrenewable resource. Econometrica 56: 1467–1471. |

| [29] |

Quyen NV (1991) Exhaustible resources: A theory of exploration. Rev Econ Stud 58: 777–789. https://doi.org/10.2307/2297832 doi: 10.2307/2297832

|

| [30] |

Reinganum J, Stokey N (1985) Oligopoly extraction of a common property resource: The importance of the period of commitment in dynamic games. Int Econ Rev 26: 161–173. https://doi.org/10.2307/2526532 doi: 10.2307/2526532

|

| [31] |

Reynolds SS (1987) Capacity investment, preemption and commitment in an infinite horizon model. Int Econ Rev 28: 69–88. https://doi.org/10.2307/2526860 doi: 10.2307/2526860

|

| [32] |

Salant S (1976) Exhaustible resources and industrial structure: A Nash-Cournot approach to the world oil market. J Polit Econ 84: 1079–1094. https://doi.org/10.1086/260497 doi: 10.1086/260497

|

| [33] | Schumpeter JA (1942) Capitalism, Socialism and Democracy, New York, Harper. |

| [34] | Tirole J (1988) The Theory of Industrial Organization, Cambridge, Mass, MIT Press. |

| [35] |

Varian HR (1982) The nonparametric approach to demand analysis.. Econometrica 50: 945–973. https://doi.org/10.2307/1912771 doi: 10.2307/1912771

|

Figures(3)

Gustav Feichtinger, Luca Lambertini, George Leitmann, Stefan Wrzaczek. Optimal drilling efforts and industry structure[J]. AIMS Environmental Science, 2024, 11(4): 610-627. doi: 10.3934/environsci.2024030

DownLoad:

DownLoad: